More technology = more need for board engagement

Technology is being adopted widely by businesses and consumers alike. Digital transformation that was underway in many organizations has moved forward at a rate few could have predicted in 2019:2 Furthermore, 85% of CEOs accelerated digital initiatives during the COVID-19 pandemic.3

Meanwhile, digital and advanced technologies, such as cloud and artificial intelligence (AI), are “rapidly and fundamentally changing what is possible for companies and how they compete,” a recent Deloitte Global article explains.4 “Innovations—often being advanced by the large cloud platforms—are building on each other to create business opportunities that, a few years ago, did not exist.”5

In 2022, worldwide IT spending is projected to total US$4.4 trillion, an increase of 4% from 2021,6 but end-user spending on public cloud services is forecast to grow 20.4% in 2022 to total US$494.7 billion,7 according to Gartner, Inc.

Meanwhile, cyberattacks over the past two years have proliferated around the world. In the United States, for example, the Identity Theft Resource Center’s latest annual report revealed that 2021 was a record-breaking year for the number of compromises.8

These developments beg two questions: 1) Have boards stepped up their engagement on technology concerns including cyber and investments? 2) Are boards being effective stewards, helping ensure that technology is supporting strategy, not the other way around? Rich Nanda, principal at Deloitte Consulting LLP, explains how boards should be operating in this environment: “The board’s role with respect to technology needs to be centered on the long-term future-proofing of competitiveness in an increasingly digital world. The board must help management strike the appropriate balance between near-term results and long-term growth and competitive advantage.”

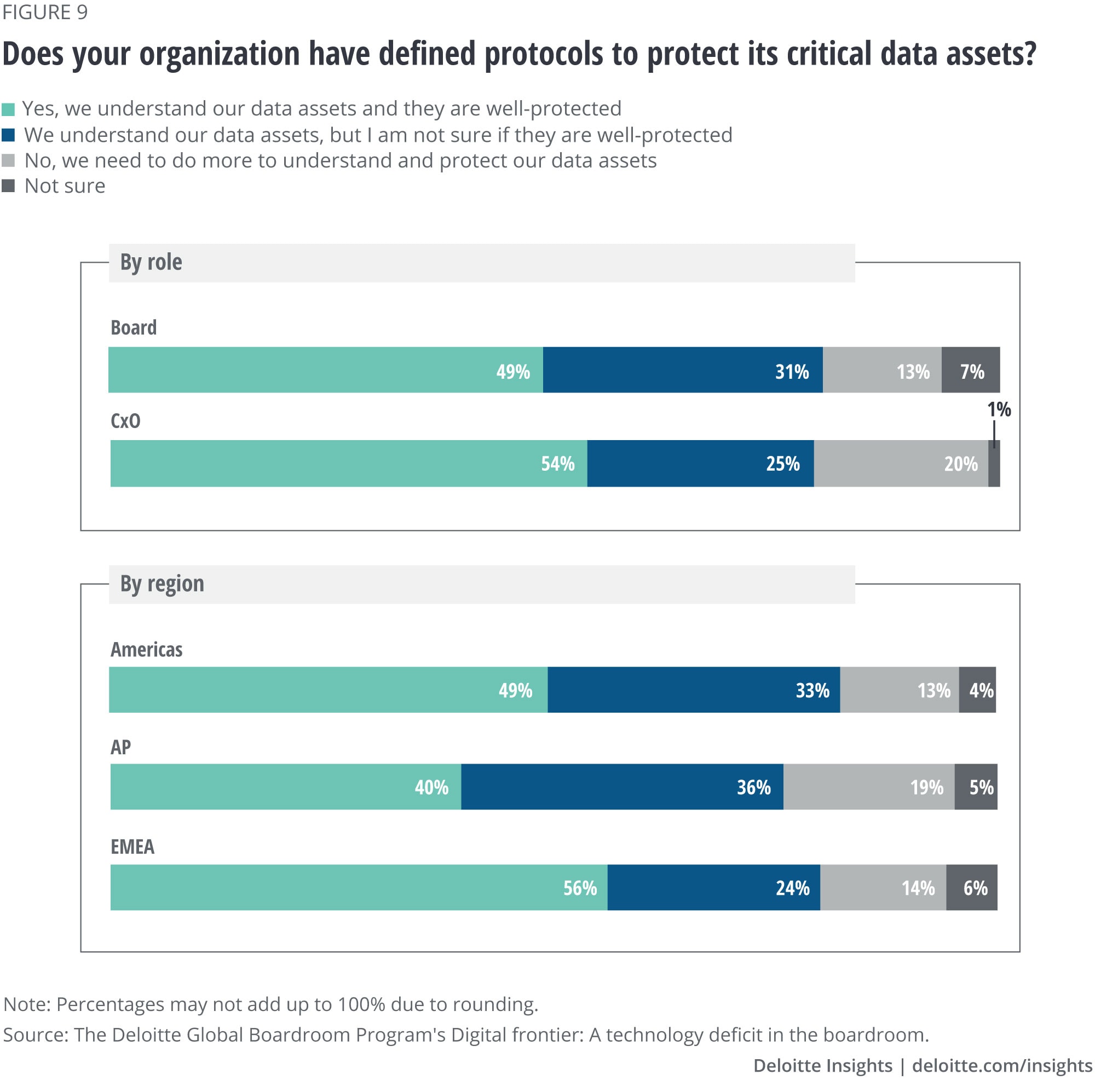

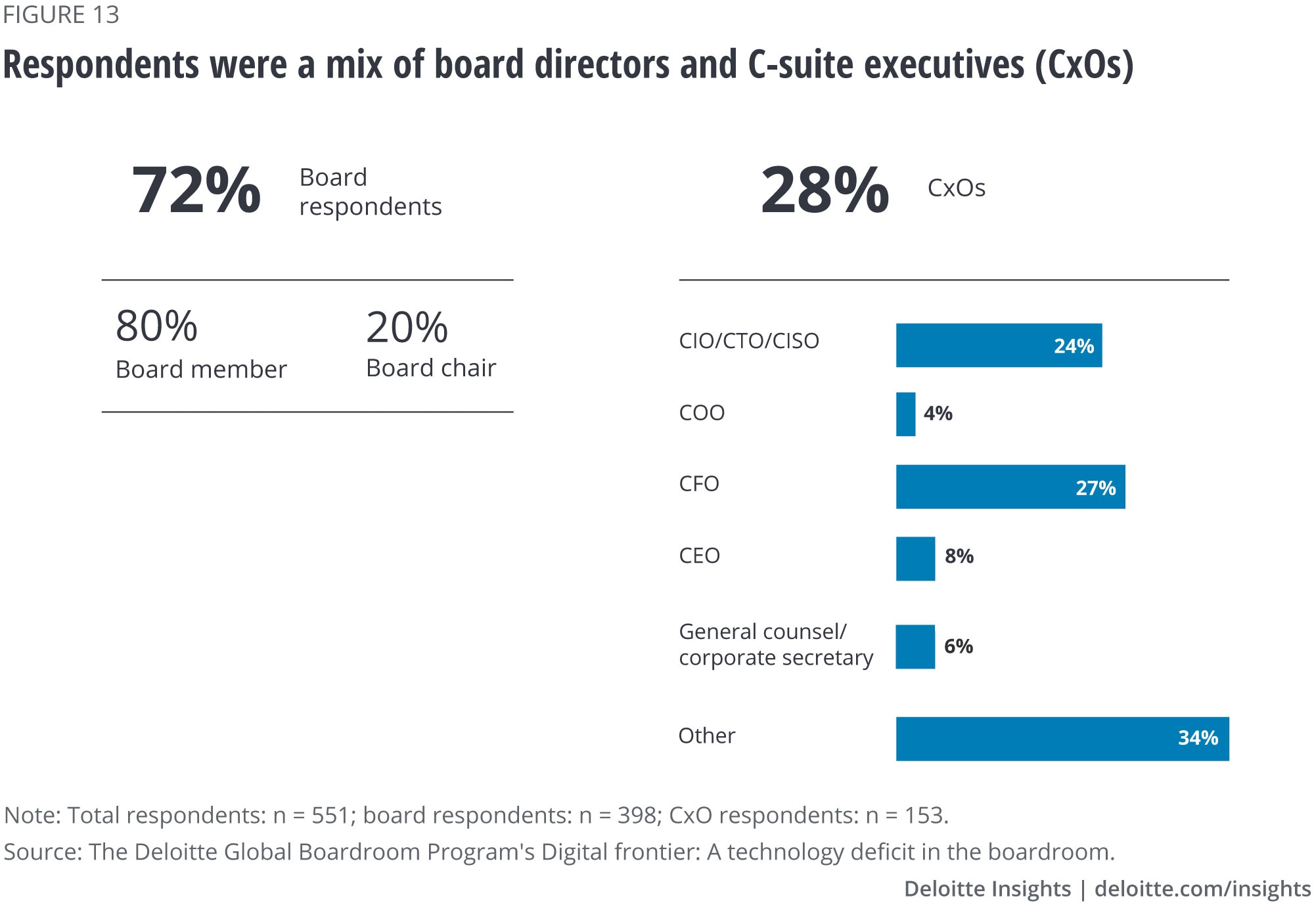

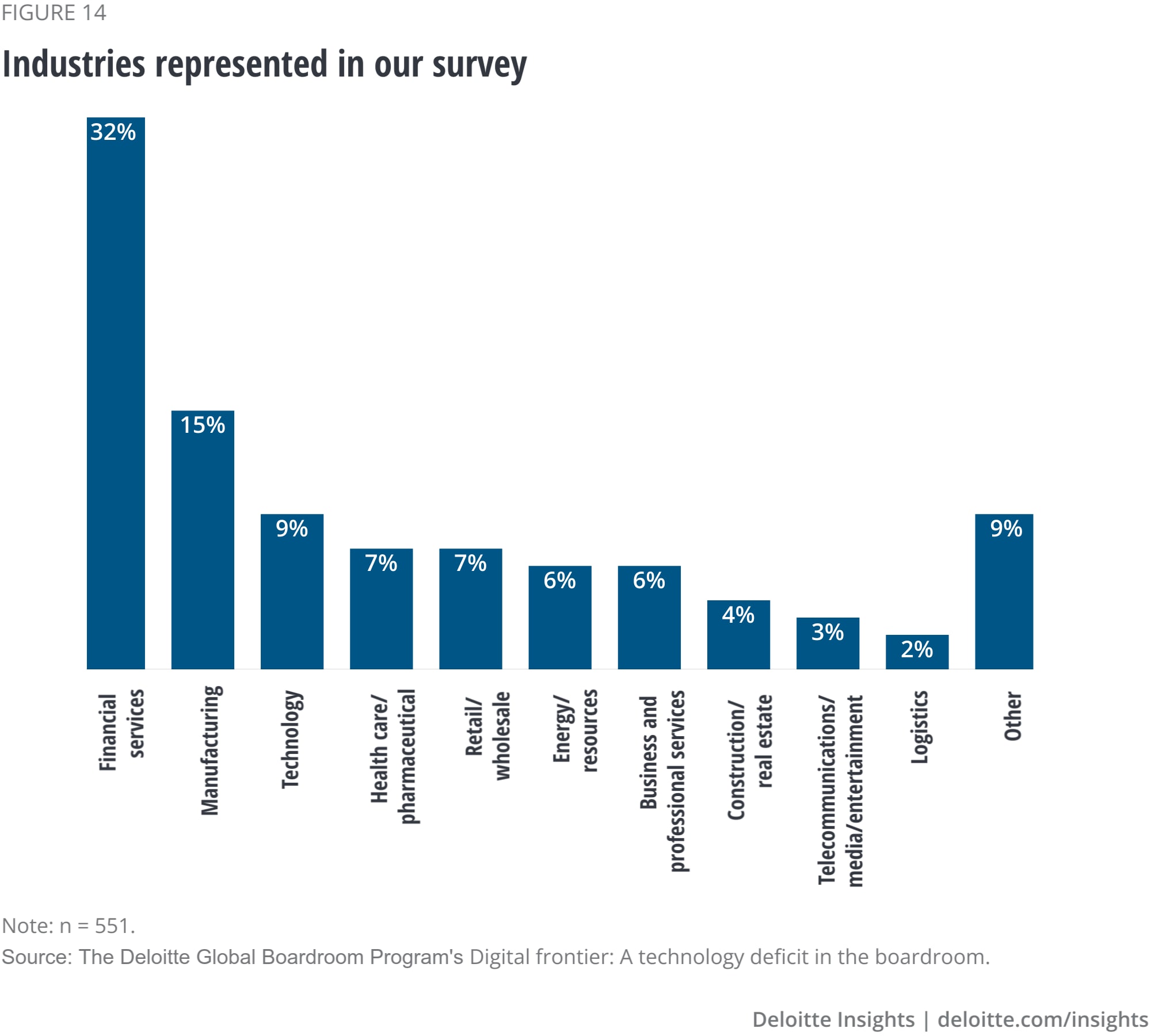

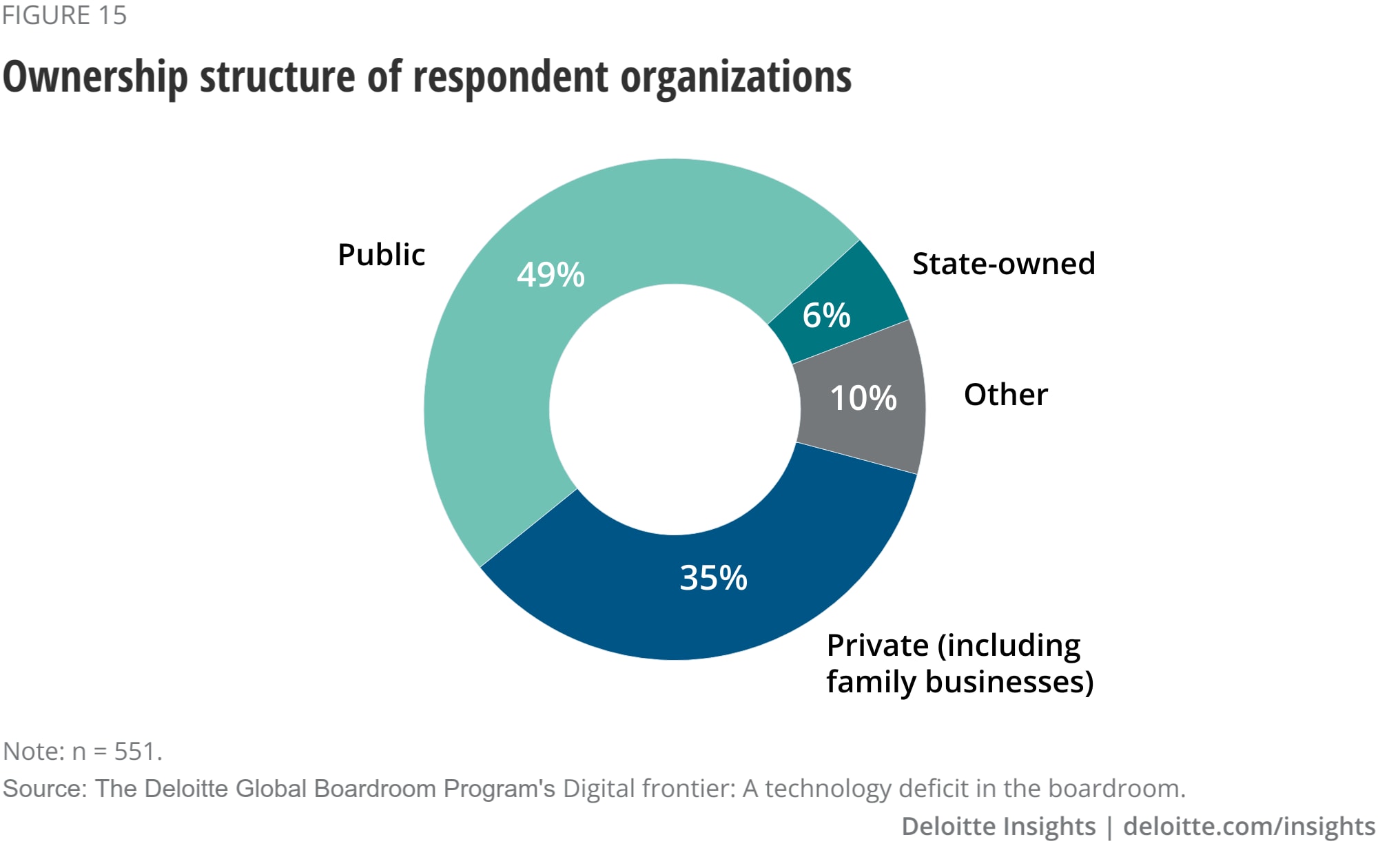

In early 2022, the Deloitte Global Boardroom Program surveyed hundreds of directors and C-suite executives (CxOs) from companies based in 55 countries to understand the degree of board engagement in technology today (see the appendix for information about the survey and its respondents). Overall, the survey revealed a gap between the growing demand for more tech understanding and engagement and what’s currently being provided by boards.

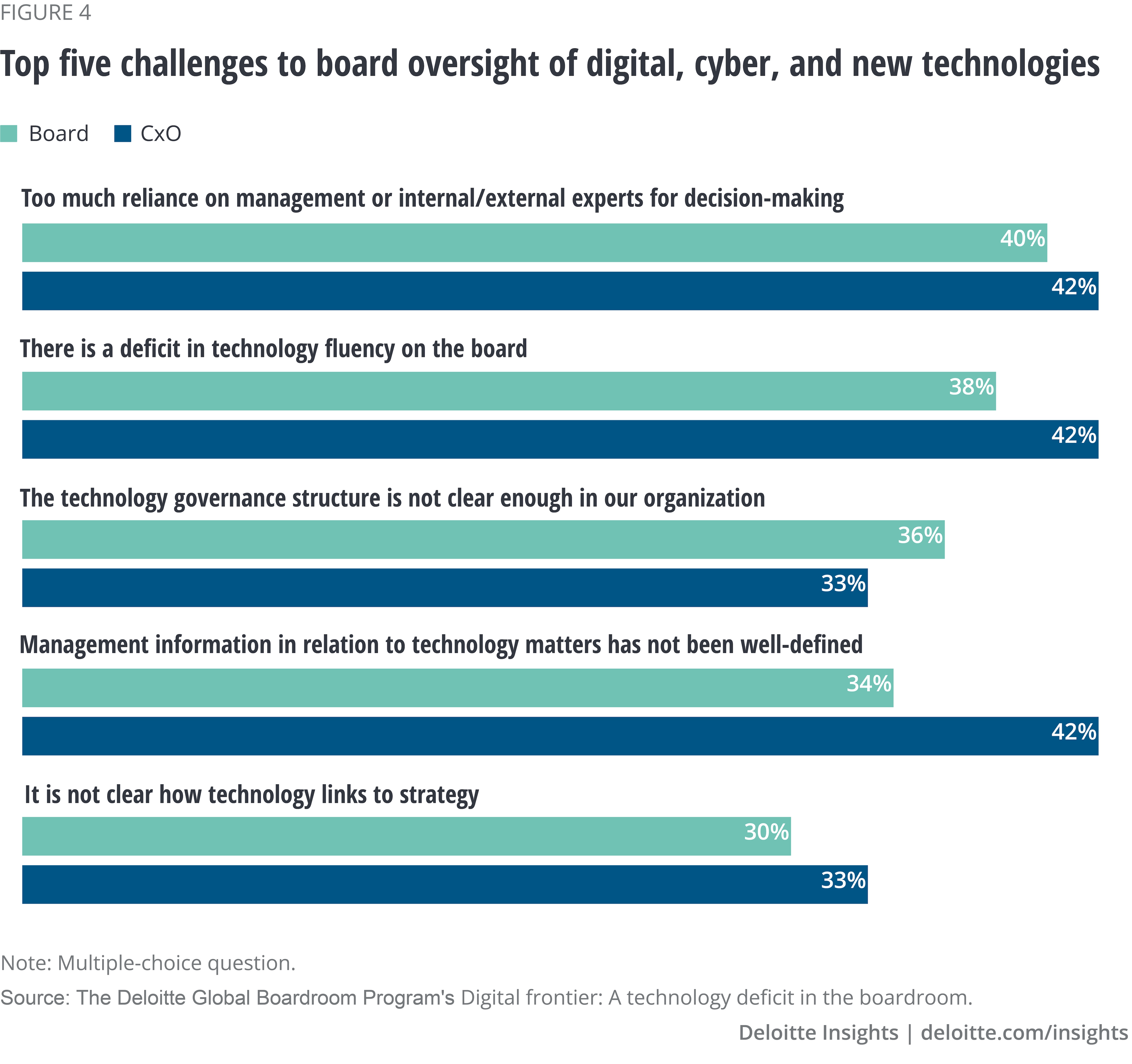

Scratching the surface: Perceptions may be deceptively optimistic

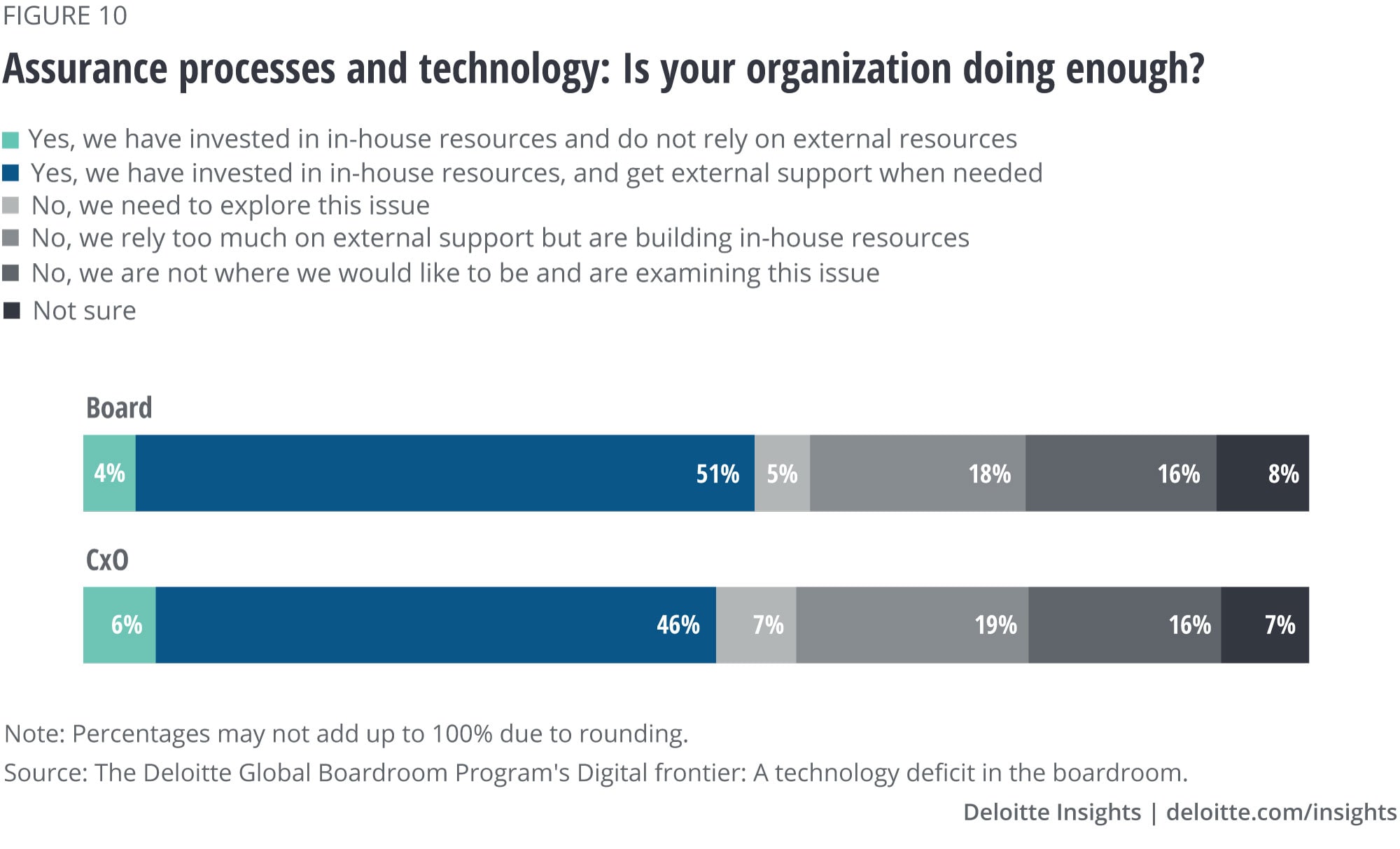

Most directors in the Deloitte Global Boardroom Program's survey feel good about the level of their engagement with tech issues: Over 80% of directors were at least somewhat confident in their ability to understand, review, and challenge the technology strategy and agenda at their organizations. Among those, nearly half say their boards rely on support from the executive/management team or an external specialist to steer the technology agenda; one in four say either a committee or a specialist board member steers the agenda, with just one in 10 saying the board handles it capably on its own. As for the one-fifth of directors who see room for improvement, most say their board “is wholly dependent” upon the executive team and some feel the board needs to develop a plan to improve its ability to provide effective engagement.

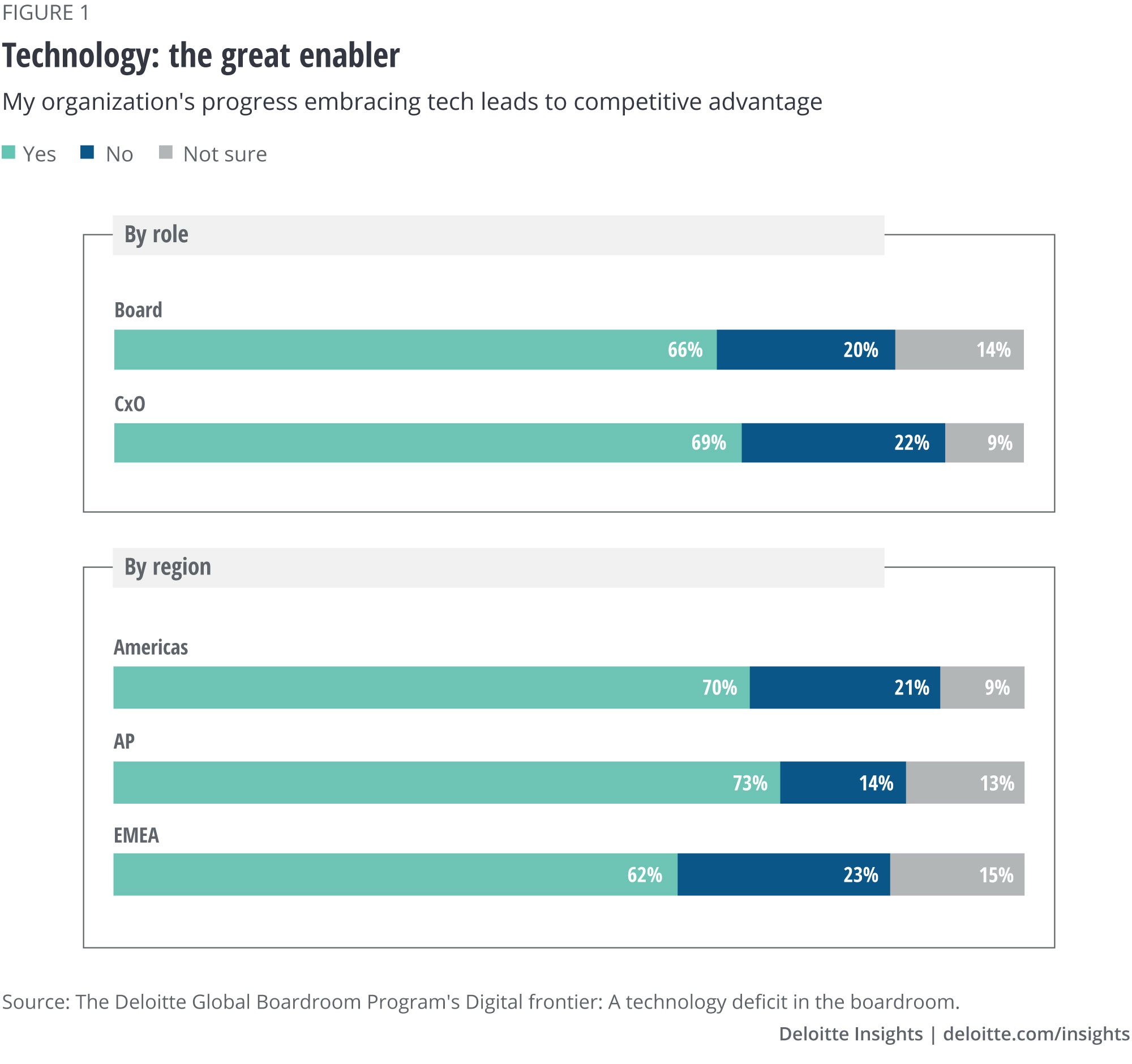

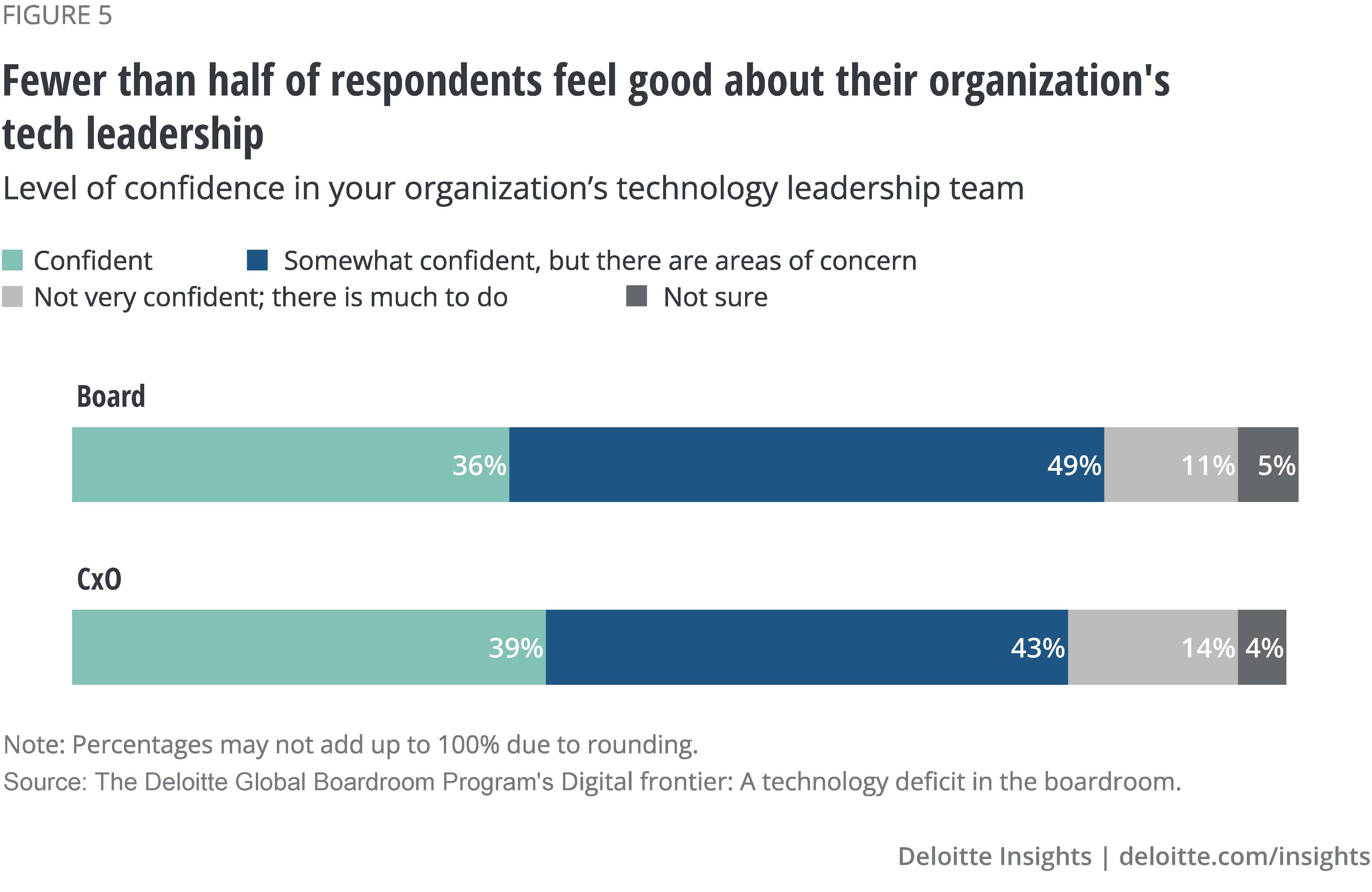

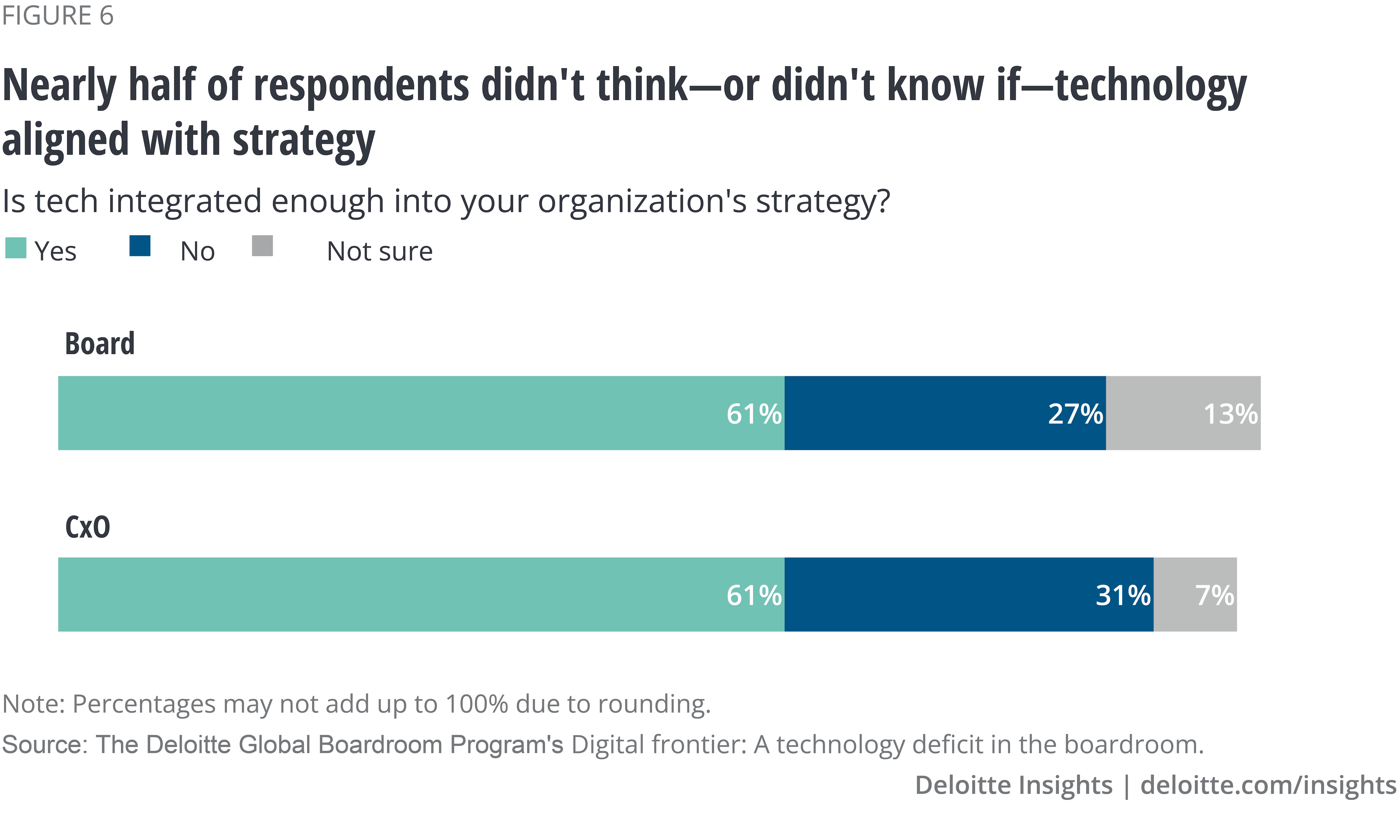

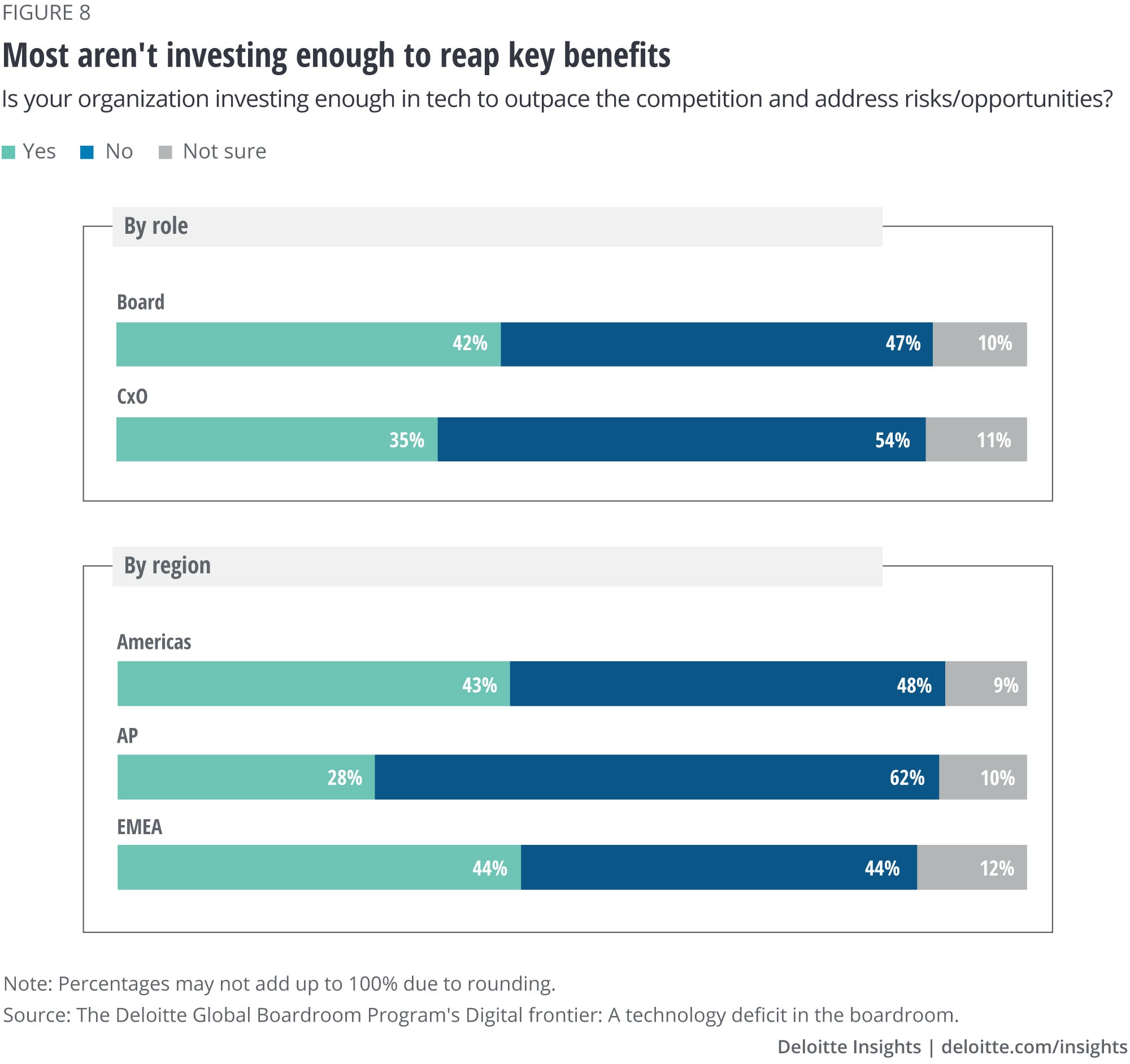

When asked how they feel about their company’s progress in embracing technology to achieve competitive advantage, most—two-thirds of respondents overall—were optimistic (figure 1).

It’s possible, however, that this optimism could be an example of a cognitive bias known as the Dunning-Kruger effect—where not knowing what you don’t know yields a false sense of security and overestimating your own ability.9 Boards need to be vigilant and self-critical in fast-changing areas. Read on …

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}