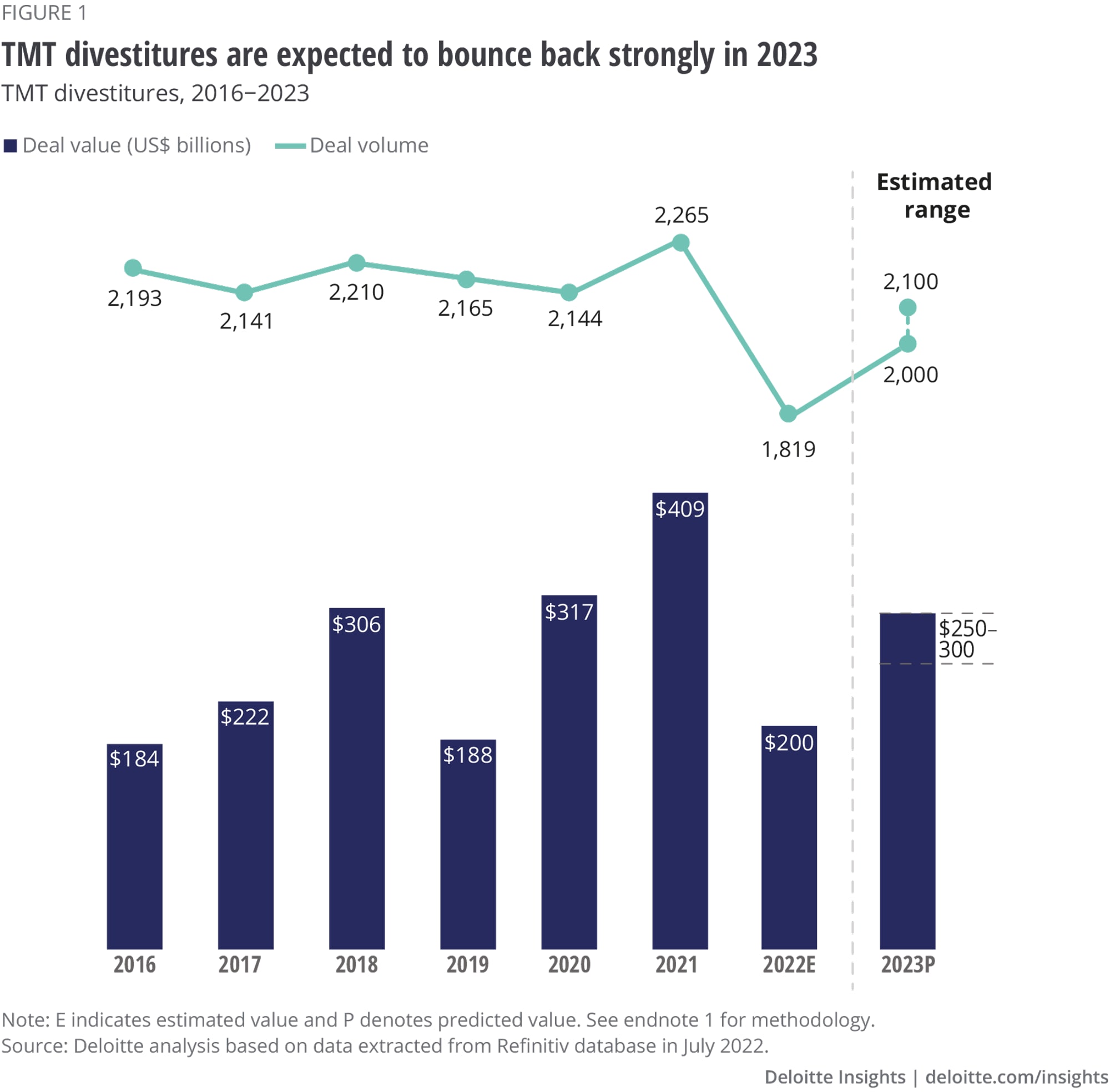

We expect the recovery in TMT divestiture transactions will probably begin sometime in mid-2023, driven by several converging factors. Macroeconomic uncertainties and business disruptions may prompt companies to reassess their strategic business assets—including which ones it makes sense to hold onto.3 Additionally, activist investors are likely to press for divestitures soon, as a variety of challenges have led to disappointing earnings and falling share prices.4 Private equity investors (PEs) and select venture capital firms (VCs)5 may become more aggressive buyers by mid-2023 as they see more stable fund flows and highly attractive valuations compared to late 2021.

TMT executives are looking to divestitures to accomplish a variety of goals. Some are aiming to sharpen one or both entities’ focus on their core business;6 others want to unlock value from specific investments and assets;7 and some are doing both as part of their portfolio recalibration efforts. All of these goals will likely involve offloading noncore business divisions, suggesting that the growth in 2023’s deal activity will begin with an increase in the number of such niche, small-size transactions, with deal value following. Additionally, companies planning mega-mergers need to comply with regulations that mandate divesting certain assets before the mergers are approved.

As exit options, we expect corporate IPOs and especially SPAC-led deals to further weaken over the next 12–18 months due to higher valuations and rising interest rates. Given the muted IPO scene, we expect PE buyers to be more active in acquiring divested assets than strategic corporate buyers. PE firms are flush with record amounts of dry powder, and they will use it to chase select assets that they believe will yield higher ROI.8 Sellers should prime the assets that they intend to sell off, as the market is less likely to simply “take over” assets available for sale.

In the technology sector, noncore assets, specialized software businesses that have the potential to scale, and financially struggling divisions with proven business models will be attractive candidates for both sellers and buyers.9 Large, diversified semiconductor and electronics companies will likely continue to spin off select fab operations and facilities to focus on the core and preserve margins.10 From the buyers’ standpoint, PE investors can take advantage of the public funding announced by several governments, and could consider co-investing with interested chip companies to acquire fab operations that get spun off. Deal activity may be further accelerated by regulators potentially forcing some larger tech companies to divest for anti-trust concerns.

Meanwhile, the media-telecom convergence trend seems to be slowing down, with some major telcos starting to look at prospective buyers for their media assets—especially, film and TV businesses—which could prompt de-mergers. But a more prominent driver behind many media and entertainment divestitures is digitization and consumer behavior. Consumers continue to change how they consume content as well as their spending on telecom, media, and entertainment services. Ongoing streaming wars and personal financial constraints are leading consumers to reduce their number of subscriptions: Deloitte’s 2022 Digital Media Trends study found that almost 50% of US consumers felt that they pay too much for streaming video services, driving one in three to plan to cut back.11 Further, they are making very specific choices about what content and services they want to spend their money on.12 For media and entertainment majors and conglomerates offering content, broadcasting, connectivity, and entertainment, these consumer trends may prompt them to shed parts of their operations, not only to focus on their core business, but also to strengthen their financial position.

Deloitte’s 2022 Charting New Horizons M&A report suggests that telecom companies may deploy a range of defensive M&A strategies to safeguard their core businesses. For instance, they could continue to sell off select nonstrategic assets as part of a defensive strategy.13 Telecom tower and infrastructure companies as well as mobile broadband service providers may seek to sell noncore assets such as media services and large data centers to invest more in high-growth areas and initiatives such as 5G, fixed wireless access, or edge computing.

{kind=link}