The paradox of flows: Can hope flow from fear? has been saved

The paradox of flows: Can hope flow from fear? 2016 Shift Index

14 December 2016

John Hagel III United States

John Hagel III United States John Seely Brown (JSB) United States

John Seely Brown (JSB) United States Maggie Wooll United States

Maggie Wooll United States Andrew de Maar United States

Andrew de Maar United States

Society today seems consumed by uncertainty, insecurity, and anxiety, as models and expectations about how the world works have come into question. But our analysis shows long-term business trends remaining both stable and predictable, notwithstanding society’s understandable disorientation.

Overview: A year of change

Learn More

View the related infographic

Explore the Shift Index Series

Subscribe to receive updates from the Center for the Edge

The year 2016: It feels unprecedented, historic—a year that seemed destined to make clear, in ways that no series of charts ever could, that the world is changing, has changed, will continue to change. Events both global and local highlighted disparities in income and opportunity, skills and future prospects, and a widening gap between geographic regions with vibrant economies and others struggling with industries in transition, and we watched it all play out on a 24/7, always-connected, virtual stage.

We are left with a sense of unease. It seems apparent that the American public, broadly, was gripped by a deep anxiety this year, manifesting as fear or pessimism or cynicism. This national anxiety led to results that confounded experts, broke models, and defied expectations. Time and again, 2016 has reminded us that our ability to understand and adapt has failed to keep pace with the speed of change in the world around us—socially and commercially—just as our ability to process and evaluate information has not kept up with the speed at which it is created, disseminated, and consumed. Even as some organizations and political candidates made appeals to the past, the very way these appeals played out made clear that the world in which we live is changing, and the models and expectations we have about how the world works may no longer hold.

Why? Much has been made of an apparent turn in the national temperament. Demographics have been sliced and diced, with explanations and counter-explanations that fit some story we tell ourselves. The same themes pervaded, yet our perceptions of them seemed to vary wildly. What preoccupied our collective imagination? Fairness, opportunity, the future, a need for change, and a fear of change already upon us. What are those changes? They are myriad. Many of the most profound are universal and long-term.

The Shift Index is our attempt to quantify and make sense of the changes we see in the world around us, primarily through the lens of business.

The index (see sidebar “The Shift Index” for further definition) measures long-term trends across three categories: Foundations, Flows, and Impact. These broad trends have been building for decades, yet they don’t affect all industries or regions equally or at the same time. Some are just reaching an inflection point at which the effects are difficult to ignore. In particular, we’re beginning to feel the cumulative effects of technological advances and demographic changes that are starting to turn up the steep part of an exponential curve. It can be disorienting.

Overall, this year’s index reflects the durability and stability of the trends we have reported on previously. Despite the feeling of great upheaval, these indices have been fairly consistent and predictable over a period of decades.

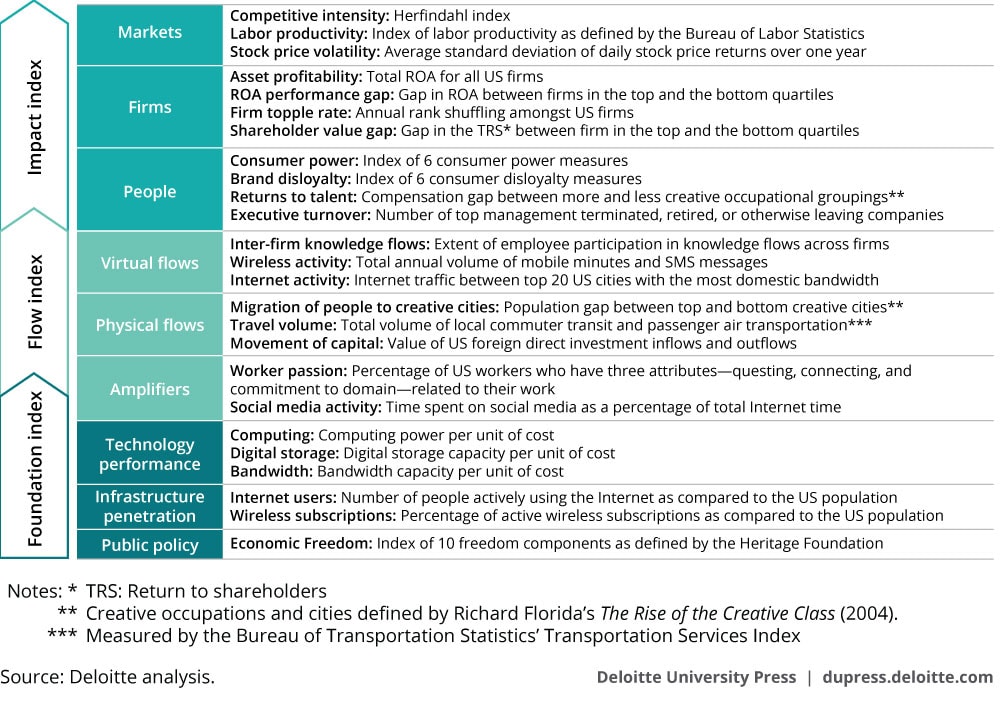

The Shift Index

We developed the Shift Index to help executives understand and take advantage of the long-term forces of change shaping the US economy. First released in 2009 and updated annually, the Shift Index tracks 25 metrics across more than 45 years, providing a comprehensive view of underlying forces not captured by short-term economic indicators. These metrics, and the relative rates of change between them, highlight the evolution and impact of long-term trends in technology and public policy.

The Shift Index metrics are divided into three indices that measure the waves of change in what we call the Big Shift in the global business environment:

- The “Foundation” index tracks advances in the digital technology infrastructure and public policy that catalyze changes in the business landscape. Trends in the Foundation metrics have systematically reduced barriers to entry and movement.

- The “Flow” index looks at the flows of knowledge, capital, and talent—key drivers of performance enabled by the Foundation—as well as at the amplifiers of these flows. Flow metrics tend to lag Foundation metrics because of the time required to understand and develop new practices consistent with advances in the foundation.

- The “Impact” index captures the effects that long-term trends have on competition, volatility, and performance across industries. Impact metrics will change as firms begin to figure out how to participate in and harness the knowledge, capital, and talent flows across institutional and geographic boundaries.

See the Appendix for the updated Shift Index metrics.

For more information, please go to www.deloitte.com/us/shiftindex.

The world of the Big Shift demands resilience and emphasizes learning over predictability and the status quo, scalable learning rather than scalable efficiency, and participating effectively in knowledge flows within and across companies. The findings of the 2016 Shift Index suggest that companies and individuals are increasingly willing to participate in knowledge flows but still learning how to understand and harness them.

Mounting pressures, narrowing focus

Paradoxically, despite the stability and predictability of these long-term trends, the world around us seems consumed by a pervasive sense of uncertainty, insecurity, and resultant fear. This effect occurs somewhat independently of whether something is actually happening. For example, nothing in the Impact Index departs from the trends we have seen over the past decade, but there seems to be more of a sense of insecurity that isn’t directly connected to whether an individual’s company has declining performance or whether volatility has buffeted that individual’s stock portfolio.

Paradoxically, despite the stability and predictability of these long-term trends, the world around us seems consumed by a pervasive sense of uncertainty, insecurity, and resultant fear. This effect occurs somewhat independently of whether something is actually happening. For example, nothing in the Impact Index departs from the trends we have seen over the past decade, but there seems to be more of a sense of insecurity that isn’t directly connected to whether an individual’s company has declining performance or whether volatility has buffeted that individual’s stock portfolio.

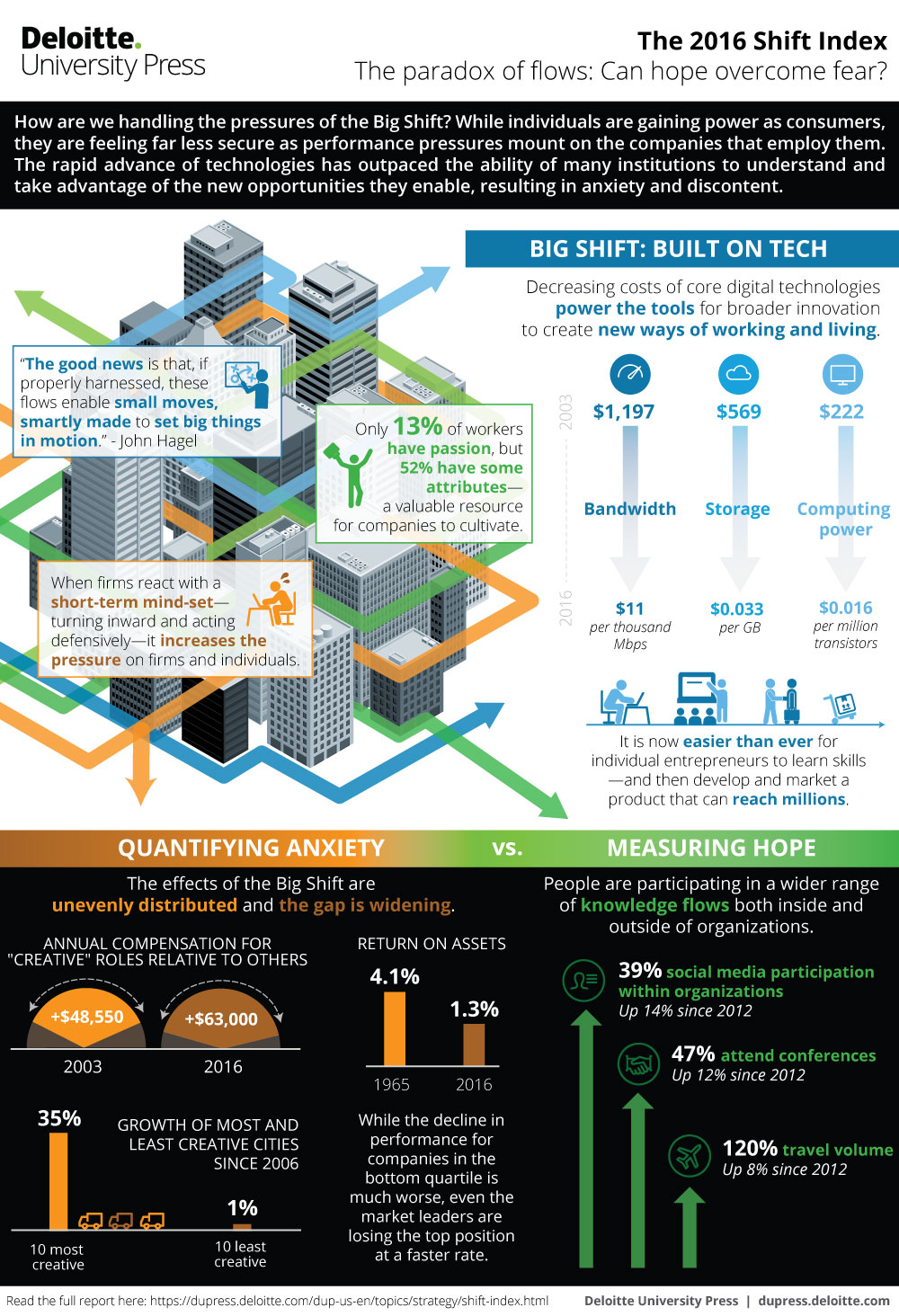

At the same time, the pressure is increasing as the effects of the Big Shift begin to accumulate. As digital technologies increasingly permeate all areas of our lives and reach all corners of our country, the positive and negative impacts of the Big Shift on business and society become more difficult to ignore. As Tom Friedman points out in his new book Thank You for Being Late, our ability (as humans or society) to adapt tends to follow a linear path, while the technological foundations are changing exponentially. The exponential curve gets only steeper when you consider the convergence of multiple, exponentially advancing building blocks (computing, storage, and bandwidth) into technologies such as cloud computing, biosynthesis, and 3D printing, and the self-reinforcing cycles of innovation that follow.1 The resulting gap causes real economic dislocation in addition to a more general disorientation and anxiety.

Companies and individuals aren’t necessarily benefiting from the technology and policy trends. In fact, the Impact index shows that although labor productivity continues to increase, firm performance, as measured by ROA, continues to decline economy-wide, especially for companies in the bottom quartile. There is real stress. Indeed, with electronic trading algorithms instantaneously reacting to ever larger flows of real-time data, both quantitative and sentiment- and headline-based, stock market volatility is ticking upward again after declining from the 2008 peak. Companies face mounting performance pressures; so do workers.

There’s a paradox here. In one part of our lives, as consumers, the Big Shift is giving us much more power; in another part of our lives, as workers, we are facing increasing performance pressure. Consumer power remains high in many categories, as does brand disloyalty. But consumer power matters only if you have money to spend, and awareness that employers might be facing significant performance challenges further fuels widespread anxiety.

This pressure leads to a narrower focus, causing many institutions and individuals to home in on isolated components and miss the broader picture of the Big Shift. Consider issues such as trade, globalization, and job losses: Most of the discussion fails to consider them as they are today within the context of the broader changes represented by the Big Shift. Friedman describes it as a “new era of globalization,” one that is defined by interconnection and companies and individuals participating in global flows.2 The mounting performance pressures can cause us to lose sight of the Big Shift and narrow our focus to more tangible components that seem easier to address through a specific policy or strategy. However, trade is only one of the forces creating and intensifying pressure. Focusing just on trade, or just on jobs, can’t help but fail to address the more complex web of flows that are reshaping our economic and social systems. Crafting effective solutions that will create new opportunity and drive higher levels of performance requires understanding the broader picture of the Big Shift.

Increasing flows hold potential, if we learn to use them

We believe part of the answer can be found in the Flow Index. Increasing volumes and speeds of flows—of information, people, and money—and greater participation in these flows create an environment full of potential opportunity. However, in the short term, these flows also increase our awareness of both an increasing pace of change and the disparity in outcomes in advance of our ability to understand and make sense of them. The natural human reaction is to feel more uncertain, fearful, and anxious. On the one hand, as more data is opened up and reported on, we have greater visibility into how our institutions are functioning. On the other, it becomes more apparent to the public that our institutions are adapting too slowly to the changing environment and the changing needs of individuals and society. The reported broad decline in trust in our institutions—according to Gallup, only 32 percent of Americans report having confidence in key US institutions, continuing a downward trend that began in 2004,3 while Edelman’s trust barometer finds that only 41 percent of Americans trust government to keep pace with change4—reflects that anxiety.

We believe part of the answer can be found in the Flow Index. Increasing volumes and speeds of flows—of information, people, and money—and greater participation in these flows create an environment full of potential opportunity. However, in the short term, these flows also increase our awareness of both an increasing pace of change and the disparity in outcomes in advance of our ability to understand and make sense of them. The natural human reaction is to feel more uncertain, fearful, and anxious. On the one hand, as more data is opened up and reported on, we have greater visibility into how our institutions are functioning. On the other, it becomes more apparent to the public that our institutions are adapting too slowly to the changing environment and the changing needs of individuals and society. The reported broad decline in trust in our institutions—according to Gallup, only 32 percent of Americans report having confidence in key US institutions, continuing a downward trend that began in 2004,3 while Edelman’s trust barometer finds that only 41 percent of Americans trust government to keep pace with change4—reflects that anxiety.

In this year’s Shift Index, we see continued evidence of increasing flows. The Flow Index looks at the flow of knowledge, capital, and talent—as well as amplifiers of these component flows—enabled by advances in the digital infrastructure and a general trend toward public policy liberalization. Flow metrics tend to lag the foundational advances because flows reflect the process of understanding and developing new practices consistent with foundational changes.

- The Interfirm Knowledge Flows indicate employee participation in knowledge flows is starting to increase significantly, as more workers participate, and participate more frequently, in various forms of knowledge flows between companies. The technology, professional services, consumer products, and telecommunications industries lead the way with increased participation in knowledge flows (see the appendix for further explanation of these and other Shift Index metrics). As we’ll discuss, we expect an absolute increase in the Flow Index, though the impact and implications of the increase depend on the type and diversity of the flows.

- Wireless activity is increasing as SMS has dipped as a result of alternative ways to connect; Internet activity continues to grow exponentially. Time spent on social media on personal computers is down to 14 percent from a high of 17 percent in 2011, but time spent on social media across all platforms continues to grow. Globally, social network users grew 9 percent in 2015, accounting for over 65 percent of all Internet users.5

- Migration to creative cities continues, widening the gap between population growth in the cities at the top of the creative list and those at the bottom. In 2015, the rate of population growth in the most creative cities was 34 percent higher than in the least creative cities, up from a gap of 24 percent in 2012. Growth in the least creative cities has declined with the population of those cities only slightly higher (less than 1 percent) than it was in 1990.

Flows are increasing; now, how can we make that productive? If the goal of expanding flows within our society and economy is to accelerate learning rather than to simply expand data flows, we might create a more useful framework for optimizing both flows and friction. What kinds of flows are generative, meaning that they promulgate even more productive flows over time? What kind of friction gives us opportunity for reflection and productive debate so that we can learn faster and come up with even more creative ideas and approaches over time?

First, we should consider the roles of both flows that happen in the physical world—of people, resources, or ideas—and flows that happen in the virtual world of the Internet: data, information, and ideas. One important finding of the Shift Index over the past decade has been that the Internet (and increases in virtual flows) is not replacing the need for physical flows via face-to-face interaction. Instead, virtual flows tend to reinforce and amplify face-to-face interactions.

One place we see this is in the Interfirm Knowledge Flows metric, in which online forums and social media have become more popular at work but so have face-to-face lunch meetings and conferences. This can also be seen in the continued growth in travel volume, which has climbed steadily, including 8.5 percent in the past five years, despite the parallel development of increasingly rich and accessible means for virtual communication and collaboration. While not a comprehensive indicator of the total volume of face-to-face interactions, it is interesting that the trade show and conference planning industry has reported 2.7 percent annual growth over the past five years.6

Face-to-face interactions have the potential to accelerate learning by bringing individuals into contact with people and ideas they might not otherwise encounter or in an experience or context that isn’t easily replicated virtually. Although multidisciplinary gatherings such as SxSW, TED, and the Aspen Ideas Festival occupy familiar convention-center settings, they expand the scope beyond simple marketing or networking. These multidisciplinary events bring attendees into contact with more diverse flows, from adjacent and even seemingly unrelated domains. Attendees have the opportunity to share ideas and make more diverse connections that can yield insights and potential collaborators. Attendance at SxSW has increased 53 percent over the past five years (to 37,660), and mega-events such as the International Consumer Electronics Show draw up to 150,000 attendees from across a spectrum of industries and disciplines. Virtual flows, such as online forums, social media platforms, and messaging apps, can help make these large events more productive, allowing exhibitors and attendees to connect and engage with each other before, during, and after the events and continue to participate in more diverse flows that reinforce and amplify the face-to-face learning. On the other end of the spectrum, numerous smaller-scale, in-person convenings—from Meetups for women coding enthusiasts to kids’ health hackathons to summits that mobilize makers or digital storytellers for the greater public interest7—are made possible by social media and other technologies that make it easier to organize, publicize, and mobilize.

There is a quality to flows individually and in aggregate. The value of flows in the Big Shift is dependent upon both having access to diverse types of flows and having diverse participants or sources of information within those flows. Lack of diversity can reinforce mistaken beliefs and make it much more difficult to adapt to changing circumstances. Thus, companies can increase exposure to flows by participating in industry consortiums. However, if all of the consortium members are large companies in the same industry, the learning to come from that flow may be limited, both by lack of diversity and unwillingness to share learning and create new knowledge with competitors. Similarly, at the individual level, social media can have a “filter bubble” effect of allowing people to self-select into echo chambers that tend to reinforce existing beliefs rather than broaden exposure to new ideas and insights.8 For individuals, this heightens our sense of fear and threat and limits our exposure to diverse, productive flows.

Companies and individuals alike can fall prey to comparing their own experiences and performance against a self-selected group of peers that can obscure a widening gap between their approach, performance, and expectations relative to others not in their defined group. The old problem of “not knowing what it is you don’t know” has not gone away in the age of increasing flows enabled by the Internet. It may in fact be greater now than ever, as a result of the accelerating pace of change and the sheer volume of data and information available.

The “migration to creative cities” metric highlights the importance of face-to-face interactions and the role of diversity in productive, generative flows. While growth among the cities ranked as least creative has declined, the most creative cities have grown, on average, 35 percent relative to 1990 populations. This despite the fact that, with the help of digital technology infrastructures and new employment models, individuals can theoretically access work opportunities from anywhere with a good broadband connection, and, in most parts of the United States, individuals all have access to the same brand-name goods and entertainment. Many of the “creative” cities suffer from higher costs of living but also have more vibrant and resilient economies. Physical surroundings and face-to-face interactions still matter, fostering new connections and insights and exposing us to a wider variety of serendipitous flows and opportunities that we would never experience if not for proximity. More and more people appear to intuitively understand that they will learn faster and improve their performance more rapidly if they are physically present in a densely populated creative city. They are willing to experience significant personal disruption as they move from a familiar location to a new city and to accept a higher cost of living in return for the perceived benefits that can help them cope with mounting performance pressure. The unfortunate byproduct of increased migration to cities is to drain economic potential and vibrancy from the areas that are seeing a significant outflow, leaving them isolated from generative flows in such a way as to further widen the gap.

To move past fear to opportunity

The challenge is to move beyond fear and focus on the chance to use the flows of information, people, capital, and resources to create more opportunity for everyone. What are some of the opportunities that come from increasing participation in global flows?

For institutions, flows can be harnessed to anticipate and capture more opportunities in a rapidly changing business environment, to build deeper trust-based relationships with customers, and to create ecosystems that provide much greater leverage and flexibility in more effectively responding to the changing environment. It is especially important that institutions take a broader view of the many flows in which they might participate. Consider the way fitness trackers such as FitBit are evolving their products to gain an increasingly intimate view of the customer’s daily life through data flows. When Nike decided to create an accelerator for companies to design products around its Fuel technology rather than further develop the tracker itself, it found its way into another useful flow: the ideas and talent that can be harnessed to drive innovation in wearables technology and wellness applications. This is part of the reasoning that drives so many large corporations to open “innovation centers” in places such as the Bay Area. While they often cannot point to specific products or partnerships, these centers serve to keep their parent companies at least somewhat connected to flows of ideas and talent beyond their four walls. The ongoing and perplexing problem for institutions, of course, is whether participation in flows can be effectively translated into learning and performance improvement for the organization.

Brand-based companies can participate in flows to better understand their customers and to adjust and evolve their brand based on an ongoing dialogue. This isn’t entirely new. Back in 1993, when a Charles Barkley ad series9 ignited a controversial exchange about role models, Nike elected not to pull the ads and, as a result, was able to learn more about customers’ values by participating in the dialogue the ad series sparked. Red Bull is another company that has chosen to play almost exclusively in the flows by creating events and media centered around the activities and personalities about which its customers care. FirstBuild offers another example of how companies can think about participating in flows as a means of creating new opportunities: In this case, GE Appliance created a microfactory and community for crowdsourcing innovations in small appliances; the initiative allowed GE Appliance to participate in numerous flows that a large corporation would not typically be part of, including maker, inventor, and crowdfunding communities.

For individuals, the digital infrastructure now offers tools to scale impact as an individual or to mobilize a group. As we’ve written about previously,10 it is easier than ever for individual entrepreneurs to learn skills, develop, and market a product and reach millions of potential customers. Friedman calls this the increasing “power of one.” Just look at Joseph Garrett, the 23-year-old Brit whose onscreen Minecraft alter ego Stampy Cat has gained a following of more than 7 million YouTube subscribers.11 Or take the example of Michelle Phan, who began posting makeup how-to videos in 2007 and now has a lifestyle network, a beauty subscription service, and her own brand with a major cosmetics manufacturer.12 In a rapidly growing number of cases such as these, social media platforms enable a certain type of flow between producer and consumer that few larger companies have effectively leveraged but are powering young entrepreneurs who use them more instinctively. Individuals can also leverage flows to learn, find collaborators, and fine-tune their ideas.

It’s worth stating that mind-sets will likely have to shift before we can effectively get through this transitory period of anxiety and insecurity to embrace the possibilities of a world connected in the Big Shift. And as some of these forms of flow mature, we can learn to use them more effectively and consciously. In emotional terms, we have to move from fear of change and growing inequality to hope that more diverse flows can lead to greater prosperity for all.

Conclusion

We believe this is a transitory phenomenon—the double-edged sword of flow and the anxiety of broad and accelerating change. The natural human reaction to the greater visibility and awareness that comes from digitization and widespread connectivity, on a global scale and in real time, is fear. And there are real risks of what that fear could produce if it continues to grow over time. But over the longer term, these increasing flows present significant opportunities to mobilize people to use these technologies to change their institutions and embrace hope. The good news is that, properly harnessed, these flows enable small moves, smartly made, to set big things in motion. A challenge for all of us is to make these small moves quickly so we can provide more tangible evidence of the positive impact that can spark hope and diminish fear.

We believe this is a transitory phenomenon—the double-edged sword of flow and the anxiety of broad and accelerating change. The natural human reaction to the greater visibility and awareness that comes from digitization and widespread connectivity, on a global scale and in real time, is fear. And there are real risks of what that fear could produce if it continues to grow over time. But over the longer term, these increasing flows present significant opportunities to mobilize people to use these technologies to change their institutions and embrace hope. The good news is that, properly harnessed, these flows enable small moves, smartly made, to set big things in motion. A challenge for all of us is to make these small moves quickly so we can provide more tangible evidence of the positive impact that can spark hope and diminish fear.

At the Center for the Edge, we will continue to measure how these trends impact the future—and how individuals and institutions can best stage their bets and make low-cost, but transformational, moves. Our next journey will tackle a bigger question: In the context of the Big Shift, what would an institution redefined from the bottom up, with the goal of scalable learning, look like? Our future institutions may look very different from today’s, with faster learning and a renewed focus on our customers and ecosystems, all interacting to seize the opportunities that the Big Shift is creating.

Appendix: 2016 Shift Index metrics

The Shift Index consists of three sub-indices that measure the rate of change in today’s business environment: the Foundation index, the Flow index, and the Impact index. We are currently in the first wave of the Big Shift (measured by the Foundation index) and are still learning to embrace the second wave (captured in the Flow index).