2024 global insurance outlook

Insurers evolving to address changing operating environment and precipitate even greater societal impact

Article

•

34-min read

•

28 September 2023

•

Deloitte Center for Financial Services

Key messages

- Escalating frequency and severity of global risks—from climate change to cybercrime—is intensifying focus on the insurance industry’s capacity and readiness to react as society’s “financial safety nets.”

- Most insurers are realizing that reacting to risks may not be good enough and are undertaking transformation efforts aimed at preventing losses from happening in the first place.

- This shift to a more customer-centric business model will likely require advanced technology adoption and modification of company culture to help minimize siloed interactions, enhance collaboration among employees, and increase accessibility of customer data—but skill sets may need to be augmented.

- Merger and acquisition (M&A) activity has been on a decline since Q2 2022 due mainly to macroeconomic factors. However, as increases in interest rates and inflation ease, pent-up activity may drive an upsurge in deals later in 2023 into 2024. Insurance technology companies (InsurTechs) remain front and center of acquisition activity as carriers increasingly look to these capabilities for point solutions across the value chain to power transformation efforts.

- A fundamental mission underlying much of this change is that the industry’s role is pivoting to that of a sustainability ambassador, influencing and propelling purpose-driven decisions and strategies of clients across industries to create a better workplace, marketplace, and society.

Learn more

Insurers are transforming to achieve customer-centricity and elevate purpose

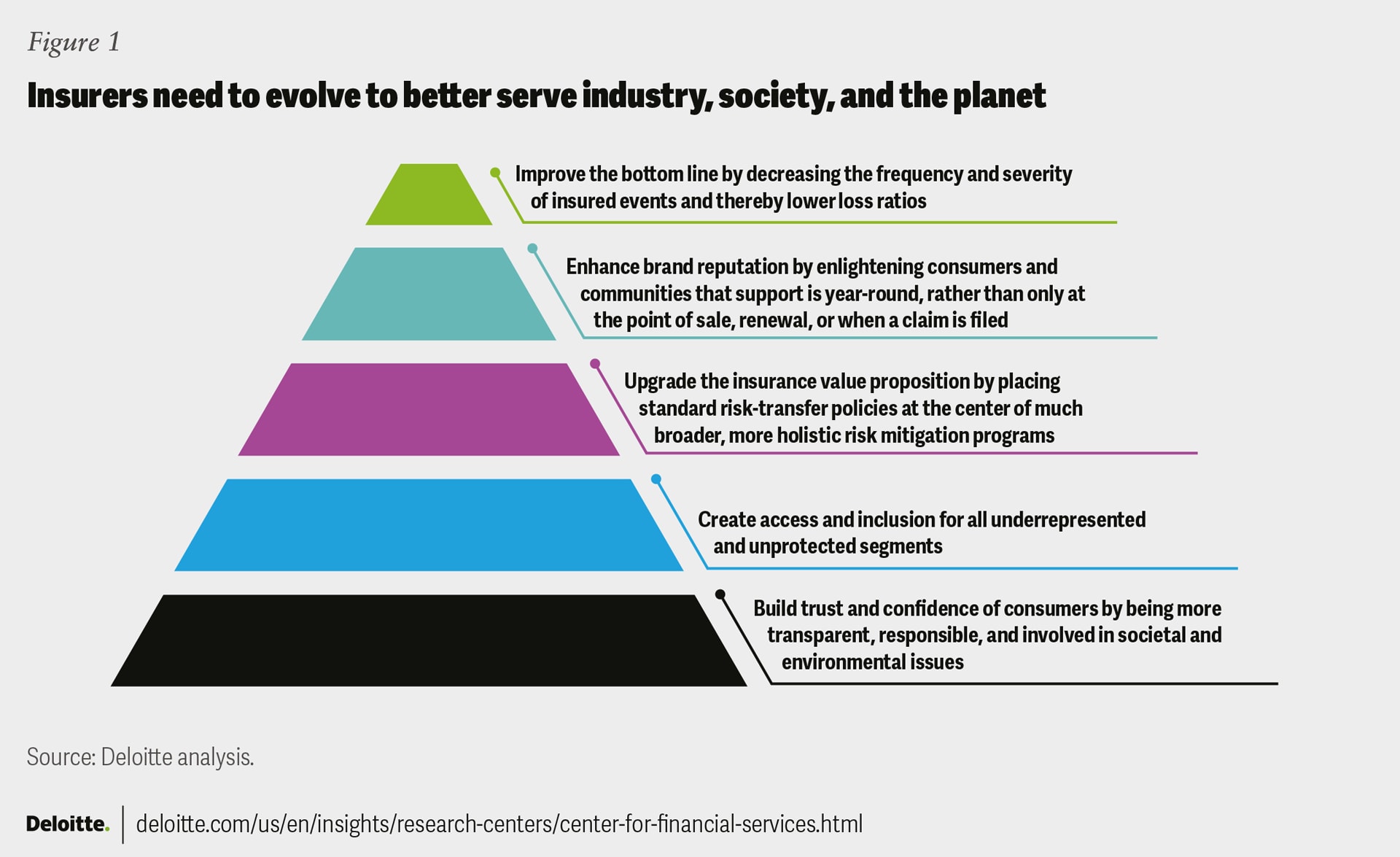

Change is accelerating all around us, possibly at a faster pace than in any period in history. Shifts in climate, technology, workforce, and customer/societal expectations combined with macroeconomic and geopolitical volatility are compelling enterprises across the globe to transform their tech infrastructure, products and services, business models, and organizational culture to adapt not just to fuel profitability but to remain relevant and survive. The insurance industry is no exception. In fact, these colliding forces could potentially be the catalyst that sparks reinvention both in how the industry conducts its business and in its overall purpose and role in society.

Insurers have the potential to achieve even greater social good largely because they already act as society’s “financial safety net,” providing a backstop against financial loss for innumerable risks worldwide. However, more insurers are realizing they have a bigger role to play in helping prevent risk, mitigating loss severity, and closing life and non-life protection gaps in global markets, especially in the face of the growing number of what appear to be financially unsupportable risks.

Existential threats, such as catastrophic climate change, the explosion in cybercrime, and concern over vast uninsured and underinsured populations, are driving many insurers to reimagine how to confront disruptions caused by the changing environment and help consumers across all segments prevent or mitigate risks before they occur, rather than merely paying to rebuild and recover after the fact. Even while the most extreme events may appear unavoidable, insurance combined with proactive risk management can still help minimize the degree of their impact on affected individuals and communities (figure 1).

Table of contents

- Key messages

- Insurers are transforming to achieve customer-centricity and elevate purpose

- Non-life insurance

- Life and annuity (L&A) insurers

- Group insurers

- Tech transformation

- Human capital

- Sustainability, climate, and equity (SC&E)

- Finance

- Merger and acquisition (M&A) activity slowing, but insurers should prepare for a potential uptick

- Changing perceptions is the path to the future

{kind=link}

To achieve this level of transformation, insurance companies may need to adopt new technology, including generative AI, to harvest actionable insights from any new data at the industry’s disposal. Industry convergence for access to more information sources, products, and services, as well as talent with the skill sets and know-how of emerging capabilities are becoming table stakes.

Transformative change will likely have to go beyond adding new tech bells and whistles. More proactive insurers are also beginning to embrace enterprisewide culture change to reduce silos, elevate their talent, and achieve a more ubiquitous focus on customer-centricity. For global insurers, this may include rethinking how capabilities are shared across geographies and business lines to help drive a more consistent and integrated customer experience.

Leaders should make an ongoing commitment to ensure diversity, equity, and inclusion (DEI), both in their workforce and the customer demographics they serve. Demonstrating such commitment could help close the trust gap that has often undermined the industry’s credibility with key stakeholders, including regulators, legislators, and rating agencies, as well as society at large, and even their own employees. This could not only prove to be a differentiator in the market, but also help resolve societal issues such as the insurance protection gap.

Earning recognition as sound ethical and financial stewards of societal welfare could ultimately empower insurance companies and their distribution force to shift away from a transactional role to adopt a broader, more holistic, relationship-based approach to consumer interactions. This transformation should not only promote insurers’ growth prospects but could also fundamentally elevate the perception of the industry’s role in protecting and enriching the ever-evolving world.

Non-life insurance: Evolving to strengthen relationships and profitability

For the third straight year, the non-life insurance sector is boosting top-line growth with higher-than-average price increases across nearly all lines of business—yet rising loss costs are making bottom-line profitability elusive for many carriers and the industry as a whole. The one-two punch of elevated inflation and catastrophic events could help fuel transformation in the way the sector interacts with consumers.

The US$26.9 billion net underwriting loss for US non-life insurers in 2022 was the biggest since 2011—over six times higher than 2021’s figure.1 The 14.1% rise in incurred losses and loss adjustment expenses overcame 8.3% growth in earned premiums by a significant margin, driving net income down by one-third to US$41.2 billion and pushing the combined ratio into the red at 102.7, up from 99.6 in 2021.2

Results for Q1 2023 weren’t any more encouraging. The US industry’s US$7.34 billion consolidated net underwriting loss was the largest in 12 years—as well as the worst Q1 figure on record.3

As a consequence, the US non-life market is “facing the hardest market in a generation”4 as insurers struggle to raise prices fast enough to cover record growth in expenses. The price of single-family residential home construction materials soared 33.9% since the start of the pandemic while contractor services are up 27%.5 Meanwhile, 2022 was the eighth consecutive year featuring at least 10 US catastrophes, causing over US$1 billion in losses, driving up property-catastrophe reinsurance costs for primary non-life carriers by 30.1% in 2023, which was double the prior year’s hike of 14.8%.6

Reinsurance rates will likely remain elevated as reinsurers’ retained earnings have been insufficient to bear their cost of capital, let alone build stronger balance sheets to cater to an increasing risk landscape.7 US demand for catastrophe reinsurance alone is expected to grow as much as 15% by 2024, putting further upward pressure on prices.8

Rising insurance rates have reverberated throughout the general economy. Commercial property premiums rose by an average of 20.4%—the first time that rates rose greater than 20% since 2001.9 While inflation has been easing somewhat in 2023, commercial insurance rates have continued to increase, although at moderating levels except for “outliers” such as property coverage.10 Average price increases for cyber insurance, for example, were down to 13.3%11—a small improvement for buyers over the 15% rise in Q4 2022, and over 20% in Q1 2022.12

Rising expenses are also impacting personal lines insurers. Auto carriers saw motor vehicle repair costs go up by 20.2% in April 2023 compared to the same period the year before, versus a 15.5% increase in premiums.13 Part of the problem is that while the assisted driving technologies in new vehicles should improve safety while lowering the frequency and severity of accident losses in the long run, the added complexity of these systems and calibration of their sensors coupled with the impact of inflation can raise repair costs considerably.14 The same trend is evident with the rise in sales of electric vehicles, which are also more expensive to repair than their gas-driven counterparts.15 Meanwhile, claims for the theft of catalytic converters—which neutralize environmentally harmful gases in engine exhaust but also attract thieves seeking their valuable metallic components—exploded from 16,600 in 2020 to 64,701 in 2022.16

Rising insurance costs are affecting consumer sentiment and behavior, with 45% of those surveyed between ages 18 and 34 saying they’ve thought about going without auto insurance as a result—including 17% of respondents who say they are already driving uninsured.17 At a minimum, auto insurance shopping and switching rates have reached new highs,18 raising acquisition and retention costs.19

Homeowners’ insurers are also handing down double-digit premium hikes to cover similar repair and replacement cost challenges, as well as increasing frequency and severity of weather-related disaster losses, such as those caused by wildfires, windstorms, and floods.20 A number of insurers are either scaling back from or moving out of catastrophe-prone states.21

Looking ahead, while further material rate increases in most jurisdictions should support strong premium growth in 2023, uncertainty related to catastrophe experience and claims severity patterns may inhibit a near-term return to an underwriting profit.22 US homeowners’ insurers are expected to post a statutory underwriting loss this year, with a combined ratio of 105, which would be the line’s sixth unprofitable 100-plus ratio in the past seven years.23

On a global basis, non-life premiums increased 0.5% in real terms year over year in 2022, far below the 10-year average of 3.6%.24 However, premiums are forecast to improve in both 2023 and 2024 to 1.4% and 1.8% year over year, respectively, mostly due to rate hardening in personal and some commercial lines (figure 2).25 Non-life insurer profitability is expected to improve through 2024 as higher interest rates strengthen investment returns, premium rate hardening continues, and expectations for slowing inflation lowers claims severity.26

{kind=link}

Even in this environment, where risks are increasingly becoming financially unsupportable, there may be opportunities available for proactive non-life insurers to generate long-term profitable growth. Insurers should consider going beyond their traditional risk-transfer models and instead become more of a protector of individual policyholders, businesses, and society at large.

One area where the industry could face significant disruption is the opportunity and potential threat posed by the growth in embedded insurance. The concept is not new, but what’s changing rapidly is the volume of insurance premiums for major lines likely to be built into other types of third-party transactions, bypassing traditional sellers, such as insurance agents, upending direct-to-consumer sales from insurers, or even excluding legacy carriers altogether.27 Gross premiums are forecast to grow by as much as six times, to US$722 billion by 2030, with China and North America expected to account for around two-thirds of the global market.28

Auto insurers are likely to confront the biggest challenge with the move to embedded coverage. These carriers should, therefore, consider actively seeking alliances before they find themselves without an embedded partner, or figure out how they are going to compete against those who do join forces with a product or service provider.29 This convergence can not only benefit consumers by way of built-in loss-avoidance and detection capabilities, but can also help carriers play a central role in creating stronger client relationships.

The use of parametric insurance is also expanding, where claim triggers and automatic payments are based on an index or specific widespread event rather than a particular loss.30 In addition to more coverage being offered for natural disaster losses, new areas covered by parametric policies include cyber exposures and operational downtimes due to cloud outages.31 Underserved communities might also benefit from parametric catastrophe coverage purchased on a group basis for a particular neighborhood rather than by individual consumers.32 A couple of Fiji-based insurers paid out US$50k to 559 smallholder farmers, fishermen, and market vendors in response to cyclones..33

The ever-expanding use of AI—not just by insurers but also by their customers—presents its own emerging coverage challenges and opportunities. Munich Re, for example, has launched a policy to cover those implementing self-developed AI programs in their own companies, mitigating potential financial losses from AI underperformance.34 Insurers can also consider using AI to help clients reduce or mitigate risks.

More insurers are also expanding their policy portfolio to cover renewable energy projects,35 including Hiscox, which plans to launch an ESG-focused syndicate at Lloyd’s to help capitalize on increasing interest and investment in green technologies.36 Such sustainability-focused efforts could go a long way in helping to enhance the industry’s brand.

A persistent hard cycle, InsurTech innovation that improves underwriting data and capabilities, and rising frequency and severity of catastrophes are just a few of the factors contributing to growth in the specialty insurance market—with projected market-size increases from US$81.5 billion in 2022 to an estimated US$130.1 billion in 202737 at a compound annual growth rate of more than 9.6%. Europe was the largest region in the specialty insurance market in 2022.38

One way or the other, innovation in both operations and products, as well as embracing strategies to drive more frequent client touch points and goodwill could be important components driving non-life insurer growth and profitability.

Life and annuity (L&A) insurers: Core system modernization and culture transformation are underway but more should be done

Due to strong growth in Q1 2022, US life insurance premiums totaled US$15.3 billion for the year, about equal to the record-high premiums in 2021.39 Despite more than 100 million US adults living with a coverage gap, sales slowed in the second half of the year due to consumer concerns over inflation and the economy, even as worries over COVID-19 declined.40

Globally, the L&A sector’s 2023–2024 premium growth drivers are projected to fuel a divergence between advanced and emerging markets (figure 3).41 The impact of inflation on discretionary consumer spending will likely pressure individual life insurance sales in the United States and Europe, while regulatory headwinds may weigh on advanced Asia.42 Conversely, the growing middle class with rising aggregate nominal incomes could power the savings and protection business in emerging markets.43 Across most regions, life insurance growth is expected to be led by rising demand for protection products by younger, digital-savvy consumers who appear to be increasingly aware of the benefits of term life products.44

{kind=link}

On the annuity front, US sales hit a record high in Q1 2023 year over year, despite a 30% decline in variable annuity (VA) transactions, as fixed rate deferred and fixed-indexed annuities increased 47% and 42%, respectively, primarily due to higher interest rates.45 Moreover, second-quarter individual annuity sales increased 12% year over year, surpassing last year’s record despite an 18% drop in VA sales.46 Weakened financial markets and economic indicators are expected to keep pressuring VAs but will likely continue to benefit sales of annuities that provide more predictable outcomes.47

To better address the business instability often driven by economic, environmental, and societal transitions, many L&A carriers are proactively repositioning for more sustained and predictable growth. Indeed, 2024 is poised to be a tipping point for the sector as the world becomes increasingly digitized and customer and agent expectations for more relevant and holistic product offerings and ease of doing business continue to escalate. Carriers are now considering what should be transformed to meet these demands as well as provide greater cushion from external market pressures.

This shift may be challenging, as many carriers continue to struggle with networks of legacy systems and siloed lines of business, products, processes, and culture. However, these obstacles are not expected to be insurmountable.

Like non-life carriers, cutting-edge technology, including digital tools and advanced analytics, could help empower life insurers and their agents to shift away from a transactional role to broader relationship-based consumer interactions. Modernizing systems can potentially facilitate the use of alternative data sources for faster application underwriting and processing, more seamless cross-selling and customer personalization and ease of engagement, as well as rapid new-product launches.

It could also enable better connectivity and collaboration with industry and nonindustry partners across the value chain, both to enhance customer experience and drive more sources of profitable growth. Such collaborations could include services for lead generation, as well as ancillary products to provide holistic coverage (wellness, wealth, health, etc.) capabilities. For example, in Asia-Pacific, insurers are investing in technology platforms and ecosystem partners to improve the customer experience for health and benefits offerings. AIA launched an integrated health strategy across Asia, to simplify customer journeys powered by technology solutions, analytics, and a cohesive ecosystem of payers, providers and partners.48 In Singapore, Manulife worked with a large Singaporean bank to provide low-cost, customizable protection products across life, health, and wealth to young Singaporeans.49

However, modernizing systems is not without its challenges. Although most respondents to a recent Deloitte survey of 100 US L&A chief information officers or their equivalents said they have begun their core system modernization journey, fewer than one-third have completed some (20%) or all (12%) of their initiatives.50 Just over two-thirds have projects currently underway or in the planning stage.51

Moreover, in the last five years, the percentage of L&A carriers intending to upgrade or enhance rather than replace their existing legacy core systems has doubled from 36%52 in 2017 to 73% in 2022.53 While there seems to be agreement that eliminating legacy systems may be too onerous and costly to undertake, carriers can explore a variety of alternative core-system enhancement strategies to achieve their goals.

For example, most of those surveyed (89%) intend to employ InsurTechs as a primary solution for one or more points in the L&A value chain.54 Lincoln Financial Group worked with Modern Life to meet an increased demand for more digitization in the insurance buying experience.55 Munich Re worked with Paperless Solutions Group (PSG) to offer a combined risk assessment and e-application product that allows life insurance carriers to underwrite new policies faster and more accurately.56

Most respondents also say they will use cloud capabilities for new solutions related to core modernization. This solution can enable business continuity and potentially offers easier scalability, greater agility, lower IT operating costs, and increased security. Socotra is one example of a cloud-native core platform that enables insurers to more rapidly develop and deploy new life insurance products.57

Adding technology capabilities can also potentially lead to increased opportunities to connect more effectively and efficiently with enormous underpenetrated global life insurance markets. The SRI mortality resilience index indicates that more than 50% of the world’s financial needs remain unprotected in the event of the death of the financial head of the household58 and emerging economies account for most of that gap.59 One key strategy to increasing penetration in underserved markets may be adopting digital capabilities to more effectively enable partnerships. Catalyst Fund’s portfolio company Turaco was able to reach over 70,000 gig-economy workers in Kenya and Uganda by offering life and health insurance coverage through partnerships with digital ride-hailing platforms.60

While Deloitte’s survey found systems enhancements are already underway or in the planning stage for many L&A carriers,61 the results may be underwhelming or unsuccessful without corresponding culture transformation. For example, 76% of carriers surveyed want to enable better integration between IT and business units.62

To help achieve more cohesion, they should consider developing a value-stream orientation that could more seamlessly enable end-to-end delivery of business initiatives. This operating model could require a shift to decentralization—creating cross-functional teams to help minimize friction points between business units and functions looking to achieve a specific business goal. Such a paradigm can help align business capabilities, relevant systems, and information flow to potentially alter long-standing company culture by breaking down the barriers posed by siloed thinking and fostering more customer-oriented focus.

From an M&A lens, private equity (PE) firms will likely continue to look to the L&A sector despite the recent decline in activity—largely due to fewer entities to target as interest rates surge. Private capital is playing an increasing role in the insurance market as PE firms seek access to insurers' huge asset pools, and insurers tap into PE asset management skills to help boost returns.63

Group insurers: Doubling down on digital capabilities, connectivity, and ancillary offerings

US employee benefit buying habits continue to be impacted by the pandemic, particularly regarding enrollment decisions for products such as life insurance and supplemental health products.64 In fact, in 2022, new premiums for coverage for accident, critical illness, cancer care, and hospital indemnity jumped 12% to US$2.9 billion year over year.65 New workplace life insurance premiums fell 1% from 2021 to US$3.9 billion—although this is likely because it was compared to the 14% increase in 2021, which was one of the largest gains in 30 years.66

As the pandemic’s impact begins to fade, Deloitte expects that the anticipated overall market growth rate for group insurers over the next few years will likely trend mostly in line with the direction of the economy, employment, and wages.

Providers that want to grow in excess of the overall market may be challenged to expand product portfolios, including voluntary offerings that can potentially add premium and generate higher margins. Forty-five percent of employees surveyed agree they are extremely likely or likely to participate in more voluntary benefits offered through their employer (e.g., critical illness, accident, disability, hospital indemnity, supplemental life, etc.) in 2023, up from 38% in November 2021.67

Moreover, as awareness of long-term care costs grow, consumers are looking to their employee benefits for coverage.68 The additional awareness of long-term care has in part been driven by the Washington Cares Fund, which mandates long-term care insurance for all employees in the state of Washington as of July 2026, supported by employee-paid premiums.69 This coverage provides access to a total balance of up to US$36,500 (adjusted annually for inflation) for eligible consumers.70 Similar initiatives have been advanced in about a dozen states.71 A growing number of employers are also offering their workers hybrid solutions that bundle life insurance with long-term care as a voluntary or employee-paid benefit, and more than a handful of carriers are active in the segment, including Allstate and Chubb.72

Group insurers are also seeking avenues to increase client engagement and add value to differentiate their brand. One trend—likely exacerbated by the pandemic and the "great resignation"—is increased consumer demand for employee benefits focused on financial health and well-being. Providers and brokers can consider working with InsurTechs to potentially help businesses benefit from healthier and more motivated employees, and at the same time, encourage more frequent touch points in customer relationships.

For example, YuLife, a London-based InsurTech is launching its holistic employee benefits and well-being platform in the United States, harnessing behavioral science and game mechanics to encourage workers to make proactive lifestyle changes while also prioritizing prevention by derisking individuals through healthy activities.73

Providers, benefits brokers, and employers who make such offerings accessible to employees can potentially turn financial products into a force for good by inspiring people to improve their mental, physical, and financial well-being in a holistic and engaging way.

Group insurers are also seeking more innovative ways to improve client experiences on digital portals while enabling self-service capabilities. As the race to ubiquitous digitization continues, HR organizations across industries should be endeavoring to keep pace in a competitive labor market. Expectations for cutting-edge innovation around benefits administration systems to enable seamless movement of employee data between providers and employers is no longer likely to be nice-to-have functionality.

One way to help deliver a more efficient and effective digital experience to HR organizations with disparate systems might be to build an application programming interface (API) connection from the provider system into the employer’s benefit administration platform. Instead of downloading data and passing it back and forth between insurers and employers, the carrier can connect directly into the employer source systems through APIs. APIs can connect to a variety of employee benefits systems for scalability and flexibility.

With expense reduction top of mind for many due to concerns about a possible economic downturn later this year into 2024,74 insurers should be considering elements, such as expected return on investment and which use cases competitors are focusing on, to strategically prioritize which of their customers’ employee benefit administrative platforms to connect to and the use cases that can be most impactful. These use cases may include capabilities such as real-time benefits enrollment, benefits eligibility checks, processes to drive specific product purchases, billing, employee updates, and employee verification of eligibility prior to claims payment.

Employees are putting higher value on their benefits and related experiences, challenging employers and providers to create improved customer experiences through broader product offerings and digital portals and services, potentially opening the door for year-round benefits engagement.

Tech transformation: AI is opening new avenues to enhance and personalize the customer experience

The evolving operating environment should put even more pressure on insurers across sectors to increase the use of automation, AI, advanced analytics, and core transformation in the year ahead. These capabilities could be the foundation for insurers to adapt to the complexities of the quickly changing environment and elevate their purpose.

Advanced technology capabilities can help achieve operational targets such as improved underwriting for more accurate pricing and risk selection, bolstering claims management to limit loss costs, and improving efficiency by streamlining operations. They could also advance longer-term goals such as proactively helping clients mitigate or eliminate risks before they even occur, promoting personalized coverage and services to strengthen customer relationships, and making outreach to underserved segments more efficient and effective.

Although digital transformation has topped insurer agendas for several years, consumers still yearn for digital services, interfaces, and experiences that are comparable to those provided by noninsurers such as e-commerce giants.

Legacy constraints, such as old mainframe-based systems, multiple core platforms, integration complexity, and ineffective data flows, still often impede experience optimization, even as more data and systems are moved to cloud platforms. To help make this shift more impactful, insurers can consider making customer interfaces more engaging and intuitive by strengthening their digital engagement layer with technologies such as AI and advanced analytics to elevate the customer experience.

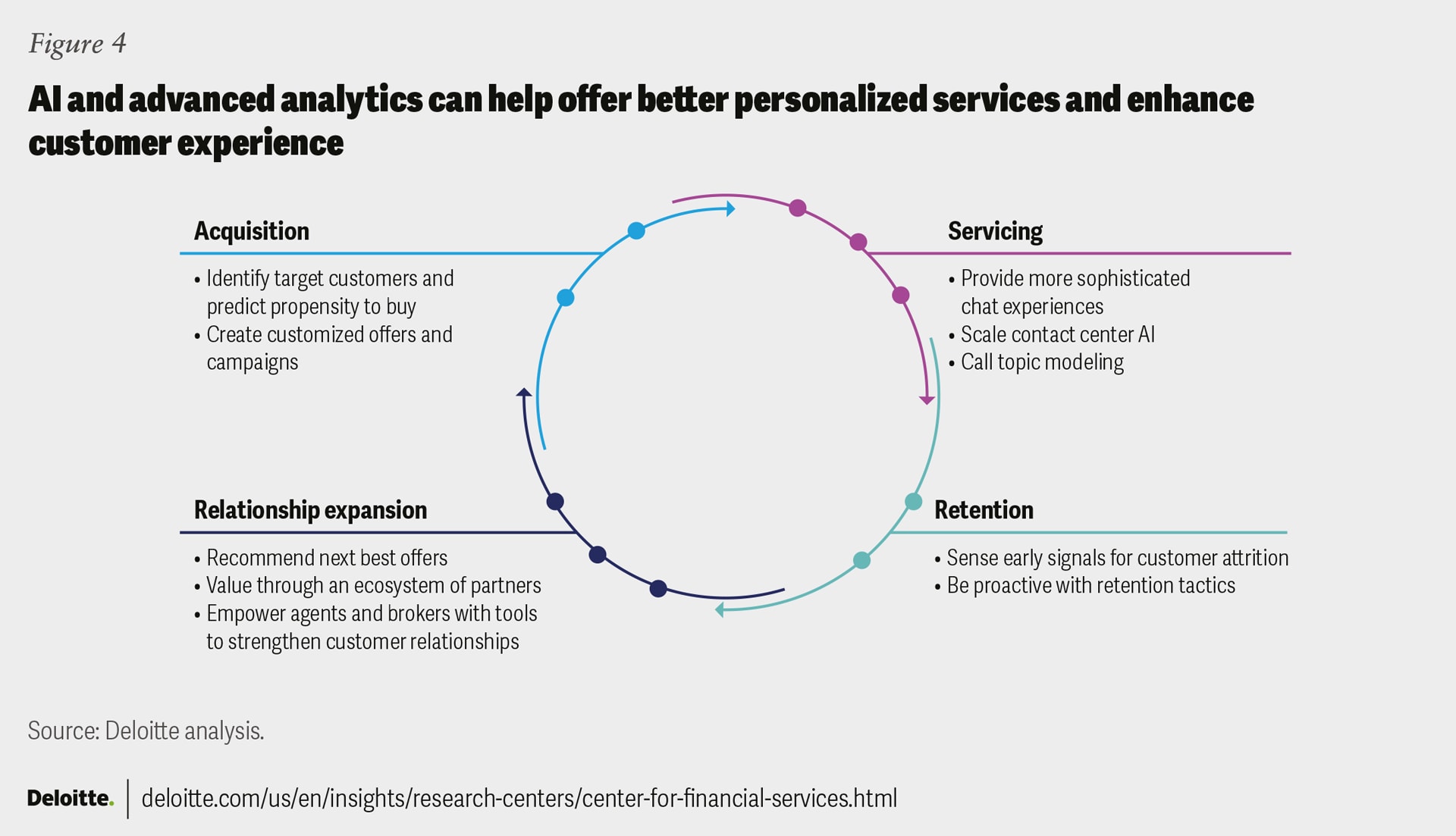

AI’s original promise was to improve employee productivity, speed up decision-making, and reduce costs, however it could also be a significant disruptor to customer experience. Coupling AI with advanced analytics can potentially provide a more complete, real-time picture of insurance customers, including their actions and sentiments. Such insights can be leveraged to target customers with offers, advice, or services most relevant to them at moments that matter most to them. For example, HDFC ERGO, an Indian non-life insurer has been using AI to offer hyperpersonalized experiences to its customers, including customer onboarding, issue resolution, and claims handling.75

Personalization may bridge the gap between current levels of insurance customer experience and desired e-tail-like experiences (figure 4).

{kind=link}

Insurers can also use AI and advanced analytics capabilities to analyze Internet of Things (IoT) data to help better identify potential disasters before they happen and nudge policyholders to take corrective and preventive actions. Hartford Steam Boiler, for example, has launched Sensor Solutions, which employs a number of hardware sensors to detect elements like temperature changes and presence of water via an app for remote oversight, sending alerts to prevent loss events.76

Insurers are also seeking practical applications for how they can take advantage of generative AI, to help drive efficiency and customer-centricity. Many are identifying and validating use cases that could apply across the insurance value chain using these capabilities, with employee experience and workforce productivity already emerging as the most prominent areas of interest.77 AXA recently announced the release of an in-house–developed generative AI tool to 1,000 employees and plans an enterprisewide rollout in a few months.78

AI can also be used by insurers to fine-tune large language models (LLMs79) for specific roles and tasks within insurance organizations. For example, models can be trained to function as actuaries, underwriters, claims adjusters, and customer service representatives. However, given regulatory concerns as well as questions about the reliability of AI-generated material and decisions, insurers should be carefully vetting how much to delegate to this new technology and determine where human judgement may be necessary, especially in terms of quality control oversight.

Moreover, insurers’ AI and analytics capabilities are likely only as strong as the underlying data sources supplying it. To generate faster and better insights, insurers could eliminate silos that can cause a myopic understanding of the customer and modernize their data capabilities with an enterprise view. This may include enhanced master data management, integrating, managing, governing, and using both company data and large unstructured data sets and third-party data.

Innovation using capabilities such as AI, advanced analytics, and IoT may not always come from within the organization’s four walls. Insurers may obtain these capabilities externally from third-party vendors—from startup InsurTechs to large technology firms. For example, UK-based Send launched a generative AI–based commercial and specialty underwriting solution to help speed up underwriting by automated extraction of information from unstructured data sets.80

Insurers should also be cognizant that with advancements in AI technology, they are likely to have more capabilities than what might be permitted within the realm of local and global privacy and consumer protection laws. Therefore, AI and generative AI implementations should include collaboration with the chief risk officer and chief compliance officer to identify possible problem areas and establish guardrails to meet governance standards on how these technologies can be used.

Given the pace of development of AI and generative AI technology, regulators may find it hard to keep up. The European Union has taken the lead in paving the way for regulators around the world with a global regulatory framework for use and development of the technology.81 However, insurers’ responsibility lies in ensuring that its use and development should be driven not only through profitability lens, but also with an emphasis on ethics and trust, governed by corporate values.

AI, especially generative AI, could also empower bad actors, from hackers to insurance fraud perpetrators. Cyberattacks using LLMs are already materializing.82 Using generative AI, even novice bad actors can write elaborate malware codes or believable phishing emails impersonating insurance companies or even government agencies. For example, perpetrators of synthetic identity fraud, in which cybercriminals create new identities with stolen or fabricated data can use gen AI to impersonate others by creating images and videos in someone else’s likeness.83 This can pose significant threats both to insurance policyholders and employees. Insurers should be updating their enterprise risk management protocols as well as accelerating employee awareness and training programs to minimize emerging threats.

Technology advancements could be a huge impetus to elevating the industry’s vision and mission. Insurers should transform their conservative mindsets and embrace emerging technology capabilities that can help increase focus on societal and environmental impacts as well as profits.

Human capital: Technology and culture modernization activate focus on workforce transformation

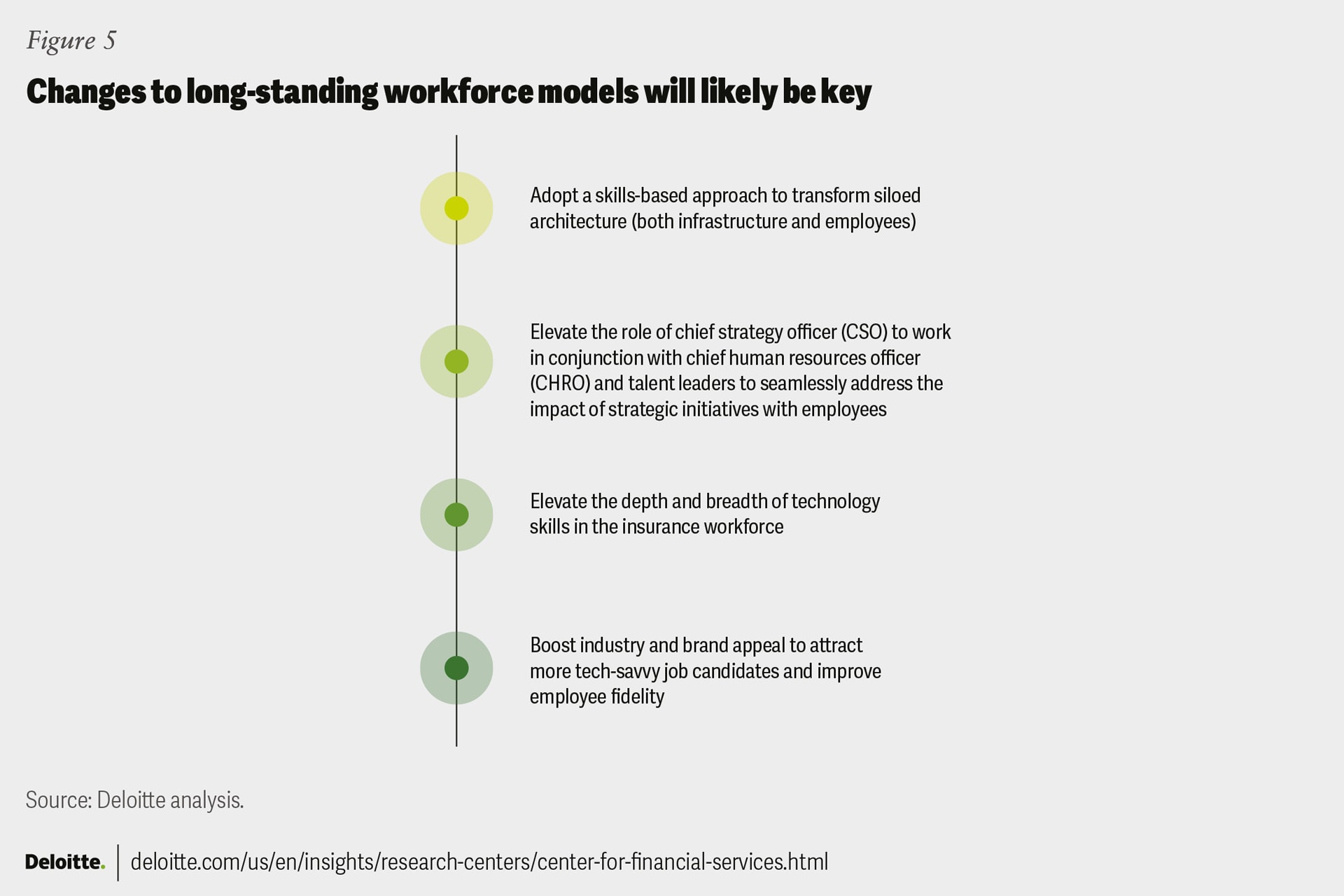

While technology is the vessel needed to move data quickly and seamlessly throughout the value chain, the human capital aspect is potentially even more elemental to a carrier’s success. Insurers seem to be recognizing that rapidly evolving dynamics impacting the industry could require workforce transformation.

There is an increasing realization among carriers that the way talent is accessed, engaged, and developed should be based on where carriers want their organizations to go in the future, not the way things have typically been done84 (figure 5).

{kind=link}

As discussed in the L&A section, the siloed architecture that tends to permeate throughout the industry—including infrastructure and workers—should be transformed to help break bottlenecks and increase the speed and agility associated with customer-centric models. What this means for the workforce is that business units and functions such as underwriting, portfolio investment, and claims management may no longer act independently, but instead adopt a skills-based approach enabled by the shift from employee-based models to workforce ecosystems.

The construct involves understanding employee competencies by role, function, and level, notwithstanding where they reside in the company, and leveraging them across business lines and functions, potentially breaking down silos and driving more impactful collaboration. This might also entail finding or developing new skills to harness digital tools while driving elevated experiences and outcomes for workers, customers, the business, and society at large.

Recognizing the impact to the workforce that may ensue from long-term growth strategies, many insurers are elevating the role of the chief strategy officers to work in conjunction with the chief human resource officer and other talent leaders. This could help ensure that shifts in the long-term strategic vision can be embedded in change management messages and are in sync with the employee value proposition.

Moreover, as insurers ramp up their technology architecture, many are looking to elevate the depth and breadth of technology skills in their workforce. This can augment skills requirements for underwriting, actuarial science, and predictive modeling positions, further intensifying competition both within and outside the industry.

Until now, this has often been a struggle, as a career in insurance may not be perceived to be as enticing a career destination as other FSI sectors or technology companies. But several dynamics are unfolding both within and outside the industry that may generate greater appeal to more tech-savvy job candidates.

The potential shift in direction for many in the industry creates an opportunity for insurers to demonstrate how they lead with a more purpose-driven value proposition to attract the right talent. Carriers may need to exhibit not only how they are embracing cutting-edge technology, but the benefits of building a career in an industry whose purpose is not only profitability, but also to make a positive impact on society, helping the world thrive by standing behind other industries to allow for greater innovation, productivity enhancements, and calculated risk-taking.

At the same time, the fallout from over 300,000 layoffs in technology companies in the first half of 202385 created a talent pool that may be looking for a more stable working environment. This talent pool could also include InsurTech employees being let go as startups battle economic uncertainty and a period of transition.86 It will likely be incumbent upon insurers to consider those with no or less industry experience to broaden the potential candidate pool, which may also add new levels of diverse thinking to the workforce.

In addition, the adoption of new technology may not only transform the industry’s appeal from “antiquated” to cutting-edge but may also provide employees with increased opportunities to focus on more meaningful, purposeful, higher-value work. Indeed, many new technologies don’t just augment human workers, they can make work better for humans and humans better at work.87

In fact, it is estimated that AI and machine learning will increase labor productivity about 37% by 202588 by eliminating or minimizing more manual tasks and freeing up current workers to add more value. This will likely require reskilling and upskilling, which should appeal not just to the current workforce,89 but also job candidates looking for a career they can grow in.

Moreover, technologies such as generative AI can provide nudges to the client-facing workforce to portray greater empathy90 or signal potential customer attrition/coverage lapse91 before it happens, which could boost goodwill and stronger relationships between the workforce and the client base.

Amid these changes to technology and operating models, carriers should remain focused on adapting to become a brand that employees are excited and proud to be part of, because it’s likely that employees will be more passionate and productive when they believe in their company’s mission.92

"With company culture as the center of gravity, providing a unique employee experience must focus on career development, purpose, flexibility, well-being, social, and environmental goals. The importance of human interaction has increased post pandemic, and we aim to harness smart working in a hybrid setup, enabled through team agreements that support individual and team needs. Going forward, how we leverage the technology advancements to innovate and further elevate the experiences and outcomes for our people and customers will be the key."

—Taeko Kawano, chief human resources officer, AXA Holdings Japan Insurance, during an interview with Deloitte Center for Financial Services conducted on August 3, 2023.

Show more

Sustainability, climate, and equity (SC&E): Insurers may look to reform brand perception through ambassadorship

SC&E, as a concept, is not new to the insurance industry. What is changing are the escalating stakeholder demands and evolving avatars of risks—from the frequency and severity of natural disasters to financial and reputational ramifications from their unique position as investors and underwriters. As regulatory bodies around the globe enhance disclosure expectations, insurers are pivoting to more impactfully incorporate SC&E into their corporate strategy and DNA.93 However, evolving into stewards of purpose may require internal enhancements both vertically and horizontally across insurance organizations.

In addition to escalating their own decarbonization goals, insurers should assist clients’ transition to net-zero

Having experience assessing and managing risk, insurers may be well-situated to position themselves as sustainability ambassadors—clearly communicating risks and opportunities and influencing executive’s decisions and strategies across industries to create a better workplace, marketplace, and societal impact.

While the insurance industry’s scope 1 and 2 carbon emissions from their own operations are rather low (10% to 25% of total emissions)94 carbon abatement can potentially be further improved through occupying greener buildings and vehicles, as well as waste management program enhancements.

Types of green house gas (GHG) emissions

Scope 1 emissions: Direct emissions from operations

Scope 2 emissions: Indirect emissions from purchasing oil, gas, and other forms of energy

Scope 3 emissions: Carbon emissions produced upstream and downstream in the supply chain by external vendors, suppliers, and partners

Show more

The industry’s scope 3 emissions (75% to 90% of total emissions)95 may require reevaluation of underwriting and investment portfolios. Several European insurers are already working to elevate the importance of sustainability throughout their underwriting and investment portfolio determinations.96 For example, global insurer Chubb launched a packaged insurance solution in the United Kingdom to support the growth of small and medium alternative and renewable energy projects with a planned global rollout.97

As investors and underwriters, in addition to balancing their own asset liability portfolio to prepare for potential devaluation of fossil fuel-based assets, many insurers are also guiding clients as they develop their decarbonization commitments. However, these decisions are not without obstacles.

This year, many large global carriers with significant US operations and membership in the Net Zero Insurance Alliance (NZIA) faced backlash from US lawyers citing potential legal concerns over their decarbonization agendas.98 Pursuing decarbonization objectives collectively could create material antitrust risks, resulting in a series of carrier withdrawals. This might ultimately lead to the disintegration of the NZIA.

Whether companies decide to partner with industry groups or proceed individually, their intent and actions around climate pledges, social equity initiatives and reporting should be transparent. Indeed, stakeholders including regulators, investors, employees, customers, and litigators are keeping close tabs on probable acts of greenwashing, where some companies might resort to selective disclosure and filtered focus.

Moreover, regulators have a growing expectation from the insurance industry to finance the transition to net-zero from now till 2050. Annual public climate finance flows estimated at US$1.25 trillion are expected to cover only 25% of the funding requirement.99 There is a need to mobilize annual private climate finance flows of at least US$3.75 trillion to cover the 75% gap.100

Financing for a sustainable economy likely requires a strong public-private partnership that can help close the funding gap. For example, a group of 11 private insurers are providing reinsurance to facilitate the largest debt conversion for marine conservation of the Galápagos Islands. This can help Ecuador save more than US$1.126 billion in reduced debt service costs. It is expected to generate US$323 million for marine conservation in the Galápagos Islands over the next 18.5 years, highlighting the impact sustainable finance solutions can have in addressing the funding gap for biodiversity conservation.101

Governance framework could require restructuring to sensitize and align people, and set enterprisewide controls and processes

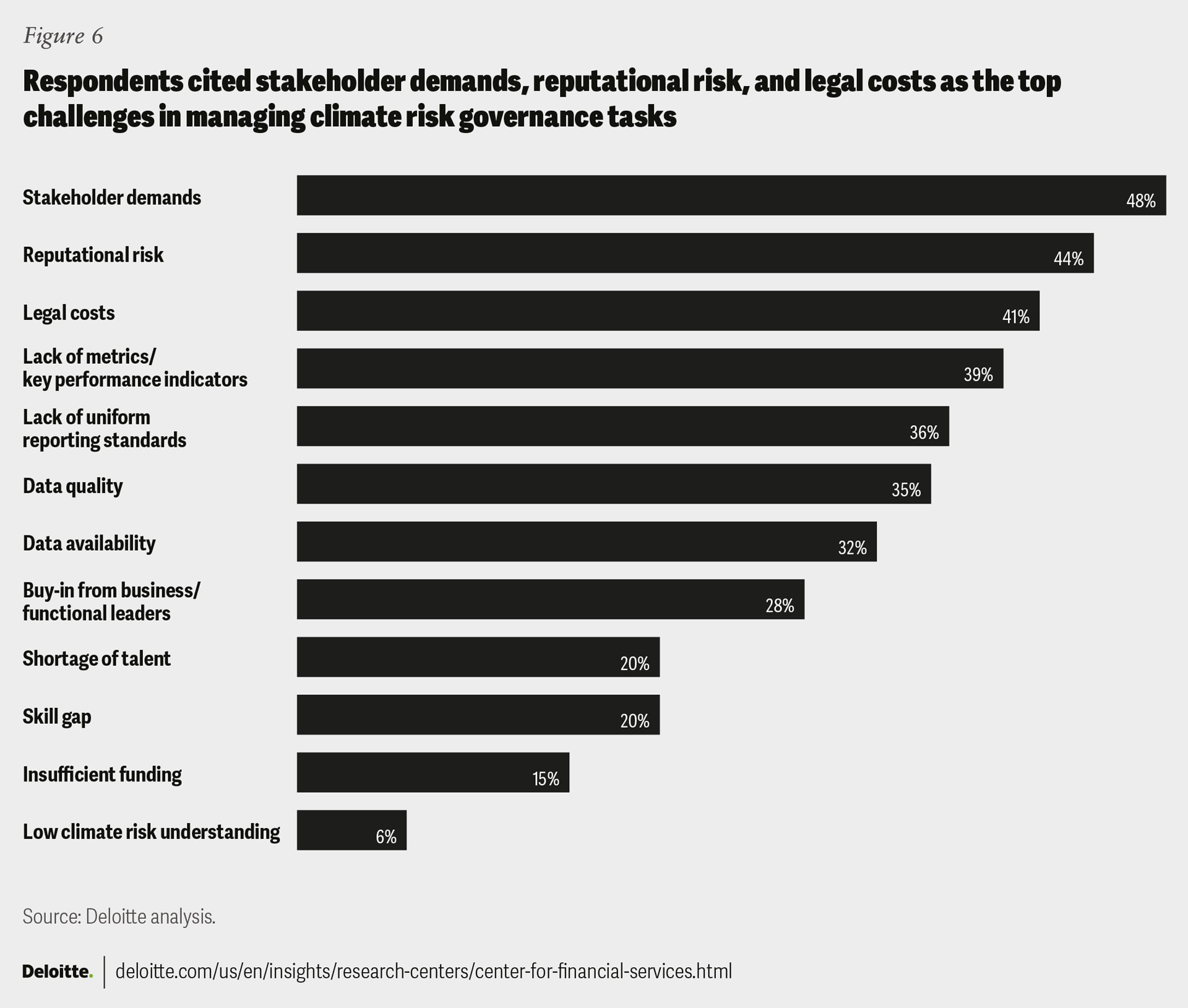

A Deloitte survey of US sustainability executive-level insurance respondents revealed several large obstacles to adherence of climate risk governance–related tasks (figure 6).102

{kind=link}

Regulators are already working on defining metrics for insured emissions calculations. The International Sustainability Standards Board (ISSB) issued its inaugural IFRS S1 and S2 disclosure standards. Europe introduced target-setting protocols and Canada’s Office of the Superintendent of Financial Services finalized climate risk management guidelines. In the United States, the Securities and Exchange Commission is framing guidelines for emission reporting, and further developments from regulators along with development of federal and state requirements for the insurance industry through 2024 are anticipated. While there is more clarity on the accounting treatment of financed emissions for insurance companies, going forward, further transparency on underwriting emissions is expected.

As regulators and other stakeholders seek more information, the scope of data collection, measurement, and reporting work is expected to increase significantly. Most insurers should reconstitute an overarching SC&E governance strategy to help facilitate more effective controls, improve stakeholder management, and achieve greater sustainability across the functions and lines of business.103

The cost of SC&E compliance may also need to be considered, particularly in the current operating environment. Rather than instituting separate initiatives, insurers can find efficiencies in compliance by working in tandem with data warehousing and reporting initiatives, like data or finance transformation. In many cases, SC&E compliance and reporting rolls into the finance organization, so it may be a natural path to reducing the cost of compliance.

Social equity demands broader product and service outreach and increased representation on executive leadership and the board

Societal and corporate commitment to DEI increased rapidly in 2020 following the death of George Floyd.104 Insurers responded by initiating DEI-specific goals, benchmarking, training, and recruitment.

There are still challenges within the industry based on interviews by Marsh McLennan and the National African American Insurance Association’s (NAAIA) of 650+ Black/African American risk and insurance professionals.105 The interviews revealed that 84% of the respondents still face challenges in advancing their careers due to conscious or unconscious racial bias. Respondents cited lack of promotions (75%), growth opportunities (70%), and mentorship (68%) as their primary concerns, which may be a major challenge with retention.106

Going forward, it is important for insurers to go beyond “treating DEI as an initiative” and take steps to develop an inclusive ecosystem that provides a sense of belonging. Improving their own internal diversity and inclusion in management, executive leadership, and the board can amplify growth opportunities for diverse groups. Evidence suggests that for each woman added to the C-suite, there was a positive, quantifiable impact on the number of women in senior leadership levels just below the C-suite.107 Some actionable steps may include establishing network groups and conducting learning and development programs on unconscious bias, allyship, and inclusive leadership.

Insurers should also consider advancing their financial inclusion initiatives with more suitable offerings in products and services when considering social goals. For example, a study by the Wharton Climate Center found low- to moderate-income households and communities of color lack adequate insurance coverage against climate-related disasters..108 Insurers may consider increasing coverage reach and affordability for unserved or underserved segments and regions, working with governments and other industries to provide better access to long-term savings and health insurance, and diversifying their workforce to better serve various demographics in the population.

International governing bodies like the World Economic Forum suggest reporting the percentage of employees per category by age group, ethnicity, gender, and other diversity indicators and talent benchmarks.109 The SEC has also established several “human capital” disclosure requirements, with more under discussion.110 However, insurers should subscribe to the idea that it’s not only about compliance, it’s about excellent corporate citizenship.

Finance: Accounting and tax rule changes should spur wider-ranging operational innovations

While technology and culture transformations are in various stages of development throughout the insurance industry, ![]() most carriers have transformed their finance systems to meet the January 1, 2023 effective date for new accounting rules for reporting on long-term insurance and annuity contracts.111 US publicly held companies are now operating under revamped Long-Duration Targeted Improvements (LDTI) rules, following a parallel path to similar global regulations laid down under International Financial Reporting Standard 17 (IFRS 17) by the International Accounting Standards Board, effective for both L&A and non-life carriers.112

most carriers have transformed their finance systems to meet the January 1, 2023 effective date for new accounting rules for reporting on long-term insurance and annuity contracts.111 US publicly held companies are now operating under revamped Long-Duration Targeted Improvements (LDTI) rules, following a parallel path to similar global regulations laid down under International Financial Reporting Standard 17 (IFRS 17) by the International Accounting Standards Board, effective for both L&A and non-life carriers.112

More than half of respondents (57%) to a December 2022 survey of insurance executives for Deloitte Global by Economist Impact said IFRS 17’s benefits would outweigh its costs—up from 40% in a 2018 survey and 21% in 2013—citing a positive impact on claims management, underwriting, and pricing, as well as operating model changes other than finance or actuarial.113

However, many insurers may still have more work to do, including how to communicate the context and meaning of financial results under the new accounting standards to external stakeholders, such as equity analysts, rating agencies, and institutional investors. Insurers should also be looking to capitalize on potential benefits outside of the finance function, such as long-term forecasting for expenses and budget needs. Moreover, going forward, IFRS 17 and LDTI may have an impact on product choices, given that the new standard offers more clarity on profitability by product.

In addition, in the United States, while the new LDTI rules for the moment only apply to publicly traded insurers, privately held and mutual companies must also comply by 2025.114 Such carriers could benefit from lessons learned by public companies in their IFRS/LDTI implementations.

What’s next for insurance tax leaders?

Insurance tax departments with multinational operations should be monitoring legislative developments and planning for the anticipated tax impact of the Organization for Economic Cooperation and Development’s Pillar 2, which introduces a global minimum tax, by jurisdiction, based on book income with a number of adjustments. Several jurisdictions have already approved/passed legislation and many others have released draft legislation and taken other steps toward adoption of Pillar 2.115

Insurance tax departments should be proactive and invest early to become familiar with the rules, model tax impacts, as well as think about potential planning and/or restructuring that could help to mitigate adverse tax impacts. Insurance tax departments should also understand the data requirements for proper implementation of the new rules and associated reporting. Given the complexity and significance of these coordinated worldwide changes, reliable tax models call for the aggregation of new and detailed data, much of which may not be currently collected and readily available.

The United States has not drafted legislation specifically related to Pillar 2.116 However, US-based multinationals and foreign-owned US companies are expected to be subject to Pillar 2, in various forms, regardless of US legislation.117 As such, US insurance tax departments should monitor legislative developments (both in the United States and in other jurisdictions) and plan for Pillar 2 and potential future legislation in the United States. Insurance tax departments should also be assessing whether the new book-minimum tax may apply to their business. The book-minimum tax is a 15% minimum tax, effective for taxable years beginning after December 31, 2022, which is targeted at corporations with substantial book income (i.e., those with average annual adjusted financial statement income of over US$1 billion either individually or with a group of related companies).118

In addition, insurance tax departments should remain close to their business and investment units, so they are prepared to respond to changing marketplace landscapes. For instance, insurers should be closely monitoring changes in interest rates and the tax department should be involved in discussions related to things like investment planning and hedging strategies so that the tax impacts can be properly understood and estimated prior to executing trades.

Merger and acquisition (M&A) activity slowing, but insurers should prepare for a potential uptick

Globally, 449 M&A deals in the insurance sector were completed in 2022—the highest in a decade—up from 419 in 2021.119 However, activity fell from 242 deals in the first half of the year to 207 in the second, as inflation and interest rates continued to rise.120

While the macroeconomic environment in North America and Europe seems to be impeding activity in the near term, Asia-Pacific deals increased from 42 to 60 transactions year over year, with a 22% increase in the second half of 2022.121

Going forward, economists indicate that the worst of the economic downturn is likely past in most parts of the world122 and while M&A activity is expected to increase, the volume may decline from the highs of the past several years.123

From a global deal perspective, several insurers in the United States and Europe are exiting more mature markets and exploring entrance into higher potential growth regions, such as emerging Asia-Pacific, given relatively low insurance penetration rates compared to more developed countries. For example, Chubb acquired Cigna’s accident, health, and life businesses in South Korea, Taiwan, New Zealand, Thailand, Hong Kong, and Indonesia, with a value of US$5.36 billion.124

In the United States, the L&A sector’s activity fell 33% to 16 transactions with an aggregate value of US$160 million in 2022, from 24 transactions totaling US$24.5 billion in 2021.125 While there was high demand for acquisitions, supply was minimal due to interest rate hikes.126 The upward trajectory of interest rates will also likely continue to inhibit PE activity in the sector. PE firms seek to access L&A carrier balance sheets as a source of permanent capital.127 If rate hikes and inflation cool toward the latter part of 2023 and into 2024, PE firms may reenter the market with pent-up demand and begin aggressively seeking deals,128 with a likely focus on distribution networks and finding synergies.129 Life insurers could be open to deals to transform their balance sheets. As drivers of synthetic profitability diminish and hedging risk increases, there may be an increase in activity either through reinsurance transactions or sales of closed blocks of business.130

US P&C activity slowed in 2022, with 38 deals at total aggregate value of US$13.5 billion compared to 43 deals announced with total aggregate value of US$22.0 billion in 2021.131 The cost of inflation on claims continues to drive up combined ratios, fueling expectations for a prolonged hard market. This will likely diminish deal activity in the near term, with the exception of carriers looking to move into new markets or refocus on core business competencies. For example, in May 2023, AIG announced an agreement to sell Crop Risk Services to American Financial Group Inc. for US$240 million.132 AIG also sold Validus to RenRe in May for nearly US$3 billion, in an effort to continue its portfolio repositioning.133 Moreover, in July 2022, Lemonade purchased Metromile, accelerating the former’s entry into the auto space.134

Insurance broker M&A in the United States and Canada declined 24% to 359 deals in the first half of 2023 compared to the same period in 2022.135 The decrease maintained a pattern that began in the second half of 2022, when some of the sector's most active purchasers’ activity slowed dramatically from increases in the cost of capital.136

In the near term, the global InsurTech market may see more activity. Since the stock-market downturn in 2022, there was a sharp decline in InsurTech valuations and potential IPOs.137 Therefore, investors and founders may seek alternative solutions for growth, such as acquisitions to build scale, which could lead to consolidation in the sector. For example, Zinnia, an L&A insurance technology and digital services company, announced the acquisition of Policygenius, a digital insurance marketplace, on April 25, 2023, to create a tech-focused platform covering the full insurance life cycle.138

Looking ahead to 2024, there are several triggers that may signal a rise in M&A activity:

- A shift in macroeconomic indicators such as lower interest rates and inflation could impede organic growth, driving more M&A.

- Carriers seeking digital modernization will likely increasingly align with InsurTechs for the entirety of the customer journey, rather than just point solutions.

- Many venture funds will enter a period of exits and evergreen creation, as this cycle appears overdue approaching 2024.

- With increasing focus on expense reduction, insurers could look to consolidate their operations and streamline processes by divesting noncore business.

As these elements unfold, insurers should be hyperfocused on benefiting from any possible synergies, particularly for carriers looking to increase scale with M&A activity, especially in a recovering economy. While merging organizations infrastructure generally requires capital investment, it will likely accelerate the elimination of unnecessary expenses by avoiding the need for redundant resources once the companies are on a single platform.

Insurers can also consider updating a potential target list for acquisitions according to their stated growth strategies. They can work with their corporate development and trusted advisors to expose opportunities for shedding unprofitable or noncore businesses. In a quiet M&A market setting, getting your ducks in a row in anticipation of a potential uptick in activity is often the differentiator on which carrier gets to close the deal.

Changing perceptions is the path to the future

While the insurance industry has consistently made a positive contribution to society by distributing risk to help reduce financial uncertainty and make accidental loss manageable, there often remains a mismatch with society’s perception of its mission.

However, the industry is at the precipice of considerable transformation going into 2024, gearing up to augment its overall mission to the benefit of employees, society, and even our planet. This may be the formerly elusive game-changing moment that elevates the role and understanding of the insurer in the lives of their clients and communities.

Karl Hersch

United States

James Colaço

Canada

Michelle Canaan

United States