2025 global insurance outlook: Evolving industry operating models to build the future of insurance

Focusing on agility, innovation, and customers to help navigate complexities and meet new demands

How can insurers adapt to the rapid pace of change?

Insurance is a fundamental component of economy and society: It underpins progress and helps power humanity forward more securely. However, the risk-averse nature of insurers’ cultures and their focus on underwriting margins and solvency have generally reinforced a restrained pace in terms of its own innovation and modernization.

This has often resulted in unsustainable or nonoptimal strategies to respond to less predictable spikes or dips in specific business lines and profitability. For example, high inflation and increasingly erratic climate-related losses put pressure on non-life insurance lines’ profitability over the past few years.1 Many insurers responded by hiking premium pricing2 and even pulling back coverage for certain high risks.3 Moreover, as interest rates rose, life insurance and annuity carriers jockeyed for position in a crowded field to take advantage of the surge in consumer interest in savings-linked products. These short-term strategies helped drive the best year-over-year underwriting results for property and casualty (P&C) carriers since 2007 in the first quarter of 2024,4 and the highest first quarter sales of annuities for life and annuity (L&A) providers since the 1980s.5

But, as risks become more complex and unpredictable and consumers more empowered, particularly with generative AI tools at their fingertips, insurers can no longer evaluate risks through the rear-view mirror. They should continue to evolve the way insurance works and how they interact with customers and distributors. It is becoming increasingly important for carriers to elevate technological and operational excellence, innovate product solutions, and broaden the insurance value proposition—making the insurance safety net more reliable, accessible, and resilient. By modernizing and streamlining infrastructure, operations, and business models, insurers can develop a more forward-looking approach to risk modeling, assessment, analysis, and mitigation.

As insurers evolve their business models, it will be important to maintain trust with the customers and markets they serve. For example, after a period of consumer “sticker shock” from large non-life premium increases,6 coverage pullback,7 and fears of surveillance from advanced technologies,8 the industry may first need to rebuild goodwill among stakeholders to help support their objectives. Indeed, machine learning and AI can amass and analyze vast amounts and sources of data, but insurers should provide transparency and fairness to help make these approaches acceptable to consumers and regulators.

Moreover, rapidly evolving customer preferences and technological advancements may make it harder for carriers to compete alone. Building or acquiring new products and capabilities can be time-consuming, uncertain, and capital-intensive. It may become increasingly necessary to partner with vendors that can provide carriers with the speed needed to meet customer and distributor demands and the flexibility to more efficiently adapt to economic, geopolitical, or climate-related turmoil.

Amid this transformation, new tax rules are expected to present challenges and opportunities for insurance tax departments around compliance, including strategies around data collection, reporting, scenario planning, and corporate restructuring. Insurers may also need to consider changes to pricing, cost optimization, and M&A strategies in light of the erosion of tax benefits and uncertainty around the impact of new tax laws.

As known risks escalate and unknown risks arise, insurers should remain a resilient source of financial security in an environment of change and uncertainty. This will likely require agile, innovative operating models and adoption of advanced technologies. As the pace of change accelerates, insurers should consider becoming nimbler to help them quickly and effectively adapt to how they interact with consumers, distributors, government agencies, ecosystem partners, and even their own workforce.

How can each sector keep up with rapid change to create opportunities for long-term growth and inclusivity in 2025?

Non-life (property and casualty) sector

Overall, the non-life (P&C) insurance sector in the United States achieved a US$9.3 billion underwriting gain in the first quarter of 2024—a significant recovery from the US$8.5 billion loss in the previous year’s corresponding quarter.9 The industry’s combined ratio improved to 94.2% in the same quarter, year over year, driven by multiple rate increases in the personal lines sector, which outpaced claims costs.10

Pretax operating income increased by 332%, to US$30 billion, in the first quarter of 2024, year over year, which was bolstered by underwriting gains and a 33% increase in earned net investment income.11 The sector’s net premium growth of 7.4%, combined with a 2.2% reduction in incurred losses and loss-adjustment expenses, further strengthened its financial position in the same period.12

In commercial lines, US insurers should address escalating loss trends in areas like employment practices liability insurance and may choose to adopt a cautious approach to some of the underpriced segments, such as directors’ and officers’ liability.13 As social inflation—the rising costs of insurance claims resulting from litigation over plaintiffs seeking large monetary relief for injuries—leads to larger settlements and jury verdicts, insurers appear increasingly compelled to bolster their liability reserve estimates.14 While this has historically has been a growing issue in the United States, there are now signs of social inflation challenges in Australia as well.15

Geopolitical tensions, particularly in regions like Russia-Ukraine and the Middle East, continue to heighten risk assessments. This is prompting insurers to scrutinize things like cyber, political, and marine exposure more meticulously.16

For the first time in six years, worldwide insured losses from natural catastrophes surpassed US$100 billion without a single event causing over US$10billion in damages.17 This indicates a broader spread of smaller, yet costly, events. It also underscores a need for the reinsurance industry to closely monitor and reassess underwriting practices as more geographic areas fall into high-risk zones.

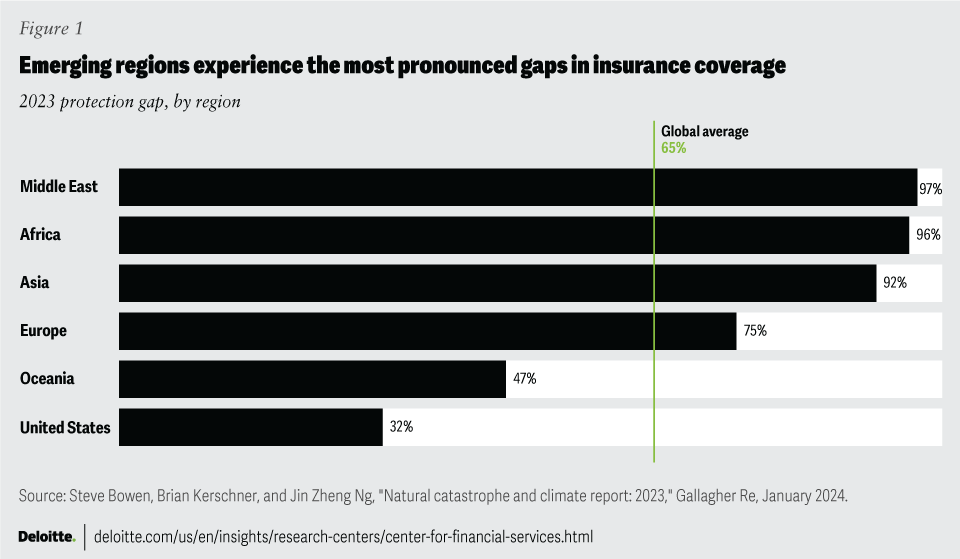

Economic losses from natural catastrophes reached US$357 billion in 2023 globally. Yet only 35% of these losses were insured, leaving a protection gap of 65% or US$234 billion.18 This gap is particularly pronounced in countries in the Middle East, Africa, and Asia (figure 1).

Table of contents

- Insurers adapting to rapid change

- Long-term growth and inclusivity in 2025

- AI leaving insurers on the outside looking in

- Getting data and governance right for AI

- Right talent and culture to capitalize on AI

- Elevating societal purpose in a financially sustainable way

- New global tax requirements

- The road less traveled

To remain viable, insurers implemented higher-than-average price increases across many P&C insurance lines.19 Globally, non-life premiums grew by 3.9% year over year in real terms in 2023, partly because insurers increased rates to offset rising claims costs.20 In the United Kingdom and Australia, for example, personal property and auto insurance premium growth outpaced inflation and disposable income growth over the past three years.21 In Germany and Japan, property insurance premiums exceeded increases in income and inflation, and auto premiums grew more moderately.22

This strategy seems to be improving insurers’ profitability. But for consumers, it could make it more difficult to afford coverage options for damages due to the increasing frequency and severity of catastrophes.

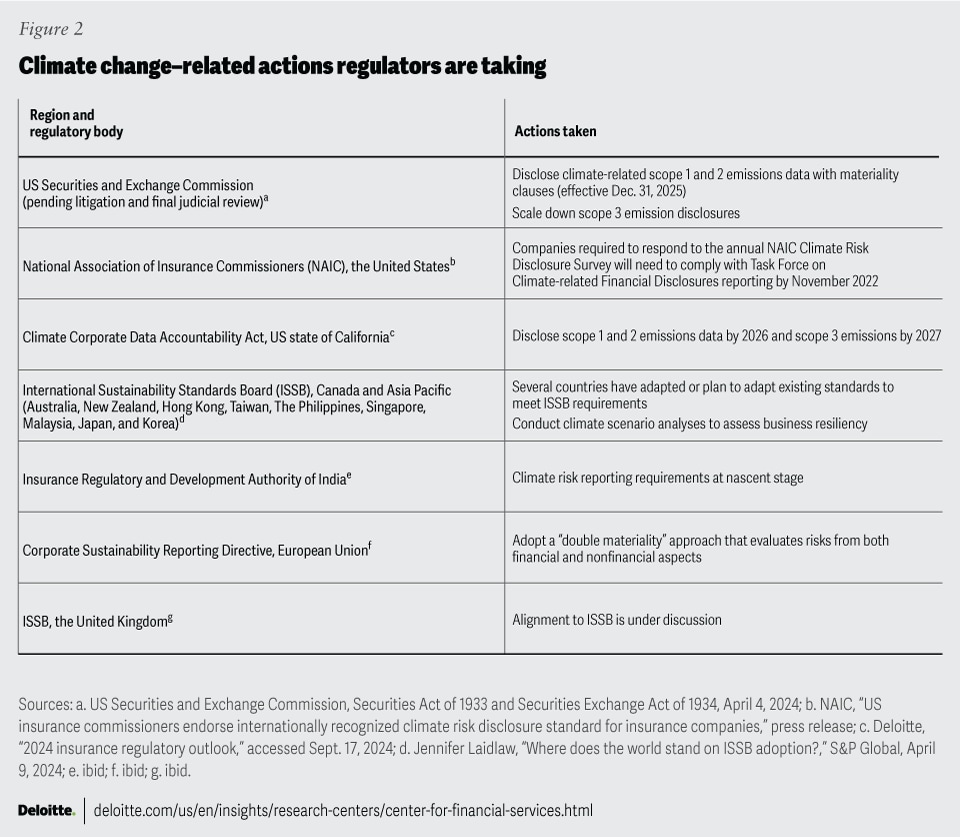

Insurance regulators and several government entities around the world are asking for greater transparency from insurance providers in how they account for climate risks in their investment strategies. They are also focused on making insurance coverage accessible and affordable for consumers, especially those in more vulnerable communities.23

Voluntary disclosures, such as the Task Force on Climate-related Financial Disclosures, the Carbon Disclosure Project, and the Global Reporting Initiative, continue to shape this landscape.24 But recent regulatory updates aim to bolster transparency and investor confidence and provide more robust strategies for assessing progress (figure 2).

There may be reason to be optimistic that non-life sector performance could improve in 2025. The recent surge in claims severity, driven by higher inflation and supply chain shortages, is waning.25 This, combined with rapid growth in written premiums from sizable rate increases and higher investment yields, is expected to provide some relief.26

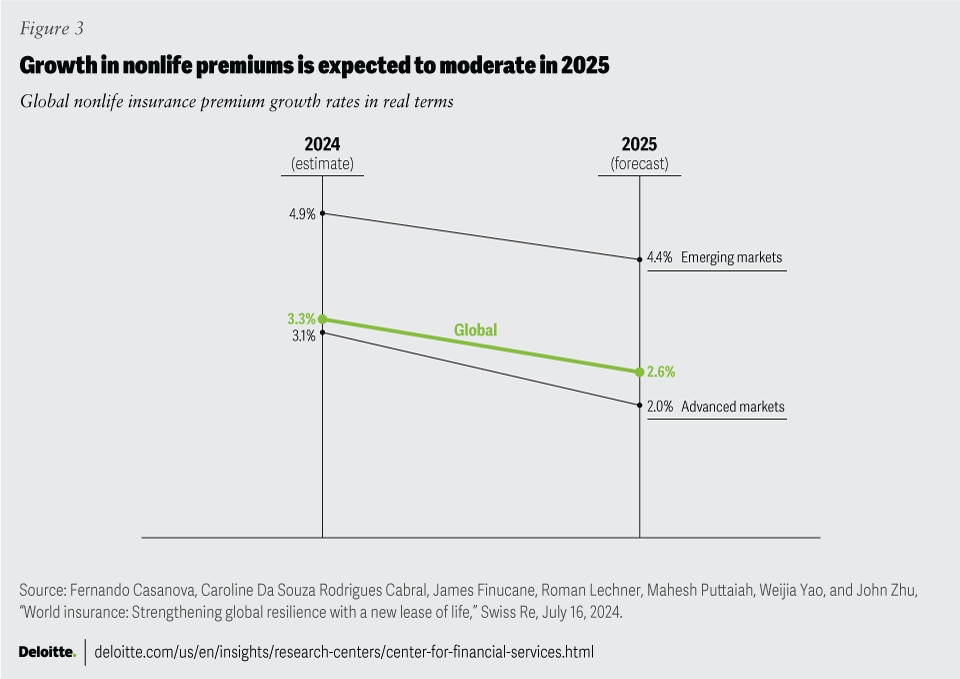

At a global level, estimates suggest that insurers’ return on equity could improve to about 10% in 2024 and 10.7% in 2025.27 Insurance premiums are estimated to grow by 3.3% in 2024, with advanced markets contributing 75% of the expansion in premium volumes (figure 3).28

Profitability is expected to improve in the United States as well. Estimates suggest a reduction in the combined ratio for the non-life sector to 98.5% in both 2024 and 2025, from an estimated 103% in 2023.29 The sector is expected to continue to benefit from deceleration in claims costs because of lower inflation, which decreased to 3% in June 2024 after reaching a peak of 9.1% in June 2022.30

As carriers regain their footing, emerging risks and changing customer expectations could present numerous growth prospects for non-life insurance carriers in 2025.

For example, a recent Deloitte FSI Predictions article revealed that businesses across all industries are investing in and deploying AI,31 and the liabilities arising from its use and development can potentially be massive for non-life insurers.32 The research predicts that by 2032, insurers could potentially generate approximately US$4.7 billion in annual global premiums from AI-related insurance, yielding a robust compounded annual growth rate of around 80%.33

Demand for customer-centric experiences has contributed to the popularity of embedded insurance (distributing insurance policies at the point of sale), which is projected to exceed US$722 billion in premiums globally by 2030.34 Embedded insurance allows insurers to bundle products and offer integrated solutions through partnerships with industries like automotive, retail, and real estate.35 For example, to reach a broader audience, insurers are partnering with real estate companies to offer homeowner’s insurance directly through the real estate’s sales platform. Such partnerships could provide customers quick and easy access to insurance, as well as broaden distribution options for insurers. They also typically require a less significant investment of capital or time compared to build-or-buy alternatives.36

Life and annuity sector

In the L&A sector, persistently elevated interest rates have driven demand for savings-type products.37 In fact, total US annuity sales increased 23% year over year to US$385 billion in 2023, led by a 36% jump in fixed annuities, to US$286.2 billion.38 In the first half of 2024, total US annuity sales rose 19% to US$215.2 billion, year over year, with registered index-linked annuities and fixed-income annuities setting new records.39 Even as the Federal Reserve signals cuts to interest rates, annuity buyers looking to lock in higher guarantees are now driving a further surge in sales.40 Tailwinds from the growing middle class in emerging markets, and declines in pension provisions from governments and businesses are expected to continue to fuel growth in savings products over the next several years.41

While annuities seem to be dominating the headlines, new annualized life insurance premiums, which have set a sales record in each of the past three years, also benefited from an additional 1% growth in 2023, to US$15.7 billion.42 However, in the first quarter of 2024, both total new premiums and total number of policies sold fell 1% year over year.43 Notwithstanding the modest drop, younger demographics (below 50 years of age) are the ones driving life application growth, and social media is a key factor in educating and influencing these consumers about life insurance products.44

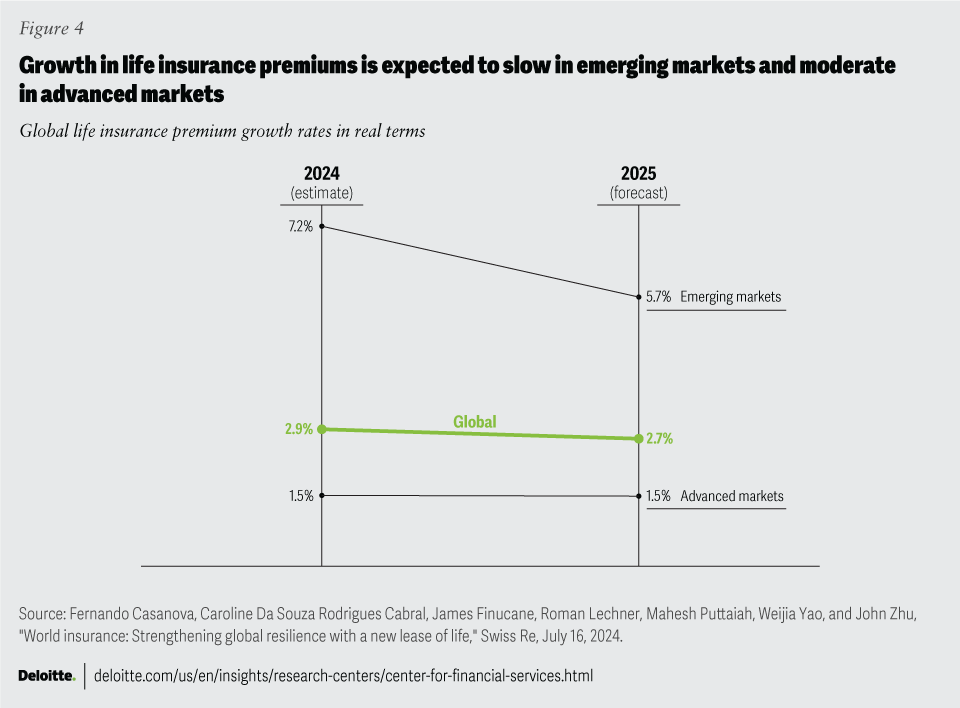

Life premiums are expected to increase 1.5% through 2025 in advanced markets. Strong sales in more emerging markets like China, India, and Latin America could potentially boost premiums by 7.2% and 5.7% in 2024 and 2025, respectively (figure 4).45

Higher interest rate levels are also fueling better investment yields for life carriers, which is expected to boost profitability through 2025.46

While these carriers appear to be enjoying the current environment, they may also recognize that neither the pandemic-fueled interest that boosted mortality product sales nor the higher interest rates that drove interest in savings products are likely sustainable growth drivers. Meaningful transformation may be necessary to help support long-term success.

To achieve the levels of operational excellence and strategic nimbleness that entice both consumers and distributors, many L&A carriers may need to invest in core system modernization, automation, and process redesign initiatives.

L&A core system modernization would not necessarily require replacement or conversion of infrastructure, but an analysis of what the current architecture cannot support, which capabilities may be required going forward, and then prioritizing where to invest. One solution may be to invest in an application programming interface-based architecture, which can enable digital distribution and give carriers more flexibility with distribution channel interactions.

To further improve their competitive advantage with intermediaries, carriers may consider providing predictive models to brokers and advisors. This can help differentiate the distribution experience by enabling more effective targeting of prospects who are most likely to purchase L&A coverage.

There are vast unmet needs for global life insurance and savings: In the United States alone, the mortality coverage gap is an estimated US$25 trillion,47 while the current global retirement savings gap is around US$70 trillion.48 Meeting these needs could be a large opportunity for insurers that effectively leverage digital advances.

Insurers that have these capabilities could make it easier for consumers to learn about and buy L&A products and make selling these policies to lower-income populations more profitable. For example, currently in Brazil, a key development is helping to democratize life insurance. Digital banking in the region has increased the banked population in the past decade, contributing to higher financial inclusivity. These banks are now adding life insurance to their service offerings, enabling millions to have access to these products for the first time.49

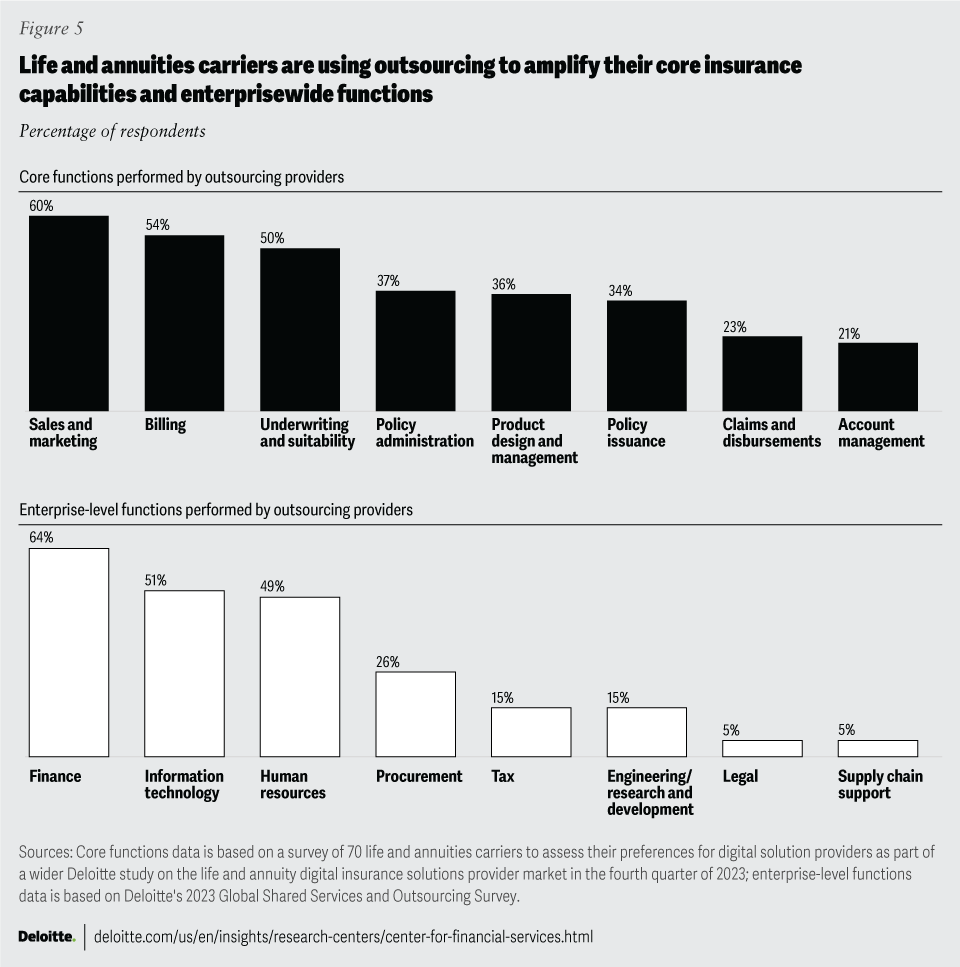

Moreover, by modernizing their operating models by breaking down silos and becoming more customer- and product-centric, carriers can improve their ability to respond quickly to changes and disruptions in the market. Since so many business-critical systems and processes span various functions and ancillary applications, any inefficiencies can slow the pace of business and directly impact customers and distributors. Investments in process redesign and straight-through processing can improve experiences, reduce costs, and help enable scalable, profitable growth. Many carriers are also turning to outsourcing; they are using managed services and third-party administrators to help improve operational efficiency and reduce costs (figure 5).

Life and annuity carriers are experiencing record-high sales volumes. Still, these results could be even better if carriers were able to penetrate more of the global market. Absent transformation that may be needed to minimize the customer and distributor impact from back-office inefficiencies and aging core systems, carriers will likely be challenged to grow current levels of profitability, especially during periods of disruption and fluctuating demand.

Group insurance

Relatively high persistency (renewal premiums) and elevated wage inflation have helped group insurance performance results over the past few years, reducing reliance on new sales growth. But diminishing persistency due to a slower pace of employment growth is expected for 2025. Deloitte economists forecast US unemployment to rise above 4% by 2026 and the employment cost index to decline to 3.3% in 2025, from 4% in 2023.50 Group carriers may need to consider some alternative avenues for growth in 2025.51

Group life insurance sales for the fourth quarter of 2023 totaled US$857 million, an 8% increase year over year, while the annual growth rate was 6%.52 However, in the first quarter of 2024, total new premiums for workplace life insurance declined 2% year over year.53

Supplemental health insurance sales, which include accident, critical illness and cancer, and hospital indemnity, posted a 5% annual growth in 2023, year over year,54 and an increase of 3% in the first quarter of 2024, compared to the same period last year.55 One survey revealed that 86% of respondents consider it very important for employers to offer them supplemental insurance benefits to protect against the loss of income or expenses arising from an unexpected event.56

Disability insurance had mixed results: Sales increased by 8% overall in 2023 compared to 2022,57 but decreased by 12% year over year in the first quarter of 2024.58 However, long-term disability incidence rates continue to trend downward,59 which could be due to wage inflation remaining relatively high. This may be enticing workers who might otherwise opt to claim disability benefits to do their best to stay in the labor market.

As employers across industries continue to face substantial competition for talent, more than 70% of respondents to a 2023 US consumer sentiment survey say their company’s benefits package is critical to attracting and retaining the best employees.60 Likely because of this high interest, 51% of respondents to the same survey said their company will increase benefits offerings in the future.61 To take advantage of this potential uptick in demand for employee benefit offerings, carriers will likely need to find ways to stand out in an intensely competitive environment.

To differentiate themselves, carriers could consider developing alignments with ecosystem participants that can provide advanced administration platforms, as well as with insurtechs that offer skills, capabilities, and data sources that group carriers do not otherwise have access to. For example, in July 2023, Prudential Financial announced a partnership with Nayya to harness AI and data science to help employees make better workplace benefits decisions during open enrollment.62

Could artificial intelligence leave insurers on the outside looking in?

One important piece of insurers’ transformation journeys across all sectors could be effectively embedding advanced technology capabilities into their business models. Insurers have been working with AI tools for several years. However, until very recently, many insurance leaders may not have seen the need to focus on strategically embedding AI throughout the organization.

But following the release of multiple publicly available gen AI tools over the past two years, AI seems to be having its “iPhone moment."63 Free public access and increasing curiosity is driving experimentation and adoption across industries and among consumers as they begin to realize the true transformative capabilities of these tools. Even for the most risk-averse insurers, gen AI is at an inflection point, driving multiple commitments and investments in the AI space.

In fact, in a June 2024 survey of 200 US insurance executives conducted by the Deloitte Center of Financial Services, 76% of respondents said that their organization has already implemented gen AI capabilities in one or more business functions.64 Many insurers in Asia Pacific are also leaping ahead with AI and gen AI implementation initiatives, primarily driven by favorable technical talent availability and cultural acceptance in the region.65 One example is Hong Kong–based life insurer AIA Group, which plans to transition from investing in foundational tech and data transformation to embedding intelligence, including gen AI, into distribution, operations, and customer service.66 Moreover, Shenzhen-based insurer Ping An owns the second highest number of patents on gen AI technology in the world, only behind Chinese tech giant Tencent.67

While many insurers remain in the proof-of-concept stage, some are starting to integrate gen AI into prioritized areas like claims and customer service. These use cases may provide better risk-reward and scalability opportunities in the short term, both from a regulatory perspective and acceptance within insurance organizations. In fact, a Deloitte Center for Financial Services (DCFS) survey of insurance executives found that the areas with the highest number of gen AI implementations to date were in distribution, risk management, and claims handling.68

For an impactful approach to scaling, it is important for insurers to have the right value levers. Over the next few years, realizing efficiencies and enhancing experience (for both customers and employees) could turn out to be more important than measuring direct business growth. Most respondents surveyed by the DCFS said they are using profitability, efficiency in handling customer queries, and employee satisfaction scores as key success metrics for assessing current and future gen AI initiatives.69

Getting data and governance right could be foundational to AI strategy

Insurers may not be able to realize business value without accurate underlying data to train and feed the models. Respondents to the DCFS survey revealed that data security and privacy, data quality, and data integration (internal and external) were the top challenges for implementing gen AI adoption at scale.70

While insurers have prioritized building the data foundation over the last decade to enable analytics and digital capabilities, the focus is now on enabling their data ecosystems to be able to support and scale AI. This includes fostering a convergence that supports both real-time and batch environments. There is also a growing trend toward developing data products, which means establishing a data environment to support use cases such as pricing optimization, fraud detection, segmentation, churn, and lifetime value. These data products are facilitated by data mesh architecture, which enables insurers to transition away from massive data warehouses toward a more compartmentalized approach that is tailored to specific business needs and can underpin scaling AI.

Effective governance for AI includes robust data management and control. As AI adoption exposes the organization to a myriad of risks—from hallucinations to propagating biases in data—insurers are actively working to thoroughly understand their data sources and inventory. Focusing on governance and data management could be critical for compliance, while developing frameworks of transparency and accountability can help foster a culture of responsible AI use.

Getting the right talent and culture to capitalize on AI opportunities

Developing this culture of accountability among the workforce could be crucial: Employees already perceive employers to be as much as 2.3 times less empathetic and human when AI tools are offered.71 The success of AI initiatives relies on having buy-in from the workforce, so as insurers develop their strategies, they should emphasize human sustainability, where organizations choose to focus more on how they can help their employees rather than how their employees can benefit their bottom line.72 Therefore, AI initiatives designed to help employees do their jobs with less friction are likely to be successful ones.

When asked about organizational readiness for gen AI adoption in the DCFS survey, respondents said they are least prepared in terms of talent availability and existing talent skillsets compared to other readiness factors.73

As expected, respondents said they are rethinking their talent strategies and organizational structures to adapt to the new AI reality. Although many insurers are already undergoing long-term organizational structural changes that can complement AI efforts, such as shifting to skills-based frameworks and promoting cross-functional collaboration, they are also focusing on some areas to prepare their organizations for AI in the short term.

The need for more technical talent is clear. In the DCFS survey, prioritizing candidates with digital literacy and AI knowledge for new job openings was the top-ranked change that respondents are making in terms of how they manage and hire talent to prepare for the long-term adoption of AI,74 Beyond technical skills, insurers will likely also need to hire for uniquely human capabilities such as imagination, curiosity, empathy, and analytical thinking to differentiate themselves because rote tasks could become increasingly automated.

However, relying on new talent won’t be enough. Many insurers are also focusing on developing their existing internal talent, in which AI can be an educational aid itself. For example, Zurich is using analytics to assess workers’ current skills and future skill requirements to curate learning and development opportunities.75 Insurers may also choose to rely more heavily on outsourcing and shared services if they are unable to attract and develop their own internal talent in the short term.

As insurers continue to invest heavily in AI technology, they may need to complement it with investments in talent. According to Sandee Suhrada, principal at Deloitte Consulting LLP, “In the AI space, technology and talent are two sides of the same coin. Insurers are building AI technology for the talent, by the talent.”

How can insurers elevate their societal purpose in a financially sustainable way?

At face value, it may seem that insurers could be forced to confront the choice between doing well or doing good. But this does not necessarily need to be the case.

Over the past few years, the rise in extreme weather events, combined with high inflation raising the cost to repair vehicles, homes, and commercial real estate,76 pushed claims losses to unprofitable levels in related lines of business.77 To return to profitability, many insurance providers hiked premiums in impacted lines; some even retracted coverage altogether.78 Faced with fewer options and rising costs of coverage, more and more customers are now at risk of being underinsured or uninsured.79

While this scenario may seem dire, insurers who innovate and collaborate could use this as an opportunity to foster resilience and sustainability and create a better balance between profitability and equity. Emerging technologies and alternative data sources are now available to help stem the mounting losses, which can benefit many stakeholders. Insurers should ensure these technologies and data sources are used properly and with transparency to build trust and be recognized as stewards of purpose.

However, a perceived lack of transparency around the collection and use of some of the data currently being included in underwriting decision-making is becoming concerning to both consumers and regulators. For example, while consumer uptake of telematic devices that monitor driving behavior has been underwhelming since its inception in some regions,80 it is now possible for insurers to harvest this data from less obvious sources, such as apps that drivers already have on their phones.81 They can then use this data to underwrite policies, often without full transparency to the driver.82

While these data points can generate more precise underwriting, to help minimize mistrust among consumers and regulators, insurers should be transparent and disclose the information they are using to rate drivers. Insurers can also consider incentivizing mitigation strategies, such as issuing a driving score (similar to a credit score) to policyholders. These scores can be raised when driving behavior improves and then reflected in pricing.

Moreover, as technology evolves, insurance companies should work to free their underwriting models of all inherent bias. This could be particularly important where those preconceptions adversely affect vulnerable communities already plagued with affordability and access challenges due to their location. Regulators are already looking into this. For example, Colorado is currently developing a regulatory framework for insurers to help prevent bias and discrimination in AI models.83

Insurers are also recognizing the importance of conserving natural capital to drive down claims costs. They may need to guide clients to move away from a linear economy (take-make-waste) to a circular economy approach (reuse-transform-recycle). Doing so can help foster an ongoing product life cycle,84 ensuring that the parts used to repair damaged assets stay in circulation for a longer time. For example, some European insurers allow auto vendors to reuse spare parts for repairs, making the process environmentally friendly as well as economical.85

Insurers could further incentivize supply chain partners to use renewable raw materials and recycle end products, as well as convert their own insurance products into services like usage-based auto insurance, which tailors pricing based on the actual driving behavior of the policyholder. They can also consider giving premium discounts to clients in the construction and real estate sector that apply green chemistry, an approach that aims to prevent or reduce pollution and improve overall yield efficiency.86 These discounts could be applied across the life cycle of construction products, including its design, manufacture, use, and ultimate disposal, since it could reduce risk exposure for insurers.

For risk elements that insurers have less influence over, like climate change, insurers can influence, collaborate, and incentivize mitigation strategies to ensure more profitable and equitable coverage. One program in Alabama offers homeowners discounts on their insurance policies when they follow specific standards for construction or retrofits.87 In Mississippi, a bill pending in the state House could create a trust fund that could provide grants to homeowners for fortifying their homes against severe weather or building safe rooms for tornadoes.88

In a recent Deloitte FSI Predictions article, analysis revealed that if insurers, in partnership with government entities and policyholders, invest US$3.35 billion in residential dwelling resiliency measures, the two-thirds of US homes that are not currently built to adopt and follow hazard-resistant building codes can become resistant enough to reduce many weather-related claims losses. This could save insurers an estimated US$37 billion by 2030.89

For life insurers, climate change impacts health/morbidity and mortality in a more subtle way. Factors such as poor air quality due to increased pollution or wildfire smoke can exacerbate respiratory and cardiovascular conditions, leading to higher morbidity and premature mortality.90 To help minimize the overall risk profile, insurers, in partnership with other stakeholders, could explore collaborative investments in communities residing in these detrimental living conditions and promote health awareness and the benefits of early prevention of diseases. For example, several insurance companies in India that offer coverage for diseases caused by pollution, like asthma and chronic obstructive pulmonary disease, also include the cost of air purifiers and specialized respiratory medications.91

Regulators could introduce policies that encourage insurers to underwrite certain emerging risks like renewable energy technology. Government support and incentives could potentially lower the capital charge on assets or liabilities associated with renewable energy projects, benefiting society and potentially lowering insurers’ risk profile.92

Many of the risk mitigation and incentivization strategies being employed are still in their nascent stages. Insurers that are already experimenting have the ability to make adjustments to the way data is collected, processed, and used. As regulatory bodies, insurers, vendors, data suppliers, and policyholders get aligned, insurers that can transform traditional mindsets and processes in this challenging environment can take advantage of unprecedented opportunities to more effectively balance profitability with purpose.

The US National Association of Insurance Commissioners announced its strategic priorities early this year, launching a state-level data collection drive to better understand localized protection gaps in property insurance markets. These insights can provide guidance to state insurance regulators to address climate risk resilience and increase access to consumers at a national level.93

In the insurance industry, where 75% to 90% of emissions are Scope 3 (indirect greenhouse gas emissions that occur outside an organization's direct control), direction on measurement is also critical.94 The Partnership for Carbon Accounting Financials has released guidance on measuring insurance-associated emissions for commercial and personal motor lines, but it could require insurers to collect vast amounts of data that is often not readily available.95 Calculating financed emissions also presents similar challenges, in particular for life insurance companies, which tend to have a large long-term investment profile.

As sustainability programs evolve, they are shifting from quantity to quality. Insurance companies are increasingly focusing their resources on reporting what’s most crucial to their organization rather than striving to cover everything.96 Moreover, the industry could see a shift from siloed compliance reporting to embedding sustainability into business strategy decisions. Introducing new metrics, such as implied temperature rise97 and portfolio warming potential98 —designed to assess and manage climate-related impacts of investment portfolios—involve complex, multidimensional data analysis. Therefore, they are expected to require long-tail investment portfolios to develop new modeling capabilities.99

Could new global tax requirements impact organizational structuring considerations for insurers?

Profits for insurers operating in low-tax jurisdictions may be impacted as a result of new global minimum tax rules. Pillar Two tax laws are expected to take effect in many jurisdictions in Europe and across the world in 2024. Many insurers are now focusing on compliance, reporting, and scenario planning.

Many countries have already passed or introduced legislation that would implement Pillar Two tax rules, which require multinational organizations with €750 million or more in annual revenues to pay a minimum tax of 15% on net income earned in each country where they operate, adding an additional burden to insurers’ bottom lines.100 Even if an entity’s jurisdiction of domicile has not adopted these rules, which is currently the case for insurers in the United States, a tax liability could still be due if they operate in a different jurisdiction that has adopted them.

Bermuda, which enacted a Corporate Income Tax of 15% on businesses that are part of multinational enterprise groups with annual revenues of €750 million or more, serves as an example of the impact Pillar Two is having on jurisdictions that have historically imposed low or no taxes.101

To respond to these new rules, insurance tax departments should understand the rules and model potential tax impacts. They may also want to analyze corporate restructuring considerations that could help mitigate adverse impacts. Even those insurers that may not see an increased tax liability as a result of Pillar Two could be subject to these rules and may need to invest resources toward reporting and compliance.

As a new global tax regime, many questions remain about how individual jurisdictions could implement and draft new regulations in accordance with Pillar Two. Therefore, insurers may need to stay updated on new rules and requirements to remain in compliance as things evolve.

In the short term, data wrangling, reporting, and compliance will likely be the biggest challenges. Although Pillar Two is nominally a tax reform, finance, legal, IT, and other impacted stakeholders may need to educate themselves on these new rules and the potential implications to their functions. These impacted units may need to collect, organize, and share financial information, operational data, and transfer pricing data from multiple sources—and, potentially, multiple geographies. These activities reinforce the potential need to invest in modern and centralized data collection capabilities.

It’s too early to assess the full impact of this new tax regime. However, the erosion of tax benefits could lead to pressure for higher pricing and greater cost optimization. And while reporting and compliance could be a significant effort in and of itself, some insurers may opt for more drastic restructurings because of these new rules, either through choice of domicile or overall corporate structuring.

The road less traveled may be trickier to navigate but more rewarding

The only constant is change. And when change is coming from many directions—customer expectations around products and experiences; emerging technologies reshaping many aspects of our lives; growing climate-related risks; tax laws; evolving regulatory scrutiny; and macroeconomic and geopolitical volatility—the insurance industry may have to pivot in the way it does business to keep pace.

The journey from underwriting via the rear-view mirror to helping consumers proactively mitigate risks and offering protection more inclusively could require transformative strategies. It could also require investments to help improve agility, form strategic alliances, and cultivate the workforce of the future while sustaining profitable growth.

For insurers, their policyholders, and society at large, the bottom line is that the best claim is the one that never happens. While total elimination of risk for society may not be achievable, the insurance industry now increasingly has the tools to help bring this pipe dream closer to fruition. In fact, 2025 could potentially be the year carriers consider taking the road less traveled to position themselves for long-term success.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}