Analysis

Divestiture M&A news: 2015 Q4 recap

Global divestiture market strength continued in 2015

For some companies, divestitures and carve-outs are part of an important strategy to refocus their businesses and improve overall performance. Divestiture M&A News provides Deloitte Corporate Finance LLC insights and market data analysis that shed light on US and global divestiture trends.

Explore content

- Divestiture activity

- Industrials lead divestiture

- Average divestiture EV/EBITDA multiples increase

- Strategic buyers drive the majority of carve-out deals

- Meet the authors

Divestiture activity remains strong globally

Trends include:

- The 12,701 global divestitures completed in 2015 represented 39 percent of worldwide M&A volume in 2015, which was a slight decline from 2014, but greater volume than in either 2012 or 2013

- Divestiture activity has historically remained strong during recessions and market downturns relative to broader M&A activity, with volume relative to non-divestiture-related M&A increasing in each of the last three recessions (’90-’91, ’01, ’08-’09)*

* Thomson Financial

Download PDF

Industrials lead divestiture deal volume

Trends include:

- With 438 divestitures announced in Q4 2015, industrials has been the most active industry in carve-out activities*

- The top three industries, industrials, real estate, and financials accounted for more than 36 percent of total volume

- The total announced value of 2015 Q4 divestitures was $409 billion*

* Thomson Financial

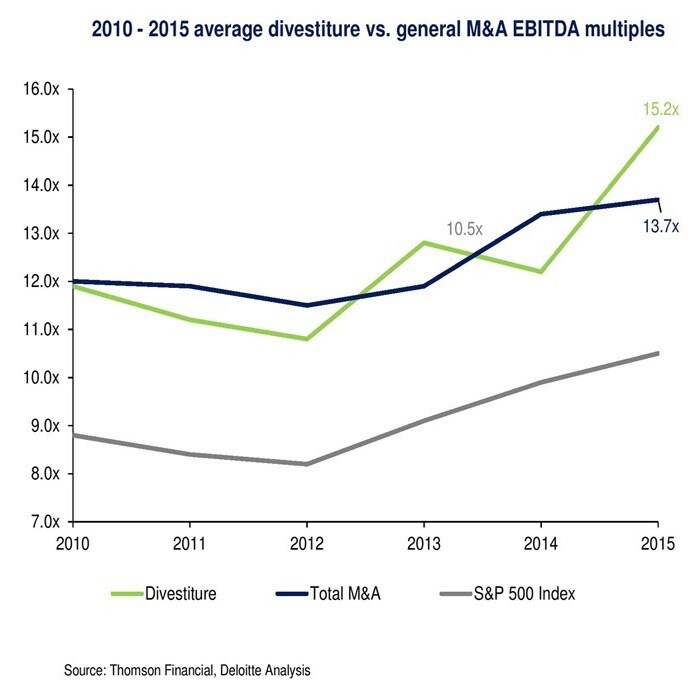

Average divestiture EV/EBITDA multiples increase

Trends include:

- Average disclosed EV/EBITDA multiples increased significantly from 2014 to 2015 due to higher average valuations and lower earnings*

- For the second time since 2010, average EBITDA multiples for divestitures exceeded average transaction multiples for traditional transactions

- Divestiture EBITDA multiples also continued to exceed the average EBITDA trading multiple for the S&P 500 Index, highlighting the valuation premiums divestitures often deliver compared to businesses as a whole

* Thomson Financial

Strategic buyers drive the majority of carve-out deals

Trends include:

- Strategic sponsors remained the largest purchasers of carve-outs, representing 64 percent of all buyers in 2015

- Over the past five years, financial sponsor purchases have increased by 12 percent while strategic buyer activities have decreased by 5 percent, indicating that financial sponsors are playing a more important role in the global divestiture market

This newsletter is a periodic compilation of certain capital markets information. Information contained in this newsletter should not be construed as a recommendation to sell or a recommendation to buy any security. Any reference to or omission of any reference to any company in this newsletter shall not be construed as a recommendation to sell, buy, or take any other action with respect to any security of any such company. We are not soliciting any action with respect to any security or company based on this newsletter. This newsletter is published solely for the general information of clients and friends of Deloitte Corporate Finance LLC. It does not take into account the particular investment objectives, financial situation, or needs of individual recipients. Certain transactions, including those involving early stage companies, give rise to substantial risk and are not suitable for all investors. This newsletter is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Prediction of future events is inherently subject to both known risks, uncertainties, and other factors that may cause actual results to vary materially. We are under no obligation to update the information contained in this newsletter. We and our affiliates and related entities, partners, principals, directors, and employees, including persons involved in the preparation or issuance of this newsletter, may from time to time have “long” and “short” positions in, and buy or sell, the securities, or derivatives (including options) thereof, of companies mentioned herein. The companies mentioned in this newsletter may be: (i) investment banking clients of Deloitte Corporate Finance LLC; or (ii) clients of Deloitte Financial Advisory Services LLP and its related entities. The decision to include any company for mention or discussion in this newsletter is wholly unrelated to any audit or other services that Deloitte Corporate Finance LLC may provide or to any audit services or any services that any of its affiliates or related entities may provide to such company. No part of this newsletter may be copied or duplicated in any form by any means, or redistributed without the prior written consent of Deloitte Corporate Finance LLC.

Meet the authors