Eurozone economic outlook A long and winding road

6 minute read

24 October 2020

The Eurozone has experienced a summer of deep recession, but recent sentiment indices signal an encouraging autumn. Still, returning to precrisis levels will take time and the recovery paths will likely differ across industries and countries.

A recession-filled summer

The COVID-19 crisis and the accompanying restrictions put in place hit the Eurozone economy extremely hard in the second quarter. The Eurozone experienced the strongest recession since its foundation—the economy contracted 11.8% in the second quarter of 2020, more than three times the drop the union had experienced in the worst quarter during the global financial crisis.

Learn more

Explore the Economics collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

Although all countries have suffered, there are some pronounced differences. Among the biggest member countries, Spain took the strongest hit with its GDP shrinking by 18%. France (down 14%) and Italy (down 13%) too suffered extreme reductions in economic activity in the second quarter, while Germany (down 10%) saw a dramatic, yet smaller, contraction.1 The differences in economic performance depended to a very large degree on the success of controlling the spread of the virus, and the length and severity of the lockdown.

Consumer spending and its sectoral impact

The contraction in the second quarter was mainly due to consumer spending. Of the 11.8% drop in GDP in the second quarter, 7 percentage points stemmed from the strong reduction in consumption. Private consumption declined most visibly (down 12.4%) while public spending also decreased slightly (down 2.6%). The decrease in public spending seems counterintuitive as governments introduced massive fiscal stimulus. However, a big share of the government support packages will come into effect only in the third and following quarters. The strong decline in consumption spending was mainly due to two factors. First, the demand for durable goods, such as motor vehicles, collapsed due to extremely high anxiety among consumers and a drop in real disposable income. Second, the containment measures aimed to decrease the spread of the virus forced households to reduce their spending in some categories, such as holidays, travel, and restaurants, as these goods and services were simply unavailable.

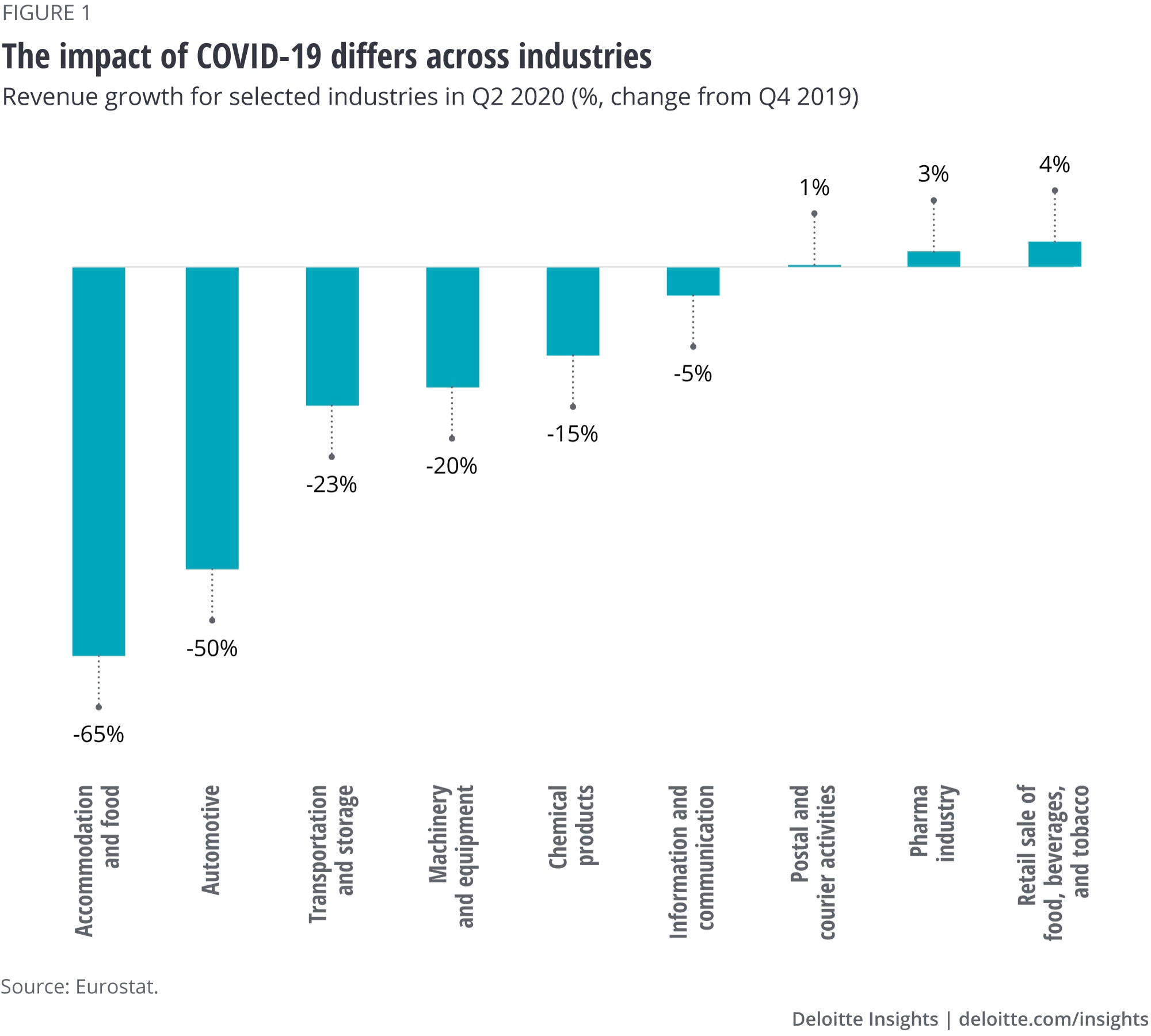

The sudden decline in consumption caused many consumer-dependent industries to shrink strongly. The accommodation and food industry as well as the automotive industry were particularly hit in the second quarter (figure 1).

On top of the reduced domestic demand, many export-driven sectors, such as machinery and equipment, and chemical products, suffered from a slump in foreign demand as well as disrupted global supply chains. In total, the Eurozone’s exports of goods and services declined by 19% in the second quarter of the year.2 However, some sectors, such as pharmaceuticals and food retail, proved to be much less dependent on the business cycle and managed to keep their revenues at least stable.

The labor market

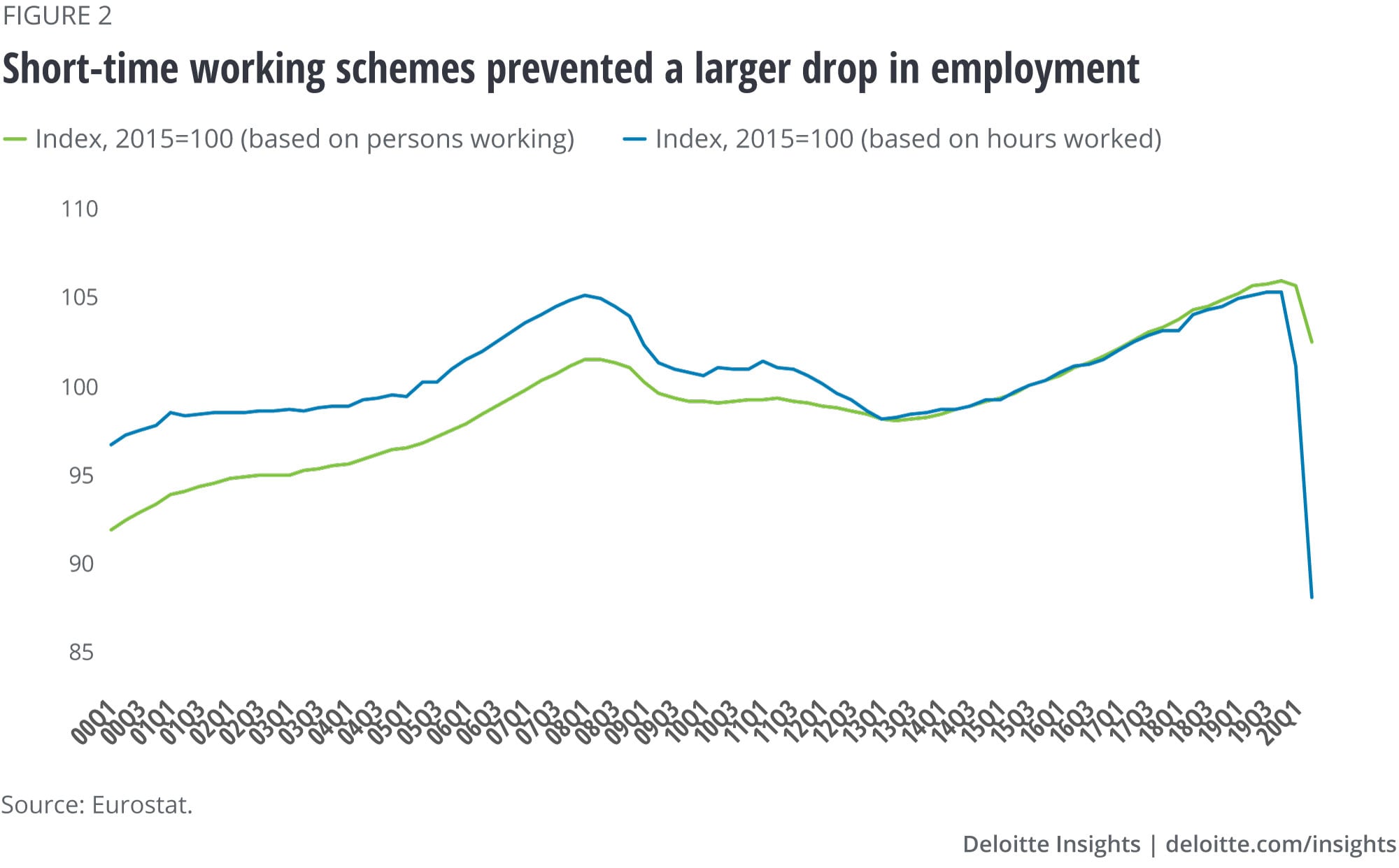

Despite the sharp drop in consumption, economic policy measures softened the impact on the labor markets. In many European countries, short-time work schemes, financed by the state, were among the key instruments put forward to bridge shortfalls in activity in an effort to prevent mass unemployment while stabilizing demand.

In all four of the largest Eurozone countries short-time work benefits significantly buffered the impact of COVID-19 on households’ disposable income. Early estimates suggest that especially in France and Italy the share of employees in short-time work or temporary layoff this summer was substantial—these schemes covered more than 40% of employees. In Germany and Spain, the share was smaller, though still substantial with around 20% of employees covered.3

Employment data shows the extent to which these schemes affected the labor market. While the Eurozone employment based on hours worked declined 16% in the second quarter 2020 compared to the last quarter of 2019, employment based on persons working decreases by only 3% (figure 2). So, employees stayed in work, but worked substantially fewer hours.

Nevertheless, differences between countries remain. While employment only dropped by 1% in Germany in the second quarter of 2020 compared to the fourth quarter of 2019, the decline was 3% in Italy and 8% in Spain. This crucially affects the disposable income available to households, job uncertainty, and consequently, consumer confidence.4

Consumer confidence supported by fiscal measures

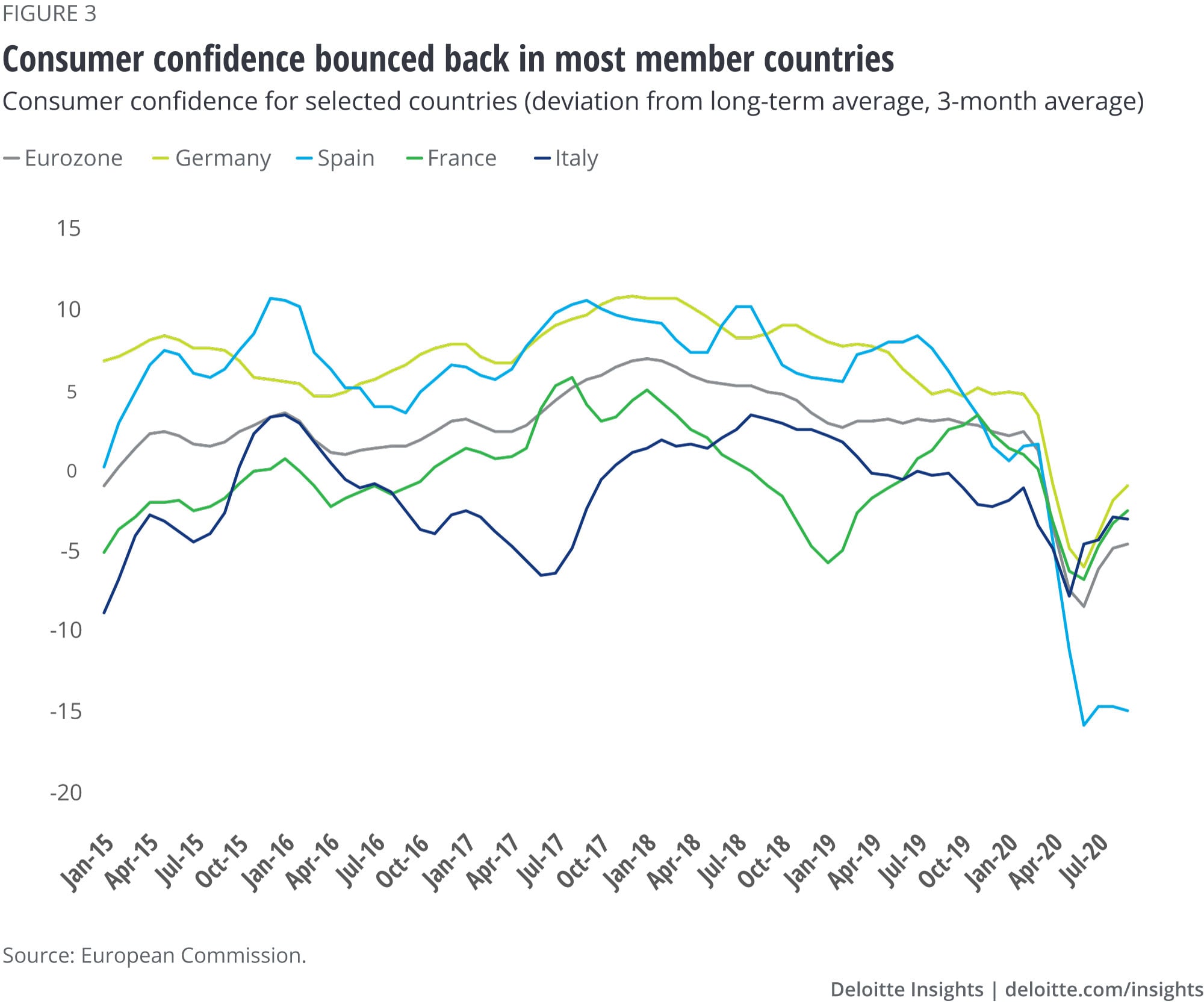

Consumer confidence in the Eurozone has picked up since July but remains well below the long-term average (figure 3). While in Germany, France, and Italy consumer confidence has partially bounced back, in Spain it remains close to unchanged, possibly reflecting high infection rates and rising unemployment.

The data from the Deloitte State of the Consumer Tracker that tracks the monthly movements in consumer behavior across the world suggests that health and financial worries directly affect consumer sentiment. While households in Spain still feel considerably concerned about their physical health as well as upcoming payments, consumers in France and Germany feel relatively more optimistic about their physical and financial health. In Italy, health concerns are below the European average, but many households are still delaying large purchases.5

Business sentiment on the upswing

Despite the fact that there are still many COVID-19–related restrictions in place or that have been reintroduced in response to rising infection rates, business sentiment has significantly recovered from its low over the summer. The European Commission’s economic sentiment indicator is rising steadily but remains below the long-term average,6 while the Purchasing Manager Index indicates economic expansion since July.7 Sentiment has particularly improved in the manufacturing sector, which benefited from an improving export climate, while many services sectors—especially travel agencies, accommodation as well as food and beverage services—still suffer from the ongoing restrictions and low demand.

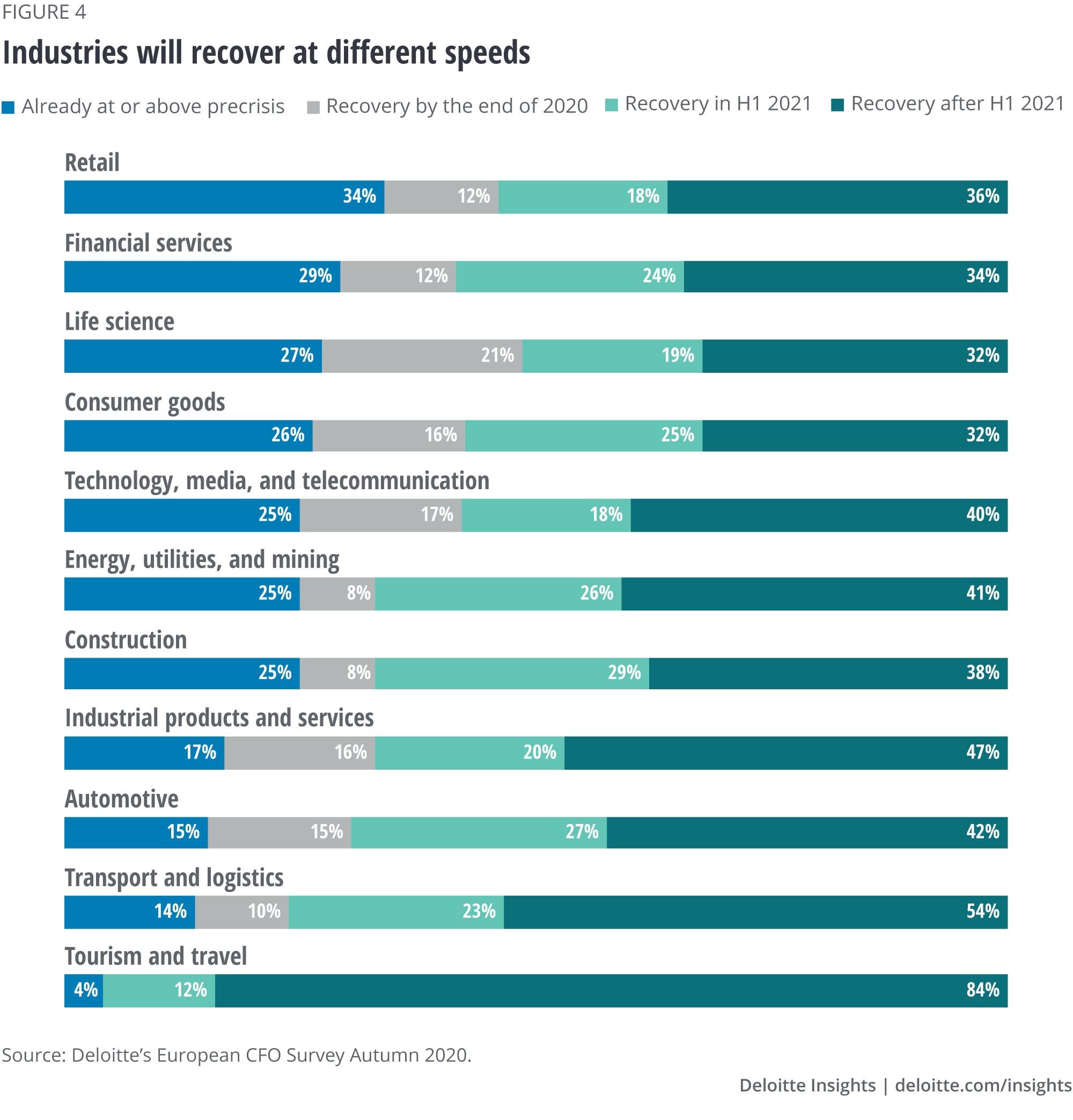

The current Deloitte European CFO Survey confirms the generally more positive outlook, but also the divergence between sectors (figure 4). Survey data reveals that revenue generation at many firms in the retail, consumer goods, and technology sectors has already returned to the precrisis levels. In contrast, a majority of companies in the automotive and industrial products sectors expect to recover by the end of the first half of 2021, while most of the transport and travel sector will likely recover only after 2021.8

Signal of hope in autumn

The recent pickups in consumer and business sentiment suggest that the Eurozone economy is currently recovering and growing substantially, at least in comparison to the previous quarter. In the third quarter, many sectors will likely make up for some—but not all—of the losses that occurred in the first two quarters.

On a country level, the gradual lift of restrictions likely benefitted all major member economies. Since Spain and France experienced the biggest drop in economic activity, we expect these two economies to grow by 12% and 14%, respectively. In Italy and Germany, an increase of output by 7% and 5%, respectively, seems likely.9 While these growth numbers sound impressive, they will not be enough to make up for the large drops in activity in the first two quarters, i.e., the Eurozone remains well below its precrisis levels of economic output. However, these pickups in activity are higher than what was expected a couple of months ago, which shows that the Eurozone economy has the potential to recover robustly, provided the infection rates can be contained.

Prepare for an uneven recovery

Recently, however, almost all big member states have experienced rising infection rates as well as new hot spots, followed by a tightening of restrictions. European governments are determined to prevent a second lockdown, but uncertainty will likely accompany the recovery for a prolonged period. Until a vaccine is available, contact-intensive service sectors will especially suffer.

This uncertainty weighs on business investments more generally, and the still-ongoing health crisis in some of the Eurozone’s most important export markets will likely prevent a fast recovery of exports to precrisis levels. How fast the Eurozone economy will recover depends therefore to a large degree on the consumers and indirectly on the labor markets.

The recovery in the third quarter is more than welcome news for the Eurozone, nevertheless, but it is not difficult to identify many downside risks. In any case, given the differences in recent business and consumer sentiments across industries and countries, the recovery is likely to proceed at different speeds in different Eurozone countries and sectors.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting, and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Get in touch

- Alexander Börsch

- Director

- Deloitte & Touche GmbH

- aboersch@deloitte.de

- +49 (0) 89290368689

More from the Economics collection

-

-

Emerging Markets Outlook Article3 years ago

Emerging Markets Outlook Article3 years ago -

India economic outlook, April 2024 Article11 hours ago

India economic outlook, April 2024 Article11 hours ago -

State of the US Consumer: April 2024 Article11 hours ago

State of the US Consumer: April 2024 Article11 hours ago -

Asia’s economic recovery Article3 years ago

Asia’s economic recovery Article3 years ago -

The long and short of short-time work amid COVID-19 Article3 years ago

The long and short of short-time work amid COVID-19 Article3 years ago