The large Nordic banks1 continued their great run in the first quarter of this year with an average return on equity (ROE) of 15% and a cost-to-income ratio (C/I) below 40%. All the banks delivered above 10% ROE and had a C/I below 50%. These are remarkable numbers, especially when taking into account that the banks’ average Common Equity Tier 1 ratio (CET1) was above 18%, which is 4.5% above the regulatory minimum requirement and much higher than that of their European, US and Asian peers.

.PNG)

Chart 1: The key financial figures for Q1/2023.

Source: The sample banks’ Q1/2023 interim reports.

FX rates as of 31 March 2023. Source: https://www.ecb.europa.eu/stats/policy_and_exchange_rates/html/index.en.html.

Chart 2: The average CET1% of selected banks in the Nordics, and their peers in Europe, the US and Asia.

* Santander, Deutche Bank, BNP Paribas, UBS, Barclays, HSBC

** JPMorgan Chase, Bank of America, Goldman Sachs, Morgan Stanley, Wells Fargo, Citigroup

*** DBS, Bank of China, MUFG Bank, State Bank of India, KB Financial Group

Source: The sample banks’ Q1/2023 interim reports.

The main reason for the strong results was the significantly higher net interest income (NII), which was up by double digits in percentage points for all the banks and by a staggering 84% and 77% for OP and Swedbank, respectively. Expenses were up as well, but less than income, resulting in so-called positive jaws (income growth > expense growth) that is a common mantra right now with many of the banks’ external messaging. Finally, as loan loss provisions remained at low levels, all the banks reported very high profitability in Q1/2023.

Key events in the quarter

The global banking market went through major turbulence in the quarter following the collapse of a few regional US banks, most notably Silicon Valley Bank2, and the takeover of Credit Suisse by its rival UBS3. While the quarterly announcements of all the large Nordic banks emphasised that these events had no impact on their operations, the global stock markets disagreed as most bank stocks fell significantly upon the news. This reminds us of the global connectivity of the banking system and the importance of the banking reforms introduced since the Great Financial Crisis (GFC). But this also highlights the prevalence of the contagion effects within the system and the fact that bank bankruptcies still require extraordinary government interventions, even if much has been done to avoid that.

Chart 3: The stock price development of the large, listed Nordic banks during the bank collapses in the US and Europe in March

Source: Copenhagen, Helsinki, Oslo and Stockholm stock exchanges.

In the Nordic banking market, Swedbank was fined SEK 850 m by the Swedish financial supervisory authority following weaknesses and failures discovered in its internal change control mechanisms relating to its IT systems4. These caused a significant IT incident leading to millions of payments being delayed and incorrect balances being shown to Swedbank’s customers. The bank was able to fix the issues within a week and has not (reportedly) experienced any further issues with the IT system in question since then.

We also note OP’s shrinking balance sheet as an area of interest. OP’s balance sheet shrank by more than 10% during the quarter, mostly as a result of major reductions in two items on OP’s liability side, namely liabilities to customers and liabilities to credit institutions. The latter item was reduced from more than EUR 12 bn to virtually nothing. On the asset side, this resulted in OP’s cash position (cash and cash equivalents) being reduced by 50% (>EUR 17 bn), which is significant. We also note that OP’s liquidity position remained strong (as measured by the Liquidity Coverage Ration), being stable at 217%, and OP’s cash and cash equivalents in relation to its total assets are even after the reduction at similar level to its peers (i.e. around 10%).

The current, significantly higher income levels of the banks may lead to erosion in the banks’ cost cultures, risking future challenges.

Expenses on the rise

Another thing to keep an eye on in the coming quarters is the cost base of the banks. Most of the large Nordic banks reported significantly higher expenses than a year ago (in many cases they were up by double digits in percentage points). A notable exception in this sense is Danske as they were able to reduce their expenses compared with last year.

Obviously, there are good reasons for the higher expenses. First of all, high inflation is driving the banks’ expenses up, and secondly, it makes a lot of sense to make extra investments in good times. On the other hand, the current, significantly higher income levels of the banks compared with multiple past years, which allows for the higher expenses, may lead to erosion in the banks’ cost cultures, risking future challenges.

For example, at some point interest rates in the Nordics will begin to fall again, leading to lower NII. At that point the banks will need to readjust their expense levels accordingly. This might be difficult if the current cost increases are driven by inelastic items, such as personnel.

Ready for bad times

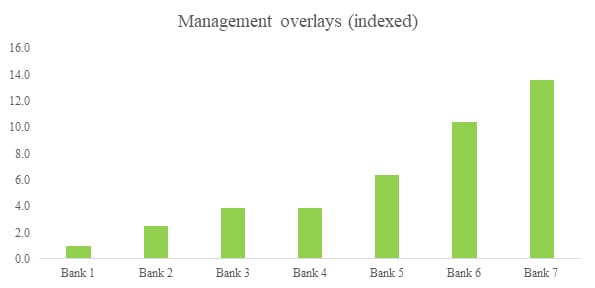

All the banks’ result announcements highlighted the challenging macroeconomic conditions of Q1/2023. These include the final waves of Covid-19, the Russian invasion of Ukraine, high inflation, rapidly rising interest rates and falling property prices. Most of the banks started to add to their loan loss provisions discretionary management buffers or overlays at the beginning of 2020 due to Covid-19, and many of those buffers have since been repurposed to account for the other macro shocks listed above.

These mechanics should be used as part of a top-down analysis of the banks’ expected loan losses under extraordinary circumstances for which their standard models are unable to cater5. While the use of these add-ons is (to a certain degree) discretionary, it is interesting to observe how differently they are applied among the large Nordic banks. We looked at the management buffers of the large Nordic banks in relation to the banks’ total lending portfolios and noticed significant differences.

The difference between the smallest and largest management buffer is close to 14x, which is very large given that the banks operate in similar geographies with similar customer bases and product portfolios.

Chart 4: The management overlays of the large Nordic banks (indexed) at the end of Q1/2023.

Source: The sample banks’ Q1/2023 interim reports.

This does not immediately imply that some banks are better prepared for bad times than others, but it does raise questions about the banks’ consistency in evaluating credit risk and could suggest that some banks might benefit from a review of their credit practices.

We urge the small Finnish players to continue this path of consolidation as that is the only way to stay relevant in the banking market and to challenge the biggest players over time.

The Finnish banking market: The next wave of consolidation begins?

On 31 May 2023 SHB announced6 that it had reached an agreement to sell part of its Finnish business to a group of Finnish banks and insurance companies. This is good news for SHB as it has been seeking a buyer for its Finnish business for more than 1.5 years now and exactly as we predicted in our Q2/2022 analysis7. The transaction represents ~30% of the bank’s lending volumes in Finland, meaning that a large part (EUR 10 bn) of its lending portfolio is still on sale.

For the buyer banks (i.e. S-Bank and Oma Savings Bank) this adds to their current customer portfolios and increases their size, but ultimately, we do not think this changes much in the Finnish banking market.

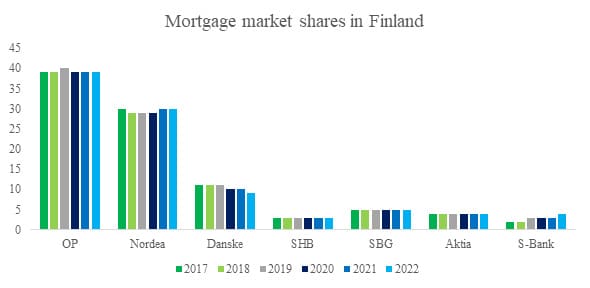

The Finnish banking market is dominated by OP, Nordea and Danske, and this has been the case for years (see Chart 4 below on mortgage markets shares as an example). The combined market share of these banks is around 80% while the share of the next four banks i.e. SHB, the Savings Banks Group (SBG), Aktia and S-Bank adds up to around 15%. The story is very similar across different customer segments (household and corporate segments) and products (loans, deposits, savings).

Chart 5: The mortgage market shares of selected Finnish banks.

Source: The Bank of Finland, https://www.suomenpankki.fi/en/Statistics/mfi-balance-sheet/tables/rati-taulukot-en/markkinaosuudet_luottolaitokset_en/

In our assessment, the only way for the smaller Finnish banks to really challenge the market leaders is to continue consolidation as the dynamics of banking favor size and scale benefits. This is true, for example, in relation to compliance (implementing new regulatory requirements) and customer service (e.g. in the form of new digital services). Evidence of this can be clearly seen in the banks’ efficiency ratios (their C/I) as that of the large Finnish banks is on average 46% while for the small ones it is 69%8. This equals a delta of close to 50%!

We urge the small Finnish players to continue this path of consolidation as that is the only way to stay relevant in the banking market and to challenge the biggest players over time. As a hypothetical, should the small banks listed above merge into one, that would immediately create the third largest bank in the Finnish market with a market share of 15%. This would be a real game-changer and would disrupt the current market dynamics.

In conclusion

While the current business performance of the large Nordic banks is – by any measure – excellent, we recognise that the banks’ rising cost levels are a potential long-term risk and caution the banks to monitor this development closely. We note major differences in the banks’ approaches to potential future loan losses because of extraordinary macroeconomic shocks and cannot justify these differences based on publicly available objective data.

In the Finnish banking market, we have observed what we hope to be the next wave of consolidation with SHB’s partial sale of its local business. We believe that this is the right path and urge the smaller banks to explore similar or even more aggressive plays in order to grow their size and challenge the large players.

Finally, the Silicon Valley Bank and Credit Suisse collapses reminded us again of the global nature and interconnectedness of the banking system. These distant events had ripple effects in the Nordics, evidencing that the contagion effects are very much prevalent in the global banking system, even after all the regulatory reforms implemented since the GFC.

_________________________________________

[1] Nordea Bank, Danske Bank, Skandinaviska Enskilda Banken (SEB), Svenska Handelsbanken (SHB), Swedbank, DNB, Nykredit, OP Financial Group (OP)

[2] https://www.nytimes.com/2023/03/10/business/silicon-valley-bank-stock.html

[3] https://www.nytimes.com/2023/03/19/business/ubs-credit-suisse.html

[4] https://www.fi.se/en/published/sanctions/financial-firms/2023/swedbank-receives-a-remark-and-an-administrative-fine/

[5] https://www2.deloitte.com/content/dam/Deloitte/gr/Documents/risk/gr_IFRS_9_ECL_measurement_in_the_Covid19_era_onwards_ noexpa.pdf

[6] https://vp292.alertir.com/en/node/5978

[7] https://www2.deloitte.com/fi/fi/blog/finland-blog-homepage/2022/boring-but-good.html

[8] Large banks: OP, Nordea, Danske. Small banks: SBG, Aktia, S-Bank. SBH FI is not included in the calculation due to their legal structure whereby the Finnish business is run as a branch of the Swedish company.

Contacts

Mikko Leinonen

Mikko is a Partner and leader of Deloitte’s Banking Consulting practice in Finland. Mikko has +15 of experience in the Nordic banking sector as a leader and business advisor. He is specialised in people, business and technology transformations, including e.g., organisational change, new technology implementations and strategy design. Mikko has deep knowledge of the end-to-end operations of universal banks ranging from the back-end technologies to the front-end customer solutions. Mikko toimii partnerina johtaen Deloitten pankkialan konsultointipalveluita Suomessa. Hänellä on yli 15 vuoden kokemus Pohjoismaisesta pankkisektorista johtavana asiantuntijana ja yritysneuvojana. Mikko on erikoistunut ihmisten, liiketoiminnan ja teknologian muutoksiin, mukaan lukien organisaatiomuutokset, uuden teknologian toteutukset ja strateginen suunnittelu. Hänellä on syvä, kokonaisvaltainen tuntemus yleispankkien toiminnasta aina taustateknologioista asiakasratkaisuihin asti.