Services

CFO Signals™ 1Q 2023

As the end of the first quarter of the year approaches, our 1Q 2023 North American CFO Signals survey reflects mixed views on the economic front. A vast majority (93%) of surveyed CFOs have their finance organizations focused on planning for a mild recession. At the same time, CFOs have higher expectations for year-over-year growth in earnings, revenue, capital investment, and domestic hiring, compared to the prior quarter.

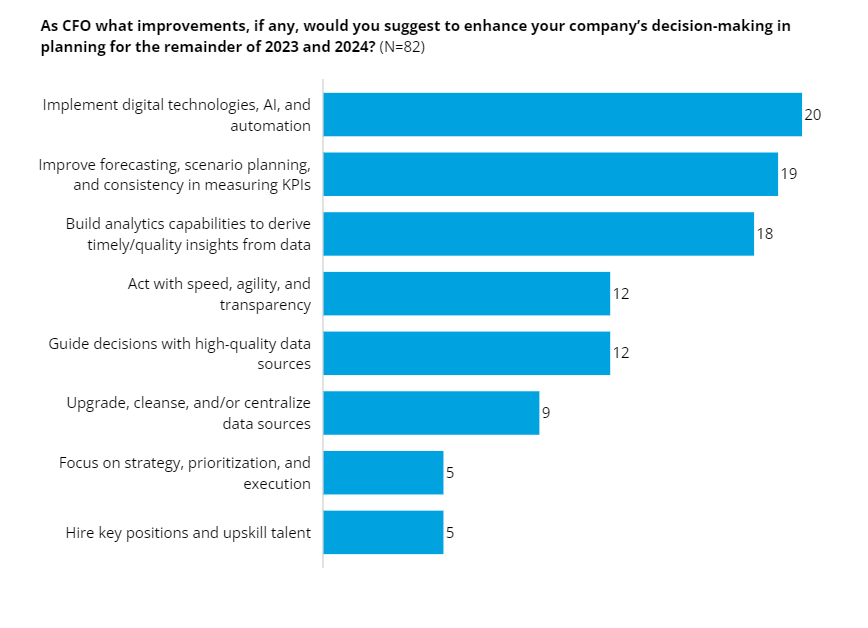

While CFOs are virtually unanimous in focusing their finance organizations on a mild recession, they also indicate they are generally satisfied with their organizations’ ability to plan for a recession/downturn and a recovery/rebound should that occur. As organizations plan for the remainder of the year and for 2024, CFOs offered several suggestions to enhance their organizations’ decision-making. Implementing digital technologies, AI, and automation was cited most frequently, followed by improving forecasting, scenario planning, and consistency in measuring KPIs. Interestingly, some CFOs cited a need for speed, agility, transparency, and collaboration improvement—as most likely to help their companies pivot as economic and market conditions change.

For a more detailed look at this quarter’s results, download the report.

CFOs’ views of regional economies and capital markets

Although most surveyed CFOs are planning for a mild recession, more than half (54%) see the North American economy improving over the next 12 months, up from 29% in 4Q22. While CFOs’ views of current economies in Europe and China appear cautious, 32% of CFOs expect the European economy to improve in a year, up from 9% in 4Q22, and 41% project China’s economy to do the same, up from 19% in 4Q22.

With regard to capital markets, the proportion of CFOs saying U.S. equity markets are overvalued in this quarter’s survey increased to 36%, from 30% in 4Q22. The proportion of CFOs considering U.S. equity markets as undervalued declined to 14% from 20% in the prior quarter.

Growth expectations and risk appetite

Earnings growth is pegged at 5.4%, up from 2.9% in 4Q22, while capital investment is estimated to grow 5.7%, up from 4.0% last quarter. With talent still, a concern among surveyed CFOs, domestic hiring growth expectations increased slightly to 2.3% from 2.1% last quarter. Growth expectations for domestic wages/salaries, however, fell to 4.3% from 4.6% in 4Q22.

The survey also reveals that the proportion of CFOs saying now is a good time to be taking greater risks stands at 40%, a jump from 29% in the previous quarter. The increase in CFOs’ risk appetite most likely reflects their expectations for economic conditions across all regions tracked by CFO Signals to improve a year out, as well as higher net optimism for their own companies’ financial prospects this quarter.

Chief risk concerns

Despite continued reports of layoffs across industries, retention and talent availability and hiring continue to dominate CFOs’ list of internal worries. CFOs also express concerns over execution and prioritization—from strategic and transformation initiatives to cost-cutting measures. CFOs also cite innovation and growth, plus cost management, among their most worrisome internal risks. In addition, some CFOs indicate change management and the hybrid work environment as top-of-mind concerns, most likely related to their worries over talent. Interestingly, enterprise risk appears more often in CFOs’ comments in this quarter’s survey than in some recent ones.

Inflation and geopolitics/instability, cited by CFOs as their top external risks in 4Q22, again stand out prominently this quarter. Policies and regulations and concerns over a recession, along with interest rates and their impact, also are prominent among CFOs’ most worrisome external risks. This quarter, there are notable mentions of consumer spending and behavior and capital costs and availability as a concern. Some CFOs note competition and market constraints, as well as interest rates/impact, among their most worrisome risks. In addition, some CFOs cite risks associated with energy and commodity pricing, macroeconomics, and supply chain, although with less frequency.

Special topic: Economic scenarios, inflation expectations, and data and insights for decision-making

Economic scenarios. A vast majority (93%) of surveyed CFOs have their finance organizations focused on planning for a mild recession. That figure contrasts markedly with just 6% of CFOs who say their finance organizations are focused on planning for no recession and the 1% who are planning for a recovery/rebound.

A number of CFOs are also taking actions to prepare for a recovery or rebound. The top three actions being taken are investing in growth, sales, customers, and new markets; controlling costs/increasing operational efficiency; and building inventory and/or production capacity to meet demand.

Views on inflation. Inflation has declined since the start of the year, partly attributable to lower energy prices. Still, the majority of CFOs don't expect it to fall much further before year-end, pegging it between 4% and 6% for the U.S. and Canada. Some CFOs might view tightness in the labor market and higher wages as an inhibitor to inflation dropping faster. The likelihood of more interest rate hikes this year could also explain their cautious attitude.

Where do you think the rate of inflation will likely be by the end of 2023 in the following countries?

| Rate | U.S. (N=111) | Canada (N=103) | Mexico (N=101) |

| Less than 4% | 31% | 35% | 2% |

| Between 4% and 6% | 65% | 55% | 16% |

| 6% or greater | 4% | 10% | 82% |

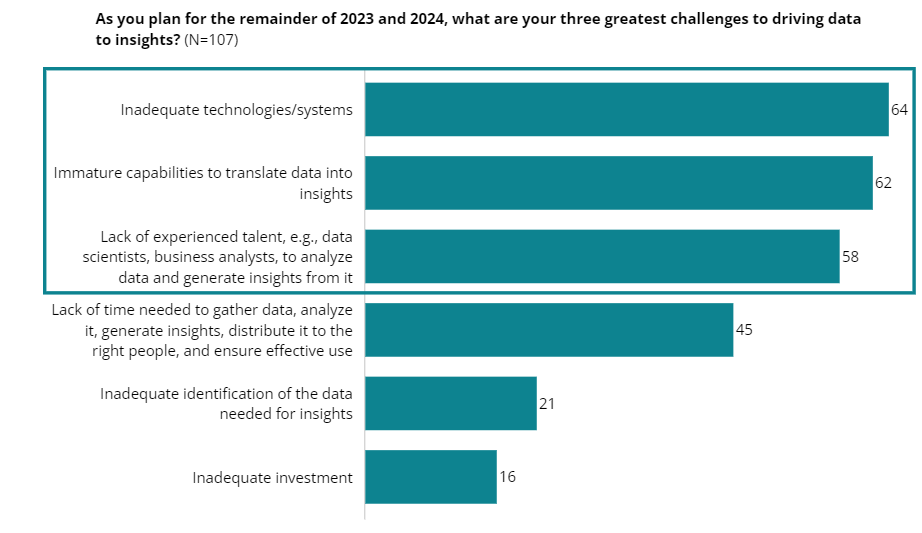

Data, insights, and decision-making. Our special topic this quarter focused on the challenges and opportunities CFOs and their finance organizations have in providing their businesses with data and insights for timely decision-making. More than half of CFOs pointed to inadequate technologies/systems, immature capabilities, and lack of experienced talent each as their greatest roadblocks in driving data to insights. The majority of surveyed CFOs have taken actions to address those challenges, such as investing in new systems and automation and upgrading existing systems, implementing talent/organizational changes, and streamlining data structures and evaluating processes and controls.

The 1Q23 CFO Signals survey was conducted from February 6-21, 2023.

Get in touch with our experts

Eszter Lukács

Finance & Performance Director, GBS Advisory Lead