CFO Insights 2020 December has been saved

Article

CFO Insights 2020 December

Japan Economic Outlook: External demand-led economic growth, but will it last?

CFO Insights is a monthly publication to deliver an easily digestible and regular stream of perspectives on the challenges confronting CFOs. This time, we are happy to share latest Japanese economic outlook published by Deloitte Insights.

Foreign demand has pushed Japan’s economy in the right direction, but rising infections at home and abroad threaten the ongoing recovery.

Explore Content

- Introduction

- The pandemic threatens consumers’ recovery

- Weak domestic demand weighs on business investment

- Strong external demand may wane

- Endnote

After declining for three consecutive quarters, Japan’s economy returned to growth in Q3. Japan has managed to keep infection rates low relative to other large developed economies, and strong demand in China and other parts of Asia has supported export growth.

However, real GDP remains more than 5% lower than a year earlier and the recovery is already facing several headwinds. The first is that infection rates are on the rise again. Although they remain far below those seen in the United States and Europe, new confirmed cases in Japan recently hit a record high. Some prefectures are raising restrictions on economic activity, and consumer spending could contract. Similarly, weak domestic demand and excess capacity are expected to weigh on business investment.

The one upside for business spending is the necessary upgrades in technology to accommodate new processes and preferences amid the pandemic. External demand has been a large contributor to Japan’s nascent recovery, largely thanks to China. However, demand from China may slow as stockpiling subsides, and demand from the United States and Europe may take a hit as infection rates rise in those export markets.

This article was originally published on Deloitte Insights on December 1, 2020. Reproduced with permission.

The pandemic threatens consumers’ recovery

Although consumer spending has improved since the first half of the year, real household spending was still 7.8% lower in Q3 compared to a year earlier (figure 1).1

Some of the weakness is due to last year’s consumption tax hike—consumers increased their spending, especially on big-ticket items, in 2019 Q3 to avoid the October tax increase, making year-ago comparisons look overly pessimistic. Still, household spending on durable goods remained weak, with spending levels around where they were more than four years ago. Plus, spending on services and semi-durable goods struggled to rebound.

Despite relatively low infection rates and government subsidies on domestic travel, consumers remain cautious. Indeed, the number of new COVID-19 cases per capita in Japan was just 2–3% of the number in the United States or the European Union in mid-November.2

Unfortunately, the pandemic in Japan has worsened notably since the beginning of October, with the number of new confirmed cases reaching a record high in November as the country embarked on its third wave of infections. The surge in cases threatens to upend the ongoing recovery in household spending.

As of mid-November, there had not been a discernable change in national mobility near retail and recreation establishments, which is tied to consumer spending. However, mobility has started to dip lower in Hokkaido where the outbreak has been particularly bad.3 Hokkaido policymakers have asked residents of its largest city, Sapporo, to avoid nonessential activity in an effort to curb the spread of the virus. Other prefectures are considering implementing similar measures.4 As local restrictions go into place, Japan may ultimately see a drop in mobility and spending throughout much of the country.

The national government is simultaneously encouraging more services consumption yet preparing for a drop in such spending. For example, it is maintaining its subsidy programs for dining out and domestic travel despite the surge in COVID-19 cases. In addition, travel restrictions have been loosened for visitors coming from countries with low infection rates, such as Australia, China, Singapore, and South Korea.5

The efficacy of such programs remains in doubt as Google predicts daily new cases will rise to a record 2,400 by December 12, up from about 1,300 per day in mid-November.6

As more prefectures prepare to announce additional restrictions, Prime Minister Yoshihide Suga announced that the government would set aside 50 billion yen for businesses adversely affected by local measures to cut hours and limit capacity.7 Suga’s cabinet is also putting together another stimulus package that ruling party lawmakers said should be between 10 and 30 trillion yen.8 These funds are meant to hold over affected businesses and their workers until a vaccine is made widely available.

Learn more

Learn how to combat COVID-19 with resilience

Explore the Economics collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Tohmatsu Group app

Weak domestic demand weighs on business investment

Even with additional government support, the prospect of weaker domestic demand as infections rise is expected to bode ill for business investment. Business sentiment had been improving since the first half of the year. The Economy Watchers Survey of current conditions, a measure of small business sentiment, jumped in October to its highest reading since 2014,9 and the Reuters Tankan survey, a measure of large business sentiment, continued to improve in November.10

However, the forward-looking components of these business sentiment indicators suggest businesses expect some contraction in the near future. In addition, core private-sector machinery orders, an indicator of future business investment in equipment that excludes volatile orders for ships and electric power companies, declined just 0.1% in Q3, but Japan’s Cabinet Office forecasts a steeper decline in Q4.11 Weak profits and excess capacity will also weigh on capex.One potential upside to business investment is that the pandemic has forced households and businesses alike to adopt new processes to limit the spread of the virus. The number of households ordering goods and services via the internet was up 21.3% from a year earlier, with older households contributing more to the recent gains.12

Businesses previously relied heavily on fax machines and the hanko seal to conduct business, requiring workers to come into the office.13 However, the national government is promoting digitalization to raise productivity and eliminate reliance on such analog practices.14 Additional investment in software and tech-related equipment may be necessary to accommodate the changes in consumer preferences and business practices. As a share of GDP, Japan’s investment in intangibles, such as software, was already lagging behind the United States’.15 If such investments yield the desired productivity gains, they can also help to counteract the negative effects of a shrinking population on GDP growth.

Strong external demand may wane

On a positive note, a growing trade surplus accounted for more than half of Japan’s Q3 rebound in real GDP. Exports reversed two consecutive quarters of declines while imports fell further. Japan’s trade balance is supporting the economy as consumer and business spending struggles to rebound strongly.16 Japan’s exporters may get an additional boost now that the Regional Comprehensive Economic Partnership, a free trade deal between ASEAN countries, Japan, China, Australia, New Zealand, and South Korea, was inked on November 15.17 One estimate suggests Japan’s national income could increase 1% by 2030 under the deal, though the gains would be incremental as tariff reductions are phased in gradually.18 Japan is also providing subsidies to companies that will build factories in Japan or Southeast Asia to diversify production away from China. It could also support Japanese exports.19

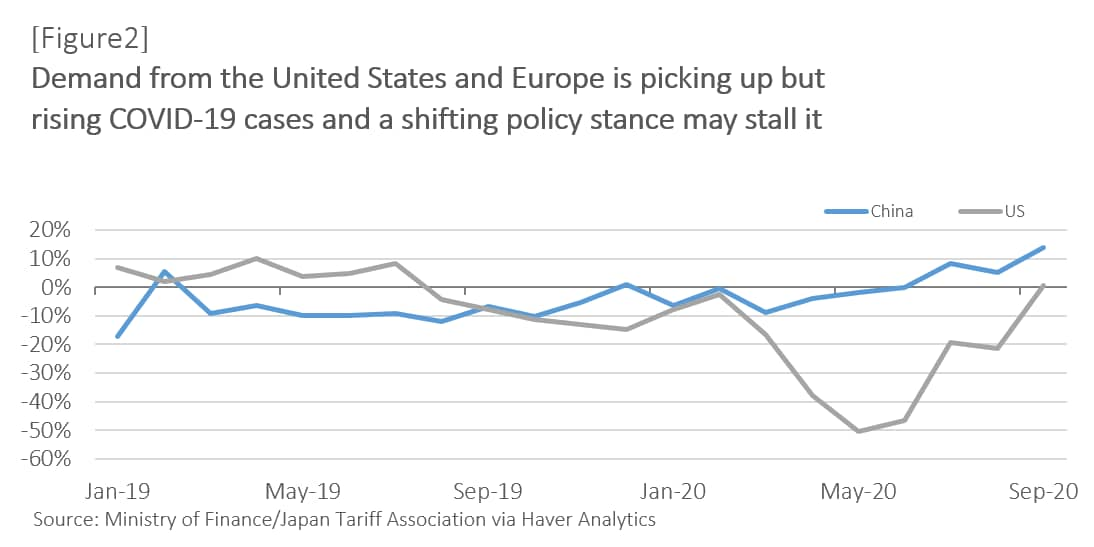

However, Japanese exports face two serious headwinds. The most imminent headwind is from the resurgence of COVID-19 in the United States and Europe. Exports to the United States, Japan’s second-largest export market, were 0.6% higher than a year earlier in September (figure 2). Although that number may sound small, it is a dramatic improvement from the –21.3% year-over-year rate in August and the –50.6% rate posted in May.20 With US infection rates reaching new highs and policymakers restricting economic activity, US demand for Japanese exports could fall in the coming months. The same is true for Europe, though it is a smaller export market for Japan.

The second headwind comes from China. Exports to China have been exceptionally strong, thanks in part to China’s ability to keep infection rates low and to rebound to prepandemic levels of output. Japan’s exports to China in September were up 14.0% from a year earlier.21 China has also been stockpiling semiconductors and related machinery as it attempts to build its own chips amid tensions with the United States.22 That has boosted demand for semiconductors machinery from Japan that accounted for nearly 20% of the year-over-year rise in exports to China.23 Strong semiconductor sales to South Korea and Taiwan may also ultimately be headed to China for stockpiling. Although China’s demand for Japanese technology should remain strong, it is likely to wane once inventories are deemed sufficiently large.

Japan’s relatively low infection rates and ample government support should foster a relatively strong recovery. However, already-cautious consumers may pull back on their spending as infection rates move higher. Plus, businesses are holding off on major expenditures until a more robust recovery is evident. Meanwhile, the rebound in external demand that has underpinned the recovery faces its own set of challenges ahead.

Endnotes

1. Cabinet Office, Government of Japan, “Quarterly estimates of GDP: July–September 2020,” accessed November 30, 2020.

2. Our World in Data, “Daily new confirmed COVID-19 cases,” accessed November 30, 2020.

3. Google, “COVID-19 community mobile reports,” accessed November 30, 2020.

4. Japan Times, “Hokkaido raises alert level for Sapporo as virus surge continues,” November 17, 2020.

5. Magdalena Osumi, “What you need to know about the latest travel restrictions for Japan,” Japan Times, November 17, 2020. View in article

6. Google Data Studio, “Japan COVID-19 forecast dashboard,” accessed November 30, 2020.

7. Kyodo News, “Japan gov't to give financial aid for shorter hours as virus surges,” November 16, 2020.

8. Yoshifumi Takemoto and Daniel Leussink, “Japan PM Suga instructs cabinet to compile new stimulus package,” Reuters, November 10, 2020.

9. Cabinet Office, Government of Japan, “Economy watchers survey,” September 29, 2014.

10. Daniel Leussink, “Japan manufacturers' less pessimistic in November: Reuters Tankan,” Reuters, November 9, 2020.

11. Cabinet Office, Government of Japan, “Machinery orders in September, 2020 and forecast for Oct.-Dec. 2020,” accessed November 30, 2020.

12. Statistics Bureau of Japan, “Items related to expenditure statistical tables: September 2020,” November 6, 2020.

13. Lisa Du and Shoko Oda, “The low-tech way that Japan managed to tackle the virus quickly,” Japan Times, June 24, 2020.

14. Japan Times, “Digitalization key to spur Japan growth in ‘new normal,’ report says,” November 6, 2020.

15. Heizo Takenaka, “Take a fresh look at intangible assets,” Japan Times, January 24, 2020.

16. Cabinet Office, Government of Japan, “Quarterly estimates of GDP: July–September 2020.”

17. Eric Johnston, “What does RCEP mean for Japan and its Asian neighbors?,” Japan Times, November 15, 2020.

18. Peter A. Petri and Michael G. Plummer, “East Asia decouples from the United States: Trade war, COVID-19, and East Asia’s new trade blocs,” Peterson Institute for International Economies, June 2020.

19. Bloomberg, “Japan starts paying firms to cut reliance on Chinese factories,” July 18, 2020.

20. Ministry of Finance (Japan) accessed via Haver Analytics.

21. Ibid.

22. Lori Ioannou, “A brewing U.S.-China tech cold war rattles the semiconductor industry,” CNBC, September 18, 2020.

23. Ministry of Finance (Japan) accessed via Haver Analytics and author calculations.