CFO Insights 2021 August has been saved

Article

CFO Insights 2021 August

Tax implications associated with creating a comfortable workspace for remote employees

CFO Insights is a monthly publication to deliver an easily digestible and regular stream of perspectives on the challenges confronting CFOs. In this article, we highlight how CFOs and tax teams play an important role in designing their company’s remote work financial assistance policy.

Explore Content

- Overview

- Financial assistance for remote working

- 1. Expenses

- 2. Purchases of furniture and equipment

- Conclusion

Overview

Many companies are considering making remote work permanent for all, or parts of their workforce, or have implemented a hybrid model where employees are expected to work partly in the office and in part remotely. As a result, in order to maximize employee experience and business efficiencies, companies are also considering how to assist its workforce in creating a comfortable remote workspace. CFOs and tax teams have an important role to play in formulating remote work policies and to ensure the company stays compliant with international and domestic tax regulations while minimizing disruption to the business and working style of the employees. Among these policies should be guidelines regarding financial assistance to employees incurring telework expenses (e.g. furniture and equipment purchases, electricity costs, etc.). These policies may be driven by the need to increase business efficiencies in a remote environment and to attract and retain talent, but the tax implications may strongly influence how companies design them.

In Japan, the National Tax Agency published an update to its Frequently Asked Questions Concerning Expenses Relating to Telecommuting (related to WHT) ("FAQ") on 31 May 2021 to provide more clarity on the Japanese tax implications to both the company and the employees when finanical assistance is provided to employees for expenses related to remote working.

In general, if a company pays an employee a remote work allowance (i.e., funds that do not need to be repaid to the company, even if the employee does not use the funds for normal teleworking expenses), it must treat the allowance as a taxable benefit. Conversely, certain amounts paid by a company to its employees that are calculated using amounts equivalent to the actual costs of remote working typically are not treated as a taxable benefit to the employee.

Financial assistance for remote working

As part of any policy related to providing financial assistance to employees, at a minimum, it is recommended that all employees be eligible for the financial assistance. If not, the entire allowance amount may be treated as a taxable benefit to the employees receiving the allowance and be subject to payroll withholding tax (the amount of the taxable benefit to the employees would generally be deductible for corporate tax purposes). Or, while unlikely, the allowance may be treated as a gift to the employees receiving the allowance. A gift would still be a taxable benefit to the employee (though not subject to payroll withholding tax), but it would not be deductible by the company.

It should be noted that if the allowance (or part thereof) made to directors are treated as a taxable benefit to the director, the allowance should be treated as directors’ compensation and subject to the normal restrictions imposed on the deductibility of directors' compensation for corporate tax purposes.

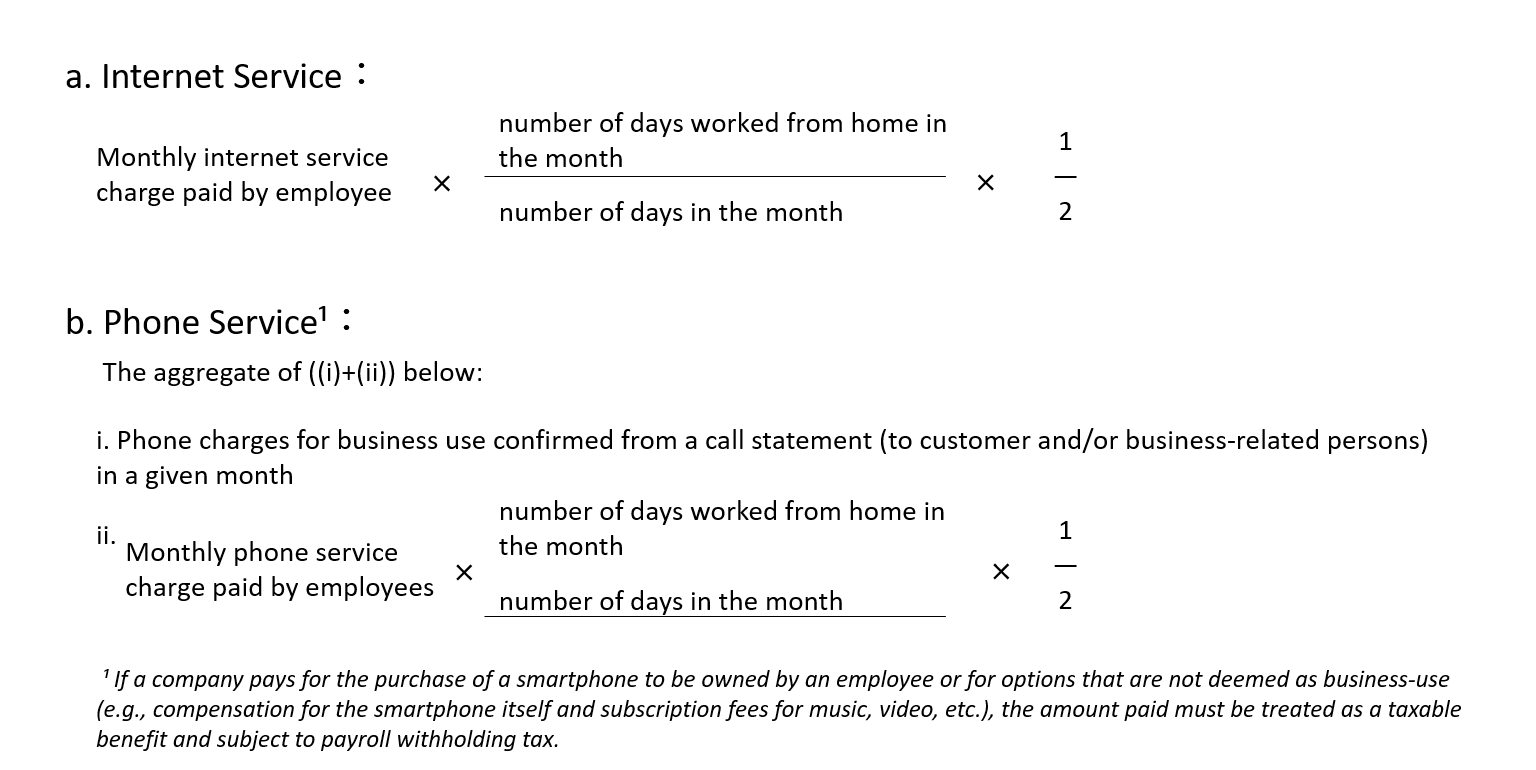

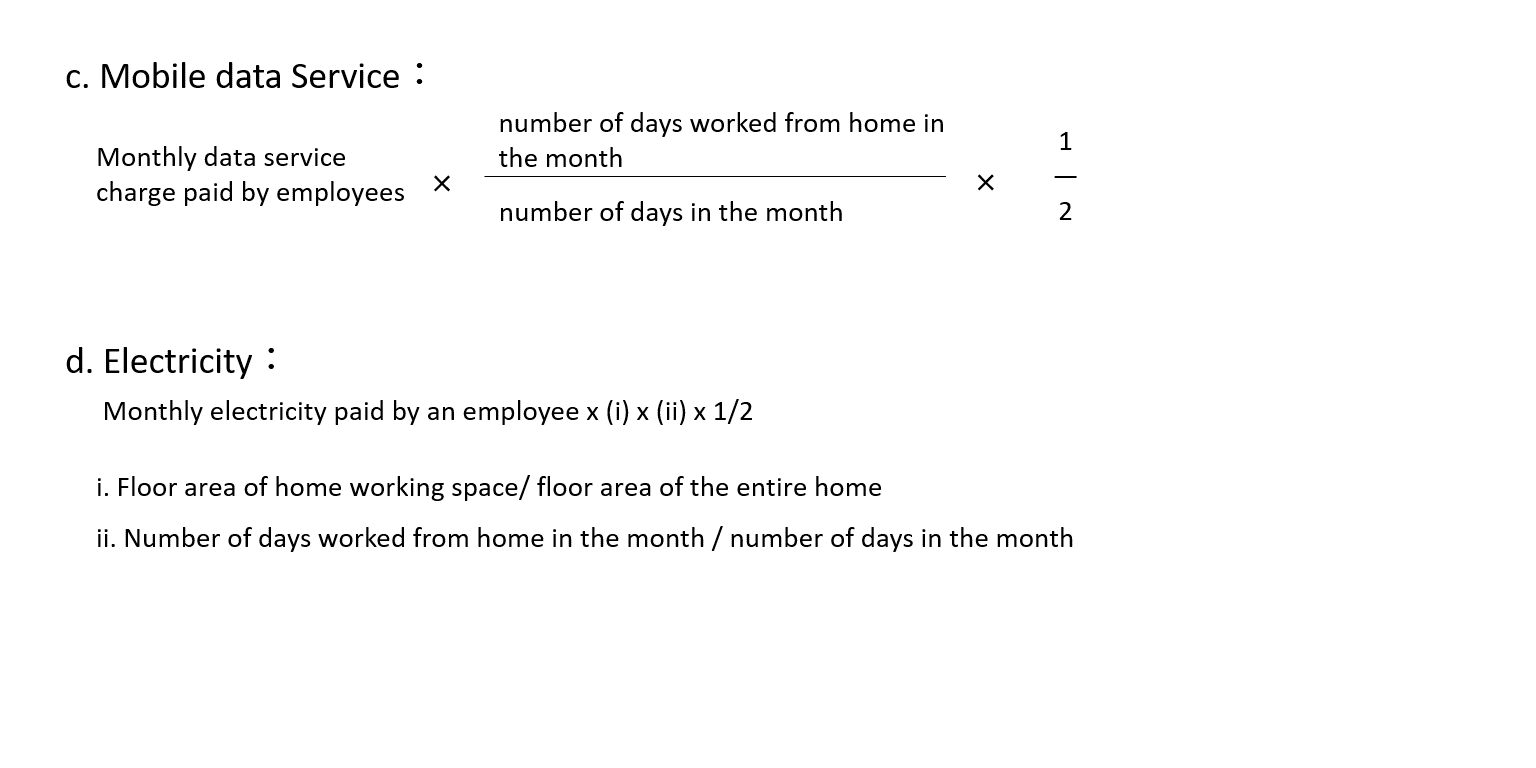

1. Expenses

Allowances paid to employees are generally treated as a taxable benefit and subject to payroll withholding tax. However, payroll withholding tax is not imposed on allowance if the allowance is a necessary business expense in order to work from home. Below is a non-exhaustive list of the common types of expenses discussed in the FAQ. The amount considered to be a necessary business expense is capped at the amounts described below for each type of expense (please note that if the business expense can be determined more precisely, it may be acceptable also). Any excess amount should be treated as a taxable benefit and be subject to payroll withholding tax. The entire allowance amount should generally be deductible for corporate tax purposes (subject to the normal restrictions for directors' compensation).

2. Purchases of furniture and equipment

Allowances for work furniture and computer equipment should be treated as a taxable benefit and subject to payroll withholding tax if employees have ownership of the computer equipment/ work furniture. If treated as a taxable benefit, the allowance should be deductible for corporate tax purposes (subject to the normal restrictions for directors' compensation).

It is not necessary to recognize a taxable benefit if employees simply use the computer equipment/ work furniture that is owned by the company (i.e. the employees will return the equipment/furniture upon leaving the company, etc.). In this case, the company should treat the allowance similar to how it treats the acquisition of the equipment and/ or fixed asset which requires monitoring the assets and would be burdensome.

Conclusion

Depending on the company, remote work allowances and expenses may be consuming a larger portion of a company’s budget, especially if remote working becomes a permanent feature for the company’s workforce. Regarding the company’s remote financial assistance policy, input from the finance and tax teams will become increasingly important to ensure the company appropriately recognizes amounts that are considered a taxable benefit to avoid any failure to properly and timely withhold tax.

While companies should design their remote work financial assistance policy to create a comfortable remote workspace for their employees, that helps to increase productivity, understanding the tax implications can help businesses determine the right policy and ensure it is appropriately budgeted for.

Should you have any inquiries, please contact the author, Brian Douglas (brian.douglas@tohmatsu.co.jp).

Other latest CFO Insights

Is rising corporate debt a problem? Not necessarily. (Deloitte Global CFO Insights)

Rising debt in an expanding economy with low interest rates may not necessarily be a bad thing if companies are increasing investments as well. Explore whether investments are keeping pace with rising debt and why some of those investments may well add to productivity growth in the wider economy in the medium- to long-term.

Contact us