Article

Tax audits and controversy are returning

Japan Tax & Legal Inbound Newsletter January 2023, No. 83

Background

Japan’s National Tax Agency recently published its latest fiscal year (FY) 2022 statistics on tax audits (July 2021 through June 2022) and tax appeals and litigation (April 2021 through March 2022). The statistics clearly show the return of tax audits and controversy in FY 2022, regardless of the effects of several waves of COVID-19. In FY 2023, tax audit activity has almost returned to pre-COVID-19 levels.

Tax audits

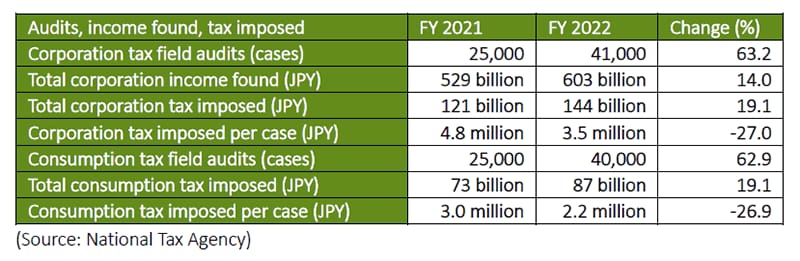

The number of field audits of corporate taxpayers in FY 2022 increased by 63.2% from FY 2021, and the total amount of income found in FY 2022 increased by 14% from FY 2021. The total amount of corporation tax imposed by field audits in FY 2022 increased by 19.1%. These increases indicate that tax audit activities were expanding in FY 2022.

The number of field audits on corporations for consumption tax in FY 2022 increased by 62.9% from FY 2021, and the total amount of consumption tax imposed by field audits in FY 2022 increased by 19.1%, which indicates that consumption tax was one of the major tax audit focal points in FY 2022. In particular, the tax authorities conducted intensive tax audits of corporate taxpayers claiming a refund of consumption tax, conversely imposing

JPY 37 billion on those taxpayers.

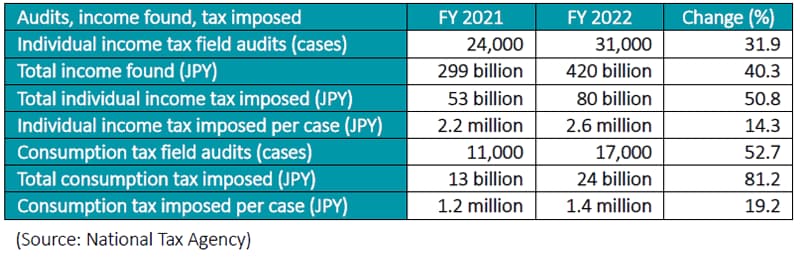

Regarding individual taxpayers, the number of field audits in FY 2022 increased by 31.9% from FY 2021, and the total amount of income found by field audits in FY 2022 increased by 40.3% from FY 2021. The total amount of individual income tax imposed by field audits in FY 2022 increased by 50.8%. As with corporate taxpayers, tax audit activity against individual taxpayers also increased during the year.

The number of field audits on individual taxpayers engaged in business activities for consumption tax in FY 2022 increased by 52.7% from FY 2021, and the total amount of consumption tax imposed by field audits in FY 2022 increased by 81.2%. A major tax audit target historically has been wealthy individuals, but in FY 2022 the tax authorities also rigorously targeted individual taxpayers taking advantage of consumption tax exemptions, additionally imposing JPY 1.2 billion on those taxpayers.

In FY 2023, the tax authorities are carrying out tax audit activity at levels approaching those seen before the spread of COVID-19. As such, taxpayers, especially those with consumption tax issues, should prepare for tax audits in advance.

Tax appeals and litigation

The number of first tier tax appeals filed with the tax authorities in FY 2022 increased by 11.9% from FY 2021, and those completed in FY 2022 increased by 19.9%. The number of second tier tax appeals filed with the National Tax Tribunal in FY 2022 increased by 11% from FY 2021, and those completed in FY 2022 decreased by 2%. Also, the number of tax litigation cases initiated in FY 2022 increased by 14.5% from FY 2021 and those completed in FY 2022 increased by 10.6%.

As tax audit activity increased in FY 2022, the number of unresolved points of

contention between taxpayers and the tax authorities also increased, showing that tax controversy also was returning in FY 2022.

The number of successful first tier tax appeals in FY 2022 decreased by 17% from FY 2021, with the success ratio in FY 2022 decreasing by 31%. The number of successful second tier tax appeals in FY 2022 increased by 27.5% from FY 2021, with the success ratio in FY 2022 increasing by 30%. Furthermore, the number of successful tax litigation cases in FY 2022 decreased by 7.1%, with the success ratio in FY 2022 decreasing by 16.7%.

Compared with the recent five-year average, the first tier tax appeal success ratio has decreased, and the successful tax

Deloitte Japan’s View

Tax audits and controversy are returning, and the tax authorities are conducting even more tax audits in FY 2023 than in FY 2022. Consumption tax continues to be a major tax audit focal point in FY 2023, and a key issue often is whether a fact that is considered to be true by a taxpayer is actually correct.

For example, if a tax-free shop sells certain goods, such as cell phones or cameras, to a nonresident in accordance with tax-free procedures, the sale of the goods is exempt from consumption tax. However, if the tax-free shop sells the same goods to a resident, the sale of the goods is subject to consumption tax at 10%. Therefore, the consumption tax treatment of the sale depends on whether the purchaser is actually a nonresident. In practice, most customers visiting a tax-free shop, stating they are nonresidents and showing their passports, are actually nonresidents. However, abuse of the system is possible if a nonresident assists a resident in purchasing goods at the tax-free price. In this case, whether the purchaser is actually a nonresident could be a point of dispute in tax audits.

If a tax position relies on uncertain facts, taxpayers should determine whether there is enough evidence to prove the position in preparation for a future tax audit.

Professional