{kind=link}

{kind=link}

{kind=link}

Japan economic outlook, October 2022 has been saved

Cover image by: Jaime Austin

Japan’s economic recovery since the pandemic hit has been more subdued than its developed-economy peers. Real GDP growth picked up in the first half of this year, but still remains below its all-time high level reached in Q2 2019.1 The silver lining is that inflation, at 3% year over year (YoY) in August, has also been relatively subdued, particularly when compared to the double-digit rates seen in parts of Europe.2 As other countries raise rates to combat inflation, Japan has held tight, leading to strong depreciation of the yen. Policymakers have intervened to support the exchange rate,3 but it remains unclear if their efforts can be sustained.

A weak yen and high commodity prices have raised the cost of imports and eroded the trade balance this year,4 but export growth has still been strong. Unfortunately, the outlook for the global economy has deteriorated, which will likely keep goods export growth down. Even so, there are some bright spots in the near-term outlook. A strong rebound in China’s growth next year may partially offset weakness elsewhere. Plus, supply chain relief in the auto sector will likely act as a tailwind to related manufacturers. Consumer spending will also get some help from government programs. However, if the global economy weakens further as expected and government assistance expires, Japan’s economic growth will likely slow as well.

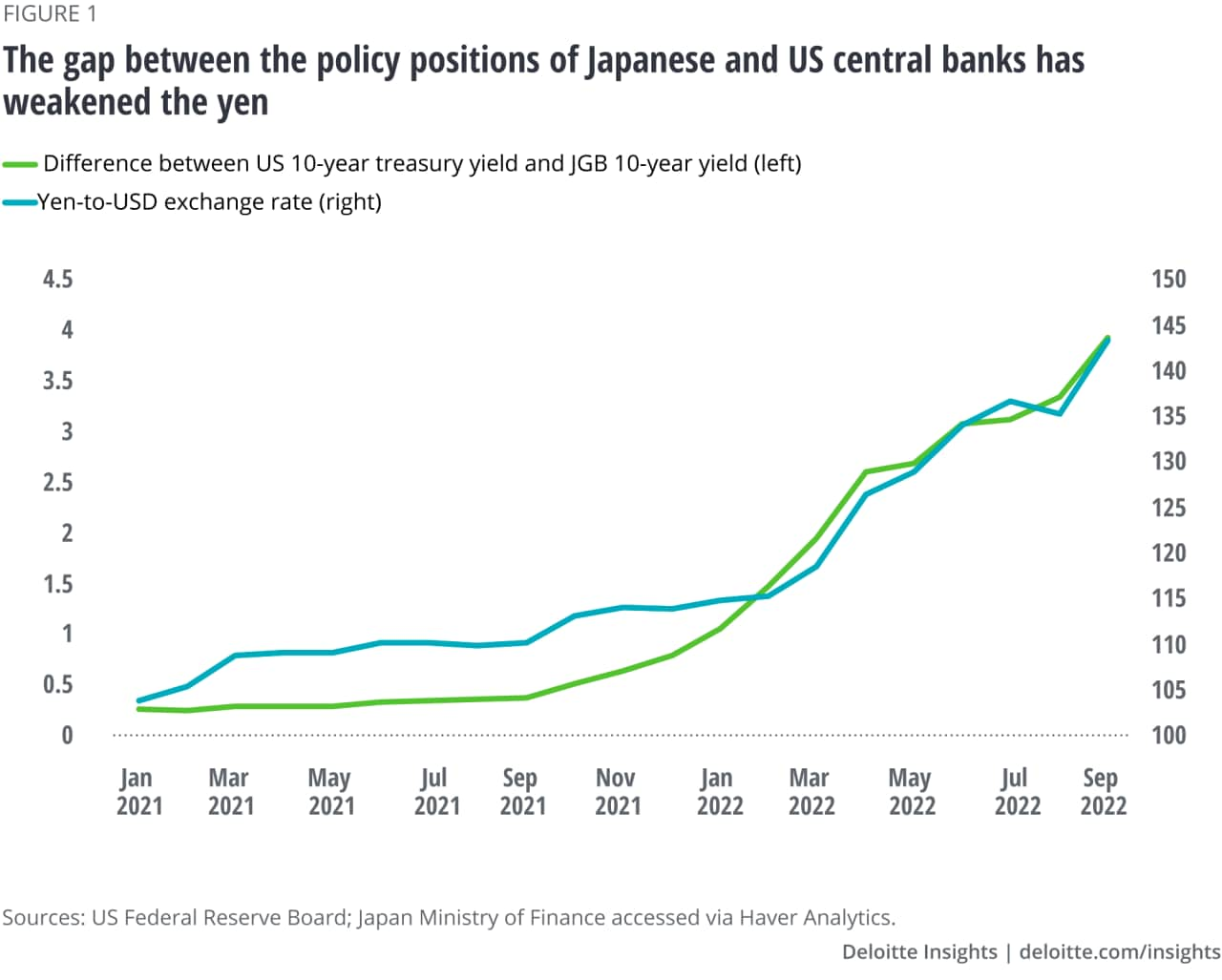

The weak value of the yen, which lost roughly 20% of its value against the US dollar since the start of this year,5 is primarily due to the interest-rate differential between Japanese government bonds (JGBs) and US Treasuries. The Bank of Japan (BoJ) has committed to maintaining its ultra-loose monetary policy stance while the US Fed has raised rates relatively quickly this year. The widening gulf between these two policy positions pushed capital away from yen-denominated assets such as JGBs and toward dollar-denominated assets such as US Treasuries (figure 1). The United States is expected to raise rates further, while the BoJ insists that it will not raise rates.

On September 22, policymakers at the Ministry of Finance intervened in foreign exchange markets to support the value of the yen—a first since 1998. Policymakers had grown concerned that the yen was depreciating too quickly, and thus, decided an exchange-rate intervention was necessary.6 At the order of the Ministry of Finance, the BoJ dipped into its foreign exchange reserves to buy yen in an effort to support the yen. During the two weeks following the intervention, the exchange rate mostly moved sideways. However, by October 21, the yen had depreciated further, which prompted another intervention in foreign exchange markets and raised questions over how much depreciation policymakers will tolerate.7

The initial intervention cost roughly US$20 billion.8 Given that the BoJ holds more than US$1 trillion in foreign reserves, it has plenty of additional room to buy more yen.9 However, policymakers may not want to deplete a substantial portion of their current holdings. Other policy interventions would raise the value of the yen without dipping into reserves. One way to prop up the exchange rate would be for the BoJ to ease up on its yield-curve control, which holds the 10-year JGB yield around zero percent. Allowing the yield curve to steepen slightly would likely support the exchange rate. The same would be true for a policy-rate hike. However, the BoJ believes the domestic economy is too weak and inflation remains too low for a tightening of monetary policy. This is likely true, especially given that Western core inflation, which subtracts out food and energy, is up just 0.7% from a year earlier in August.10

Instead, it seems that policymakers are buying themselves some time. As of this writing, markets anticipate that the Fed will continue to hike rates through the end of next year. However, it remains possible that the Fed will have to pivot away from this projected path of rate hikes should inflation come down more than currently anticipated. Indeed, markets assign about a 25% probability that the Fed will reverse course next year.11 Japanese policymakers only need to support the yen until more market participants expect the Fed to pivot, at which point, the interest-rate differential between the two countries should narrow, supporting the value of the yen relative to the US dollar. Policymakers may also tolerate additional depreciation of the yen, assuming the moves are more gradual than what occurred in September.

The operating environment for Japanese manufacturers has improved. Industrial production for all manufacturing was up 3.4% YoY in August—the highest growth rate since September 2019.12 Part of the improvement comes from a rebound in motor-vehicle production, which was up 11.9% YoY—the first positive growth rate posted in more than a year.13 Automakers have been plagued by supply chain issues since the pandemic hit, but conditions have improved markedly this year. The improvement in manufacturing output is not confined to the auto sector, however. The manufacture of machinery, particularly semiconductor and flat-panel display manufacturing equipment, was up a sizable 38.7% from a year earlier.14

Core machine orders grew by 5.3% in July, suggesting that business investment should be reasonably strong through the end of this year.15 Additional business investment is sorely needed too, as it was still 7.1% below where it was three years earlier in Q2 in inflation-adjusted terms.16 However, business sentiment has since fallen. For example, the Reuters Tankan index dropped to 10 in September from 13 the previous month as cost pressures weighed on Japanese businesses.17 Additional worries about the global economy over the next year could further weigh on business-investment decisions.

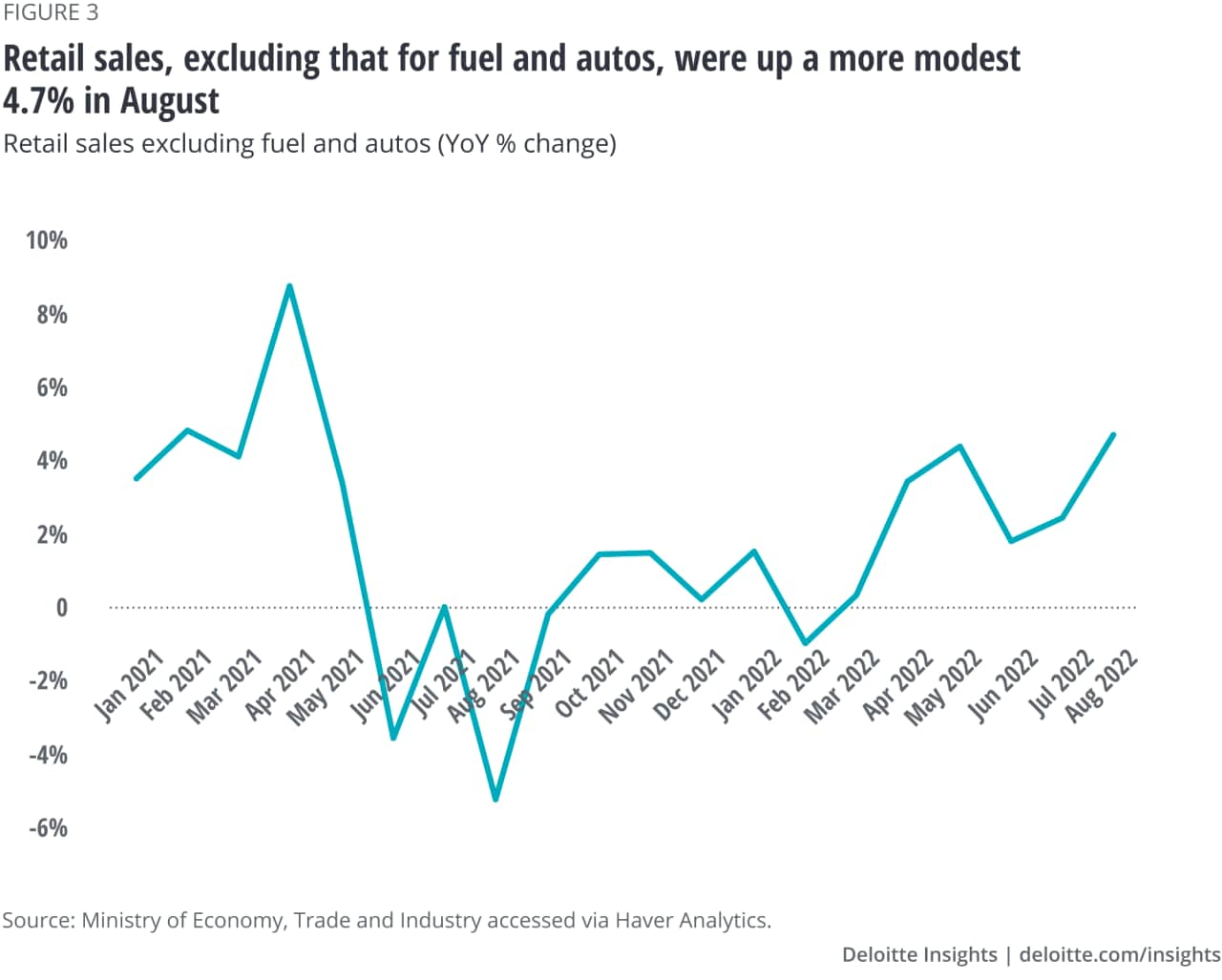

So far this year, export growth has been very strong. Goods exports were up 22% from a year earlier in August.18 Part of the strength is related to the auto sector, which was reflected in industrial production numbers. Exports of passenger motor cars were up 37.9% over the same period (figure 2). Even after subtracting used cars from the equation, exports of autos were up 37.4%.19 Another part of the underlying strength in exports was a pickup in economic activity in China. Exports to China jumped 13.4% from a year earlier.20 As recently as May, exports to China had been below their year-ago level.

Despite the rebound in exports to China and the improvement in supply chains, Japanese exports face headwinds. First, the global economy is expected to slow dramatically in the coming quarters. Europe and the United States are at high risk of recession, which would sap exports to those regions. For context, the United States alone accounted for just shy of 20% of all Japanese exports in 2019.21 As mentioned earlier, the value of the yen will likely appreciate should strong disinflation accompany an economic slowdown in those regions. While a weak yen has supported export growth this year, a likely strengthening of the yen next year will have the opposite effect.

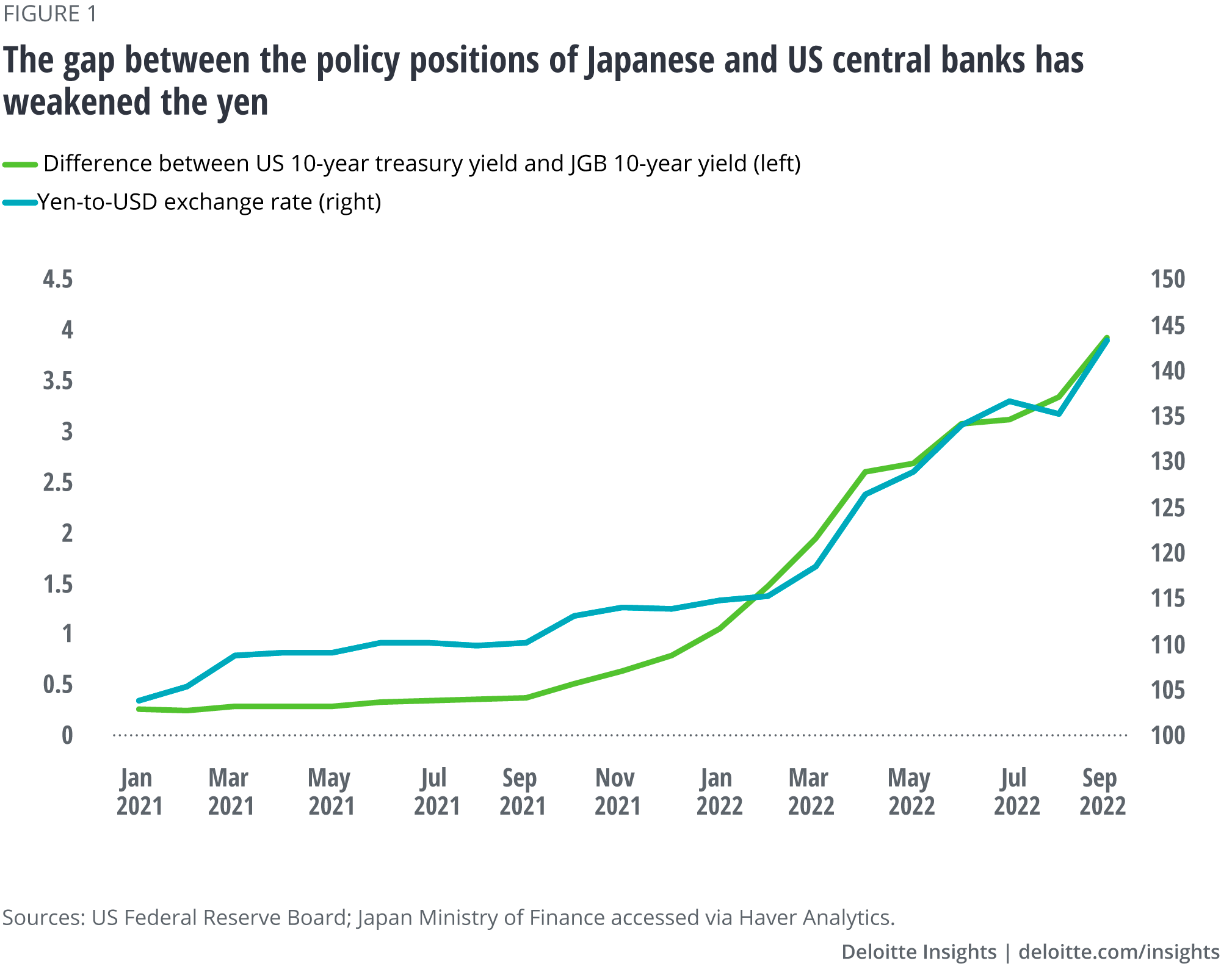

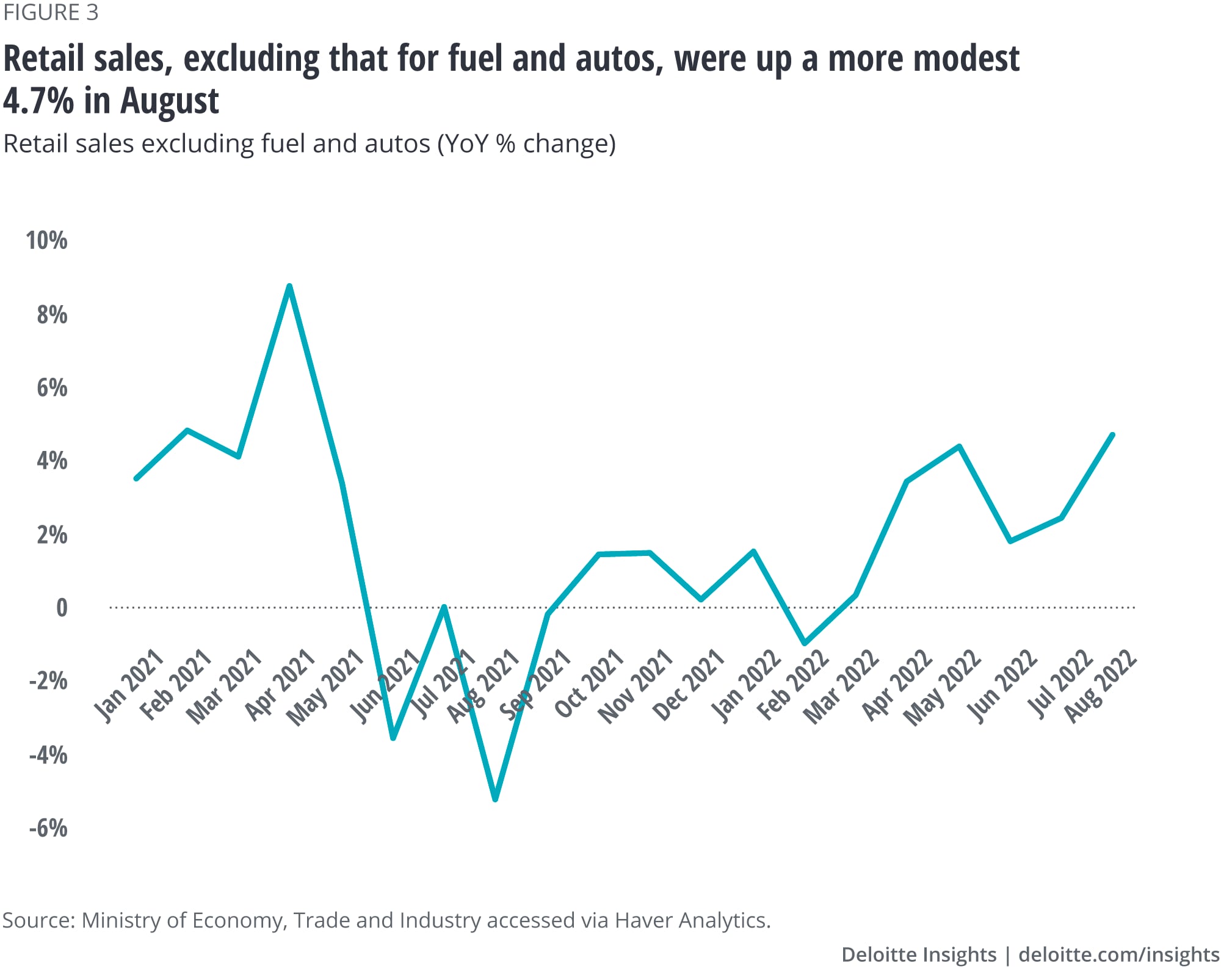

Consumer spending has picked up this year despite headwinds to growth. For example, real household consumer spending grew at an annualized rate of 4.9% in Q2 relative to the prior quarter.22 Consumer spending has been moving in the right direction since, with the inflation-adjusted consumer activity index up 3.3% in August from a year ago. However, elevated inflation, particularly fuel costs, is eroding consumer purchasing power. For example, retail sales for fuel were up 10.8% from a year earlier in August, while sales were up a more modest 4.7% after removing fuel and autos (figure 3).23 A recent rebound in crude oil prices is unlikely to help.

With regular employee earnings up just 1.7% over the same period,24 such strong consumer spending numbers are unlikely to be sustained in the long run. However, several policy interventions may support spending, at least in the near term. Subsidies for fuel and price caps on wheat and animal feed should provide assistance to households struggling with the elevated costs of fuel and food through the end of the year. Another round of direct stimulus for low-income households will also support spending.25 On top of those support measures, the government announced its National Travel Discount Program, which offers up to 11,000 yen per day for seven days to cover accommodation and other travel-related costs.26

While domestic tourism will get a boost from this new government program, international tourism is poised for a strong rebound as well. Japan has fully reopened its borders, eliminating the cap on foreign-tourist arrivals. A weak yen could raise the average expenditure per visitor. However, a sudden return to prepandemic levels of international tourism is highly unlikely. Prior to the pandemic, China accounted for about 30% of all international travelers in Japan. Until China abandons its zero-tolerance COVID-19 policy, the number of international travelers in Japan will remain subdued relative to prepandemic norms. Even so, international-traveler numbers are so depressed that it is virtually inconceivable that they will not rise dramatically. After all, the number of international travelers in August was still 93% lower than it had been three years prior.27

Japan’s relatively low-inflation environment will likely spare it from the contractionary effects that other countries will experience as interest rates climb higher. In the near term, government programs and improvements in the auto sector will support consumer spending and manufacturing, respectively. Japan’s exposure to China should support exports next year, but the expected global slowdown will ultimately create headwinds to its economic recovery.

Cabinet Office of Japan, accessed via Haver Analytics.

View in ArticleTrading Economics, “Japan inflation rate,” accessed October 27, 2022.

View in ArticleChikako Mogi and Tian Chen, “Japan intervenes to support yen for the first time since 1998,” Bloomberg, September 22, 2022.

View in ArticleTrading Economics, “Japan balance of trade,” accessed October 27, 2022.

View in ArticleMogi and Chen, “Japan intervenes to support yen for the first time since 1998.”

View in ArticleIbid.

View in ArticleKana Inagaki and Leo Lewis, “Japan made intervention of at least $30bn to prop up yen,” Financial Times, October 23, 2022.

View in ArticleDavid Finnerty and Ruth Carson, “Yen traders show resilience to risk of more Japan intervention,” Bloomberg, October 10, 2022.

View in ArticlePaul Jackson and Masaki Kondo, “Even $1.2 trillion of reserves isn’t enough to scare yen bears,” Bloomberg, September 13, 2022.

View in ArticleMinistry of Internal Affairs and Communications.

View in ArticleCME Group, “Target rate—Current,” accessed October 27, 2022.

View in ArticleMinistry of Economy, Trade and Industry, accessed via Haver Analytics.

View in ArticleCabinet Office of Japan.

View in ArticleIbid.

View in ArticleDaniel Leussink and Kantaro Komiya, “Japan’s machinery orders posted surprise gains in July,” Japan Times, September 14, 2022.

View in ArticleCabinet Office of Japan.

View in ArticleLeussink and Komiya, “Japan’s machinery orders posted surprise gains in July.”

View in ArticleMinistry of Finance and Japan Tariff Association.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleOEC, “Japan,” accessed October 27, 2022.

View in ArticleCabinet Office of Japan.

View in ArticleMinistry of Economy, Trade and Industry.

View in ArticleMinistry of Health, Labor and Welfare.

View in ArticleYoshiaki Nohara and Toru Fujioka, “Japan’s Kishida orders stimulus as analysts warn of overspending,” Bloomberg, September 30, 2022.

View in ArticleWill Fee, “Japan's eagerly anticipated reopening gets off to slow start,” Japan Times, October 11, 2022.

View in ArticleJapan National Tourism Organization.

View in ArticleCover image by: Jaime Austin