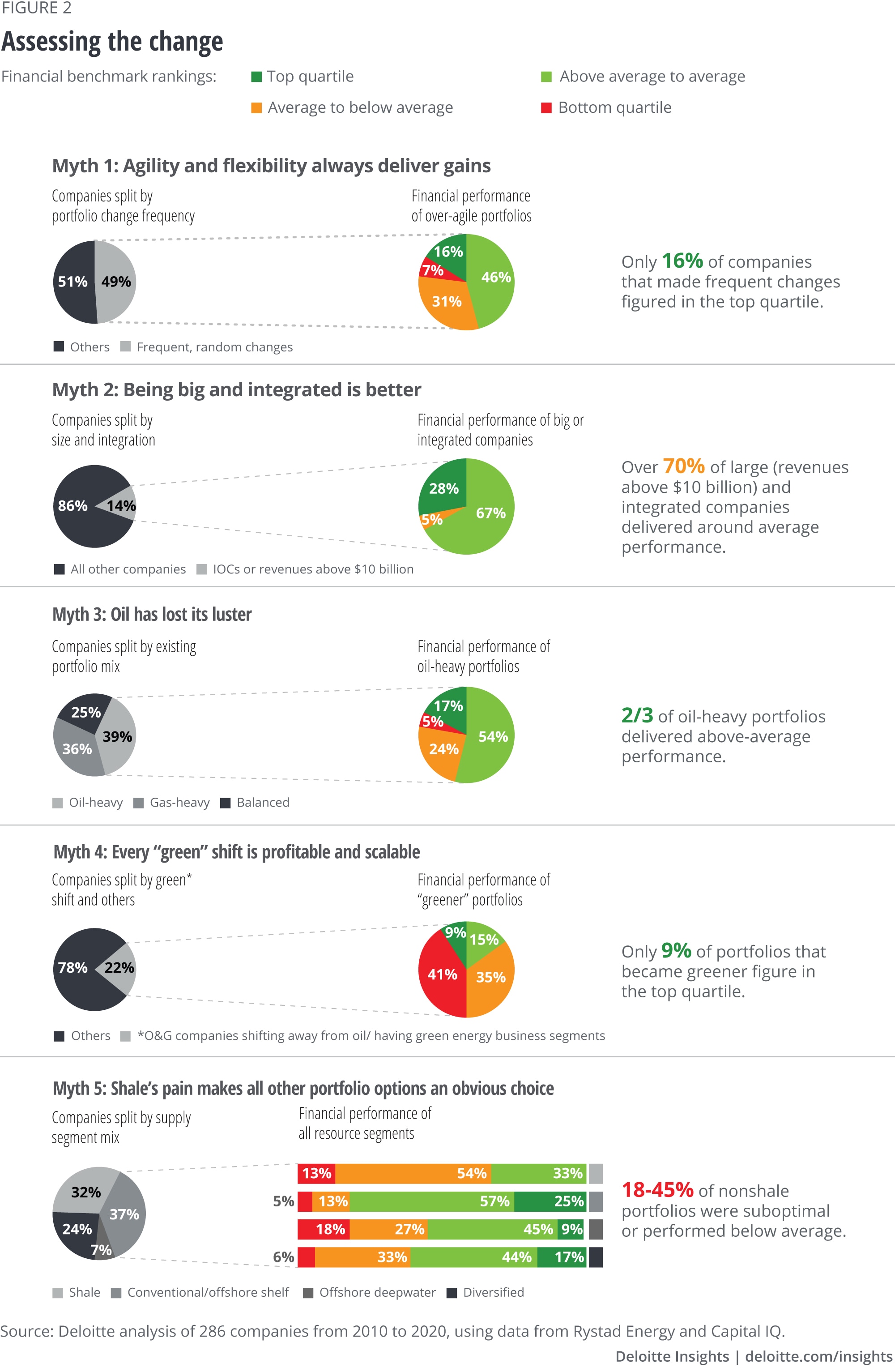

1. Myth 1: Agility and flexibility always deliver gains.

Reality: Only 16% of companies analyzed that made frequent changes figured in the top quartile.

Having an agile and flexible portfolio (especially one that includes short-cycled shales) is often hailed as a silver bullet for O&G companies to unlock new value. If done correctly and consistently, agility and flexibility can create tremendous impact.

But if portfolio optimization is “overdone” or done indiscriminately and follows oil price cycles, it can destroy the value and trust of stakeholders. An integrated company, for example, constantly changed its fuel and supply segment strategy over the past 10 years, moving between oil to gas, shale to conventionals and back, but failed to generate lasting value from these changes.

About 49% of companies in our sample set made frequent changes in their portfolios (i.e., they made many and frequent changes in their fuel mix, supply segment, or regional footprint over the past 10 years).3 Of these 49% of the companies we analyzed, not surprisingly, only 16% delivered top-quartile performance across the 10 parameters (figure 2).4 In contrast, companies that seemed more strategic and deliberate in their portfolio building, delivered much better results. Cimarex Energy, for example, has made consistent changes to its portfolio and stayed true to its strategy of building a low-cost position in the Permian basin by following a standardized proppant intensity and completion design strategy for its shale wells.5

2. Myth 2: Being bigger and integrated is better.

Reality: Over 70% of large and integrated companies delivered subpar performance.

Size and integration make strong strategic sense when used to exploit market access and supply chain efficiencies, or to offer a stable investment avenue. But in today’s lackluster hydrocarbon scenario, the cons of this strategy are beginning to outweigh its pros. In fact, in some cases strong balance sheets and integrated reporting structures could be hiding inefficiencies in portfolios of large companies.6

Of the publicly listed non-NOC companies that are either big (revenues >$10 billion) or integrated, a majority underperformed over the past 10 years. Only 28% of them delivered top-quartile performance with only three companies figuring in the top 10 performers, despite having some of the strongest balance sheets.7 Interestingly, many NOCs have outperformed their publicly traded counterparts due to their low-cost resource base, high-pressure fields, and access to markets.

3. Myth 3: Oil has lost its luster.

Reality: Two-thirds of oil-heavy portfolios delivered above-average performance.

Even as oil reaches peak demand, demand is expected to slowly plateau over the coming decades, and is projected to remain above 87 MMbbl/d till the end of this decade.8 Just to replace the annual consumption and offset natural field declines, the industry would need to invest more than $525 billion annually in O&G projects.9

Even in a decade marred by disruption and acute price pressure, oil generated significant value for many low-cost oil operators and their stakeholders. In our analysis, for example, about 66% of oil-heavy portfolios sampled delivered above-average returns.10 In fact, a few oil companies have delivered average returns on capital of over 20% over the last 5 years, higher than many companies in nonservice industries including utilities and capital goods. For example, Lundin Energy AB has realized value from its oil-heavy portfolio and consistently delivered an all-round performance over the last 4-6 years.11

4. Myth 4: Every “green” shift is profitable and scalable.

Reality: Only 9% of portfolios that became greener figure in the top quartile.

If judged by the growing interest of investors, there is a perspective that green portfolios and sustainable business models are can’t-miss and must-own investments of the future. And while costs have fallen considerably, the relative economics of green energy businesses are yet to deliver consistent results. Of the portfolios we analyzed, 22% became greener (i.e., companies that increased the share of natural gas and/or renewables in their portfolio mix) over the past 10 years. But only 9% of them figured in the top quartile. The delivered returns of a business are important for O&G companies that are looking for a scalable and competitive revenue source that can generate similar, if not higher, returns of around 20%.12

For instance, a few electric-vehicle charging station companies have seen their stock price rising by up to 3000% in the last 12 months, although they’ve only made losses since incorporation.13 Examples like these strengthen the caution of conventional O&G companies that are scrutinizing the green wave from the sidelines. But in cases where O&G companies have made investments in renewables or clean tech that are complimentary to their core business, they have seen benefits. Although the green shift is inevitable in the medium-to-long term, striking a right balance between hydrocarbons and green energy can be essential in the near term.

5. Myth 5: Shale’s pain makes all other portfolio options an obvious choice.

Reality: 18-45% of nonshale portfolios analyzed delivered below-average performance.

Since 2012, the going has been tough for US shale companies—the domestic gas price fell to $1.8/MMBtu in 2012 and they had to absorb a price discount of $3-5/bbl in the WTI crude, make repeated capex cuts, and declare layoffs and bankruptcies in 2020,14 which is likely why no shale company figures in our top quartile. Even then, the pain in shale doesn’t make other resources an “obvious” investment choice—in our analysis, about 18% of conventional-heavy portfolios analyzed figure in the third and bottom quartiles, with most delivering average to slightly above-average returns in the overall analysis. The under-performance among offshore deep-water and diversified portfolios is high with 39-45% of them featuring in the bottom two quartiles. Put simply, it’s less about where one drills and more about how one drills—through operational excellence, companies can create a differentiated value irrespective of the resource including shales they are in.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}