The smartphone multiplier: Toward a trillion-dollar economy TMT Predictions 2020

12 minute read

09 December 2019

From selfie sticks and ringtones to mobile ads and apps, the market for smartphone apps, accessories, and ancillary devices is almost as big as the market for smartphones themselves—and it's likely to continue growing fast in the medium term.

Smartphone sales, to state the obvious, are big business. But even that market may soon begin to pale next to the sums commanded by the sale of products and services that depend on smartphone ownership—the so-called “smartphone multiplier.” From selfie sticks and ringtones to mobile ads and apps, smartphone multiplier revenues may eclipse the revenue generated by smartphones themselves in just a few short years.

Learn more

View TMT Predictions 2020, download the report, or create a custom PDF

Download the infographics

Watch the video on this year’s TMT Predictions

Download the Deloitte Insights and Dow Jones app

Subscribe to receive related content

We predict that the smartphone multiplier will drive US$459 billion of revenue in 2020 alone.1 This represents a 15 percent (US$58 billion) increase over the prior year, already greater than the US$26.6 billion (6 percent) year-over-year growth that smartphones may see in 2020.2 With smartphone sales in 2020 expected to reach US$484 billion,3 the entire smartphone ecosystem—smartphones plus smartphone multipliers—will be worth over US$900 billion. And that’s not even including anticipated likely future spend on cellular and fixed-broadband connectivity, each of which is also expected to generate hundreds of billions of dollars in revenue in 2020.4

Nor is this all. We expect the smartphone multiplier market to grow at between 5–10 percent annually through 2023, lifted by continued robust growth in its largest components. This means that in 2023, the smartphone multiplier is likely to generate revenues of more than half a trillion dollars per year.

What does the smartphone multiplier consist of?

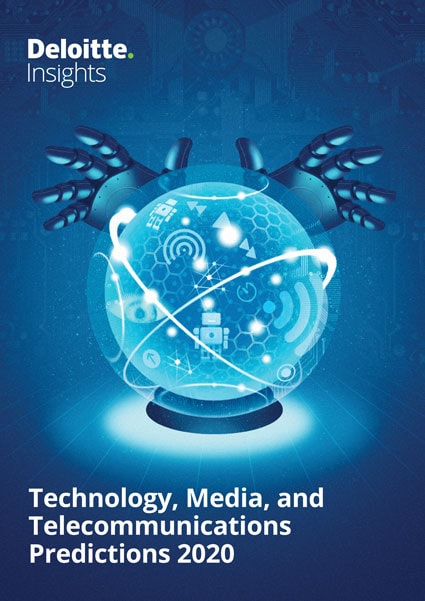

The smartphone multiplier includes a wide array of products and services (figure 1), most of which fall into one of three categories:

- Hardware, including audio accessories, power-related accessories, adjunct devices such as wearables and smart speakers, camera accessories such as selfie sticks and gimbals, cases and screen protectors, phone stands, and spare parts.

- Content, including mobile advertising and software content spanning games, music, video, and many other content types.

- Services, including repairs, insurance, cloud storage, and business software.

A note about wearables and smart speakers

Our 2020 smartphone multiplier forecast includes revenues for wearables (primarily fitness trackers and smart watches) and smart speakers because—while these are distinct devices in their own right—their utility is highly reliant on smartphones.

Although smart watches have their own screens and processors, and a few models have cellular modems, their usefulness is greatly enhanced when they act as companion devices to smartphones. The battery in a smart watch is too small to permit sustained usage of a cellular modem.5 With its larger battery, a smartphone can fill the gap, relaying subsets of information (such as news or messages) via Bluetooth to the smart watch’s screen.

With regard to fitness trackers and smart watches, the fitness and environmental data they collect (such as steps, heart rate, and sound levels) can be much more comprehensively displayed on a smartphone’s larger screen. This data can also be more readily shared with third parties via a smartphone’s modem.

As for smart speakers, the vast majority are screenless and require the use of a smartphone to configure at all, as well as to display any information they may generate, such as the output of search requests.

In 2020, we expect the three largest elements of the smartphone multiplier to be mobile advertising, apps (mostly games), and hardware accessories. We predict these three elements together will generate US$370 billion, or 81 percent of the total, in 2020. For perspective, consider that the value of smartphone hardware accessories alone (US$77 billion) is several times that of other entire device categories: three times greater than tablets (US$25 billion), five times more than video game consoles (US$15 billion), eight times more than smart speakers (US$9 billion), and 11 times greater than virtual reality devices (US$7 billion).6

Inside the top three smartphone multiplier moneymakers

Mobile advertising: Billions of dollars’ worth

Mobile advertising, the smartphone multiplier’s top moneymaker, has thrived despite the smartphone’s relatively small screen. While the phone screen offers little real estate, it is near-ubiquitous, heavily used, and deeply personal. We predict that smartphones’ share of all mobile (smartphone and tablet) advertising will reach about US$176 billion in 2020, an 18 percent increase year over year.

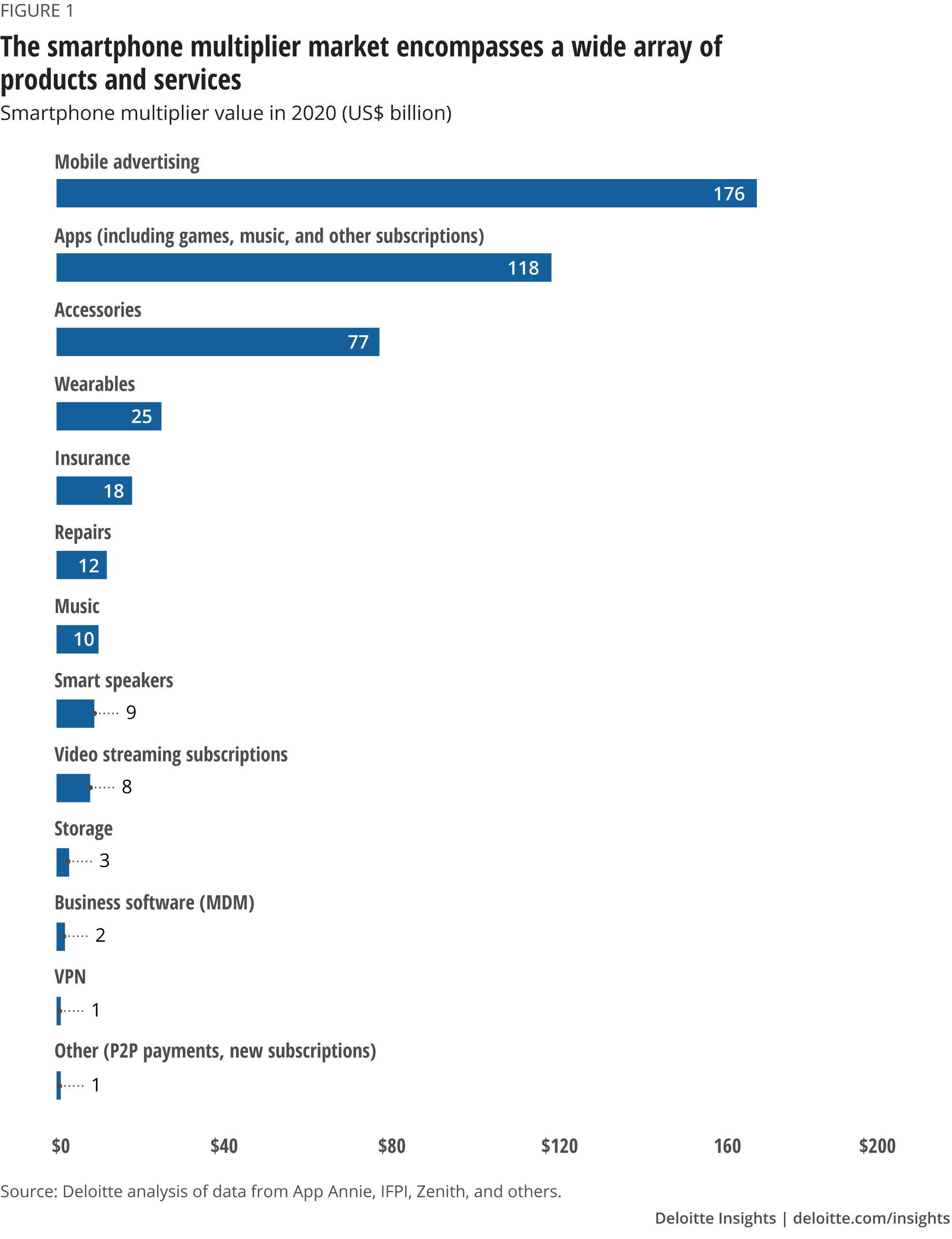

Mobile advertising itself will continue to grow strongly, having already overtaken TV advertising as the world’s biggest advertising category in 2019.7 Mobile advertising’s share of all ad spend is forecast to grow by 13.2 percentage points between 2017 and 2020 (figure 3). This contrasts with TV advertising’s decline of 4.7 percentage points over the same period. In subsequent years, too, mobile advertising may continue to grow rapidly, supported by the introduction of new mobile ad formats. Spending on mobile ads is expected to grow by 13 percent between 2020–2021, which should enable online ads overall (across all devices) to represent more than half (52 percent) of all advertising revenue by 2021.8 Particularly notable is that online ad growth is being propelled by online video and social media—genres that are bolstered primarily by sustained advances in smartphone technology.9

One thing that makes smartphones so attractive to advertisers is their seamless capabilities for commerce. A smartphone user can find, view, buy, and review a product with just a few taps. Prestored credit card and address information coupled with biometric authentication can make transactions almost instantaneous. Newer functionalities such as augmented reality filters can even allow people to try before they buy. This capability has been used for a range of goods, such as makeup by Kylie Jenner.10 This contrasts with ads on traditional media, such as television and print advertising, that require consumers to shift to a connected screen to search for or buy a product.

Mobile ad revenues may also get a boost from the introduction of visual search (also known as reverse image search).11 With visual search, an image, rather than words, serves as the search term. Smartphones, which are far more capable of photographing objects than laptops or tablets, are ideal for instigating such searches; as smartphone camera capabilities continue to improve, especially in low-light conditions,12 the use of visual search is likely to rise. Visual search is just beginning to gain ground in the West, but it is already prominent in China, where up to a quarter of searches currently start with an image. One leading visual search engine, Taobao from Alibaba, hosts over 3 billion images of 10 million products.13

Smartphones are also likely to dominate in one other ad format: App install advertisements, which are expected to be worth over US$60 billion in 2020.14 App install ads appear within apps to encourage users to download other apps. Each app installed and opened may generate a few dollars in payments. While apps are available on all devices, their usage is highest on smartphones, making them the likely primary vehicle for delivering app install ads to users.

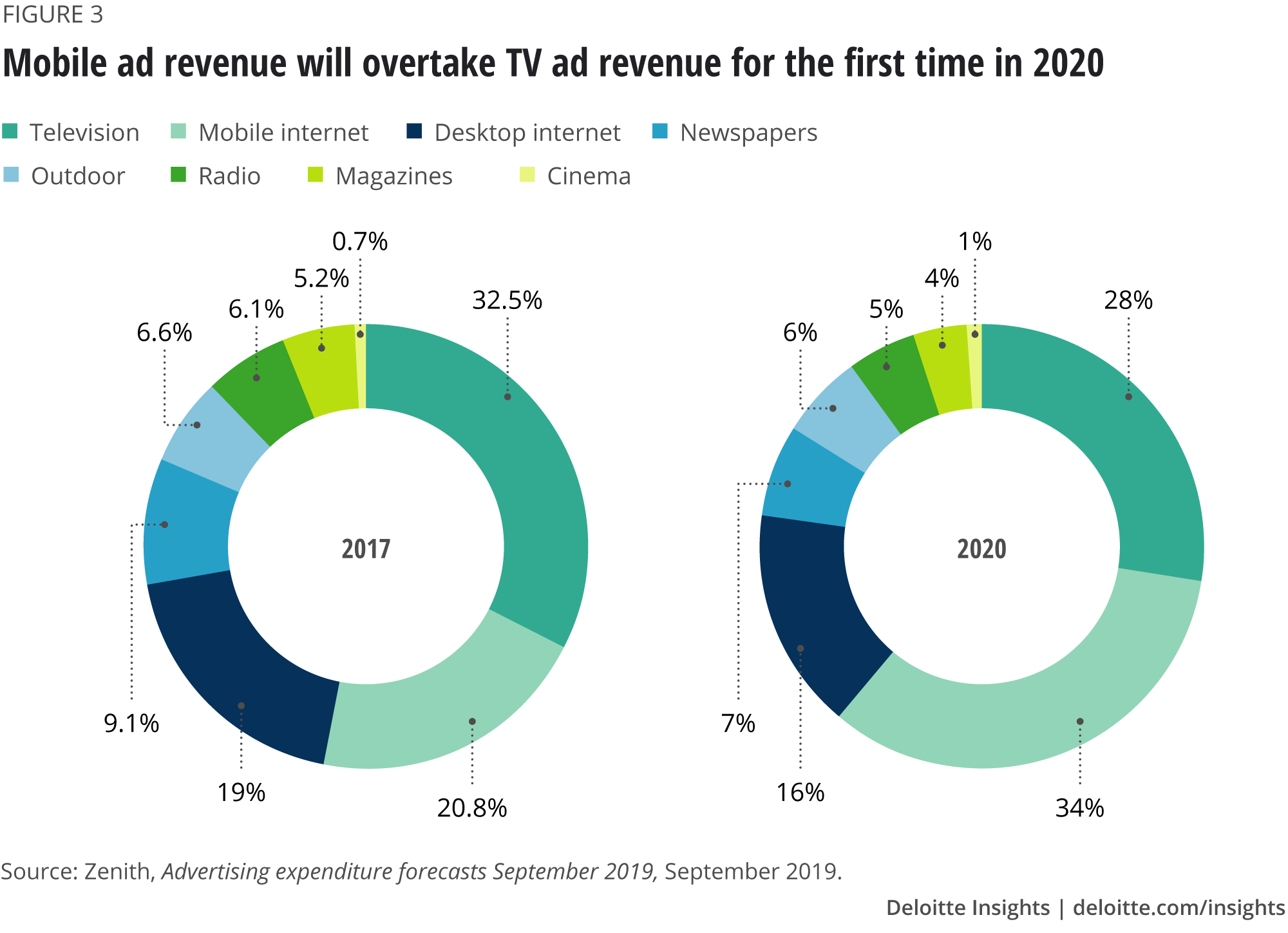

Interestingly, mobile ads account for almost all of the growth in online ad spend since 2014. Mobile ad spend is forecast to increase from US$56 billion in 2015—about a third of total online advertising spend—to US$251 billion in 2021, 71 percent of the total. During this period, desktop online ad spend is expected to remain largely unchanged at about US$102 billion per year (figure 4).15

Apps: Games, games, and more games

The second-largest component of the smartphone multiplier market is apps, expected to generate US$118 billion in 2020.16 We expect the value of app stores to continue to grow in the near term, driven primarily by existing apps.

Perhaps to no one’s surprise, we predict that the top app stores by revenue in 2020 will be Google Play and Apple’s App Store.17 These two stores combined are expected to generate about three-quarters of 2020’s total app store revenues. The remainder will be distributed among hundreds of other app stores, some of which are managed by smartphone vendors such as Samsung, Huawei, and Xiaomi.18 Many are located in China, which has an estimated 300 Android app stores.

Apps exist in a smorgasbord of genres, including games, photo and video, entertainment and lifestyle, social networking, and music. In addition, app store revenues include a small proportion of subscription video on demand (SVOD) and music revenue. The largest content providers for these tend to have a direct billing relationship with subscribers.

Game apps make the most money by far. They are expected to earn around US$80 billion in revenue in 2020, up by over 10 percent from 2019.19 And while mobile phones and games have long had a close relationship—even most 2G handsets came with at least one bundled game (remember Snake?)—the smartphone, along with app stores and the freemium business model, has enabled the mobile game market to take off. According to one forecast, revenues for game apps for smartphones and tablets may surpass US$100 billion by 2022, with smartphone users representing over 80 percent of this.20 Revenues may be lifted further by the availability of mobile games subscription services. Apple launched a game subscription service, Apple Arcade, in September 2019, which offers access to more than 100 games—some exclusive to the platform when played on mobile devices—for a monthly payment of US$4.99 per household.21 Google launched its game subscription service, Play Pass, on September 23, 2019.22

The mobile game industry has undoubtedly benefited from smartphones’ increasing processing power, which makes gameplay more compelling. The most powerful smartphones now support 120Hz games. At 120Hz, the screen refreshes 120 times per second,23 enabling smooth motion graphics, ideal for fast-moving games. As of May 2019, more than 100 titles supported this frame rate.24

The introduction of game streaming, in which gameplay takes place in the cloud and is then streamed to a device, may further boost the market. Hatch Premium, one of the first game-streaming subscription services, offers instant, unlimited access to more than 100 high-quality, premium mobile games, including Hatch Originals. As well as freeing up device memory space, game streaming also enables massive collaborative play: Hundreds of people could collectively solve a puzzle, hunt an enemy, or run a race. The low latency available with 5G could make mobile game streaming an even more compelling experience.25

Hardware accessories: Headphones, batteries, and cases

The smartphone hardware accessories market, projected to be worth US$77 billion in 2020, consists of three principal subcategories: audio, power, and protection. Of these, audio and power are likely to experience significant growth over the medium term.

Headphone sales may grow markedly over the next few years, predominantly driven by users upgrading wired headphones for wireless versions. Currently, wired headphones are the norm among smartphone owners in a range of developed countries (Belgium, Canada, Denmark, Finland, Germany, Ireland, Italy, Japan, the Netherlands, Norway, South Korea, Spain, Sweden, UK, USA). According to our 2019 mobile consumer survey for developed countries, 68 percent of smartphone owners have wired earbuds, while only 23 percent had a wireless model.26 But although they are more expensive—quality wireless earbuds typically cost between US$100–US$200, while simple wired earbuds rarely cost more than US$30—wireless sets have the advantage in ease of use: There are no cords to untangle, and the earbuds have little chance of being yanked out by a stray arm or chair armrest. Some claim that wireless earbuds also offer better audio quality. Over the next few years, we expect most owners to ditch the cable, driving wireless earbud sales up to a potential 129 million units in 2020, from 46 million in 2018.27

Further, we expect headphones to be regularly upgraded over the coming decade as new functionalities become available. Improvements in audio quality, noise cancellation, battery life, water and sweat resistance, and wireless charging are all possible. A minority of smartphone owners will also purchase multiple headphones, each suited to different contexts, such as office, exercise, commuting, and high-fidelity. Currently, among headphone owners in the United Kingdom, 28 percent have two types, 11 percent have three, and nine percent have four.28

The demand for power-related accessories (external batteries, replacement batteries, chargers, and cables) should remain strong over the coming years. Purchases of higher-speed chargers are one likely driver of growth, especially as more smartphones integrate USB-C technology. Currently, chargers vary widely in the rate at which they can transmit power: A standard charger works at 2.5 watts, while the fastest units for smartphones operate at 40 watts.29 USB-C chargers, however, can operate at up to 100 watts—40 times faster than the current standard—and they can support bidirectionality as well (so a device can send as well as receive power).30 The migration to USB-C is expected to take many years to complete, implying multiple years of upgrade purchases to come.

Demand for wireless charging accessories will also likely rise. Wireless chargers transmit power more slowly, but some users may find them more convenient. While only a minority (about 20 percent) of smartphone owners in developed countries now have a wireless charger, ownership should increase over the coming years now that major smartphone vendors have agreed to adopt the Qi standard for wireless power transfer.31 The establishment of a common standard is likely to prompt third-party accessory makers to introduce a wider range of wireless chargers, which should continue to bring their cost down. (Wireless chargers today cost about US$10, and they are becoming increasingly more affordable.)32 A few wireless chargers are now also able to charge multiple devices simultaneously,33 a capability which will grow in attractiveness as users accumulate more peripherals that support wireless charging, such as wireless earbuds, fitness trackers, and smart watches.

External, portable battery packs are likely to remain popular as well, as charging points are not always available at the point of need. The global power bank market was worth US$16.3 billion in 2017, and is expected to rise to US$19.4 billion by 2025.34 Just over half (51 percent) of smartphone owners in developed countries currently own an external battery; because these battery packs lose capacity over time, they need to be regularly replaced, driving repeat sales. On top of this, the switch to USB-C is likely to spur a slow-moving but inexorable wave of power pack upgrades by consumers hungry for more and faster power.

At the foundation: 3.6 billion smartphone users and counting

Every successful device cultivates—and in turn relies upon—an associated ecosystem. The better the device, the more vibrant the ecosystem. By this measure, the sheer number and variety of smartphone-linked accessories, devices, content, and services surely qualify smartphones as one of history’s most successful products.

Approximately 3.6 billion smartphones are in use globally today. This huge user base is the smartphone multiplier’s essential foundation, and it is still growing. Although global smartphone unit sales appear to be nearing a ceiling of 1.4–1.6 billion units per year, the overall number of smartphone users should continue to increase at both the global and the country level. As it is, the 1.6 billion smartphones expected to sell in 2020 is multiple times the number of sales expected for any other major consumer device.

Smartphone unit sales are forecast to grow somewhat in 2020, boosted by 5G.35 The next few years beyond that may see unit sales decline, albeit modestly. One sign pointing to this possibility is the stretching renewal cycle in many markets. In the five largest European markets, for instance, the average lifetime of a new handset increased from 23.4 months in 2016 to 26.2 months in 2018.36 This may be due to smartphones’ approaching an asymptotic limit of functionality. Upgrades, which are the predominant driver of sales, appear to be becoming less meaningful to mainstream consumers, who may not find the latest crop of features—such as mechanized pop-up selfie cameras, additional rear-facing lenses, or water resistance to greater depths37—worth the cost.38

The launch of 5G handsets will likely stimulate demand moderately. But unlike a decade ago when flip and feature phone users upgraded to both smartphones and 4G in one go, today’s smartphone users may have less motive to buy a 5G device at the first possible opportunity. The upgrade to 4G offered a Wi-Fi type of experience when outdoors, markedly improving the user experience; 5G may not bring a similarly striking additional benefit.

The bottom line

The smartphone market is nearing its peak in terms of unit sales per year. But its power as a foundation for multiple associated revenue streams—advertising, hardware, content, and services—is growing apace. Already approaching half a trillion dollars in 2020, these ancillary revenues may exceed the value of smartphone sales within the next five years. Those looking to strike it rich in the smartphone business may find that the best opportunities lie, not in the smartphone market itself, but in the vast and growing markets the smartphone has created.

One of the largest of these could be payments at physical stores as well as online, enabled by near-field communication (NFC) technology. Payment by smartphone is already common in China, where consumers used their phones to pay for US$41 trillion worth of goods in 2018 (figure 5).39 However, the growth opportunity in Western markets could be significant. Although relatively few Western consumers today use their phone for brick-and-mortar transactions—despite several major players offering the option to do so—adoption could grow as more people come to appreciate the advantages. Smartphone-based payments are more secure than chip-and-PIN or sign-and-swipe methods, both of which remain popular in the United States. With chip-and-pin or sign-and-swipe, a stolen card could be used multiple times before fraud is detected. An individual’s signature can be faked; a personal identification number can be obtained by looking over someone’s shoulder. Smartphones, on the other hand, authenticate users on a per-transaction basis, and they can enable biometric recognition, which can be extremely secure relative to other methods. While it is possible to spoof fingerprint readers and facial imprints, it is very resource-intensive to do so. NFC-based mobile payments use a one-time token to authenticate each payment; if this token is intercepted, it cannot be used for another transaction.40 This capability could be widely deployed to not only accelerate the pace at which individual payments can be made, but also to lessen fraud.41

Another opportunity is enterprise apps, such as software used to handle work email and files securely on a user’s smartphone.42 Little business software today is created specifically for smartphones: Enterprise apps are forecast to generate a modest US$2.4 billion in direct revenue in 2020, far less than the US$118 billion expected for consumer apps in the same year.43 Established and startup companies that can successfully resize and reinvent their B2B software for mobile use—for everything from intranet access to expense processing—could be looking at a potential gold mine. We estimate that in developed markets, only about two-fifths of workers are currently using a smartphone for work tasks beyond calls and instant messaging.44

For billions of people today, it’s hard to imagine life without smartphones—or without the apps, accessories, and ancillary devices that integrate them ever more seamlessly into our lives. The booming smartphone multiplier market presents a clear opportunity for businesses that can devise even more ways to extend smartphones’ capabilities. We don’t expect that opportunity to fade anytime soon.

Technology Consulting

Today, business and technology innovation are inextricably linked and the demand for technology-enabled business transformation services is rapidly growing. Deloitte technology professionals around the world help clients resolve their most critical information and technology challenges.

Learn more

Get in touch

- Paul J. Sallomi

- Global TMT industry leader, Partner

- Deloitte Tax LLP

- psallomi@deloitte.com

- +1 408 704 4100

TMT Predictions 2020

Explore the collection

-

My antennae are tingling: Terrestrial TV’s surprising staying power Article4 years ago

My antennae are tingling: Terrestrial TV’s surprising staying power Article4 years ago -

Robots on the move: Professional service robots set for double-digit growth Article4 years ago

Robots on the move: Professional service robots set for double-digit growth Article4 years ago -

-

Ad-supported video: Will the United States follow Asia’s lead? Article4 years ago

Ad-supported video: Will the United States follow Asia’s lead? Article4 years ago -

High speed from low orbit: A broadband revolution or a bunch of space junk? Article4 years ago

High speed from low orbit: A broadband revolution or a bunch of space junk? Article4 years ago