Brazil has been saved

Cover image by: Tushar Barman

Brazil had a rough ride in 2020 with the pandemic deeply impacting public health and economic activity. Yet the economy also saw some light at the end of the tunnel as growth continued its rebound into the fourth quarter of last year.1 Forward-looking economic indicators, however, suggest only a modest expansion in the first quarter of 2021. This is most likely due to a steady rise in COVID-19 infection rates2 since November of last year, which in turn has impacted consumer and business confidence. Fiscal support, which came to the economy’s aid in 2020, is unlikely to play a major role this year as the government turns to healing its finances. So, will monetary policy play a greater role in aiding growth? That is unlikely as the central banks shifts focus to inflationary pressures in the economy, including rising production costs and currency weakness. On March 17, the central bank raised rates by 75 basis points and hinted at further tightening if inflation expectations do not remain anchored.3

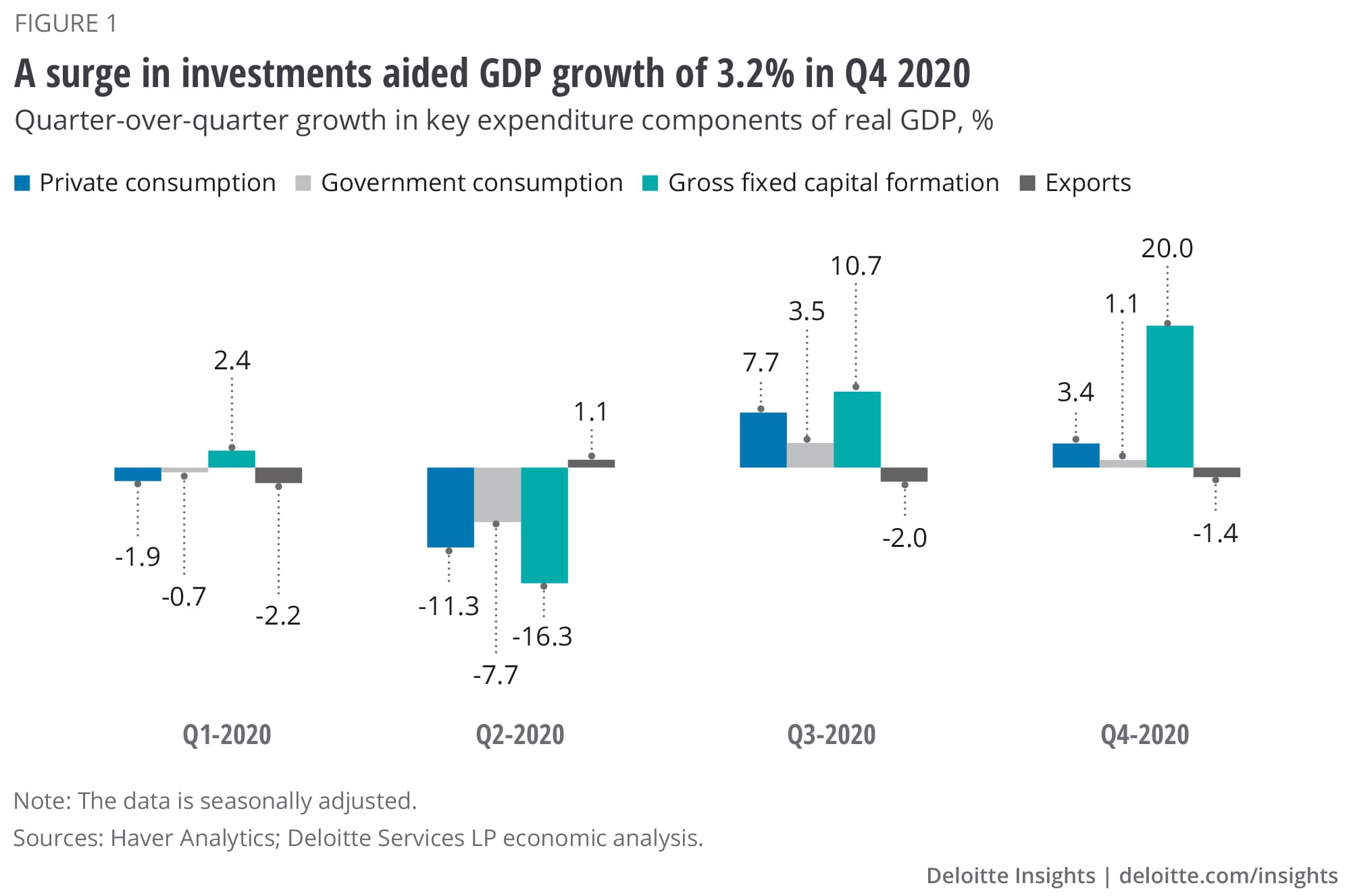

The economy continued its rebound in the final quarter of last year although growth slowed from the sharp expansion in the previous quarter. Real GDP grew by 3.2% quarter-over-quarter in Q4 2020 with expansion in domestic demand offsetting a decline in exports. Investment was a standout for the economy during the quarter with gross fixed capital formation rising by 20%, the fastest pace of quarterly expansion since the series started. This augurs well for potential economic growth. Private consumption continued to support the economy in Q4, although its contribution slowed from Q3 (figure 1). And government spending too eased as the focus started shifting toward healing fiscal health following strong stimulus measures after the start of the pandemic last year. Figure 1 also shows faltering support to the economy from the external sector with exports contracting for the second straight quarter in Q4. Overall, the economy contracted by 4.4% over the whole of 2020, a setback to the modest recovery that had started to take shape in 2017.

A steady rise in new virus cases since November 20204 is a grim reminder that COVID-19 continues to cast a shadow on economic prospects for Brazil as consumers and businesses struggle to reconcile the urge to stay safe with the need for incomes and revenues. Rising virus cases also mean greater implementation of social distancing measures. For example, Brazil's capital, Brasilia, entered a two-week lockdown toward the end of February and at least eight states have adopted curfews.5 While the start of vaccinations offers hope for the economy, the end-goal of herd immunity6 is still some time away given that only 4.2% of the population have received at least one dose of the vaccine till March 15.7

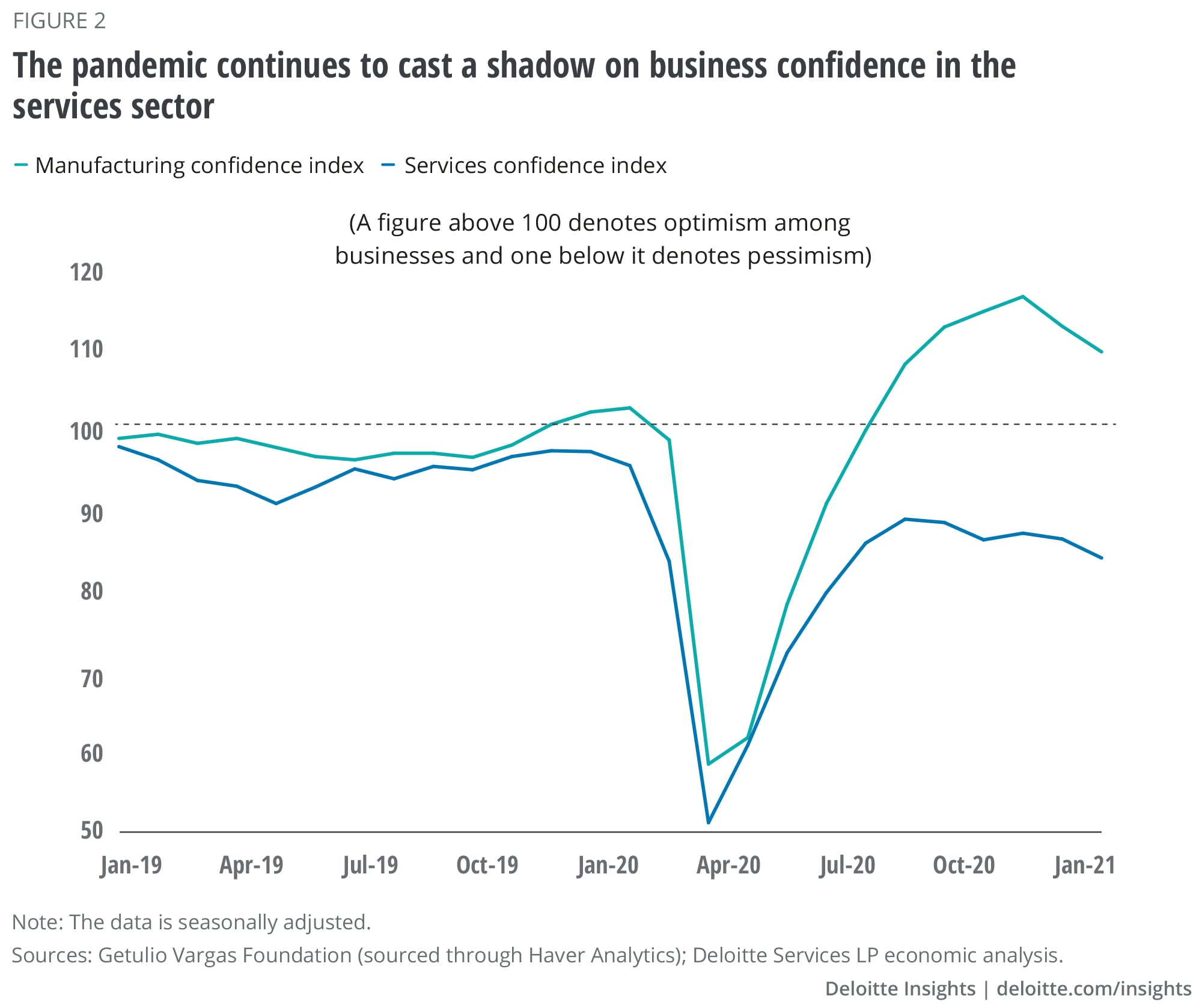

Consequently, the virus continues to weigh on businesses and consumers. Manufacturing output, for example, contracted by 0.1% in January from the previous month. Consumer spending, too, appears to have lost a bit of momentum with retail sales volumes contracting for the second consecutive month in January.8 Consumers’ concerns appear to show up in confidence indicators as well—according to the Getulio Vargas Foundation,9 consumer confidence is still in pessimistic territory with the index nearly 10 points lower in February compared to a year back. Virus fears and prospects of weakening domestic demand appear to be putting off businesses too (figure 2), especially in services10 where sectors such as food services, hospitality, and travel continue to face the burden of the pandemic.

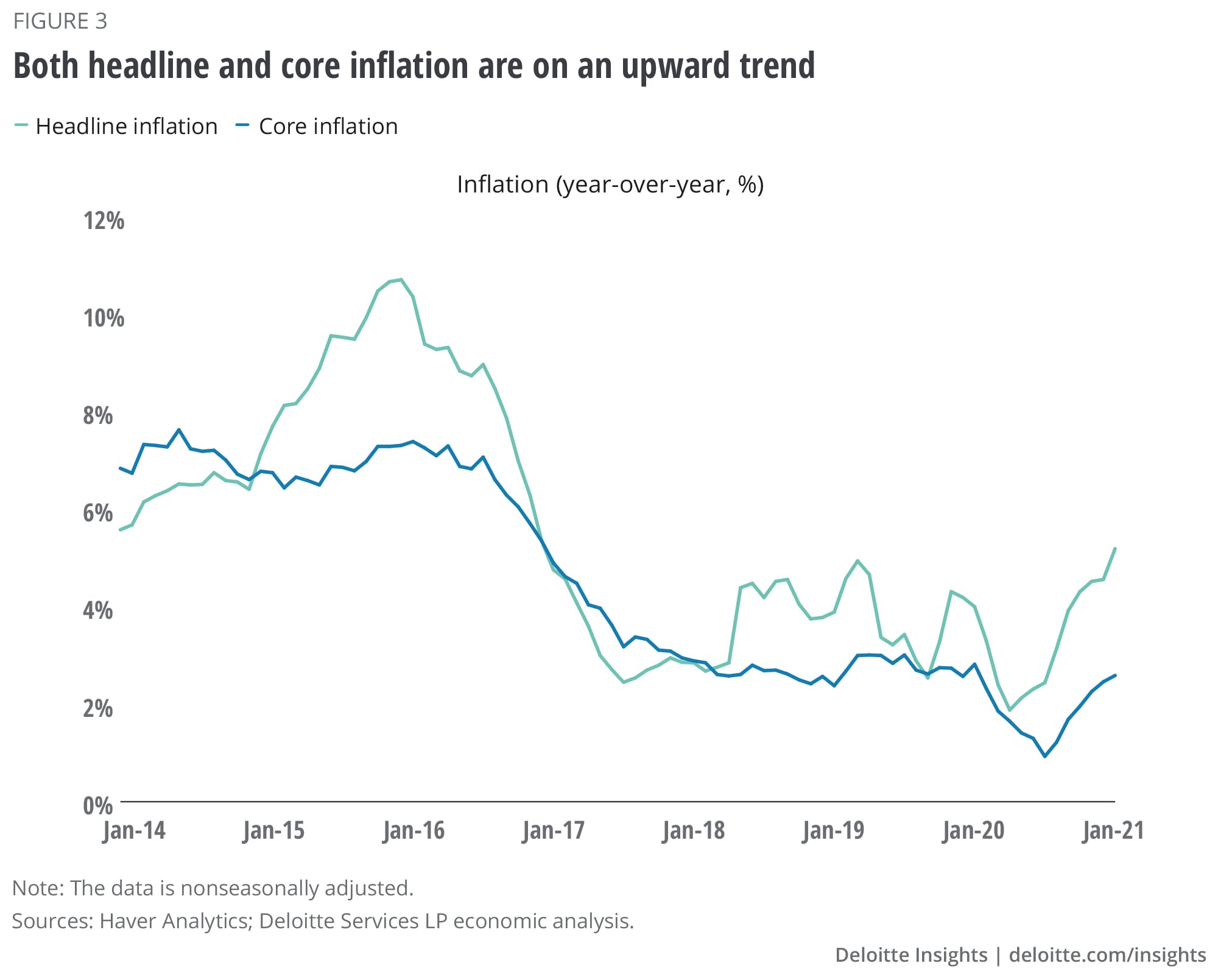

As worries over the virus persist, there are also concerns about an old foe—inflation. Price pressures have been increasing since the middle of last year with headline inflation touching 5.2% in February, higher than the Banco Central do Brasil’s (BCB’s) mid-point target11 of 3.75% for 2021. Rising food prices have been a key driver of headline inflation with housing goods-related inflation also contributing to overall growth in consumer prices. And although core inflation, which excludes volatile food and energy prices, is relatively lower than overall inflation—core inflation was 2.6% in February—it has been steadily edging up since August 2020 (figure 3). Producer prices have also surged in recent months due to sharp increases in prices of intermediate goods and commodities. Since the middle of 2020, producer price inflation has accelerated sharply, rising to 23% in January. This does not augur well for headline inflation, especially if a sustained rise in the cost of production forces producers (and retailers) to pass it on to consumers.

Closely linked to BCB’s inflation worries is currency weakness. Like major emerging market currencies, the Brazilian real weakened sharply when the pandemic started. The currency fell by 15.6% against the United States dollar between February and March of last year with further depreciation in the next few months. While the economic rebound in the second half of last year has enabled the currency to recover some of its losses, the real was still 22.9% below the dollar in February compared to a year back. This is much worse than other emerging market currencies such as India’s rupee and Mexico’s peso (figure 4). A slow recovery in portfolio flows into the country hasn’t helped either. Between March and April of 2020, nonresident portfolio outflows from Brazil amounted to about US$32 billion due to a global spike in risk aversion;12 this loss is yet to be offset by recovering inflows since June 2020.

High virus cases amid signs of a loss in economic momentum early this year poses a unique problem for the economy, especially with the government signaling a move toward fiscal consolidation after strong stimulus measures last year. Where does further policy support to the economy come from? Well, certainly not from the central bank as the BCB turns its gaze on rising price pressures amid currency weakness and high producer prices. The BCB also knows too well the burden of central bank credibility;13 it can look back to the period between 2013 and 2015 when rising inflation put the brakes on economic growth and stability. Consequently, the BCB started adopting a more hawkish tone early this year.14 And in its March meeting, it started the process of normalizing monetary policy by raising its key policy rate by 75 basis points to 2.75%, its first rate hike in six years.15 And the BCB also raised the specter of monetary tightening if inflation expectations do not remain anchored, including a 175 basis points hike to the policy rate in the central bank’s baseline scenario this year.16

Much of the economy’s fate, therefore, will depend on how the pandemic evolves in the country. Controlling the spread of the virus and increasing the pace of vaccinations may perhaps be the best bet to get consumers and businesses back on their feet.

{kind=link}

{kind=link}

{kind=link}

{kind=link}