Japan economic outlook, May 2023 has been saved

Cover image by: Jaime Austin

Japan’s economy struggled to rebound after fully reopening in the second half of last year. Real GDP contracted in 2022 Q3 and inched up by just 0.1% on an annualized basis in Q4.1 However, the economy has gained momentum in 2023. Surveys of business activity indicate the economy has been growing moderately since January, which bodes well for Q1 real GDP growth.2 The service sector has been gaining momentum, thanks to a rebound in consumer spending and the reopening of borders. The labor market remains relatively tight, and wages are expected to accelerate this year.

The rebound in economic activity has contributed to inflation running above the Bank of Japan’s (BoJ’s) 2% target. So far, the central bank has maintained its highly accommodative monetary policy stance. However, inflationary pressures may require modest tightening from the BoJ. In addition, changes to the supply chain could create inflationary pressure, as the cost of moving production lines can be high.

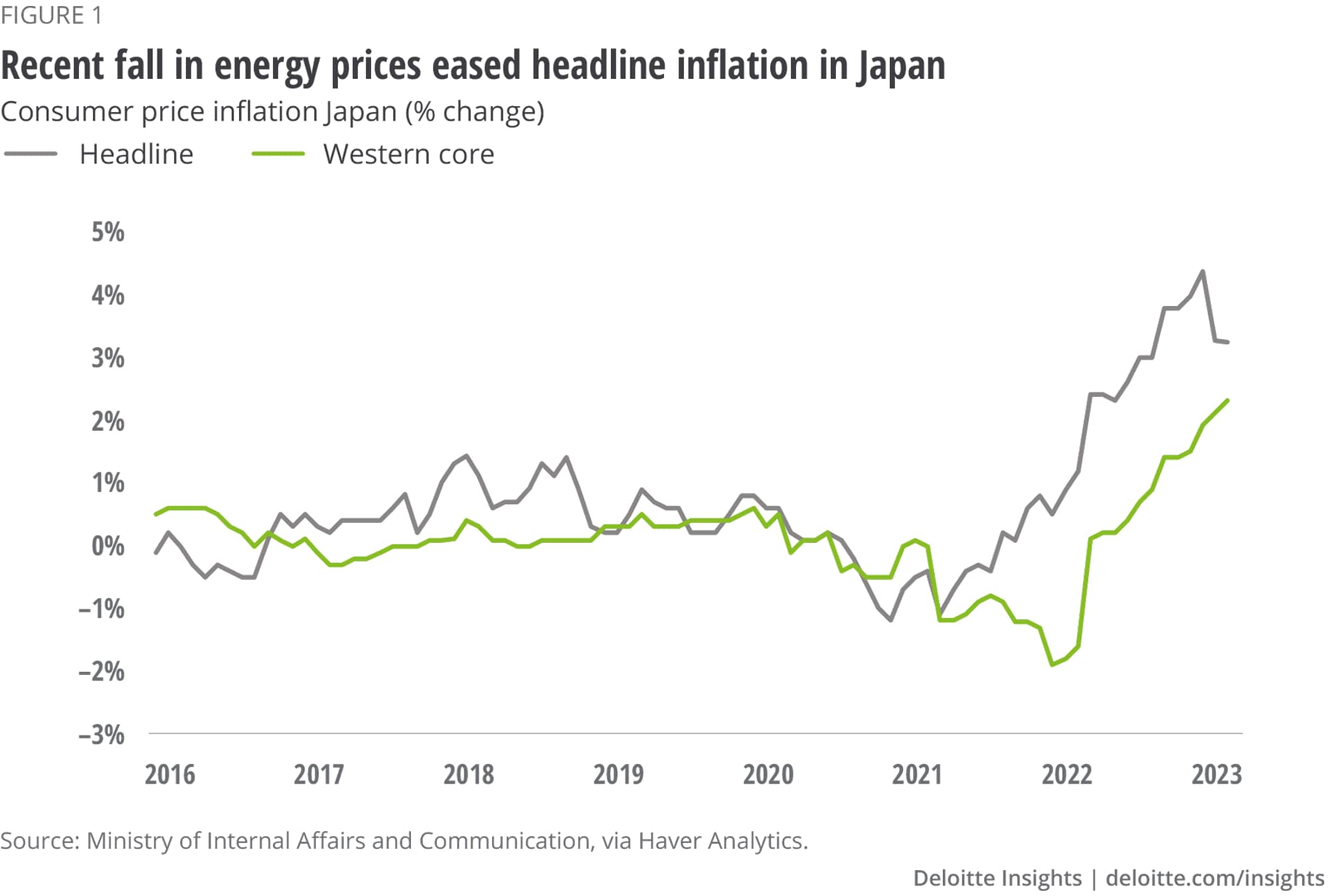

The BoJ left its monetary policy unchanged in April. The new governor of the central bank expects inflation to ease in the second half of this year,3 thereby allowing the bank to maintain its accommodative policy stance. The weighted median inflation rate, one of the central bank’s underlying inflation gauges, slipped to 1% year over year in March,4 which likely gives the central bank some confidence that inflation remains relatively benign. Plus, headline inflation eased to just 3.2% year over year in March, down from 4.3% in January, thanks to easing energy costs.5

Although the central bank currently expects inflation to ease later this year, it may prove to be more enduring. Indeed, inflation has defied central bankers’ expectations throughout much of the developed world recently. Central bankers initially expected inflation to be transitory and delayed rate hikes as a result. For example, US core inflation was above the 2% target for a year before the Fed responded with higher interest rates.6 Japan is still nowhere near the inflation that the US or Europe has seen recently, but several signs suggest that inflation may struggle to move lower without central bank intervention.

Headline inflation eased recently, but it was almost entirely due to falling energy prices (figure 1). Western core inflation, which excludes food and energy, accelerated to 2.3% year over year in March. This measure of inflation also accelerated on a month-to-month basis, indicating that the rise was not due to base effects. Inflation has also been relatively broad-based.7 Over 80% of the items in the consumer price index (CPI) have been increasing in the last three months.8 Furniture, household utensils, apparel, medical care, and recreation all had accelerating prices to start the year. Home rental prices continue to be flat, which has been crucial in preventing stronger inflation. However, residential property prices were up 7.9% in December from a year earlier.9 Higher home sale prices could lead to an uptick in rental prices, which would further aggravate inflationary pressure.

Inflation expectations also remain very strong. In February, 65.8% of households expected prices to rise 5% or more over the next year, the highest share since the data began in 2004.10 Since then, the share of households expecting inflation to top 5% has dipped to a still lofty 56.3%. Businesses also expect inflation to run hot. Their inflation outlook over the next three years was 2.3%, on average, which was also the highest on record.11 Small- and medium-sized firms have also indicated that they are continuing to raise prices, which points to additional price pressure in the near term.

Import and producer prices have improved recently, but both remain uncomfortably high on a year-ago basis. Producer prices were up 7.2%, while import prices were still 9.9% higher than a year earlier.12 Although these prices should ease further, labor costs are likely just beginning to ramp up. One assessment of the ongoing shunto, or spring wage negotiations, shows wages should rise 3.7%.13 Not all businesses participate, and the wage gains announced typically outpace those seen in the economy as a whole. For example, contractual wage growth was just 1.6% higher than a year earlier in Q4 2022, despite a 2.1% gain during the shunto that year. If a similar differential between announced wage gains and actual wage growth emerges this year, Japan could still see contractual wage growth rise by more than 3%.

A 3% rise in wages is likely inconsistent with 2% inflation. Wage growth can be offset by a rise in labor productivity. However, labor productivity in Japan has been weak. Productivity growth in services has been negative in seven of the last 10 years.14 Although productivity growth has been stronger in the manufacturing sector, it has averaged just 0.5% over the last decade. Assuming wages grow by 3% and labor productivity growth remains relatively flat, inflation will run hotter than 2%, which will likely force the BoJ to tighten policy.

Consumer demand has been notably strong this year. Retail sales accelerated, rising 7.3% from a year earlier.15 Spending on general merchandise and motor vehicles has been growing by double digits. Strong wage growth will help support demand going into the summer. The labor market also appears relatively strong, with the unemployment rate hovering around where it was before the pandemic. Plus, the number of job openings was up more than 10% from a year earlier in February,16 which should put downward pressure on unemployment and upward pressure on wages.

Some of the strength in consumer spending is likely still pent-up demand after pandemic-related restrictions were lifted toward the end of last year. Even so, there seems to be additional upside for spending, especially for services. For example, the number of guests at accommodation facilities in January was more than 7% lower than it was in 2019.17 Plus, the number of foreign visitors in Japan was still more than a third lower than prepandemic levels in March. As the economy continues to normalize, demand for tourism-related services, such as hotels, airfare, and eating out, should see some upward movement. This could create additional inflationary pressure in these categories. Prices for food away from home and airline fares were already 7.6% and 5.3% higher than a year earlier, respectively.

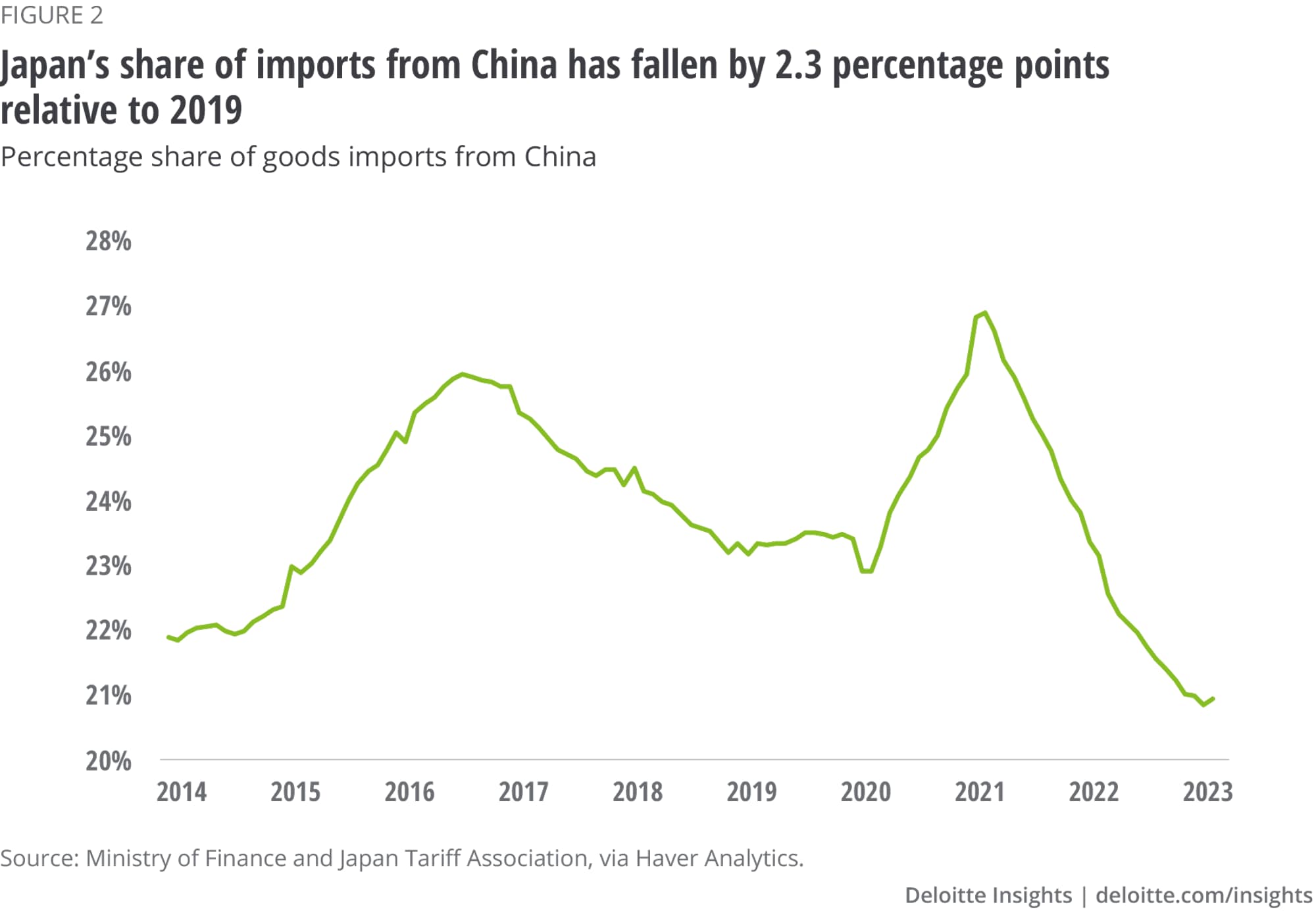

After the pandemic hit, Japan provided incentives for businesses to diversify their supply chains away from China. It appears that some movement away from China may be underway. Japan’s share of imports coming from China has fallen by 2.3 percentage points relative to 2019.18 Some of the loss is due to a higher price of oil, which Japan sources from other countries. For example, the share of imports coming from the Middle East grew by 0.9 percentage point over the same period.19 This aligns with the lost share from other major trading partners, such as the US and EU, which each lost 1.1 and 1.3 percentage points, respectively.

Japan has diverted its imports from China in two key categories. The first is in clothing, where the share of imports coming from China has fallen 5.0 percentage points since 2019.20 Japan’s incentives to diversify trade early in the pandemic, largely focused on medical goods, including apparel used for personal protection. Companies were encouraged to source these goods from other countries, particularly in southeast Asia. Indeed, the share of these imports coming from ASEAN countries grew 3.7 percentage points over the same period.

The second category is in electrical machinery, where China’s import share fell 2.1 percentage points since 2019. Electrical machinery includes semiconductors and related products. The imports of these critical goods now appear to be coming from Taiwan in increasing numbers.

To be clear, Japan still imports more than 20% of goods from China, which is its largest single source of goods imports. It is still a bit early to determine if these changes are the beginning of a larger trend. The pandemic and the supply chain policies Japan implemented are likely having some effect. Geopolitical tensions between China and the West will likely drive additional diversification in supply chains moving forward. If these trends continue, the costs of moving supply chains could be passed on to consumers, which would add to the inflationary pressures seen in the economy.

Japan’s economy is expected to grow modestly as pent-up demand drives spending in the near term, and a relatively strong labor market maintains spending thereafter. The path of inflation will largely determine changes in monetary policy and therefore how quickly the economy can grow this year. The BoJ is likely to take a relatively dovish approach, only tightening modestly this year, as it expects some of the inflationary pressure to recede by year-end. Although this is supportive of growth in the near term, it could lead to higher inflation and a more hawkish response from the BoJ.

{kind=link}

{kind=link}