The pandemic has also reversed years of progress in alleviating poverty in Asia. According to the World Bank, the number of people who were forced into poverty due to COVID-19 has gone up sharply in South Asia, and East Asia and Pacific regions—the increase is about 80–82 million at the US$1.90-a-day poverty line and 180–184 million at the US$3.20 poverty line.14 Apart from rising poverty, the pandemic has also hit the growth of the middle class in Asia—a key beneficiary of strong GDP growth over the last three decades and a major contributor to the region’s global attractiveness as an economic powerhouse. According to Pew Research Center, the size of the middle class is likely to be 32 million lower in South Asia and 19 million lower in East Asia and the Pacific in 2020 relative to pre–COVID-19 estimates.15 In fact, Asia is likely to have contributed the most to the decline in global middle-class population last year, despite having a lower share of middle-income people in the total population compared to several other regions.

Not all is gloom and doom, though

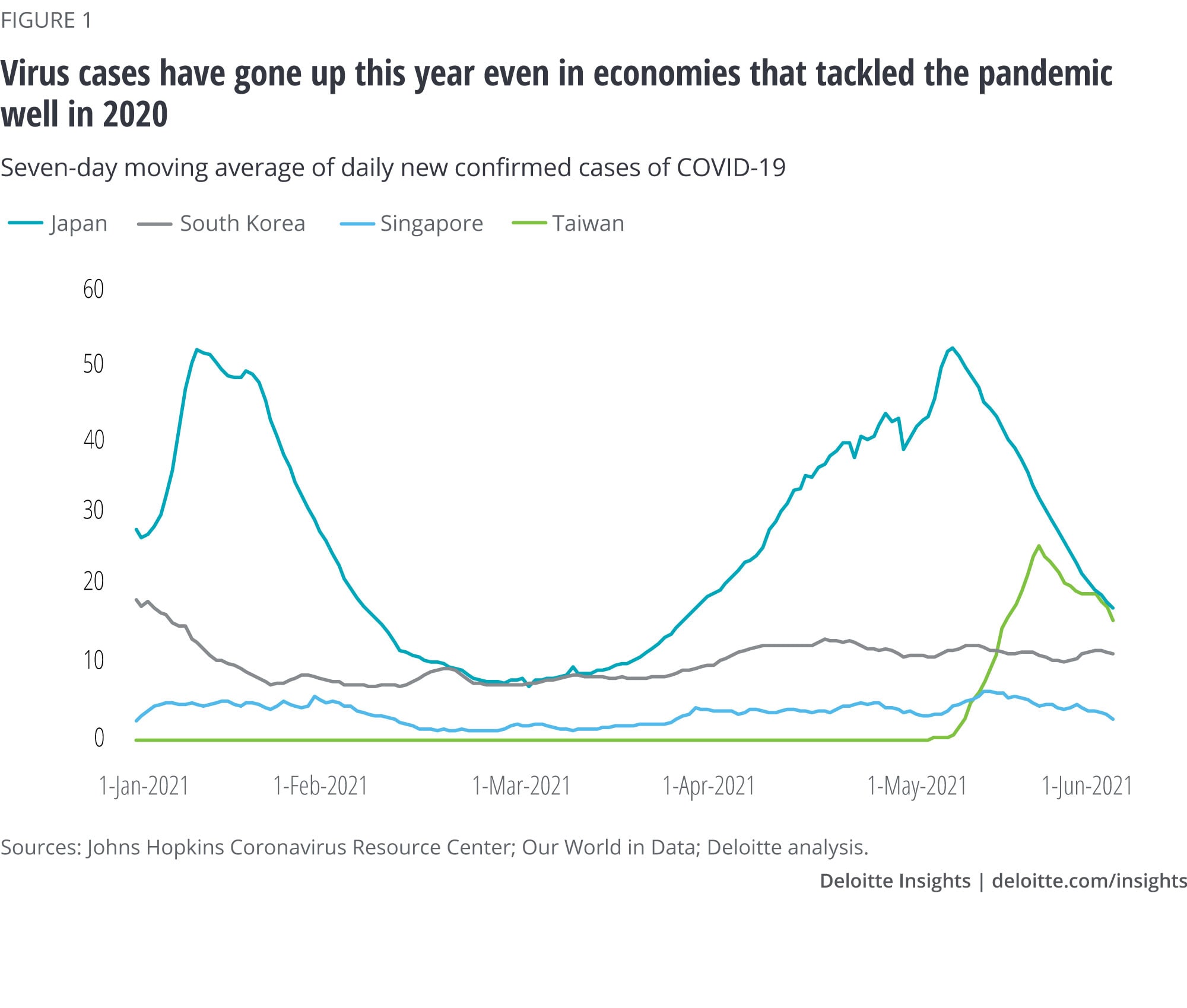

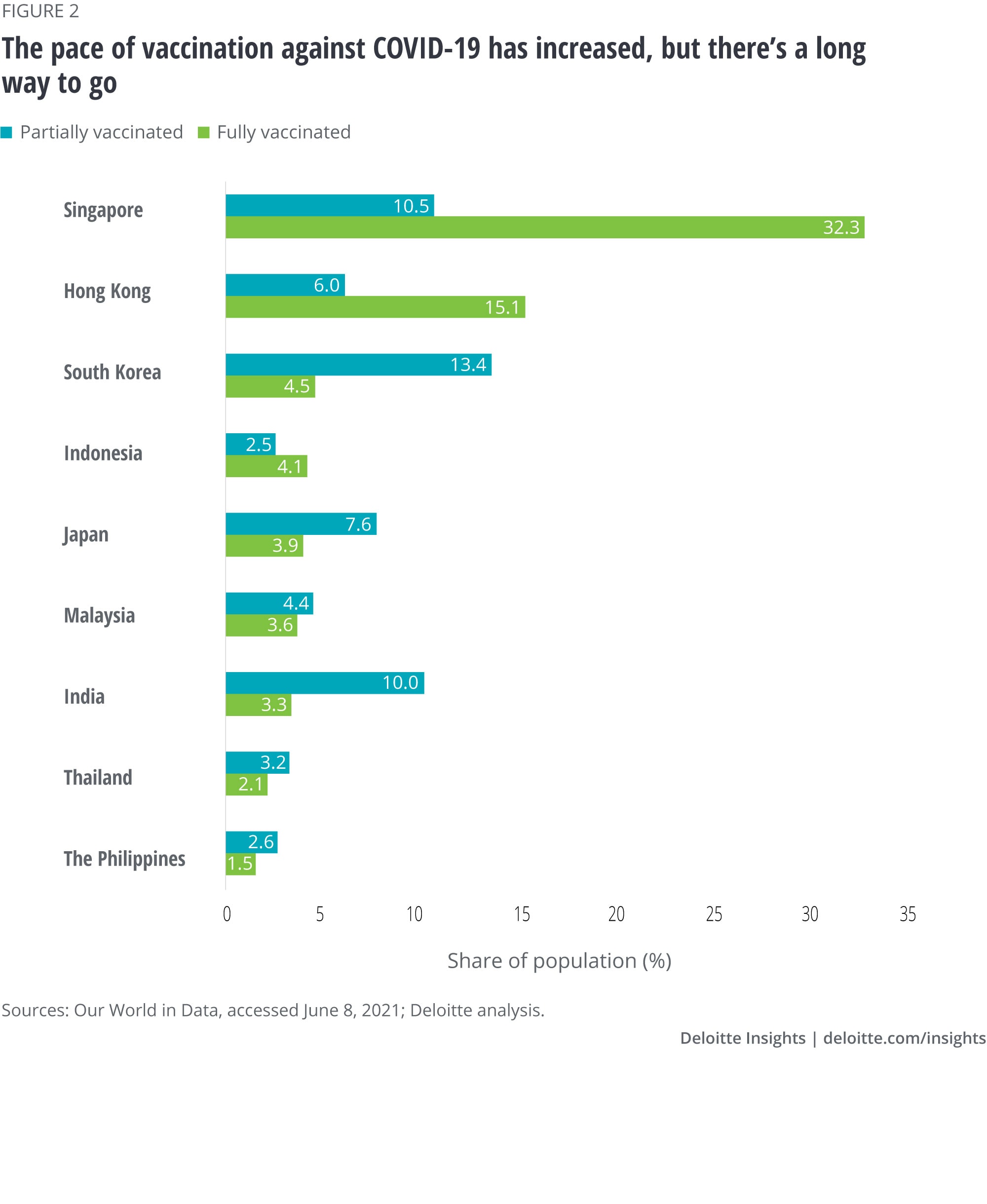

Nevertheless, it will be a tad unwise to write off consumers in Asia. If the pace of vaccination increases and virus cases continue to decline, consumer sentiment and spending will likely improve. Across the Pacific, in the United States, consumers’ concerns about their health and well-being have gone down due to rising vaccination and slowing down of the pandemic.16 Consequently, more people appear willing to travel, go to restaurants and pubs, and attend in-person events now than at any time since the pandemic started last year—this has started to aid services spending in the country.17 The same can be expected in the other parts of the world, including Asia. In fact, consumer confidence in nations across the region has increased every time domestic virus cases have eased. In Indonesia, for example, consumer confidence dipped in January when virus cases went up but then gained as the health situation improved, with sentiment turning to optimism in April for the first time in 13 months.

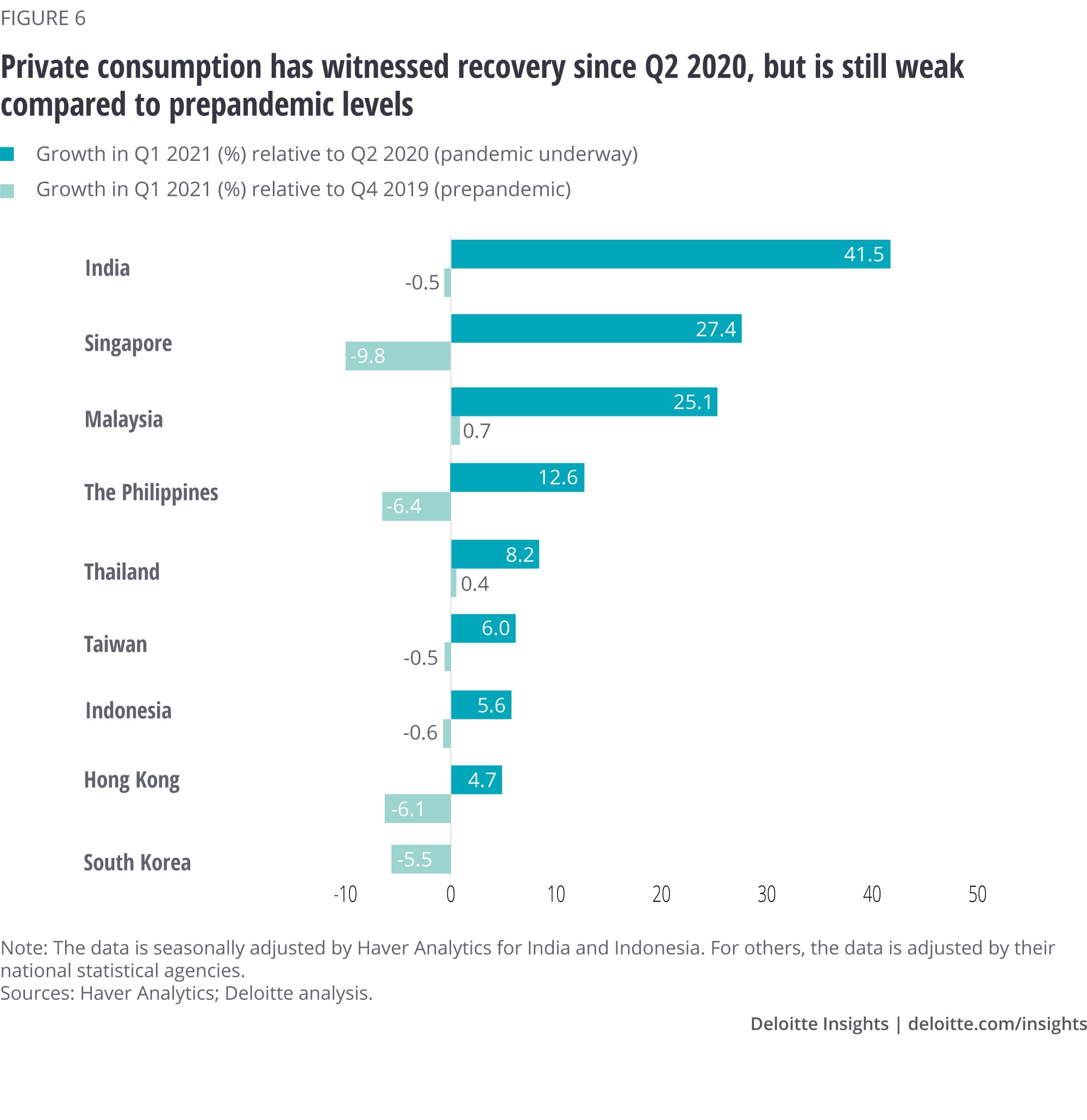

According to national accounts data, change in sentiment leads to an increase in consumer spending. For example, consumer spending started edging up from the second half of 2020 after the initial impact of the pandemic in the first half of the year. Spending, however, at the end of Q1 2021 for most countries was still lower than prepandemic levels (figure 6). This indicates, yet again, that for consumer spending to edge back sharply to pre–COVID-19 levels, countries will have to vaccinate their way out of the pandemic.

While spending is likely to have suffered in the Q2 2021 for some economies due to a resurgence of new virus cases and localized lockdowns, households may find support, directly or indirectly, from fiscal measures that governments are likely to roll out. India18 and Malaysia19 have rolled out new stimulus measures, while the Philippines20 and South Korea21 are likely to follow suit. Direct cash transfers, low-interest financing, and loan moratoriums will help soften some of the blow of localized lockdowns and their impact on key sectors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}