{kind=link}

{kind=link}

South Africa has been saved

Cover image by: Jamie Austin

South Africa’s Finance Minister Enoch Godongwana delivered his maiden Medium Term Budget Policy Statement (MTBPS) on 11 November 2021. As expected, he closely followed the fiscal consolidation and growth stimulation trajectory that was initiated by his predecessor, Tito Mboweni. Indeed, Godongwana stated, “The MTBPS charts a course that demonstrates government’s unflinching commitment to fiscal sustainability, enabling long-term growth by narrowing the budget deficit and stabilising debt.”1

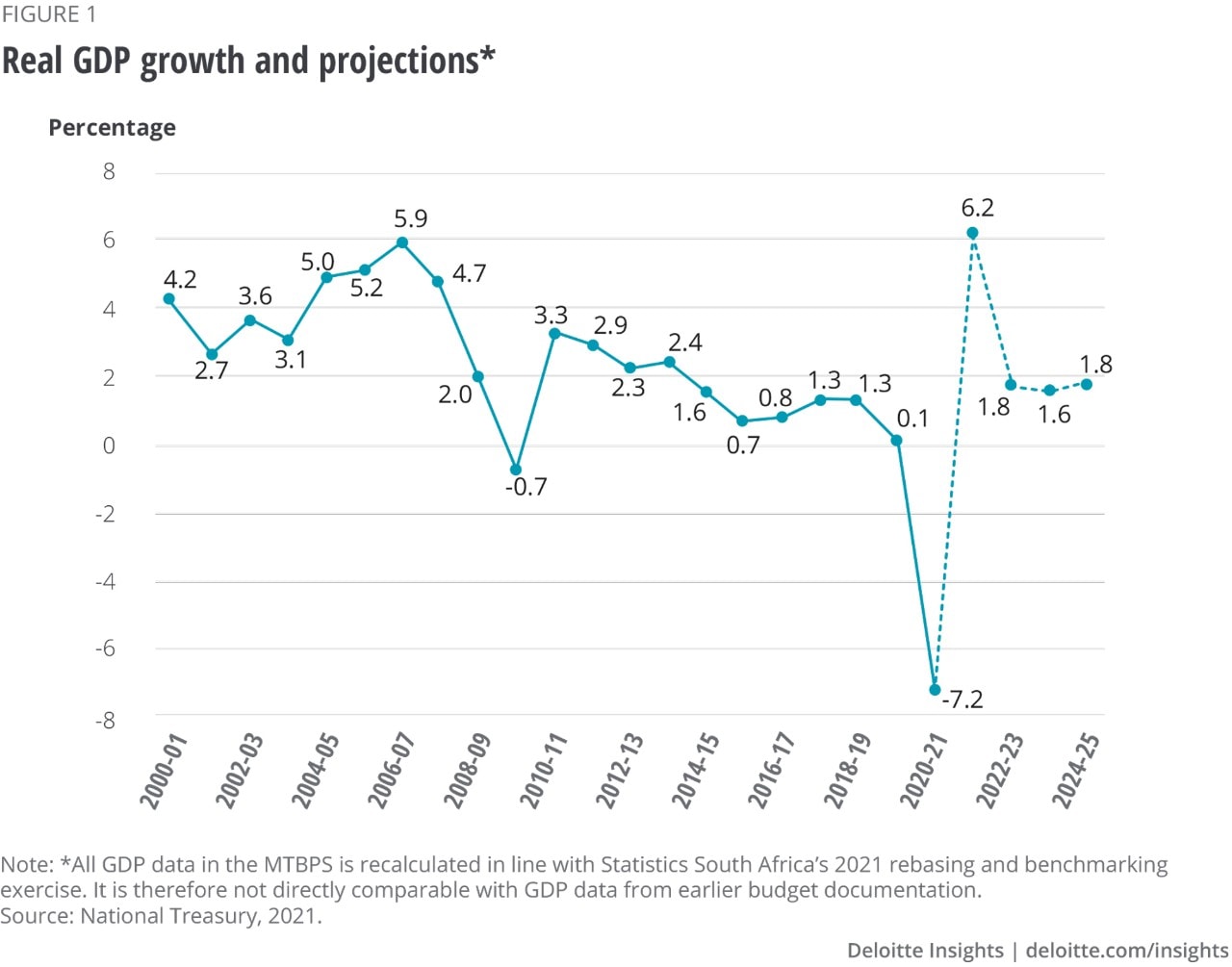

While the economy is expected to rebound at a rate of 5.1% in 2021, this is largely due to base effects following the 6.4% contraction in 2020. From a sectoral perspective, mining and manufacturing grew 25.2% and 17% respectively, year on year, in the first half of 2021. The agricultural sector also saw strong growth over the same period, expanding by 8.3%.

Growth during the second half of 2021 is expected to be less impressive, with public violence and the third wave of the pandemic adversely affecting the manufacturing, wholesale and retail, restaurants, hospitality and recreation sectors. Nonetheless, the South African economy is projected to return to pre-pandemic levels a full year earlier than previously expected, with the outlook for the local economy bolstered by improved global conditions.2

Looking ahead, the uptake of the government’s vaccination drive will partly determine the degree of economic recovery. So too will the government’s reformation efforts, which – as per the updates provided in the MTBPS – are focussed on the electricity, transport, tourism, water, telecommunications and infrastructure sectors. The degree of success in these reforms will have long-lasting effects on the South African economic outlook.

Yet, the economy still faces considerable challenges, with the ongoing fallout from the pandemic exacerbating structural constraints such as inadequate and unreliable electricity supply. The MTBPS once again outlines that electricity supply constraints “are a drag on growth” and “will continue to limit the speed and durability of the recovery and long-term growth.”3 Global factors, such as monetary policy changes from the major central banks due to changes in inflation outlook, will add uncertainty to South Africa’s recovery.

Consequently, the National Treasury expects the economy to grow by an average of only 1.7% per annum over the next three years, with the weaker growth outlook reflecting South Africa’s pre-pandemic struggles with structural weaknesses.4

Of further concern in the immediate term is the rising inflationary pressure expected both globally and locally, which is likely to erode consumer pockets. Deloitte’s research, released in October 2021, showed that South African consumers – despite feeling safer and optimistic that their financial position will improve over the next three years – are particularly concerned about price rise in everyday purchases, making upcoming payments, and about the amount of money saved.5

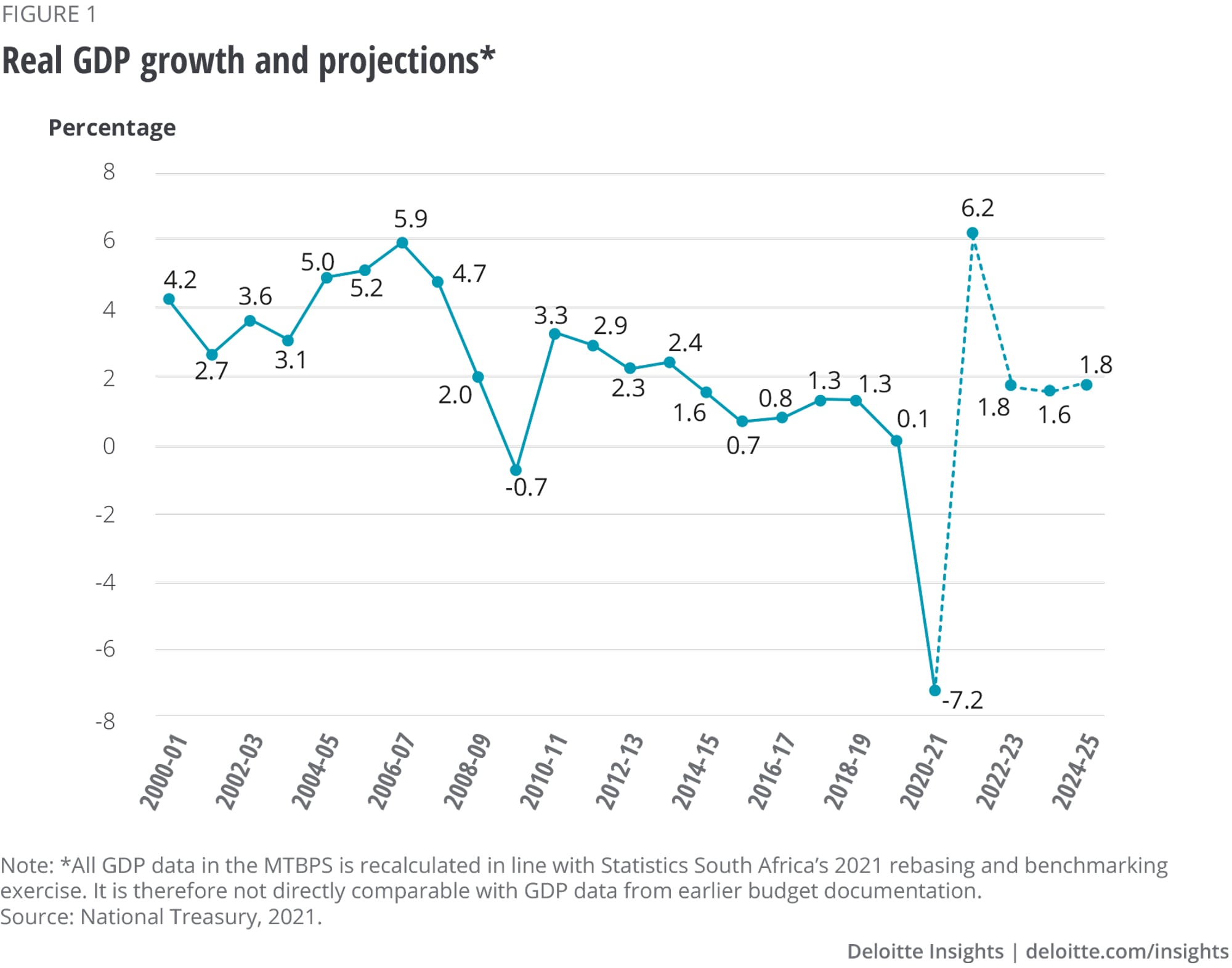

On a more positive note, Godongwana revised up the government’s revenue expectations for the 2021–22 fiscal year to 1.5 trillion rand, compared to 1.4 trillion rand during the 2021 Budget in February. The upward revisions were largely because of unexpected mining tax windfalls due to higher commodity prices. As a result, the budget deficit is expected to be 7.8% of GDP in 2021–22, with further consolidation efforts to see the deficit narrow to 4.9% by 2024–25.6

It is important that government begins to look ahead and beyond the response to the COVID-19 pandemic. Keeping in mind that fiscal consolidation and stabilising debt levels will remain a priority over the medium term, the government will face growing pressure to refocus on the vast levels of poverty and inequality prevalent across the country.

Consequently, the conversation has recently turned (again) toward the implementation of a Basic Income Grant (BIG). The grant, at its most base level, is meant to place all South Africans above the poverty line. However, this would come at a considerable cost and place the fiscus under immense pressure at a time of fiscal consolidation. Indeed, Godongwana provided scant details on any momentum regarding the implementation of a BIG, stating that the decision is to be made by the cabinet and will be addressed in the 2022 Budget speech.

The other initiative that has largely fallen by the wayside in the wake of the pandemic is the implementation of National Health Insurance (NHI). The NHI bill was introduced to the South African National Assembly on August 8, 2019. While much uncertainty remained in the wake of the bill, it did create a road map on the operational processes and structure of NHI, thereby moving it into the realm of possibility.7 However, the pandemic forced the government to sharply prioritise, and rightly so, its finances and efforts.

Since the Supplementary Budget of 2020, the government has been forced to make reprioritisations – stemming from the deteriorating fiscal position – across a number of health spending areas to fund the COVID-19 response. Between MTBPS 2020 and MTBPS 2021, planned growth in health spending fell broadly from 2.9% average annual growth over the next three years, to a -0.6% average annual contraction.8

Despite the focus on the COVID-19 response, the lack of effective data and systems exposed failings in both the public and private health sectors, highlighting the need for an effective and consolidated national health system. The current crisis, however, means that the priorities and timing of the NHI roll-out are likely to shift compared to the pre–COVID-19 expectations.9

While the government continues to promote that NHI remains a key policy priority, it will require a significant increase in spending over the medium term to ensure it is successfully rolled out without damaging the quality of health care. The MTBPS is focussed on damage control over the pandemic’s knock-on effects on the health system, with spending set to remain concentrated on combatting the continued effects of the COVID-19 pandemic, expanding vaccine roll-out, and providing socioeconomic support measures to the affected population.

Given that South Africa, along with the rest of the world, will likely need to deal with renewed COVID-19 challenges and additional infection waves in the foreseeable future, initiatives from the private sector will become increasingly important to address structural inequalities.

Indeed, the government’s investment drive on infrastructure development relies heavily on sourcing private sector investment. As seen over the last year, the health of the economy, as a whole, is closely linked to the ability of the health care system to respond to an influx of infected patients. To supplement the government’s capacity constraints, the private sector is increasingly engaging in strategic partnerships with government and health care organisations to advance health care equity in South Africa and the rest of the continent.10

While South Africa’s medium-term economic outlook has improved slightly in 2021, primarily due to improving global conditions, its economic health is still in fragile territory. Structural constraints, lack of investor confidence, and continuing fallout from the pandemic on jobs and investment will undoubtedly have long-term adverse consequences on the economy and people’s livelihoods. Now, more than ever before, there is a responsibility on the private sector to support the government’s efforts to grow the economy and alleviate poverty and inequality.

Cover image by: Jamie Austin