Eurozone has been saved

Cover image by: Jamie Austin

The Eurozone saw an acceleration in economic growth in the second quarter, driven by private consumption. However, business activity grew at a markedly reduced rate in September. This partly reflects the peaking of demand in the second quarter, but also indicates supply chain bottlenecks. The latter, along with rising inflation, challenged the pace of economic recovery in the region.

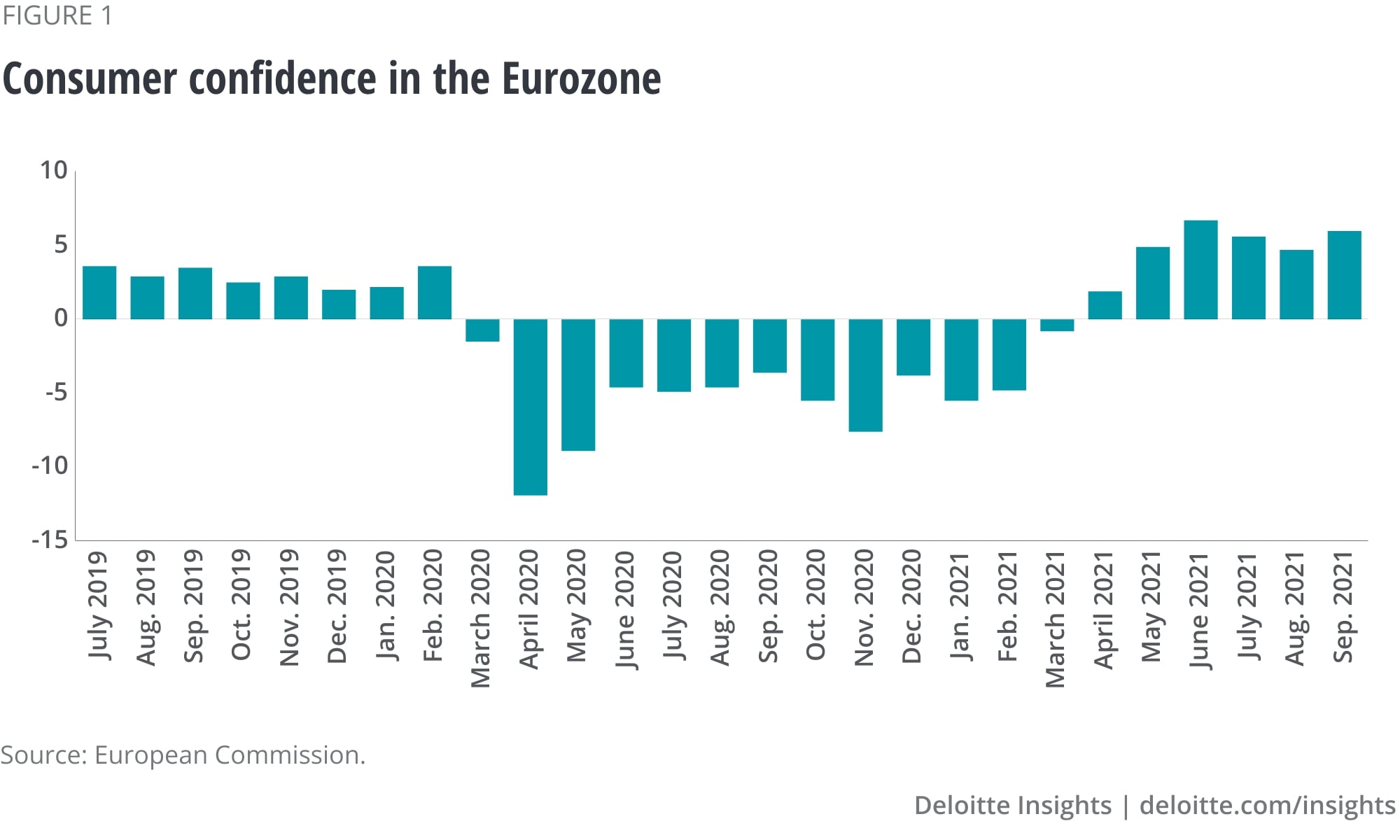

In the second quarter of 2021, seasonally adjusted GDP in the euro area increased by 2.2% compared to the previous quarter, suggesting that the Eurozone continues its solid recovery from last year’s deep recession. The key driver of the recovery has been private consumption.1 This indicates two factors: First, there is strong pent-up demand for goods and services that have been inaccessible during the lockdowns. Second, households in the Eurozone collectively accumulated around 480 billion euros of excess savings according to Deloitte estimates, a consequence of the stable labor markets during the crisis and constrained consumption possibilities.2 Of course, consumers will not spend these enormous savings at once, but disburse them gradually, supporting private consumption in the medium term. Consumer sentiment in the Eurozone reached positive territory after the end of the lockdowns in the second quarter and peaked over summer (figure 1). Moreover, consumer sentiment appears to be well-supported by labor market developments. In September, the unemployment rate continued to decline to 7.5% from a peak of 8.6% in August 2020. Rising vacancy rates suggest that this trend will continue.3

Corporate investments also show a positive trend, even though this is not yet visible in hard data due to time lags in measurement. But recent sentiment indicators show that investment propensity is on the rise. According to the Deloitte German CFO Autumn Survey, German corporates have the second-highest willingness to invest since the start of the survey in 2012. Capacity constraints, resulting from lower investments last year and the surprisingly strong recovery in demand, are important driving factors behind the rising investment intentions.4

Despite the positive news around private consumption and corporate investments, economic sentiment in the Eurozone is on the decline. The Purchasing Managers’ Index peaked in summer and has been declining since then (figure 2). The composite index marked a five-month low and the manufacturing index a seven-month-low in August (figure 2).

A major contributor to the declining economic sentiment is shortages in materials and upstream products. A combination of rapidly rising demand and reduced production capacities during the pandemic has led to serious shortages that are increasingly holding back industrial production.5 In surveys among German companies, over 70% report that supply shortages hamper their production. In the automotive industry, over 90% suffer from these shortages; in the engineering sector, it is over 80%. This is a historical high. Over the last three decades, the corresponding values never amounted to more than 20%.6 In this sense, interrupted supply chains pose a threat to recovery at a time when industrial orders have surged.

Supply chain shortages, alongside rising commodity prices, shipping costs, and baseline effects due to low economic activity and partly negative inflation rates last year, are also partly responsible for rising inflation risks.7 The inflation rate in the Eurozone stood at 3.4% in September, the highest in the last 13 years. Inflation in Germany jumped to 4.1%—the fastest pace of consumer price increases in nearly three decades—while inflation in Spain reached 4.0%, in Italy 3.0%, and in France 2.7%.8 The prices of energy, groceries, and industrial goods rose the fastest. The core inflation rate on the other hand, excluding energy and food, rose only to 1.9%.

Whether rising inflation pressures translate into inflation will depend on several factors. First, how long will it take until supply chains work smoothly again? Second, will energy prices continue to rise? Third, to what degree will producers roll over input price increases to consumers? Fourth, how are commodity prices and shipping costs likely to develop? According to the Organisation for Economic Co-operation and Development (OECD), the last factor (commodity prices and shipping costs) is responsible for three quarters of inflation rate increases in the G20 consumer price index since the second half of 2020.9

The Eurozone’s economic performance will largely hinge on the development of supply chain shortages and inflation. A negative scenario would include higher inflation and reduced growth rates, which would mean stagflation, the combination of stagnation and inflation. A positive scenario would develop if inflation proves to be transitory and supply chains recover quickly. In that case, the recovery would stay on track and the Eurozone would see a continuation of the solid rebound that has been ongoing since late spring. While the development of inflation should not be underestimated, a continuing recovery remains our baseline scenario, in which we estimate the Eurozone will grow by 5.1% in 2021 and 4.4% in 2022.

{kind=link}

{kind=link}