Global economic outlook, January 2024

Nations will still face inflation, labor shortages, debts, and geopolitical tensions in 2024. Even so, economic conditions are improving, creating opportunities for stronger growth.

Introduction

One year ago, we introduced our first annual global economic outlook, written by our economists from around the world. In my introduction to that report, I raised questions about the outlook for 2023 regarding inflation, recession, supply chains, and labor markets. We now know what happened in 2023. Inflation receded significantly in most major economies, recession was mostly avoided, supply chain disruption eased considerably, and labor markets remained historically tight.

Now, as we head into 2024, major central banks appear on the verge of loosening monetary policy, confident that inflation is largely beaten.1 Although the global economy has slowed, the outlook is somewhat more benign than anticipated. But new problems emerged over the past year. The Russia-Ukraine conflict continues, there is a new war and crisis in the Middle East, tensions between the world’s two largest economies remain significant, and patterns of trade and cross-border investment are shifting.

In the following sections, economists from 21 of Deloitte’s member firms offer their views on their respective countries’ outlook for the year. Our hope is that readers will find these outlooks to be interesting, insightful, and helpful. Your feedback is most welcome, and our economists are available for more in-depth discussion about these issues.

Best regards,

Ira Kalish

The Americas

The United States

Daniel Bachman

“Out of this nettle, danger, we pluck this flower, safety.”

—Henry Hotspur in William Shakespeare’s Henry IV, Part 1 (Act II, Scene iii)2

US economic policymakers might well be feeling like they have managed to follow Hotspur’s advice. The US economy seems to have avoided the pain of a recession while enjoying a pretty significant fall in inflation.3 That’s a good outcome under any circumstances, but it looks even better in light of everything that’s been going on over the past couple of years. The labor market has remained tight, but there is little sign of a wage-price spiral getting out of control. Geopolitical tensions are rising, growth in key US economic partners is slowing, and Congress has added budget-funding volatility into the mix. But somehow, none of these have drawn enough blood (yet) to prevent more job growth in the United States, a rise in real wages, and a growing economy.

The current state of the economy has created questions about some of the standard paradigms economists use to explain inflation and labor markets.4 But the final scene of this play is still to come, and the immediate risks to the economy remain relatively high.

Deloitte’s baseline forecast continues to be optimistic. But while October and November data support this view, several factors could derail US economic growth in the next year.

- Inflation is falling, but it’s not completely back to target levels. Although Fed officials are beginning to discuss rate reductions, if inflation remains above target, they might tighten monetary policy further.5

- Long-term interest rates have only recently risen above their prepandemic levels—this delayed reaction means that part of the impact of the Fed’s previous tightening efforts remains to be seen.

- The US budget process still poses some risk to economic growth. The differing objectives and lack of will to negotiate these differences among key members of Congress suggest that a partial or even full government shutdown remains a possibility.

- Geopolitics continues to create new challenges for US policymakers. US allies are asking the country to provide weapons, ammunition, and financing, which will further challenge the budget process.6 Supply shocks—particularly oil price–related—might also derail the US economy.

Even if the US economy continues to shrug off these risks, there are other longer-term challenges:

- Climate change poses a large challenge for the US economy because immediate costs are growing, and the need to invest in mitigation efforts is becoming more critical.7

- US population growth is slowing. While US demographics are better than that of many other developed countries, the country will need to continue to adjust to slow labor force growth,8 tighter labor markets, and the need to pay for the care of an aging population.

- The current US budget trajectory is unsustainable (which is, of course, related to the need to pay for the health care of an aging population).9

- The most important question for the future of the US economy is whether trend productivity growth can be achieved fast enough to improve the standard of living. Before the pandemic, productivity growth was disappointing. If productivity growth picks up, many of the country’s other problems will likely become easier to solve.

The Deloitte forecast is optimistic that the US economy can overcome these challenges. Our baseline shows inflation falling, unemployment staying low, and productivity growth picking up. But the truth is that, like Shakespeare’s Hotspur, we haven’t actually picked the flower. In the play, Hotspur’s speech doesn’t reflect what will happen to him—he meets a bloody end at the hands of the future King Henry V. US policymakers are justly concerned that what looks like success could turn into failure soon. With so many potential challenges, nobody should take US economic growth for granted.

Canada

Dawn Desjardins

Canada’s growth outlook for 2024 is poised to be the mirror image of 2023, with a very slow start followed by stronger gains in the second half of the year. Interest rate cuts rather than increases will be the theme in 2024, not just in Canada but across many of its trading partners as well. And interest rate relief will be needed if the anticipated recovery is to materialize in the second half of the year.

There’s every reason to believe that the aforementioned scenario will be the case. As inflation pressures continue to ease,10 we project that the 2% target will be in the Bank of Canada’s sights by mid-2024. The steady deterioration in household and business confidence reflects worries about the impact of higher rates on their financial condition and will continue to constrain spending in the first half of the year. About one-third of Canadian households have a mortgage, and the Bank of Canada’s analysis showed that almost half of mortgages will have renewed at higher rates by the end of 2023, climbing to two-thirds by the end of 2024.11 Our forecast calls for the peak level of interest payments as a share of disposable income to occur early in 2024. Declines in the ratio thereafter will be slow. Surveys of business sentiment similarly point to elevated costs of financing and rising wages as major concerns.

In 2023, wage gains outpaced inflation providing welcome relief for households while creating challenges for businesses. So far, companies have refrained from cutting their labor force but have pulled back on the number of vacant positions. Employment growth has slowed, and we expect this to persist in 2024 as employers manage softer sales growth and higher costs. With population growth continuing to outpace job gains, the unemployment rate will rise further in 2024.

Against this backdrop, 2024 may be an opportune time for businesses to invest in automating processes and integrating artificial intelligence. Canadian labor productivity has fallen for six consecutive quarters and the gap between Canada and the United States has widened. A recent study by C.D. Howe Institute12 showed that for each dollar a US company invests in its workers, its Canadian counterpart spends 58 cents. Investment spending is running 2% below pre-pandemic levels, although—encouragingly—business investment in research and development and software has been running higher post pandemic.

Investment in housing is projected to pick up in 2024. Canada’s rapid population growth shone a spotlight on the limited availability of housing in many of Canada’s largest cities. Governments are now focused on increasing housing supply despite elevated costs and labor shortages creating challenges. The federal government announced several policies aimed at reducing costs and opening up funding channels for builders.13 The housing supply shortage is exerting upward pressure on rents, which rose 7.4% in November from a year earlier—near the fastest pace of increase since 1982. Home sales activity conversely slowed as high interest rates and eroding affordability saw buyers pull back. Given supply concerns, however, we expect that further price declines will be limited with buyers expected to return to the market once interest rates begin to decline.

As the global economy absorbs the impact of higher interest rates and central banks pivot to an easier policy stance, demand for Canada’s exports is expected to recover in the second half of the year after a soft start. With the Bank of Canada likely to ease policy ahead of the Fed in 2024, Canada’s dollar is expected to trend weaker early in the year limiting the weakening of exports.

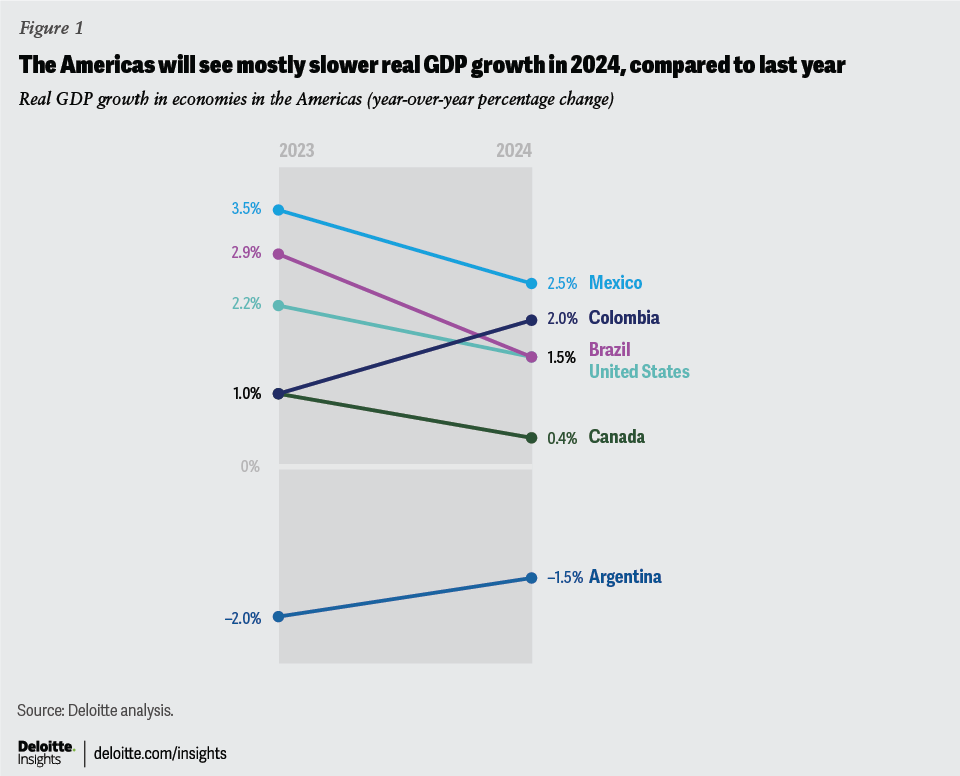

Mexico

Daniel Zaga

Mexico’s economy grew approximately 3.5% in 2023.14 This performance can be explained by four factors. First, the stronger-than-expected US economy, which helped the nation through trade and remittances; second, the resilience of private consumption, thanks to increases in real wages and a strong labor market; third, gains due to nearshoring,15 observable through the recovery of business confidence and private investment; and fourth, big infrastructure projects (a new refinery, trains, airports, and others), now clearly seen in government expenditure and construction.

For 2024, we expect the economy to maintain its performance in the first half of the year, but growth will likely slow in the second half once the elections are over and a weaker global economy begins to weigh on exports. We anticipate private consumption to remain on track, thanks to the large disbursements approved in social spending ahead of the presidential elections in June. Additionally, strong job creation (1 million jobs created so far in 2023) and multiyear records in real wages—which have grown more than 200% since 2018—will keep consumer spending strong, though at the cost of generating inflationary pressures. Also, we expect manufacturing activity and fixed investment to continue reaping the benefits of nearshoring.

Gradual moderation in economic activity and improving supply conditions in 2024 should result in inflation easing from 4.4% to 4%. However, an overheating economy would prevent the central bank from easing policy aggressively. We currently expect cuts of 175 basis points, which would bring the policy rate to 9.5% by year-end 2024. The position of the Federal Reserve will determine if the Central Bank of Mexico (Banxico) has some leeway to cut deeper; but, in our view, current conditions suggest the bank will remain cautious throughout the year, given sticky core inflation and the upcoming elections in Mexico and the United States. The Mexican peso—with regard to the US dollar—is expected to depreciate from 17.7 to 18.8 by year-end 2024, as Banxico starts to cut its reference rate, and presidential elections take place.

The government plans to loosen its purse strings as it ramps up spending ahead of the 2024 presidential elections.16 It expects a primary deficit, which excludes interest payments, equivalent to 1.2% of GDP, and an overall fiscal deficit equivalent to 4.9% of GDP—both the largest since 1990. Public debt as a percentage of GDP should rise from 46.5% in 2023 to 48.8% in 2024—the second largest jump in the last eight years—(although it remains much lower than the Latin American average of 68% in 2022). In our view, the debt-to-GDP ratio is consistent with no immediate credit rating downgrade, but it will force the next government to present an austere budget for 2025.

Federal elections will take place on June 2 with a full restructuring in Congress, plus nine state elections, and the presidential contest.17 This is the first time that both the incumbent party (National Regeneration Movement [Morena]) and the opposition coalition (Broad Front for Mexico [FAM]) have presented women candidates for presidency. Now, all eyes are on how the new administration will manage public finances, investment, and public spending, as well as on how policies take full advantage of nearshoring opportunities. The more pressing challenges are energy availability, water and natural gas shortages, human capital, and infrastructure investment, as well as improvements in security and the rule of law.

Colombia

Daniel Zaga and Alejandro Mina

After expanding at a 7.3% rate in 2022,18 Colombia’s economy came to a halt in 2023, with real GDP growth not exceeding 1%—lower than initially expected. For 2024, this figure should be slightly higher, buoyed by a rebound in consumption. Two main questions dominate the outlook: first, will investment pick up? And second, can the current government push its economic agenda in Congress?

The most concerning economic fact of 2023 was the state of investment. This was most challenging in infrastructure construction, which fell 40% below prepandemic levels. Additionally, public spending was very slow during 2023. This year, all eyes will be on how the government will counteract its low spending level and whether it can get a countercyclical infrastructure program rolling. Another critical area will be investment in the oil and coal sectors. The ruling government has expressed its intention to substantially reduce the production of both, mainly to combat climate change. To that end, it included a provision on a tax bill aimed at discouraging the production of nonrenewable resources.19 However, with the Constitutional Court overruling that provision, it will be interesting to see if the oil and coal companies’ reaction includes further investments in the sector.

The left wing government of President Gustavo Petro has an ambitious set of structural reforms that include a health care reform bill, a pension bill, and a labor bill. Each could impact the economy in several ways. The health bill aims to create a single payer system like the one prevalent in the United Kingdom. The pension bill looks to transfer a large share of pension savings from private funds to the public pot. Finally, the labor bill has the intention of formalizing the labor market but could make hiring and dismissal more expensive for companies. In the second half of 2022, the government enjoyed majorities in both chambers of Congress and was able to swiftly pass a tax bill.

However, currently, the situation is quite different because political infighting within the coalition has eroded the government majority20 and it looks unlikely that reforms will be passed smoothly. International markets have discounted this possibility, and 10-year bonds are trading at their highest since President Petro took office.

Hence, our economic outlook anticipates the Colombian economy to grow 2% in 2024. Once again—as it has happened post pandemic—private consumption is expected to be the main driver of growth on the back of lower inflation and lower interest rates. It is unclear whether investment will rebound. This is crucial because, if it does not, it could undermine potential growth in the medium and long term. Government spending should pick up a little but will still lag historical averages. As for the economic reforms, we don’t expect much to change. The government has lost its grip on Congress, and even if bills were approved, they are unlikely to pass muster with the Constitutional Court.

Brazil

Daniel Zaga, Frederico Di Yenno, and Juan Ignacio Lacapmesure

Over 2023, the Brazilian economy outperformed initial projections, with GDP growth of 2.8%.21 This was driven by a dynamic agricultural sector, achieving a 14% growth rate due to record soy and corn harvests. The services sector—particularly financial, real estate, information, and communication—also contributed significantly, while manufacturing displayed a comparatively less impressive performance. A key factor in Brazil’s economic growth has been the remarkable recovery of the labor market, showing resilience since 2022. Unemployment dropped more than 7 percentage points by the end of 2023 to 7.7% of the active population, reaching the lowest level since 2015.

External factors—such as a record trade surplus—have had a positive impact on the economy, associated with a substantial reduction in imports, especially of products like fuel oil and chemical fertilizers. Inflation continued its downward trend—expected to end the year at 4.6%—well within the central bank's target range. This has allowed for the initiation of a gradual interest rate–reduction cycle, making the Brazilian Central Bank one of the first Latin American central banks to do so in the current cycle. Reforms implemented in recent years, including pension, labor, and administrative reforms, higher central bank autonomy, slightly higher trade openings, a new fiscal framework, and a recently approved tax reform, contributed to Brazil’s economic performance exceeding expectations.

Looking ahead to 2024, the scenario for Brazil will likely be challenging, however. We expect the economy to continue to grow, albeit at a slower pace of 1.5%. The agricultural sector is expected to have good outputs—but lower than the numbers seen in 2023—considering the climatic effects of droughts in the northern and northeastern regions and above-average rainfall in the south. Economic expansion will be less dependent on agribusiness and better distributed across sectors. The labor market is anticipated to continue growing, maintaining high wage levels and supporting private consumption. Inflation is projected to further decelerate to 3.9% during the year. With lower inflationary pressures, it is expected that the central bank will have more room to continue easing monetary policy, creating better conditions for private credit acquisition.

Nevertheless, there are certain crucial risk factors to consider in the growth prospects of the Brazilian economy. First and foremost, attention must be given to public debt and government spending. The growth rate of Brazil’s gross public debt in 2023 may pose some concerns. In 2022, the gross debt of the public administration closed at 72.9% of GDP, while it is expected to reach around 76% by the end of 2023. Furthermore, the primary fiscal result for 2023 is expected to be 2.4 percentage points lower than that of 2022, stemming from a significant increase in public spending. There is considerable uncertainty regarding the possibility of achieving the fiscal balance target for 2024, leading to tensions within the national government. It will be crucial for the Brazilian economy to control the level of uncertainty associated with the future evolution of public accounts, thereby contributing to a stable macroeconomic environment.

A second risk involves the slowdown of the global economy, particularly in China, which has become Brazil’s main trading partner with approximately 25% of the overall trade of the Latin American country. A more pronounced deceleration in Chinese economic growth could directly impact both exports and the domestic economy. Another additional risk involves elevated levels of global public and private debt, as well as international conflicts, which could create an uncertain scenario in the global economy for 2024 and a reallocation of capital toward less risky countries.

In summary, Brazil’s economic outlook for 2024 presents opportunities peppered with risks, mainly related to the credibility of the tax reform, the evolution of fiscal measures, and the effects of the global economy.

Argentina

Daniel Zaga, Frederico Di Yenno, and Juan Ignacio Lacapmesure

The Argentine economy is anticipated to experience a contraction of 2.0% in 2023, primarily due to a severe drought affecting the agricultural sector and uncertainties surrounding post–presidential election economic plans. For 2024, further GDP reduction of up to 1.5% of GDP is expected, driven by cuts in government expenses and adjustments in macroeconomic variables.

The 2023 presidential election marked a significant shift in Argentina—with Javier Milei as president—signifying a radical change in Argentine politics.22 His victory triggered market optimism, anticipating transformative economic changes. Milei, representing the libertarian party Libertad Avanza, advocates for limited government intervention and proposes radical economic reforms, including tariff updates, government spending cuts, and privatization of state-owned enterprises.

Although Milei proposed dollarizing Argentina’s economy, there are challenges to implementation arising from short-term debt-amortization burdens. The government’s initial focus is on tackling inflation and macroeconomic issues by reducing government expenses, addressing the central bank’s passive stance, and eliminating foreign exchange controls.

Despite these reforms, GDP is projected to decrease by 1.5% in 2024, with improved climatic conditions benefiting the agriculture sector and sustained production in the energy sector. However, high inflation, which exceeded 200% in 2023,23 poses a significant challenge that is likely to persist in the short term.

In 2024, a trade surplus of US$19.6 billion is anticipated due to increased grain production and momentum in the oil and fuel sector. Net agricultural exports are expected to rise by US$13 billion. Imports will decrease due to a higher real exchange rate, GDP decline, lower freight prices, and increased energy production in the country. The trade surplus would cover a significant portion of the interest and capital payments in 2024. However, access to the credit market would be needed, as this foreign exchange balance does not account for “additional financing needs.”

These additional financing needs involve payments due to an adverse result against Argentina in the national oil company trial (YPF), the commercial debt of importers, the currency swap with China, and undistributed dividends to parent companies between 2020 and 2023.24 We estimate that the entire first tranche of the China swap—amounting to US$5 billion—has been utilized. The government would attempt to avoid its decrease to circumvent the need for additional financing. If the second tranche is not renewed, it cannot be used to continue supporting imports. On the other hand, the interest-bearing liabilities of the central bank could be absorbed by the public sector, which aims to extend their maturity.

All this liability—exchanged for state debt—will increase the country’s debt-to-GDP ratio—constituting the main risk of the plan. Considering this, the foreign exchange control is unlikely to be lifted early and entirely. The parallel exchange rate and the ability to refinance debt maturities will depend on the adjustment of the fiscal deficit from 2024 to 2025.

In the third quarter of 2023, GDP fell by 0.8% annually but increased by 2.7% compared to the previous quarter. The decline in manufacturing production and the fall in real wages will exert pressure on economic activity. On the other hand, by the end of 2023, it is expected that the increase in electoral spending, improvement in the fine harvest, sowing activities for the new campaign, fossil-fuel production, and increased consumer confidence will provide an additional boost to economic activity.

Except for electoral spending and consumer confidence, these growth factors are expected to continue in 2024. The recovery of the agricultural sector’s GDP by 28% would hit in the second quarter of 2024, adding 1.5% growth to GDP. The fossil fuel sector is expected to grow by 6%, contributing 0.6% to growth.

On the other hand, the main factor determining economic activity and the stability of the exchange and monetary markets will be the government’s spending level. Based on the data provided by the government, the adjustment of current spending at various government levels would equate to a real 6% decline in one year. This would have a negative impact of 1.2% on GDP.

Argentina has great potential in the provision of energy resources, minerals, agricultural products, and various services. In the coming years, this potential could be exploited through the implementation of macroprudential measures within a framework of more institutional stability. The expectation is that, by adhering to fiscal, regulatory, and monetary rules, the country can address issues such as inflation and credit rationing.

Several sectors with high growth potential demand reforms for expansion. Unlocking the potential of these sectors to boost employment and exports requires the removal of export taxes affecting the production of tradable goods and services. Additionally, simplifying and reducing taxes would stimulate investment, facilitating increased productivity and laying the groundwork for long-term sustainable growth.

Europe

Eurozone

Pauliina Sandqvist

The eurozone experienced significant economic stagnation over 2023,25 although it proved more resilient than previously anticipated. The year started better than expected since the energy crisis turned out to be less dramatic than feared, but the eurozone economy overall worked in low gear over the course of the year. High inflation and interest rates weighed on private consumption as well as corporate investment. The construction sector cooled down noticeably, and the manufacturing sector struggled due to lower (foreign) demand and high (energy) costs. On the other hand, most service sectors did better. All in all, economic activity remained sluggish, although there were cross-country differences, with economies more orientated to services and less exposed to Russia faring better.

The economic outlook for 2024 looks sedate. The good news is that inflation—and in particular, core inflation—slowed more than expected, energy-related risks seem to be less pronounced than a year ago, and labor markets are still quite robust. The latest Deloitte European CFO Survey26 showed that hiring expectations in the euro area have softened but the net balance is still slightly positive indicating a minor expansion over the coming year.

There are several reasons for prudence. Real income increases are still smallish, consumers are keeping their purse strings tight, and savings have been rising, motivated by the higher interest rates. Restrictive monetary policy will likely keep restraining economic activity at least until rate cuts start (our assumption is that this is unlikely to happen before the middle of this year). This is the case for many other geographies, meaning that foreign demand is also likely to remain subdued. The existing geopolitical tensions and numerous elections to come keep uncertainty elevated—influencing consumption and investment decisions and keeping energy price developments skittish. Additionally, fiscal consolidation is set to start, as most eurozone countries must tighten their public spending.

Altogether, economic activity should remain relatively weak at the beginning of 2024 and gradually pick up over the course of the year, as inflation comes down and tight monetary policy starts to ease. Private consumption will likely be supported by still robust labor markets, increasing real incomes, and lower saving rates as interest rates come down. Also, NextGen EU funds should underpin investment moderately. Export activity is expected to recover modestly as world trade growth is expected to rebound in 2024 to 2.7% from 1.1% in 2023.27

There are some upside risks as well. If inflation keeps easing—as it has during the past few months—real incomes could increase more quickly than expected and support private consumption. The European Central Bank could start with the rate cuts somewhat earlier, boosting aggregate demand even more. Hence, the pace of inflation reduction is key for the eurozone’s economic outlook for 2024. Furthermore, traction in the deployment of NextGen EU funds could provide an additional boost to growth across major recipient EU economies.

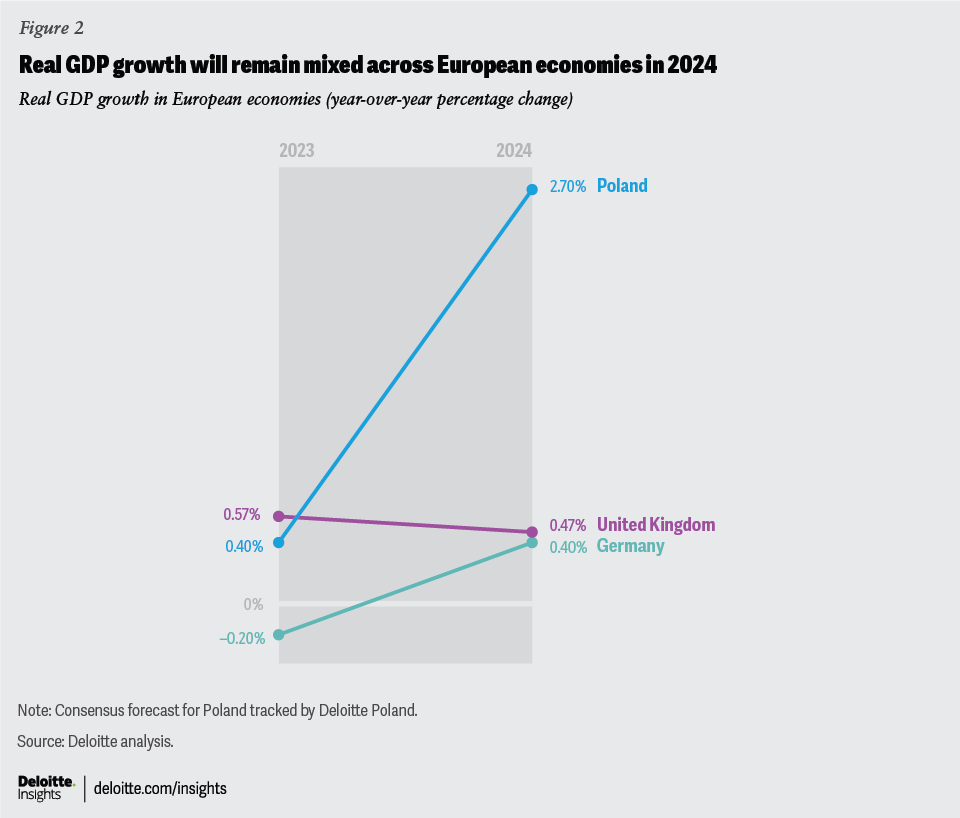

Germany

Alexander Börsch

The German economy had a difficult 2023, with two very different halves. The first half turned out to be better than expected. Despite the halting of Russian gas deliveries, there was no serious energy shortage in winter 2022 and early 2023, which could have pushed the economy into a deep recession. At the same time, the opening of China as well as the resilient US economy, nourished hopes for Germany’s export-oriented sectors.

However, in the second half, inflation turned out to be considerably more stubborn than expected, so the interest rate cycle became very steep. Restrictive monetary policy had the desired effects on inflation—in Germany, inflation fell from 8.7% in January to 3.2% in November 2023.

These headwinds resulted in a small contraction of the German economy (–0.3%) in 2023. The industrial sector had to confront a recession with falling industrial production, while the services sector held up much better. This was due to a considerable amount of extra savings and pent-up demand from the pandemic, but also due to a very stable labor market. At the end of 2023, it seemed that the economic downturn was slowing. One of the key early indicators, the purchasing managers’ index, is still at a low level and in contractionary territory, but it stabilized and showed a slight uptick in November.

Looking at 2024, several of last year’s constraining factors are expected to continue to shape Germany’s economic performance. There will not be much tailwind from foreign demand, as Germany’s two most important export markets—China and the United States—are facing declining growth rates in 2024. At the same time, high interest rates are a drag on corporate investment. This implies that any economic recovery will depend mainly on consumer expenditure.

At first glance, consumers are an unlikely candidate to drive growth in 2024, as inflation has pushed consumer sentiment into strongly negative territory. However, on the positive side, labor markets continue to be very stable. According to the Deloitte CFO Survey,28 labor shortages are the no. 1 risk for large German corporates in 2024. Demographic change and a declining labor force play a key role in this respect. Due to tight labor markets and good job prospects even in a recessionary environment, consumers do not necessarily curtail their consumption. Even more important, inflation is likely to decline further, and the first interest rate cuts are likely to happen later in the year. Lower inflation means higher real incomes and higher consumption. Therefore, Germany’s economic performance in 2024 will depend to a large degree on these questions—how fast inflation will decline further and when the European Central Bank will start cutting policy rates.

Deloitte’s economic research assumes in its baseline forecast for the German economy that it will experience growth in 2024, but at a very moderate pace of 0.4%. The key assumption behind this forecast is gradually declining inflation and a first interest rate cut early in the third quarter. If inflation falls faster, a growth rate of 0.9% is possible; if it falls slower, the German economy faces a repetition of 2023 characterized by light recession (–0.1%). In the baseline scenario, we forecast inflation at 2.7% over the year. The first quarter of 2024 is likely to be the weakest, with the economy stabilizing and picking up pace in the second quarter and onward.

In all, 2024 will be a transition year for the German economy. As a very export-oriented economy with a strong industrial base, it has been particularly affected by the multiple supply shocks over the past years, ranging from the COVID-19 pandemic to interrupted supply chains and from the energy crisis to new geopolitical risks. In this new context, the German economy has not returned to its growth trajectory of the pre–COVID-19 era and 2024 will indicate whether it can do so in the medium term.

France

Maxime Bouter, Olivier Sautel, and Pauliina Sandqvist

The French economy had a challenging 2023. Next to high inflation and financing costs, social tensions related to the unpopular pension reform depressed confidence in the first months of the year. The pension reform, which raised the state pension age from 62 to 64 starting September 2023, was passed in April after a long and controversial process.29 Besides that, French economic growth was somewhat stronger than in the eurozone on average—supported by a flourishing tourism sector. Yet, the growth momentum did weaken in the second half of the year due to a worsening trade balance and a contracting construction sector.

Sentiment indicators remained depressed at the end of the year. The labor market remains strong, with the unemployment rate close to the historical low. Less dependent on oil and gas than other European countries, and thanks to public subsidies for energy measures, France was less severely affected by the consequences of the war in Ukraine and the post–COVID-19 global fossil fuel supply shock. This has resulted in lower inflation than the European average. Inflation peaked in 2023 but is falling more slowly than in other European countries due to a relatively lower price level. In the absence of a major external shock, all inflation drivers are expected to slow down (stabilization of energy, retail, and manufactured goods prices, but also a moderate fall in employment) so that headline and core inflation should continue to fall gently over the coming quarters.

The outlook for 2024 is subdued for France. The political situation in the country is likely to remain challenging given Macron’s lack of a majority in parliament, which complicates the implementation of further reforms. Fiscal stimulus will probably turn out to be less expansionary compared to 2023, as most of the high inflation– and energy-related measures run out during 2024. The end of the energy-related measures should reduce pressure on the government’s primary deficit. On the other hand, interest payments on public debt are expected to surge as new issuance will carry higher rates than those maturing. The much-needed fiscal consolidation is set to start and will remain relevant in the coming years, as the debt-to-GDP ratio of about 110% is far above the European Union’s debt rule of 60%.30 With a relatively low GDP growth rate and in the absence of any major reforms, the public deficit is unlikely to fall significantly. As a result, France’s debt ratio should remain higher than the euro area average.

Despite these challenges, economic activity should pick up gradually over the year in line with easing inflation, less tight monetary policy, and slowly strengthening foreign demand. Moderate growth will be supported mainly by private consumption. Despite a slowdown in nominal wage growth, the fall in inflation should allow households to see their purchasing power increase. Households could also see their disposable income increase as a result of tax relief, with the abolition of the housing tax for the last segment of the population who, unlike the rest of the population, were still subject to this tax in 2023.

Despite particularly resilient business investments, their contributions to growth are likely to be moderate as high interest rates take their toll. The NextGen EU funds should foster public investment, making investment in climate and energy transition an important driver of growth. On the other hand, it is unclear how the pension reform will affect the labor market. It will cause an increase in the labor supply, but this can either be absorbed and ease labor shortages in specific sectors, or it could lead to slightly higher unemployment. A bright spot for the French economy is the Olympic Games in Paris in August 2024, which are expected to boost domestic demand, especially in the tourism sector.

Spain

Ana Aguilar

The Spanish economy has shown resilience to recent headwinds, outperforming expectations and European growth in 2023. In 2024, Spain is expected to continue to grow above the European average,31 although at a lower rate than in 2023,32 as a result of the higher interest rate environment progressively feeding through to the economy, and a more muted external sector. Spain has benefited from the global trend of greater resilience of services vis-a-vis manufacturing, with services-related purchasing managers’ indices remaining in expansionary territory at the end of 2023. In contrast, the manufacturing PMIs anticipate ongoing contraction—though comparatively less pronounced than the eurozone.

Consumer spending is expected to be the main driver of growth in 2024. The labor market should continue to grow, albeit less than last year. The unemployment rate will inch lower, although it will remain markedly above the EU average. Wages are expected to continue to rise, following an agreement between businesses and labor union representatives last year, that suggested a progressive recovery of household’s purchasing power in the form of a 4% annual wage rise in 2023, and annual wage rises of 3% in 2024 and 2025.33 Meanwhile, inflation is expected to remain stable in 2024. Food prices and core inflation should continue to moderate, while the expiry of some of the anti-inflation measures taken by the Spanish government and the contribution from energy keep some pressure on inflation.

Although higher interest rates progressively feed through to households, repayment is expected to remain within reasonable levels for most households. Spanish households have continued to deleverage—household debt to GDP is at 50%, about 6 percentage points lower than in June 2022, and 35 percentage points lower than its peak during the global financial crisis.34 The Bank of Spain has recently estimated that three in four households that have taken up a new mortgage dedicate less than 30% of their income to servicing mortgage debt.35 Out of new mortgages taken in 2021, 2022, and 2023, about 75% are on fixed rates, protecting those households from sharp volatility in interest rate payments.36

Investment grew in the first part of 2023 but stagnated in the third quarter, as uncertainty continued to influence decision-making. Against the environment of high interest rates, businesses have continued to deleverage. Net business debt to GDP is at 67%, 8 percentage points lower than in June 2022 and 53 percentage points lower than at its global financial crisis peak.37 As the prospect of interest rates starting to moderate takes hold, investment growth is expected to accelerate. This trend should be assisted by the progressive deployment of the NextGen EU funds, which should make loans available to businesses at favorable rates.

The flip side to the strength of households and businesses balance sheets is public finances. Although fiscal deficit and debt-to-GDP ratios have progressively come down from their pandemic peaks, they are still expected to remain elevated.38 The deficit is expected to continue to decrease in 2024, assisted by the partial expiry of anti-inflation support measures. The effects of higher interest rates are only expected to feed through gradually given the extended maturity of Spanish debt. The reinstatement of EU fiscal rules will require Spain to set out a medium-term path of fiscal consolidation.

The external sector stopped being a significant driver of growth in the second half of 2023. The sector is not expected to make a significant contribution to growth in 2024, as a result of subdued growth in the European Union. Nonetheless, tourism has continued on a strong trajectory and could surprise upwards, with tourist arrivals in November 2023 up 10% from November 2019 levels.39 Nontourist services exports are also expected to maintain dynamism, with Spain gaining global market share since 2019.40

Italy

Marco Vulpiani and Claudio Rossetti

After its postpandemic recovery, the Italian economy slowed down last year, recording modest growth rates that characterized the previous decade. Inflation and high interest rates were the main reasons for the weakening of the Italian economy. A significant decline in consumption growth in 2023, after the dynamic postpandemic recovery the year before, also played a role. Unfortunately, these negative effects are not expected to vanish, and the modest real GDP growth rate last year is expected to be repeated in 2024.

Higher interest rates are affecting domestic demand through the credit channel. On the business side, the cost of credit increased sharply last year. The cost of borrowing was, on average, more than twice what it was the year before. In addition, the lending criteria have also been tightened, leading to a significant reduction in the supply of loans available to businesses. Therefore, many businesses had to use up any available excess liquidity over the past year, and gross fixed capital formation recorded a striking negative growth rate.

Moreover, the construction sector will no longer act as a driving force because of the severe reduction in tax credits for housing renovation.41 Further, public investments, especially those related to the National Recovery and Resilience Plan, are expected to slow down in 2024. Gross fixed capital formation should be only partly propped up by the planned rollout of investments, especially in digital and green projects. On the household side, the picture related to the cost of credit is quite similar, with increasing interest rates negatively affecting housing mortgages and consumer credit.

Although core inflation is easing in Italy, internal pressures hampering its descent remain. Increasing labor cost is expected to make a significant contribution in 2024, because of the strengthening of contractual wages after the dramatic inflation seen in recent years. Overall, inflation remained quite high last year in Italy—at around 6.1%—and it is not clear whether the expected reduction in 2024 will be enough to foster stronger economic growth.

Given the downward trend in real income in the last two years and more restrictive financial conditions, consumption was mainly financed by a sharp decrease in savings rates. In 2024, we expect household consumption to benefit from a recovery of purchasing power resulting from higher household income in real terms, due to higher wages and lower inflation. Employment recorded a positive trend in the last year, but higher labor costs could cool labor demand.

Italy’s trade balance has significantly improved in the last year, mainly because of the moderate upward trend in Italian export prices, recovering the significant decline recorded in 2022. Nevertheless, the contribution to GDP growth that comes from international trade is modest and, although it is a source of strength for the Italian economy, it is not expected to provide a strong stimulus to economic growth.

Finally, it is well known that Italy’s economy is geographically divided, with GDP per capita ranging from more than twice the EU average in some regions in the north to about half in many regions in the south. The Italian subsidy known as citizens’ income (Reddito di cittadinanza) provided support for household consumption post pandemic, especially for residents in the south of Italy. Nevertheless, challenges remain. Results from the Deloitte Observatory on Italian regions confirm that a significant gap in productivity and efficiency between different areas of the country remains in most economic sectors. Although some progress has been made, this is also linked to deep institutional and infrastructural differences.

The United Kingdom

Ian Stewart

The United Kingdom’s economic growth slowed over 2023 in the face of rising interest rates, high inflation, and elevated levels of uncertainty. Like most major European economies, the United Kingdom has suffered from the effects of high energy—and particularly gas—prices. While economic growth outperformed depressed expectations and avoided a recession in the first half of 2023, activity contracted marginally in the third quarter. With the effects of high interest rates still feeding through to fixed-rate mortgages and to the corporate sector, and the labor market softening, UK economic activity is likely to, at best, stagnate in the fourth quarter of 2023. For 2023 as a whole, growth stands at around 0.5%, similar to the euro area average but far below previous UK growth trends of around 1.5%.

The good news is the United Kingdom has so far avoided a recession and the sort of deep stress in the financial system that has often followed previous periods of high inflation. While business insolvencies have risen, they have been concentrated in smaller- and medium-sized businesses. Profitability in the dominant service sector has provided resilience, and corporate balance sheets are, by and large, in reasonable shape. Consumer spending has grown modestly in the face of high inflation with consumers drawing down on savings and benefitting from low unemployment and strong wage growth.

Yet the country is not in a trough of the economic cycle. Inflation has peaked, but the backwash from the squeeze on incomes and high interest rates is likely to exert a significant dampening effect on growth in the first half of 2024. Our central case is for activity to reach a trough around the second quarter, with lower inflation and rising real incomes helping drive a gradual pickup in activity in the second half of 2024. This would leave the United Kingdom posting growth of 0.4% for 2024 as a whole, close to the lackluster rate seen in 2023, but with the crucial difference that the pace of growth is picking up.

This sort of outcome would represent a relatively soft landing for an economy that has experienced double-digit inflation, the biggest monetary tightening in 40 years, and a major energy-price shock. Our forecasts are predicated on underlying inflation pressures easing materially and geopolitical risks, and energy prices, remaining contained in 2024. Such outcomes are not assured and as such we think the balance of risk to our 2024 GDP forecast of 0.4% lies on the downside.

The year 2024 could well be one of political change in the United Kingdom. A general election is due by January 28, 2025; but it is far more likely to take place in 2024, probably in the fourth quarter of the year (the timing of general elections is decided by the governing party). Opinion polls currently signal—and have done so for over a year—that the Labour Party is on course to form the next government, supplanting the Conservatives who have governed since 2013.

A change of government would probably make little difference to the medium-term path of UK growth, which will be determined by the global cycle and domestic monetary policy. The Labour Party has committed itself to fiscal rules, which would constrain its capacity to materially raise public expenditure or debt levels. A Labour government would face the same central economic challenge as the current government, namely, how to raise trend productivity growth and similar constraints.

The Nordic countries

Bryan Dufour

The Nordic region is expected to expand modestly in 2024—to the tune of 0.9%. This is driven by disparate situations in different economies, but no country is expected to show negative yearly growth, despite multiple technical recessions observed in the second half of 2023 (in Denmark, Norway, and Sweden). Denmark and Iceland are the two countries expected to expand more than 1%, while other economies will be battling inflation (Norway), a subdued job market (Sweden), and a depressed construction sector (Finland).

The decline of the real estate sector—which is trickling down to the construction industry and its multiple inputs—is, however, a common theme among the Nordic economies. A decrease in central policy rates will be key to remedy this situation and catalyze investment across all sectors. Further rate increases seem unlikely (except perhaps in Norway) as inflationary pressures are easing. Both headline and core inflation are, however, expected to remain above the 2% target, which makes the decrease of central bank rates rather unlikely for the first few months of 2024.

Denmark

Denmark’s 2024 GDP growth is expected to remain within the range it grew in 2023, though possibly slightly slower. Continued wage pressures and a high cost of capital (private investment is seen contracting by 1.3%, which is an improvement over 2023) are expected to dampen economic growth in 2024. The former is driven by the momentum gathered in 2023 (the Organisation for Economic Co-operation and Development estimates average wage growth of 5.5% in 2023) but is subdued by an increase in unemployment, which was seen reaching 5.8%, up by 0.8 percentage points. Wage increases will nevertheless continue to impact core inflation, which should decelerate compared to 2023 but remain above the 2% target. As per the cost of capital, the Danish central bank is expected to keep high interest rates throughout 2024 to maintain the peg to the euro. The expected 2024 slowdown of export activities (driven by a reversal of the surge in the medical industry, which lifted the entire Danish economy in 2023) will support that objective.

Finland

Finland’s economy is expected to grow by less than 1% in 2024, hampered by the depressed confidences of both consumers and businesses. Therefore, private consumption is expected to remain stagnant, which is still an improvement over the 0.5% reduction in 2023. The unemployment rate is expected to average 7.4% over the year and will contribute to subdued consumer spending, which will help dampen imports and enable a positive contribution of international trade to 2024 growth. While interest rates are high, further increases seem unlikely (Finland is the only country among the Nordics that has adopted the euro), which should support private investment. Another growth enabler should be fiscal policy, with increased defense and security spending outweighing cuts in other spaces.

Iceland

Iceland’s GDP growth in 2024 is expected to slow down considerably to about 2.0%, from an estimated 4.9% in 2023. In 2023, among the Nordics, Iceland had the highest inflation (core inflation of 8.3%)—a trend expected to continue in 2024 (within the range of 4.0%) despite a marked slowdown. This impacts real wage growth and private consumption—the latter being a growth engine Iceland depends on more than the other countries in the region (53% of growth typically comes from private consumption, versus 46% for the other Nordic countries). Tourism reaching capacity limits, the fastest unemployment increase (expected at 4.2%, from 3.5%), and fiscal and monetary policies (central policy rate at 9.5% since August) will act as additional growth dampeners in 2024.

Norway

The Norwegian economy is expected to stagnate in 2024. The so-called “mainland” economic growth (referring to the Norwegian economy exclusive of offshore oil and gas activities) should be approximately 0.5%, down from 1.1% in 2023 (total GDP growth should be 0.7%). A key factor in the outlook will be inflation (with core inflation being among the highest in the region), which has been difficult to contain due to the weakening of the Norwegian crown and continued pressure on the job market. The Norwegian central bank is the only one in the region that increased its policy rate in the fourth quarter of 2023.

In such an environment, private investment is expected to decline further than in 2023 (around 0.9%), while the expansion of government expenditures (enabled by transfers from the country’s oil fund) should play a role in keeping the country in positive growth territory.

Sweden

After contracting in 2023, 2024 should bring the Swedish economy back into positive growth territory, although at a limited pace (approximately 0.9%). Both private consumption and investment are expected to rise in 2024, while being restrained by negative economic sentiment shared by consumers and businesses (at least in the first half of the year). The economy will also continue to suffer from the highest unemployment rate in the region, which could grow slightly in 2024. But this should help keep inflationary pressures in check, with Sweden expected to record the lowest inflation rate of the Nordics in 2024 (2.6% core inflation), after being the second highest in 2022 and 2023. Swedish fiscal policy is expected to remain neutral in 2024, but the natural expansion of government expenses will contribute to growth.

Central Europe

Aleksander Laszek and Rafal Trzeciakowski

Among Central European economies, 2023 has been a year of varied levels of economic slowdown. While the two biggest economies—Poland and Romania—avoided recession tentatively, Czechia, Hungary, and the Baltics are at risk of recording negative growth. Measured by GDP, this decline could comprise one-fourth to one-third of the region defined as 11 EU member states of the former Eastern Bloc.

The most curious development in 2023 has been the divergence between Poland and Germany. In the past, economic conditions in Poland and Central Europe have largely followed Germany due to their vast trade ties and the sheer size of Germany’s economy. Central Europe’s GDP is less than two-thirds that of Germany, while Poland stands at less than one-fourth. Despite that, economic sentiment in Poland and Germany has been diverging for the past year.

While in December 2022, the European Commission’s economic sentiment indicator appeared to be transitioning from contractionary territory into an upswing for both countries, this dynamic quickly changed, with Poland going into an upswing and progressing toward expansion, while Germany slid back deep into contractionary territory. The sentiment indicator is a composite of five sectoral indices for industry (weight 40%), services (30%), consumers (20%), retail (5%), and construction (5%). Balances are constructed as the difference between the percentages of respondents giving positive and negative replies.

Economic growth in Central Europe is expected to rebound next year, led primarily by Romania and Poland. This growth will be supported by expansion into Western Europe as inflation and interest rates decline but remains at risk of the unfavourable outlook in Germany. We looked at how exposure of Polish manufacturing subsectors to Germany drags their business sentiment. We cross-referenced the change in 28 business tendency survey indicators with sectoral exposures to the German economy, proxied by the share of German-controlled firms. While the sentiment has generally improved in the past year (from October 2022 to October 2023), the subsectors more exposed to Germany have been less optimistic. This single factor explains around 40% to 50% of the changes in business expectations about foreign order books, general economic situation of the enterprise, production, domestic and foreign order-books, and financial situation of the enterprise.

According to Ignacy Morawski, chief economist of Puls Biznesu, a Polish business daily, in the second half of 2023, industrial production has been declining in the parts of manufacturing focused on foreign markets, while increasing in the ones catering to the domestic market. And according to Reuters, the Ifo, RWI, and DIW institutes all cut their 2024 GDP forecasts for Germany in mid-December from their previous expectations published in September. Questions thus remain on how long this divergence between Poland and Germany can last.

Central Europe is forecasted to grow much faster than Western Europe. In terms of GDP growth, according to the Autumn 2023 Economic Forecast prepared by the European Commission, in 2024, Central Europe will grow more than twice as fast as the rest of the European Union (2.5% versus 1.1%). Poland and Romania—the biggest economies in the region and the fastest growing large economies in the European Union—will contribute two-thirds of this growth. The region is still benefiting from the convergence premium, as its standard of living is gradually catching up with Western Europe.

Nevertheless, labor costs remain much lower, which, coupled with improving infrastructure and access to common market, makes it attractive for investors interested in nearshoring or friendshoring42 amid growing geopolitical tensions. Although Central European countries are facing several structural challenges like aging or the need to decarbonize, most of them have vibrant, flexible economies. Their strengths were at full display recently, when they managed to house and integrate into the labor market enormous number of refugees from Ukraine.

Africa

South Africa

Hannah Marais and Hanns Spangenberg

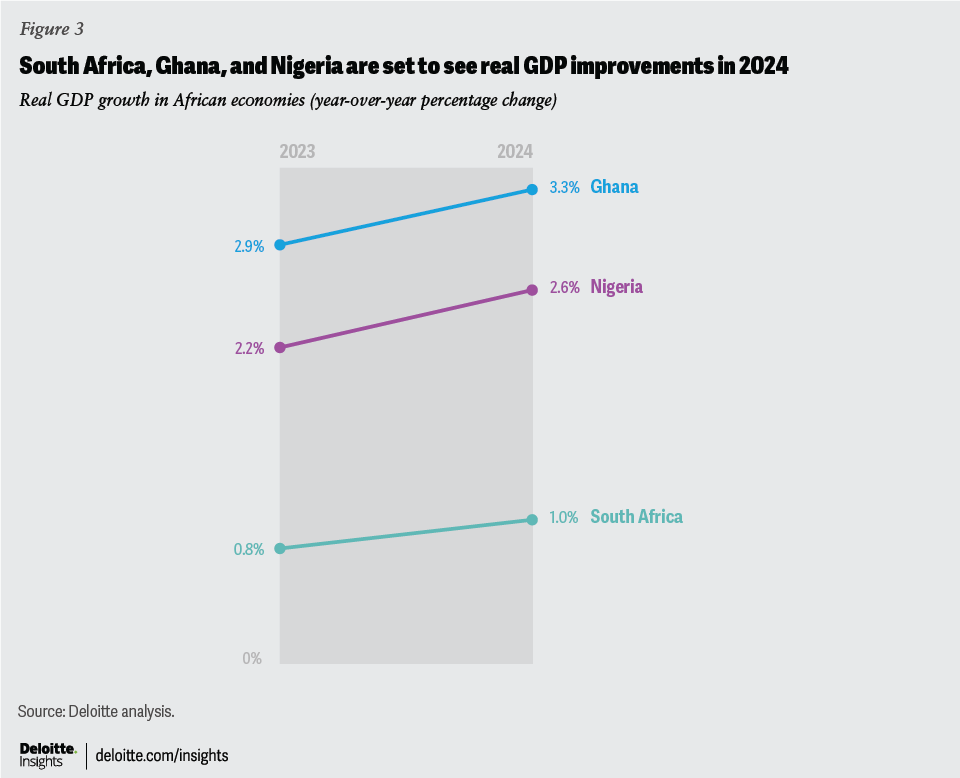

The South African economy remains under pressure going into 2024, largely due to supply-side constraints in the electricity and logistics sectors. Real GDP growth for 2023 is expected to come in below the National Treasury’s latest forecast of 0.8%. The economy only posted 0.3% growth over the first three quarters,43 including a decrease of 0.2% in the third quarter of 2023.44 Outlooks for 2024 and beyond have also moderated and are dependent on the (historically slow) speed of structural reforms, largely to address record levels of loadshedding (power cuts effected to reduce load on generating plants) experienced during 2023.

Real GDP growth is expected to be around 1% in 2024, and to average only 1.4% per year from 2024 through 2026.45 This does not compare well with the International Monetary Fund’s 4% projection for emerging and developing economies, and even falls below the outlook for advanced economies of 1.7%.46

After being a strong performer earlier in the year, the agriculture sector decreased by 9.6% year over year in the third quarter of 2023. Furthermore, the manufacturing, construction, mining, and trade industries also contracted47—of those, manufacturing and mining have faced more challenging circumstances due to ongoing electricity shortages, weaker freight and logistics capacity, and—in the case of mining—lower commodity prices. Manufacturing and mining are among the six industries (besides electricity, construction, trade, and transport) that by the end of the second quarter of 2023 were still trending below their 2019 levels of gross value added.48

The statistics on the expenditure side were no better. Household final consumption expenditure decreased by 0.3% year over year in the third quarter. Households continue to struggle financially given high interest rates, elevated inflation—particularly food- and fuel-related—the impacts of loadshedding on the cost of living, lower real disposable incomes, and higher debt.

While South Africa’s headline inflation moderated to 5% year over year in the third quarter of 2023—from a peak of 7.6% in the third quarter of the previous year—this trend reversed going into the fourth quarter.49 Headline inflation has remained sticky at the upper end of the 3% to 6% inflation-targeting band and the South African Reserve Bank noted that risks to the inflation outlook remain elevated.50

Nevertheless, inflation expectations moderated in the third quarter of 2023—the first such drop in two years. Consequently, the policy rate was kept steady at 8.25% in November 2023. As inflation moderates into 2024, rate cuts can potentially begin, which will bring much anticipated relief to consumers.

From a fiscal perspective, South Africa’s public finances weakened in 2023. An increase in the budget deficit to 4.9% of GDP was projected in November 2023—up from the 4% estimate in the February 2023 budget. This means that gross debt is expected to rise to 77.7% of GDP in the fiscal year from 2025 to 2026.51 Maintaining a fiscal policy stance that stabilizes debt is one of the key action items tabled by the treasury to unlock much-needed growth and in turn address many social and developmental woes the country faces. Another key action includes a focus on improving the efficiency of public spending.

One of the most significant focus areas in the medium term will need to be investment in infrastructure to stimulate economic growth. This will require government to enhance infrastructure delivery, through upping both quantity and quality thereof; crowding in more private sector financing for larger projects, reviewing the public-private partnership framework; and establishing an agency to support finance and implementation of infrastructure.

The need for continued progress on structural economic reforms, specifically in the electricity and logistics sectors, is now more urgent than ever. The economic costs of failure and inefficiency in these sectors have mounted over the past year, partly due to lack of investment, but also due to mismanagement, corruption, and even theft.

Reforms in the electricity sector (including lower restrictions on self-generation and reforms to encourage private investment) are expected to add over 11 gigawatts of renewable sources to help curb the power crisis in the medium term. With the electricity supply crisis continually weighing on economic growth, it is critical that these reforms continue to be implemented as the country heads into an election year in 2024, to curb power cuts, unlock investment, and get the economy back on course.

Nigeria

Damilola Akinbami

The Nigerian economy has remained resilient despite severe macroeconomic headwinds experienced in the last two to three years. The COVID-19 pandemic and geopolitical tensions in Europe have compounded domestic challenges of high inflation, insecurity, currency weakness, and foreign exchange illiquidity. This has led to sluggish economic growth, with real GDP projected to grow by 2.2% in 2023, down from 3.1% seen in 2022.52

In 2024, the economy is forecasted to grow at a subdued rate again. The consensus projections hover around the range of 2.6% to 3.8%, with the Federal Government of Nigeria projecting an optimistic 3.88% in its 2024 Appropriation Act. The projected sluggish pace of growth can be attributed to a high-inflation environment, which has stifled consumer demand and contributed to the ongoing naira weakness and dollar scarcity. Other factors that will impact the country’s growth trajectory include high interest rates, limited credit growth, an elevated debt-service burden, and a wide infrastructure gap. A faster pace of recovery is expected between 2025 and 2027, as the impact of ongoing promarket reforms begin to bear fruit and inflation starts to moderate to single digits.

Inflationary pressures in Nigeria have been predominantly spurred by cost-push factors. High food, energy, and transport costs have been the major factors driving inflation in the country. The upward trend in Nigeria’s inflation rate is expected to continue in 2024 as currency pressures, high global commodity prices, and policies (such as the likely implementation of cost-reflective electricity tariffs and higher taxes) raise the cost of goods and services. However, the pace of increase in inflation is expected to moderate from the second half of 2024 onward, primarily as a result of base effects and consumer resistance to rising prices. Monetary policy should also restrain inflation beginning in 2025, as inflation-adjusted rates rise throughout 2024.

The exchange rate passthrough effect on consumer prices has also exacerbated the inflation problem in the country. Nigeria is an import-dependent country and hence imported inflation will continue to affect domestic prices through the exchange rate. The currency has lost over 50% of its value against the dollar following the central bank’s exchange rate reform carried out in June 2023, which led to a sharp devaluation of the official rate.53 With limited dollar sources in the short term, the central bank will continue to struggle with meeting its foreign exchange needs. Other sources of foreign exchange supply such as nonoil exports, external financing, and diaspora remittances are unlikely to satisfy demand in the short run. However, the Dangote refinery, which is expected to commence operations soon will help to address some of the external imbalances.

The government is anticipating a fiscal deficit of 3.88% of GDP (₦9.18 trillion) in 2024. This is higher than the 3% threshold stipulated in the Fiscal Responsibility Act of 2007. The fiscal deficit will be largely funded through borrowing, especially domestic, which will account for 66% of deficit-financing. Other funding options include multilateral and bilateral project-tied loans and privatization proceeds, which are expected to increase the country’s debt stock.54

A major challenge the Nigerian government will face in the next few years is the growing debt-servicing burden, which will be excruciating at a time of rising interest rates amid a weakening currency. In 2022, the government used almost all of its revenue to service its debt obligations, leaving little to no room for spending and investment on critical economic sectors—this spells potentially severe implications for the country’s economic growth trajectory.

Ghana

Damilola Akinbami

The Ghanaian economy has had its fair share of macroeconomic headwinds, although it appears to be on its way toward a recovery. The country has been battling a debt crisis, which forced its government to approach the International Monetary Fund for a bailout fund. The country also has one of the highest inflation rates in Africa,55 while its local currency—the cedi—experienced bouts of instability.

The good news is that the tide may be slowly turning in the country’s favor. The approved three-year US$3 billion Extended Credit Facility package of the International Monetary Fund is a major game changer, which will help put the country back on a debt recovery path. A first tranche of US$600 million has been disbursed and the government is in talks with its bilateral creditors to finalize its external debt-restructuring plans. This is expected to restore confidence and boost foreign investment into the country. The bailout loan and the anticipated influx of foreign investment will help shore up depleted external reserves.

Policy authorities will continue to prioritize a tightening stance for both fiscal and monetary policies to address price pressures and ease balance-of-payments issues. The ongoing debt-restructuring plan of the government will lead to lower repayment needs, thereby positively impacting its fiscal position.

The growth of the Ghanaian economy is forecast to maintain its current expansion trajectory, with a projected GDP growth of 3.3% in 2024,56 which is an election year for the country. The anticipated fiscal laxity and election-related spending will likely support the projected expansion in 2024. However, high inflation and policy tightening is expected to weigh on domestic demand, limiting the pace of growth.

Between 2025 and 2028, a faster pace of growth of 5.2% per year is expected,57 which will be driven by a recovery in consumer spending and investment. In addition, easing inflationary pressures will trigger a loosening of monetary conditions, which will boost growth prospects. The country is heavily reliant on export proceeds from gold, cocoa, and oil. Investments in these commodities coupled with stable global prices are expected to lead to robust export earnings (especially from gold). This will positively impact the external balance of the country and provide the necessary revenue and investment for spurring growth.

The services sector—the largest contributor to GDP and the fastest-growing sector of the economy—will continue to drive growth, followed by industry and agriculture. Mining activities are expected to pick up following the recommissioning and expansion of the Bibiani gold mine in western Ghana. The mine’s current estimated capacity of 200,000 troy ounces per year is projected to increase by 10% in 2024 and 50% from 2025 onward.

Ghana’s inflation has started declining, although it is still significantly higher than the Bank of Ghana’s upper limit of 10%. The downward inflation trend witnessed in 2023 has been largely driven by the central bank’s tight monetary policy stance, exchange rate stability, and favorable base effects. This downward trend is expected to persist in 2024, with a year-end figure of 15%.58 The decline will be driven by falling food prices and the impact of the International Monetary Fund’s loan on the cedi. The anticipated election spending will limit the pace of moderation in inflation. Between 2025 and 2028, Ghana’s inflation rate is projected to fall even further to single digits, bringing the economic indicator within the Bank of Ghana’s 8% target (plus or minus 2 percentage points).

Asia and Oceania

China

Xu Sitao

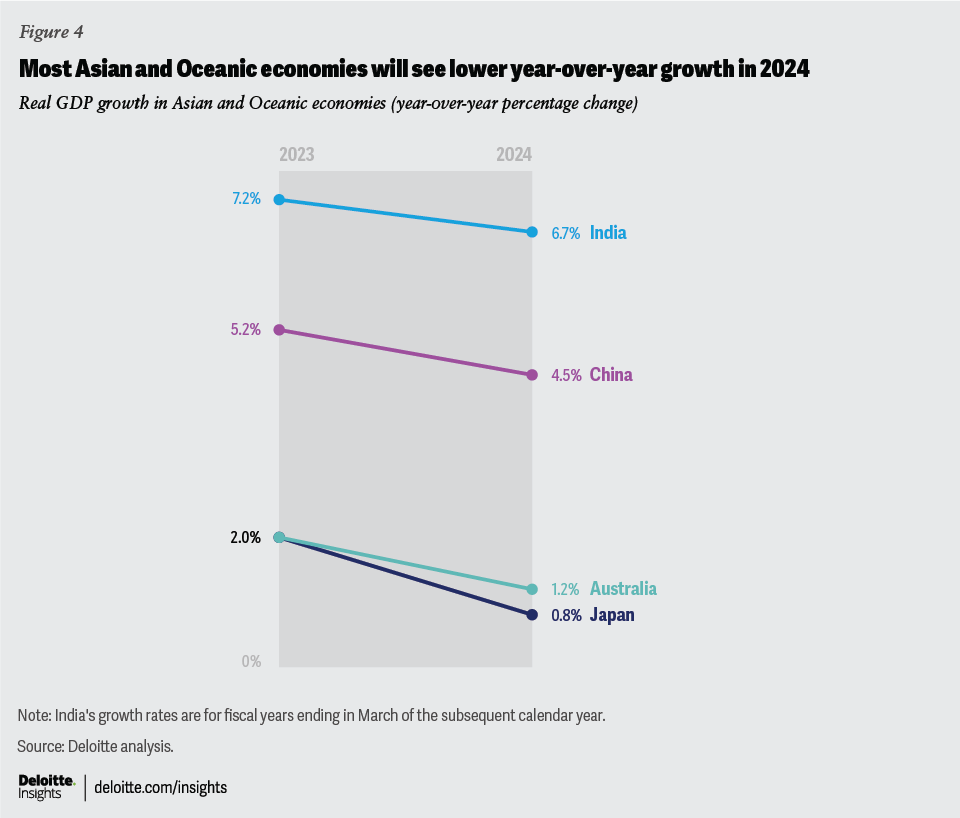

It is almost certain that the growth rate of around 5.2% for 202359 would have been comfortably achieved without additional stimulus for China. With a growth rate of 5.2% for 2023 and monetary policy remaining accommodative, would the likelihood of further fiscal stimulus be diminished? Should China set a lower growth goal or prioritize higher-quality growth? Does a higher growth target signal an emphasis on economic development amid geopolitical tensions?

This policy dilemma reflects a dichotomy between generally stable macro data in 2023 and subdued investor sentiment. Pro-growth policies and structural reforms are often trade-offs, but geopolitics has made such trade-offs more acute.

In the property sector, the offshore US dollar bond market has experienced a drying up of liquidity, and stock prices of major developers are trading at distressed levels. Residential property markets in first-tier cities (Beijing, Shanghai, Shenzhen, and Guangzhou)—considered core assets by most domestic investors due to the concentration of medical and educational resources—have declined by roughly 20% in price this year. Price corrections in second- and third-tier cities are even more significant. While we believe China is in a postproperty era and needs new growth drivers, we don’t see a systemic risk due to consumers’ vast savings and strict capital controls, allowing the central bank to maintain an easing bias without concern for exchange-rate fluctuations.

Can the green economy or various forms of the so-called “new economy” emerge as the principal growth driver if the property sector remains stagnant? The answer seems unlikely in the short run, given the profound impact of property on various sectors and consumer balance sheets. Therefore, “reflation” may become a more necessary condition for China to transition into a different growth model.

Let’s review the pros and cons of a major fiscal stimulus. On the pros side, the primary argument is to prevent a potential deflationary spiral or Japanese-style protracted slow growth. Investors are clearly eager for substantial stimulus—often referred to as a “bazooka” stimulus—that entails improved liquidity and confirms economic development as a key policy objective.

However, we are in the cons camp for several reasons. China's lack of inflationary forces has stemmed from overcapacities in the manufacturing sector and inadequate demand—policymakers have increasingly pointed to the latter as a key challenge. A large fiscal stimulus—akin to late 2008—could worsen both leverage overhang and overcapacities. The externality of overcapacities can’t be easily shrugged off, especially amid rising protectionism. A significant fiscal stimulus may exacerbate trade tensions between China and the European Union. That’s why we advocate for more fiscal relief to households and firms most affected by COVID-19–induced lockdowns.

The immediate priority is clearly the property sector, given its sheer size. Measures to ease restrictions in Beijing and Shanghai—such as the reduction of initial down payments, extension of mortgage duration, and cuts in mortgage rates in December—are steps in the right direction. Similar measures have been taken in most cities, but the actions in Beijing and Shanghai carry more weight in terms of policy direction.

The easing of policy in Beijing and Shanghai signals a few changes. Firstly, policymakers demonstrate more commitment to encouraging consumers to contribute to growth, as housing demand in these cities represents more of a demand for improvement. Secondly, removing restrictive policies on the demand side effectively rolls back previous housing policies. Of course, more could be done—a 30% initial down payment is still high and could be further reduced. The government has ample means to boost pent-up demand, which has been deterred by concerns over developers’ potential inability to deliver finished homes. Can the government underwrite this? The government could certainly designate some unsold flats as affordable housing units—the crux is that, notwithstanding excesses in terms of volume and valuation, Chinese consumers do not have high leverage in aggregate.

At the central economic work conference in December, the public sector was instructed to maintain fiscal prudence. This is logical, considering many local governments rely on land sales as their principal source of revenue. Interestingly, the notion of “building the new before breaking the old” implies a recalibrated trade-off between reforms and reflation. The emphasis is on the latter, at least until the property sector has stabilized. Before economic recovery takes hold, investors are likely to draw parallels between China today and Japan yesterday in terms of both balance sheet adjustment and policy responses.

China’s chief advantage versus yesterday’s Japan lies in its development stage—in the “catching-up” phase. However, the external environment is far more challenging than Japan faced after its bubble burst. China’s exports, which seemed to have turned the corner in November, could face severe protectionism. Following a decision by the European Union to investigate China’s electric-vehicle exports on the grounds of subsidies, there is a strong likelihood for the European Union to impose tariffs because the auto sector is being viewed by several of its member states as a key industry. If China resorts to tit-for-tat measures, there could be a mini trade war between China and the European Union in early 2024.

In conclusion, we anticipate more supportive policies to be unveiled in 2024, but these measures won’t amount to a “bazooka.” Regarding the growth target, we foresee it hovering around 5%, which aligns with our current forecast of 4.5%. Additionally, we expect a mild rebound of the renminbi due to anticipated falling USD interest rates. However, it’s unlikely that the exchange rate will crack 7.0, as interest-rate differentials are likely to continue favoring the greenback.

Japan

Shiro Katsufuji

Japan’s economy is on its way to break from its long-lasting deflationary environment. The year-on-year consumer price index inflation rate, excluding fresh food was 2.5%. Excluding fresh food and energy, the rate stood at 3.8% in November.60 Those figures suggest that inflationary pressure is penetrating across the economy, and, though still partially driven by higher energy and material prices, is likely to stay between 1% and 2% for the coming year. Various surveys indicate that Japanese business firms are currently keen to keep raising wages, to cover labor shortages and retain skilled talent for digitalization, sustainability, and several other “growth” businesses.

The Bank of Japan is targeting “sustainable inflation accompanied by wage growth” as a condition for normalizing the current quantitative and qualitative easing in its monetary policy. Bank of Japan Governor Ueda has said it requires evidence that negotiations will yield significantly stronger wage growth before raising rates. The Japanese government had set out four criteria to determine if Japan’s economy could break away from deflation, namely 2% consumer price index inflation, positive GDP deflator growth, a positive output gap, and positive unit labor costs. We expect wage growth to be above 3% in the 2024 spring wage negotiation (shunto), as was achieved in 2023. With inflation running above wage growth, there is a good chance of stronger wage hikes from the country’s largest employers. Should this come to pass, wage growth will accelerate in the middle of the year as inflation decelerates. We expect that those conditions will be met in 2024 and that the Bank of Japan will lift rates in spring 2024.

Japan’s economic fundamentals are making a solid recovery. We forecast 2.0% real GDP growth in 2023 and 0.8% in 2024. The government lifted all pandemic-induced restrictions at the beginning of 2023. Thanks to those policy shifts, the economy rebounded strongly in the first half of 2023. Though real GDP growth turned negative in the third quarter, we think this was a temporary step back from the rebound in the preceding periods. In 2024, though slowing slightly from 2023, Japan’s economy is likely to maintain its potential growth rate and positive output gap (excess demand).

Consumer spending made a strong recovery in the first half of 2023. However, the spending temporarily peaked in the middle of 2023—partially because pent-up demand ran out and spending on daily necessities was affected by higher inflation. Still, consumers are actively spending money on leisure and tourism, utilizing excess savings built up during the pandemic. In 2024, steady growth in consumer spending will sustain economic growth if wage hikes and slower inflation generate more spending power.

The business sector generated historically high profits in 2023, thanks to higher demand in the service sector as consumers’ social activities recovered, and a weaker exchange rate that gave higher yen-denominated profits. Business sectors are now more aggressive in passing input costs to sales prices, which had not been evident in conventional Japanese corporations during the deflationary era. The practice enables firms to use their profits to hike wages and make investments to expand their business. We believe this trend will continue through 2024, and the business sector will lead to economic growth in Japan.