{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

EU regulation drives the sustainability transition has been saved

Cover image by: Rovinya Sollitt and Mark Milward

United Kingdom

United Kingdom

United Kingdom

United Kingdom

United Kingdom

This report is brought to you by the EMEA Sustainability Regulation Hub

The shift to a more sustainable planet is gaining momentum, but at an insufficient rate. As things stand, the world is on course to miss its principal target of limiting average global warming to less than 1.5 degrees Celsius above pre-industrial levels by 2050. Companies from every industry are therefore facing increasing calls from their consumers, investors and employees to play a greater role in accelerating the net zero transition–and to manage the risks and seize the opportunities it creates.

The net zero transition is the transformational shift in the global economy needed to ensure atmospheric greenhouse gas (GHG) emissions are no greater than the amount of emissions removed. Multiple new regulatory proposals are making rapid progress in the EU as it seeks to lead the way on addressing climate change and stimulating the social and economic benefits that can come from doing so. Implementation of these new EU regulations will drive forward the net zero transition in Europe and play an important role in determining the shape of the new sustainable economy.

While new regulations–regulatory and supervisory policy and legislation–invariably introduce additional compliance costs, they can also help provide certainty, coordinate the collective activities of the private sector, and open up first-mover advantages. As companies attempt to comply with new obligations, they will need to grapple with how they can effectively change their current business strategies, operating models and financing plans.

If business leaders proactively consider and respond to the evolving landscape of new regulations, they will be better equipped to turn the challenges they face into catalysts to unlock opportunities and drive business value. In particular, an understanding of emerging sustainability regulation that extends beyond mere compliance will help business leaders steer their companies through the complex technological, economic and social changes required.

In this report we explore five key themes within which the EU is driving a number of sustainability-focused regulatory initiatives: decarbonisation, greenwashing, transition planning, supply chains and circularity, and sustainable finance. We believe these thematic areas will significantly affect companies’ business strategies, operating models and financing plans, and will force business leaders to act in 2023 and beyond. Across each of the five themes we set out the regulatory changes that are taking place and how these changes create new priorities for companies.

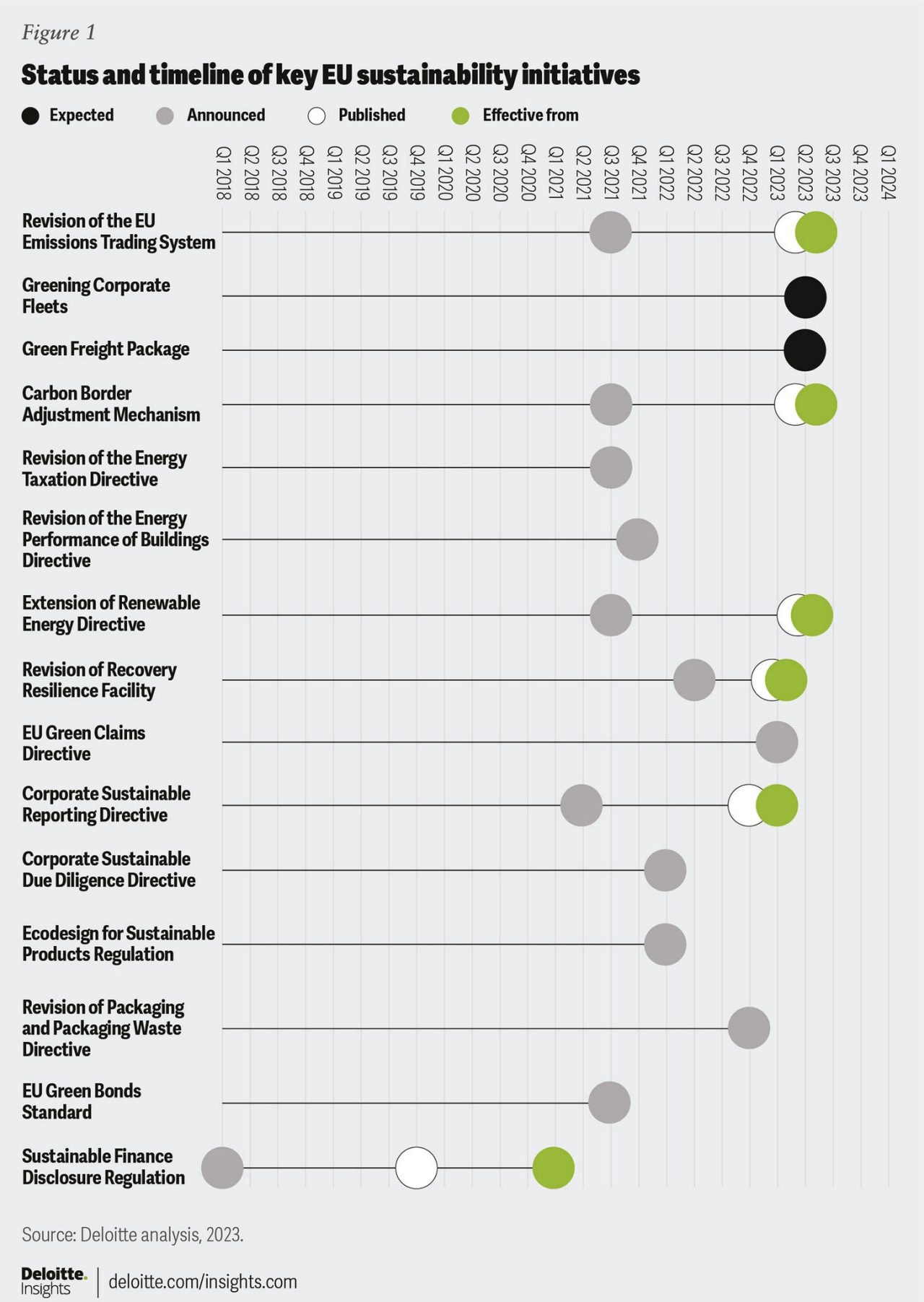

All the regulatory changes we explore originate in the European Green Deal. The Green Deal was adopted in 2020 and is a collection of ambitious EU-wide policy initiatives that aim to make the EU carbon neutral by 2050. At the heart of the Green Deal is a commitment to transform the EU into a fair and prosperous society with a modern and competitive economy. Under EU law, Member States are obliged to take the necessary steps set out in the Green Deal to meet the EU’s climate targets. If a Member State is suspected of failing to fulfil this obligation it could be prosecuted by the European Court of Justice. The obligation for Member States to take adequate climate action has therefore led to a growing number of sustainability-related regulations and requirements for companies operating in the EU and their global value chains. An overview of the key initiatives analysed in this report and their respective timeline is provided in Figure 1 at the end of this section.

Our analysis focuses on the following five broad themes:

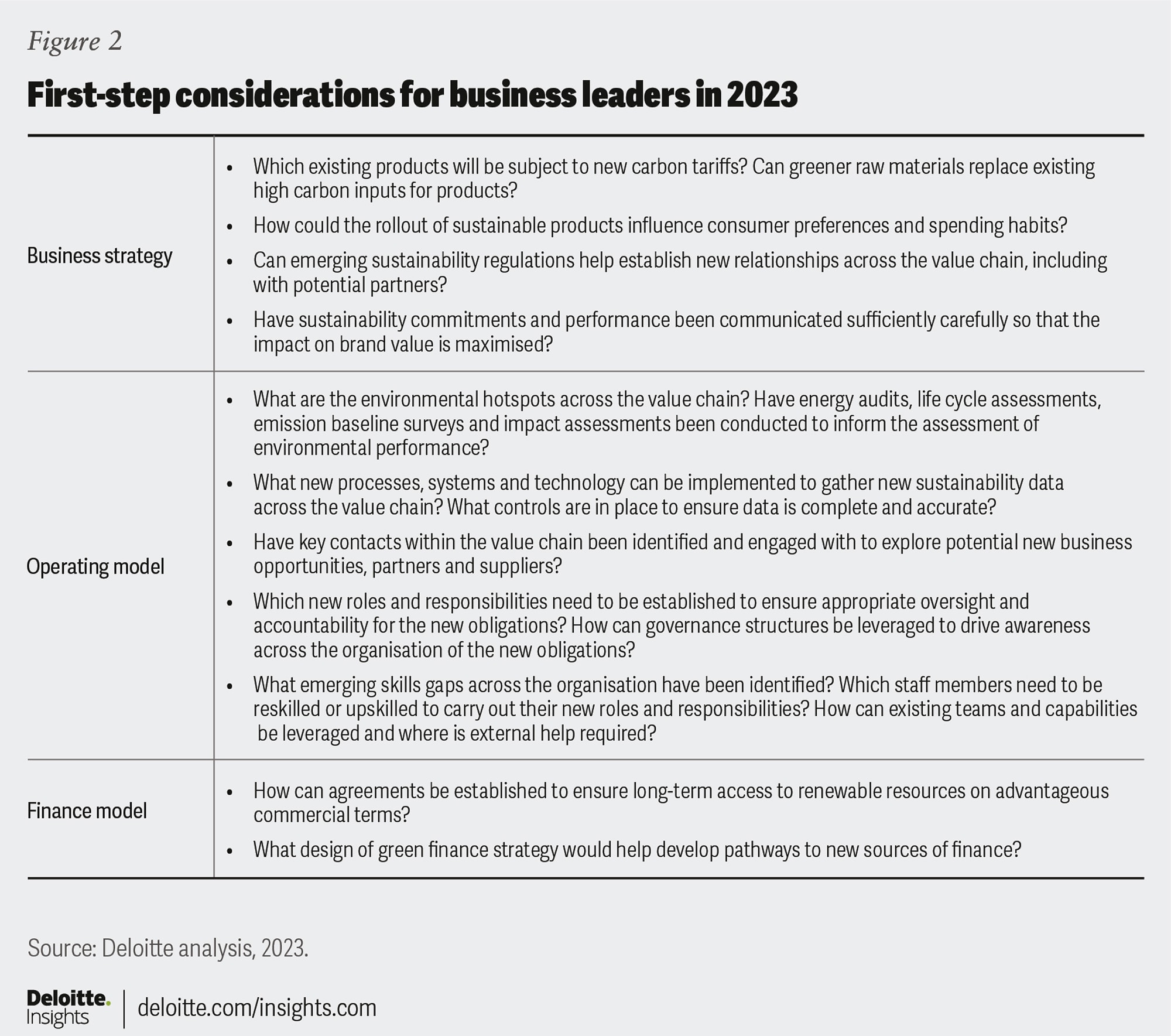

Addressing these priorities will be complex and require long-term planning and significant investment. We highlight a number of ‘first-step’ actions that we believe are priorities for business leaders to consider in 2023. The key considerations for these are summarised in Figure 2.

The regulatory developments analysed in this report may create compliance obligations. But, by considering the implications for companies’ business strategies and operating and finance models they also provide clear opportunities for companies, from enhanced stakeholder reputation and new revenue streams to better risk management and business continuity. By exploring their work within this report’s five thematic areas and taking ambitious action early, companies can build both short-term resilience in a turbulent economy and long-term viability in a world set for significant change.

Regulation: A legal act that is directly applicable in all EU Member States when it enters into force.

Directive: A legislative act that sets out a goal or a result that all EU Member States need to achieve when transposing it into their national legal framework, within a specific deadline.

There are three institutions involved in setting EU legislation:

Legislation is typically decided by the three main institutions coming to an agreement on a specific proposal. The process starts with the European Commission submitting a proposal to the Council and European Parliament. The Council and Parliament then consider the proposal and either accept it or suggest changes. If the text is agreed by both institutions, the legislation is passed and becomes law. If the Council and Parliament are unable to reach agreement, the proposal is discarded and the procedure ends.

“The hard part is getting started, having the momentum, and making the initial investments. Once that’s in place, it's easier to keep going”, John Ferguson, President and Chief Executive Officer, Purolator (in: Deloitte 2023 CxO Sustainability Report)

Regulation is driving the targeting, sequencing and pace of decarbonisation. Companies need to prioritise decarbonisation of transportation, raw materials and energy in their financial and operational strategies.

The reduction or elimination of carbon dioxide emissions from the economy is an area of focus for EU policymakers, as well as for businesses and society, and decarbonisation of transportation, raw materials and energy is a top priority. Carrying this out will have major financial and operational implications for companies in both their upstream and downstream value chains. Changes to the scope and extent of carbon markets will also have implications for carbon offset strategies.

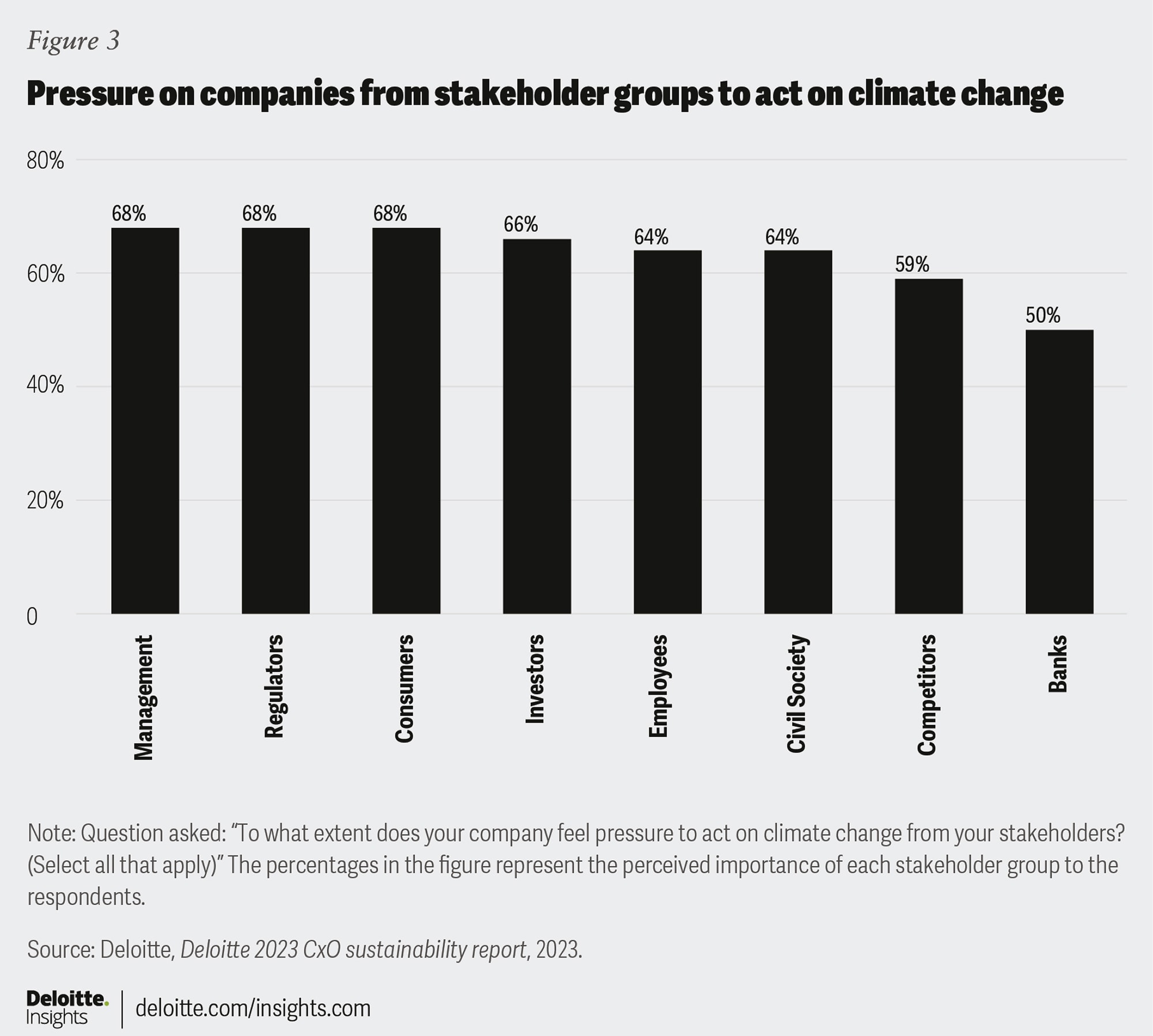

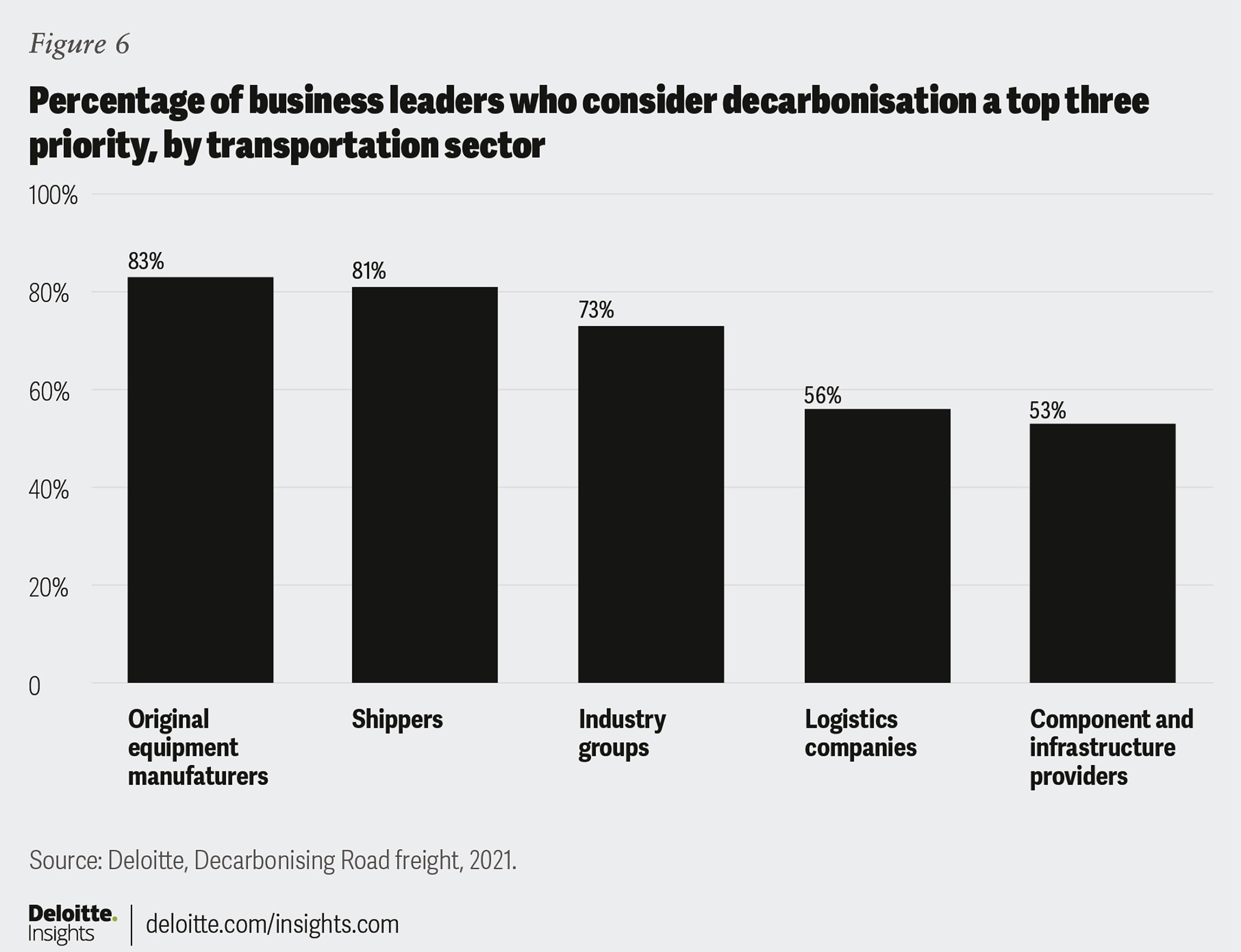

The pressure to act is now coming, however, not just from policymakers but from multiple stakeholders, including employees, banks and investors, as recent Deloitte research reveals (see figure 3). Companies report that the regulators, consumers and management are the strongest sources of pressure.1

The complexity of the task, the scale of change and the large investments required means that it will take most companies many years to plan and fully execute their decarbonisation strategies. Companies therefore need to take policymakers’ current and probable future actions into account when setting out their plans. Recent regulatory developments mean that in the next 12 months companies should, in particular, consider focusing their decarbonisation strategies on the areas of transportation, raw materials and production processes, and carbon trading within their value chain.

Carbon will become more expensive across several key industries, increasing the use of green transportation and of green raw materials.

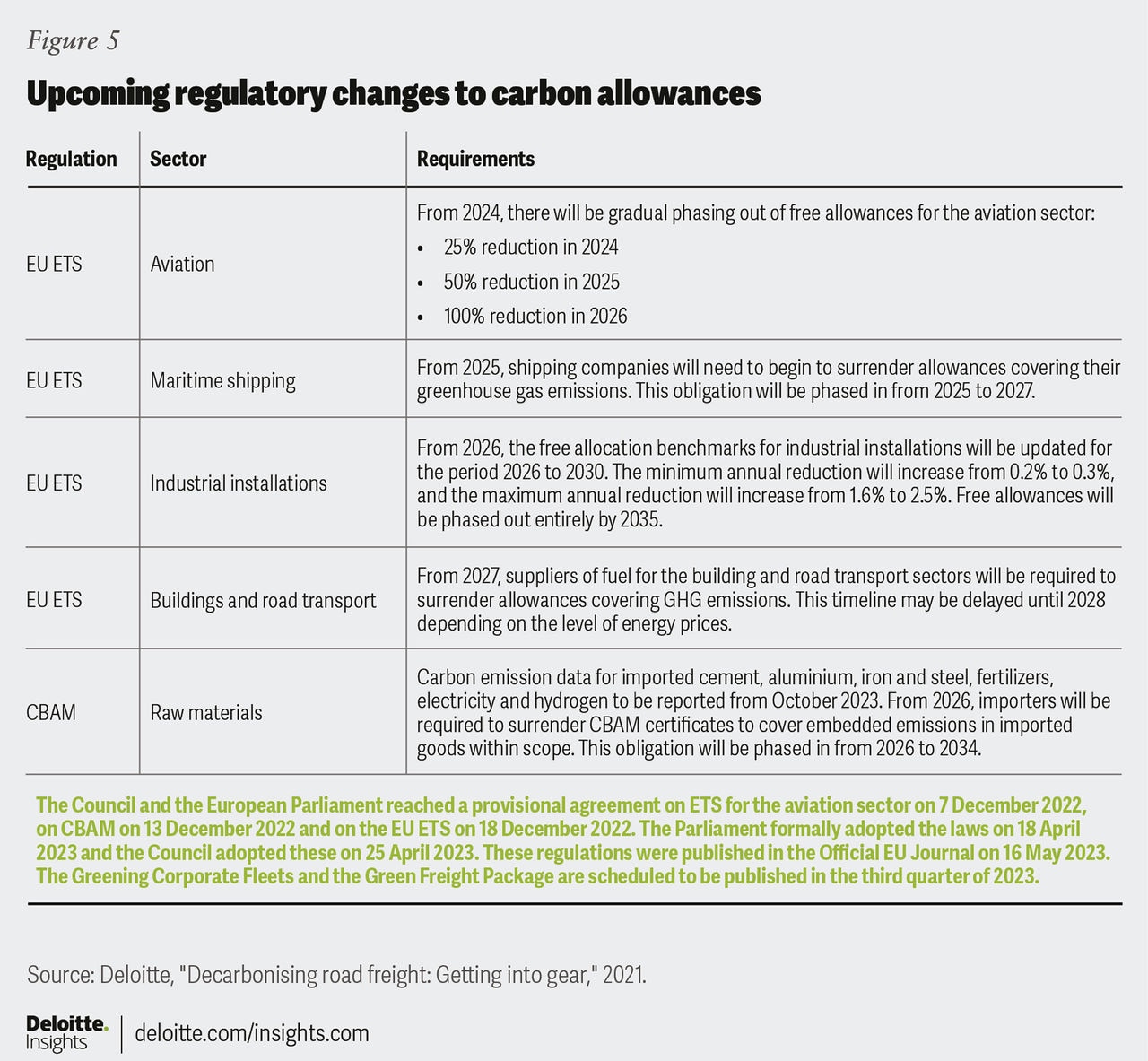

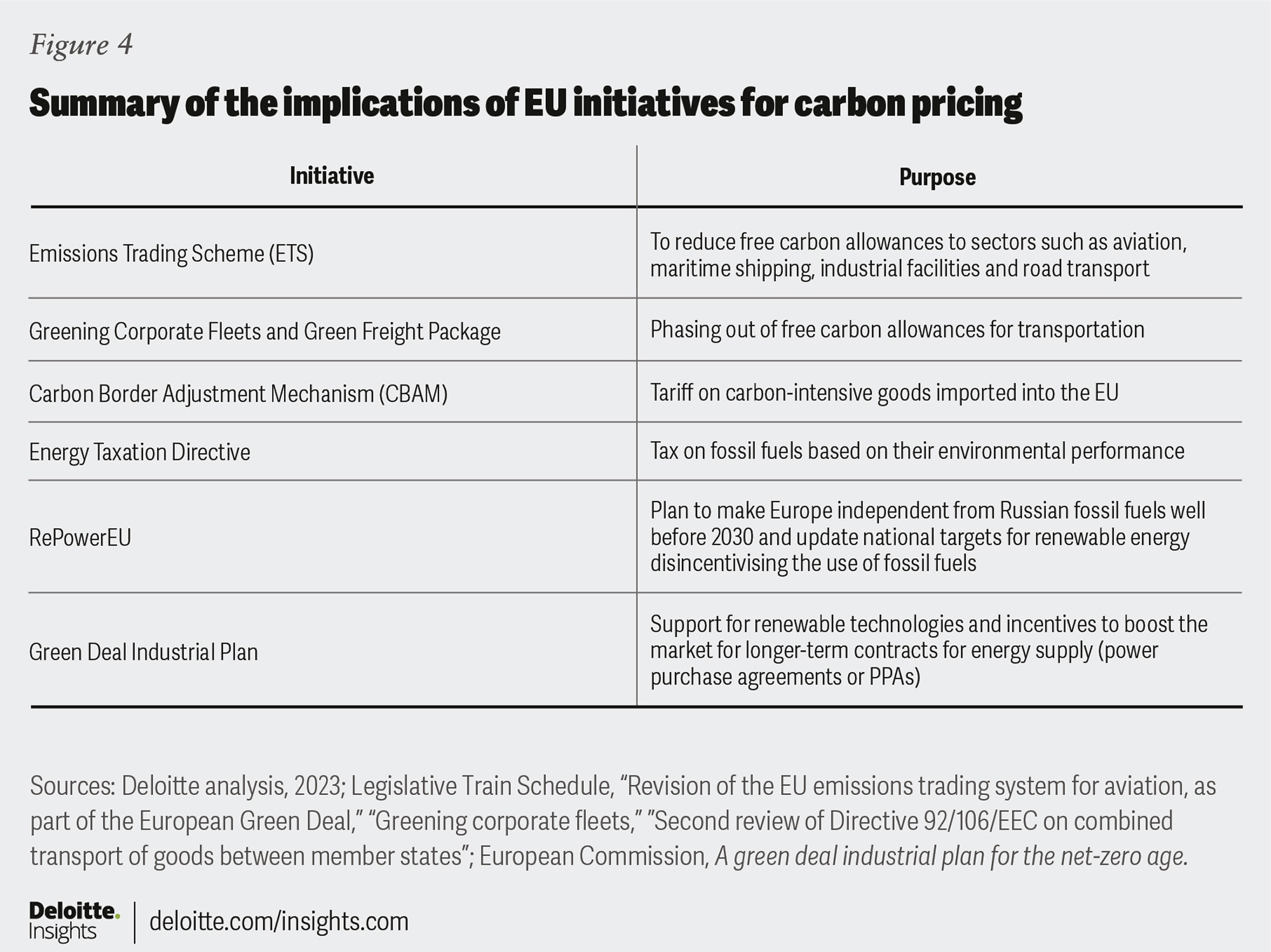

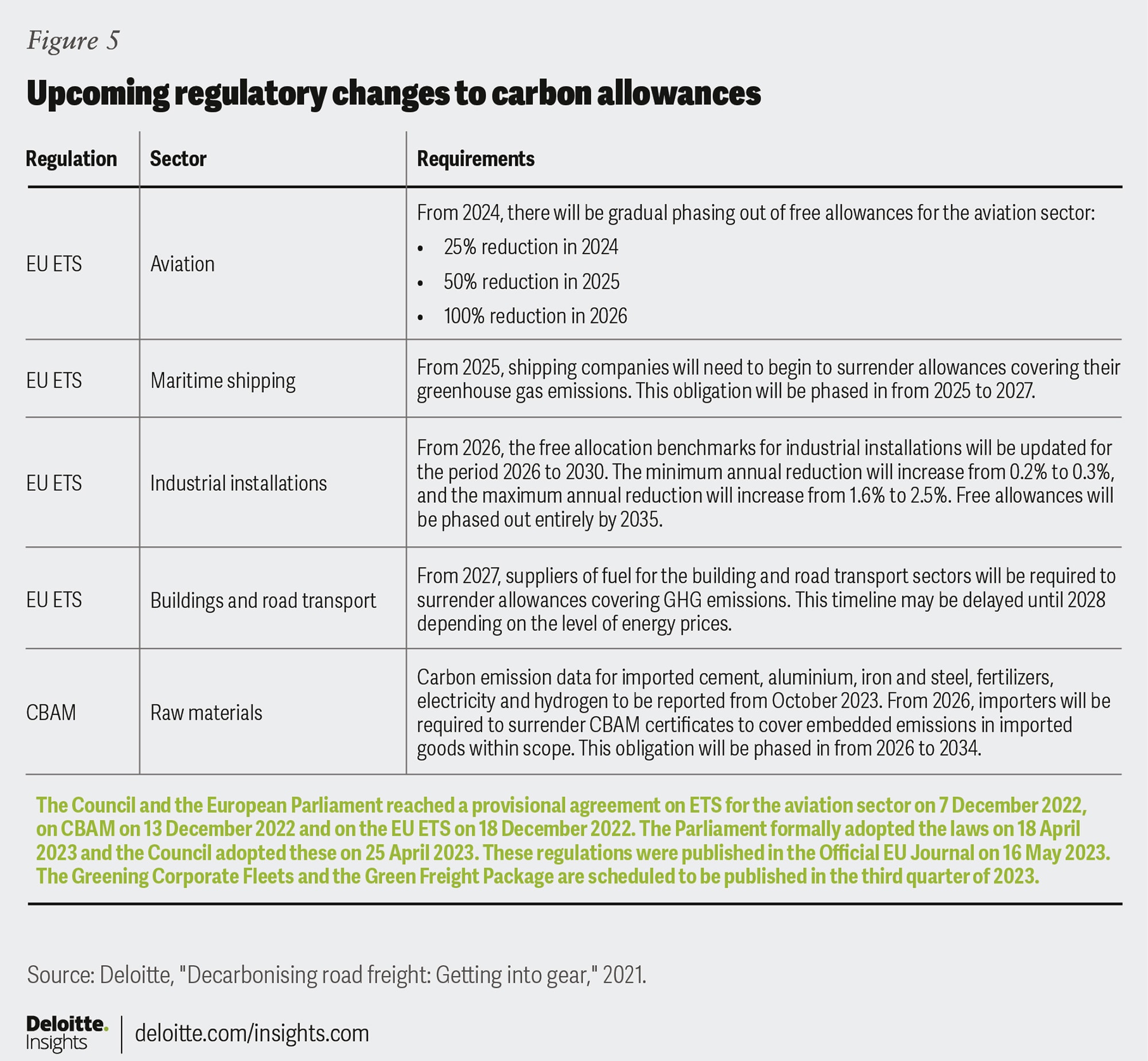

Proposed new EU legislation or changes to existing legislation including the EU Emissions Trading System (ETS), the Carbon Border Adjustment Mechanism (CBAM), the Energy Taxation Directive, Greening Corporate Fleets, the Green Freight Package, the REPowerEU Amendments and the Green Deal Industrial Plan will make carbon more expensive or disincentivise its use.

These initiatives include measures ranging from tighter maximum emissions limits to taxes and incentives. Companies can reduce their carbon use and emissions or pay more for them. They face a range of choices from which they must determine their optimal approach.

Once corporate fleets are covered by EU initiatives, the cost-benefit analysis of transitioning to green transportation changes. At the same time, the availability of affordable, low-emission transportation technologies is increasing rapidly. This means that switching to electric vehicles is now a realistic strategy for companies that own or lease their fleets. However, when a company relies on third parties to provide transportation, whether upstream or downstream, it will have to closely engage with them to ensure that they make increasing use of environmentally-friendly modes of transportation.

Companies in the EU will also be affected by CBAM, as the EU will seek to reduce free allowances to all EU industries covered by CBAM. Companies need to acquire a better understanding of their supply chain and the data related to it in order to be able to assess the carbon footprint of their raw materials (especially those covered by CBAM). This will allow them not only to manage their exposure to carbon taxes but also to reduce the total carbon footprint of products sold. Raw materials wholly produced with fossil fuels using energy-intensive processes will be taxed based on their carbon footprint. Moreover, manufacturers that are already reporting their Scope 3 emissions would need to disclose the higher carbon content of the products they manufacture, which could reduce their appeal to certain consumers.

Fourth parties within the value chain (entities providing goods or services to an organisation’s third party) will also require further consideration. It will be necessary to know whether or not those fourth parties are supporting their suppliers’ decarbonisation transition plans. This could affect a company’s decarbonisation timeline if it becomes necessary to reassess and potentially terminate certain business relationships. There is an element of extraterritoriality, as non-EU based companies serving EU-based companies may be required by clients to comply with EU standards as a condition of conducting business with them.

Under CBAM the need for green raw materials is likely to grow. Importers of key raw materials used in most industries (such as cement, aluminium, iron and steel) will be required to collect and report carbon emissions data from October 2023, and a carbon tax will be applied based on their emissions levels from January 2026.2 If an international Carbon Trading Scheme is adopted at COP28 in November 2023, the pressure to reduce emissions will expand globally. Companies that do not reduce their emissions would need to buy carbon allowances in the market to offset them.

The EU’s CBAM impact assessment estimated that EU imports from all covered industries would decrease by approximately 11 percent in 2030 compared to the baseline.* This decrease in imports suggests that there will be an increase in the demand for EU raw materials with lower carbon footprints.3 For example, some vehicle manufacturers are already using green steel in parts of their range to achieve carbon reduction goals.

*The baseline consists of the EU Reference Scenario 2020 (“REF”), the main elements of which are depicted in an Annex of the impact assessment for the revision of EU ETS Directive.

Increasing the use of clean energy will be increasingly cost effective. Measures such as the Energy Taxation Directive, the REPowerEU Amendments and Green Deal Industrial Plan promote clean energy and disincentivise the use of fossil fuels by making them more expensive.4 Fuels will be taxed based on their energy content and environmental performance, with those most harmful to the environment being taxed the most. The use of renewables will be promoted by making power purchase agreements (PPAs) more attractive, accelerating the deployment of renewables and integrating renewables in electricity systems.

Companies should therefore analyse their energy supply to ensure that they use mostly renewable sources and avoid fossil fuels. In addition to identifying clean energy suppliers, companies should also invest in renewables by installing renewable energy solutions (e.g. solar or wind) in their facilities. Similarly, energy suppliers should be prepared for a continuous increase in demand for renewable energy, which will require significant investment.

It should be noted that since every Member State will need to transpose the amendments to the Directive into national law to achieve the target, the actual impact of these initiatives on energy prices will be subject to this process.

The initial actions companies should consider taking are:

In a joint report by Deloitte and Shell, over 150 business leaders and experts from over 20 countries were asked about the importance of road freight decarbonisation for their companies. One of the conclusions of the report was that companies still face multiple challenges decarbonising transportation, including higher fleet costs, a lack of financial incentives and government support to switch, and technical limitations.

Over 70% of interviewees considered road freight decarbonisation one of their three highest priorities. These responses reflect the fact that, after heavy industrial sectors, road transportation is the second largest category of carbon dioxide emissions and one of the most difficult to address. Heavy-duty trucks (HDTs) and medium-duty trucks (MDTs) account for approximately 60% of road freight emissions and, until very recently, no reliable greener options to replace them were available. Recent technological advances mean that zero emission electric HDTs and MDTs are now available in the market. For example, trucks with up to 40-ton loads can now travel up to 350 km, while with additional batteries the range can be extended to over 550 km. The number of electric truck alternatives is likely to grow considerably in the near future and the cost of such units is expected to decrease over time.6

“Customers, citizens want proof of the positive impact…Reliable data are important. Auditors have a key role–to drive reliable positive data so that consumers, government, stakeholders can trust companies and work better together with them” – Claire Berthier, Chief Executive Officer, Trusteam Finance

“Customers across regions have high expectations for the products they purchase and companies they choose to do business with. ESG metrics are an increasingly important part of their decision-making process” – Mary Jacques, Executive Director, Global ESG and Regulatory Compliance, Lenovo (in: Deloitte 2023 CxO Sustainability Report)

Greenwashing has become a key concern for policymakers as misleading practices and unsubstantiated green claims become more frequent. As regulatory developments in this area expand rapidly, companies need to be aware of the risk of being accused of greenwashing and guard against it by ensuring their claims are accurate, complete and fully defensible.

FS firms are already subject to a number of regulatory initiatives that address greenwashing in financial products and services and in reporting. There is no official definition of greenwashing in the EU but the term has been defined in EU financial regulation of some products and instruments.7

“The practice of gaining an unfair competitive advantage by marketing a financial product as environmentally friendly, when in fact basic environmental standards have not been met.”8

“The practice of gaining an unfair competitive advantage by recommending a financial instrument as environmentally friendly or sustainable, when in fact that financial instrument does not meet basic environmental or other sustainability-related standards.”9

In this report we define greenwashing as an attempt by a company to make its policies, products or services appear to be ‘greener’ than they actually are, thereby misleading its clients, customers or investors.10 It is important to note that companies can be judged to be engaging in greenwashing regardless of whether a misleading claim is deliberate or inadvertent.

When the European Commission and national consumer authorities in the EU screened corporate websites in 2020 they found that out of 150 claims about products’ environmental characteristics over 50 percent provided ‘vague, misleading or unfounded information.’ The sectors analysed in the survey included garments, cosmetics and household equipment.11

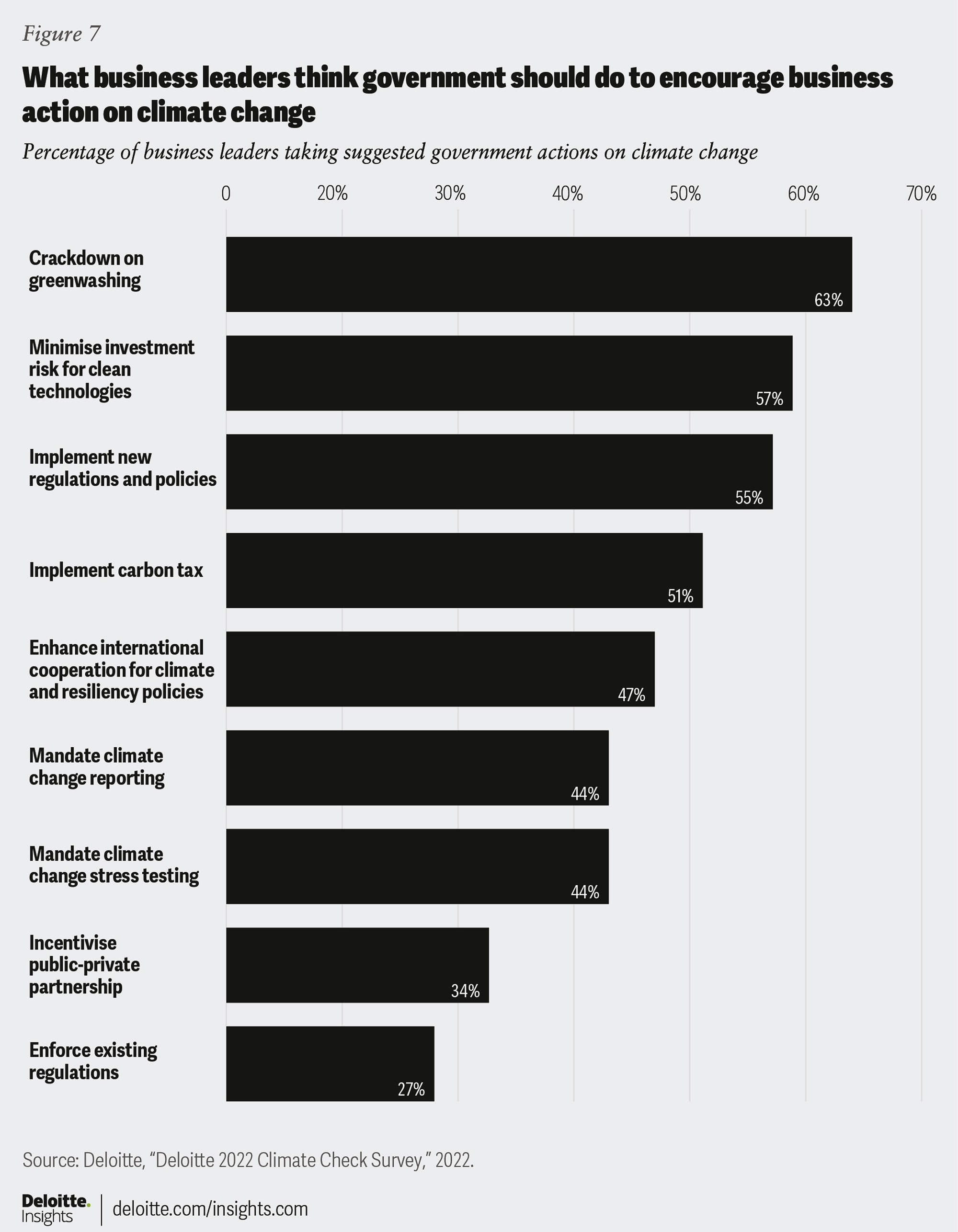

In a recent survey conducted by Deloitte of 700 business leaders, greenwashing emerged as one of their most serious concerns. Asked what governments should do to encourage businesses to address climate change, business leaders listed ‘a crackdown on greenwashing’ as the highest priority. In fact, greenwashing was considered more important than key strategies such as mandatory climate change reporting or carbon taxes.12

There is likely to be increased scrutiny from regulators and stakeholders in coming years as they use existing regulations more actively. In the recent past corporate obligations such as fiduciary responsibility, fair advertising and trading standards have been highlighted to make clear that the issue of greenwashing is already covered by existing regulations. For example, Directive 2019/216113–which entered into force in early 2020 and began to be applied by Member States in May last year, provided remedies to consumers harmed by unfair commercial practices and allowed Member States to adopt rules relating to misleading commercial practices.

Consumers, activists and shareholder groups in the EU and UK have brought an increasing number of cases relating to unsubstantiated green claims to regulators. The UK developments are important as they are often used as a model for other jurisdictions.

These claims have led to notable developments in: the Netherlands, with guidelines issued by the Authority for Consumers and Markets;14 Denmark, where the Consumer Ombudsman now requires life cycle analysis data for sustainability claims;15 and the UK, with the Green Claims Code issued by the Competition and Markets Authority,16 where companies have had to withdraw advertisements, change product labels and modify company communications. Some UK companies have even been taken to court.

The EU Green Claims Directive

New stringent standards requiring companies to substantiate green claims have been proposed. In March 2023 the European Commission proposed a new EU regulation related to greenwashing. The EU Green Claims Directive sets requirements for environmental footprint methods for both products and companies: life cycle environmental performance must be measured and communicated in order to make valid green claims, which must be substantiated and verified ex-ante.17 Claims would need to be checked by an independent verifier against the requirements of the Directive and the verifier would need to issue a certificate of compliance. Environmental labels or ecolabels are also included in the proposed initiative, requiring testing, third-party verification and regular monitoring for companies to be able to use them. The Directive has extraterritorial reach as it would apply to companies outside the EU making claims for goods and services intended for EU consumers.

Life cycle assessment (LCA)

While the proposed Directive is likely to be modified as part of the legislative process due to the regulatory burden it creates, especially for small and medium-sized enterprises (SMEs), one implication is that sustainability data need to extend beyond aggregate company-level information and focus on products or services. A programme of life cycle assessment18 (LCA) of core products and services would be an effective way for companies to approach this, and to meet regulatory and stakeholder expectations.

Ecolabels

LCA can also be complemented by the adoption of ecolabels. Though ecolabels do not consider the carbon footprint of a product, they can be helpful in determining the ingredients or raw materials of a product (for example, whether it is ‘organic’) or by disclosing that a product is free of toxic and persistent chemicals and considers the energy used. An example of this is ‘good environmental choice,’ a Swedish labelling scheme. Ecolabels are likely to become more common once the EU Green Claims Directive has been implemented. Companies need to consider that not all products affect their GHG emissions.

Water footprinting is becoming increasingly relevant, and companies need to be aware that stakeholders are now scrutinising all product aspects, including water use (especially in water-depleted areas) and ecosystem depletion.

LCA can help identify the carbon footprint associated with a product or service and how that carbon footprint could be reduced.

LCA can be complemented by water footprinting analyses. These look at how green water (water from precipitation), blue water (surface or groundwater) and grey water (pollutants discharged to fresh water sources) are used through a product lifecycle.

Gathering data for these analyses could be challenging. However, when suitable data are not available at the local level, it is possible to conduct the analyses using estimates from existing databases.

The objectives of the proposed Green Claims Directive are aligned with other pieces of legislation such as the Ecodesign for Sustainable Products Regulation (ESPR), the Corporate Sustainability Reporting Directive (CSRD) and industry guidance. The potential incremental effect is that many companies, especially small and medium sized ones, could be subject to adverse competitive consequences because they decide not to make environmental claims due to the high costs of compliance and sustainability disclosures. Making unsubstantiated claims could expose companies to fines, legal action, a consumer and investor backlash or a decrease in brand value. With regard to industry guidance, the adoption of the ISEAL Code of Good Practice, which is currently under post-consultation review, is likely to be aligned with the Green Claims Directive.

The initial actions companies should consider taking are:

Last year, based on the comments made by the Danish Ombudsman regarding the need for evidence to support green claims, RE-ZIP, a small Danish enterprise providing circular packaging solutions to webshops, commissioned a comparative LCA for RE-ZIP Bag 2.0. Its packaging solution can be reused up to ten times. The study compared the RE-ZIP Bag 2.0 with single-use mailing bags and included all life stages (cradle to grave) from raw material extraction to production, use and end of life treatment. The purpose of the analysis was to provide environmental savings to consumers in terms of GHG emissions and water consumption. In addition to utilising the data as evidence to substantiate its green claims, RE-ZIP also used the LCA results to identify hotspots in its products. The results showed that a RE-ZIP Bag 2.0 reused ten times saves 1.3 kg of carbon dioxide equivalent (79%) and 6 litres of water (44%).19

New regulations–and rising expectations from stakeholders–are obliging companies to gain a deeper understanding of how to design, implement and disclose a credible transition plan aligned with the 1.5 degrees Celsius target. By prioritising this now, companies will be able to turn their climate ambition into action, reduce the risk of greenwashing and improve their access to sources of green finance.

Despite the rise in the number of companies setting and publicly declaring climate commitments, few have translated their climate ambitions into action. For those which have, only a small number have fully considered and implemented all the steps they must take to pivot their entire strategy and business model to become aligned with limiting global warming to at most 1.5 degrees Celsius above pre-industrial levels. However, stakeholders are increasingly expecting companies to develop and show evidence of actionable and credible transition plans so that they can make an immediate start on the next chapter of their climate journeys. These include policymakers, who are now introducing new standards and disclosure requirements.

New regulations will likely eventually require every large company to design and disclose a transition plan. The EU’s Corporate Sustainability Reporting Directive (CSRD)20 and its accompanying standards (set to be finalised by June 2024)21 state that all listed companies (including SMEs) in the EU and all large companies operating in the EU will need to disclose a transition plan aligned to 1.5 degrees Celsius warming in their annual reports or explain why they have not (and if not, whether they plan to adopt a plan in future). With the CSRD now in force, we will begin to see companies disclose their transition plans in 2025 (figure 8).

For the largest companies operating in the EU (proposed by the Commission as EU companies with more than 500 employees and a net global annual turnover of €150m, and non-EU companies with an EU-wide annual turnover of over €150m), the design of transition plans is expected to become mandatory under the forthcoming Corporate Sustainability Due Diligence Directive (CSDDD).22 The CSDDD is expected to dovetail with the technical requirements set out in the CSRD’s accompanying standards and will set out the obligation for companies to adopt a transition plan; the CSRD will then continue to govern how they disclose it. The CSDDD is currently making its way through the European legislative process. We expect it to be finalised in 2023 and apply from 2026.

The CSRD and CSDDD are extensive in their requirements and go beyond regimes, such as the recommendations made by the Taskforce for Climate-related Financial Disclosures (TCFD), and therefore require a tailored strategic response. Companies’ transition plans must include reduction targets for Scope 1, 2 and 3 emissions23 that are aligned with 1.5 degrees Celsius consistent scenario, be implemented in the company’s business strategy and financial plan and be assured by a third party. As a result, the new regulations cannot be met through a one-size-fits-all approach. Instead, companies need to ensure their responses to the proposals are comprehensive, strategic and embedded within the context of their business, taking into account its size and complexity. This is paramount for company directors who, under the CSDDD, will be responsible for designing and overseeing execution of the transition plans.

The whole value chain needs to prepare for the regulatory changes. Companies within the scope of the regulations will need to scrutinise climate action across their value chain to measure and reduce their Scope 3 emissions, and to identify new risks and opportunities. We expect companies without a credible transition plan in time to find it harder to access new sources of finance from financial institutions. This effect on the value chain is expected to be especially apparent for the business partners of companies within scope of the CSDDD. Under the proposed requirements, in scope companies are responsible for identifying and addressing environmental impacts across their value chain. Business partners can therefore expect to be asked to contractually agree and verify that they will comply with new climate-related obligations as companies pass on their regulatory demands.

The initial actions companies should consider taking are:

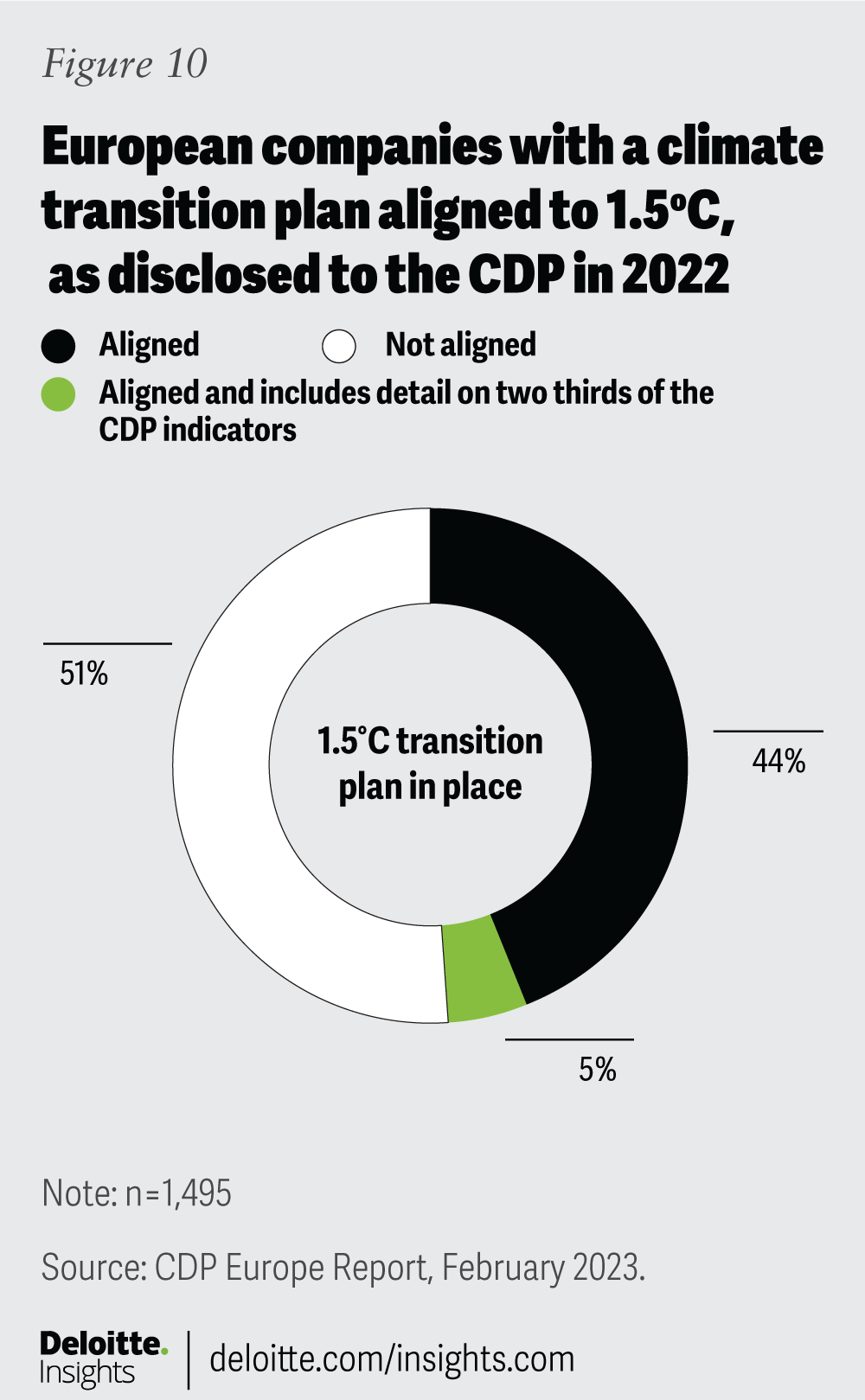

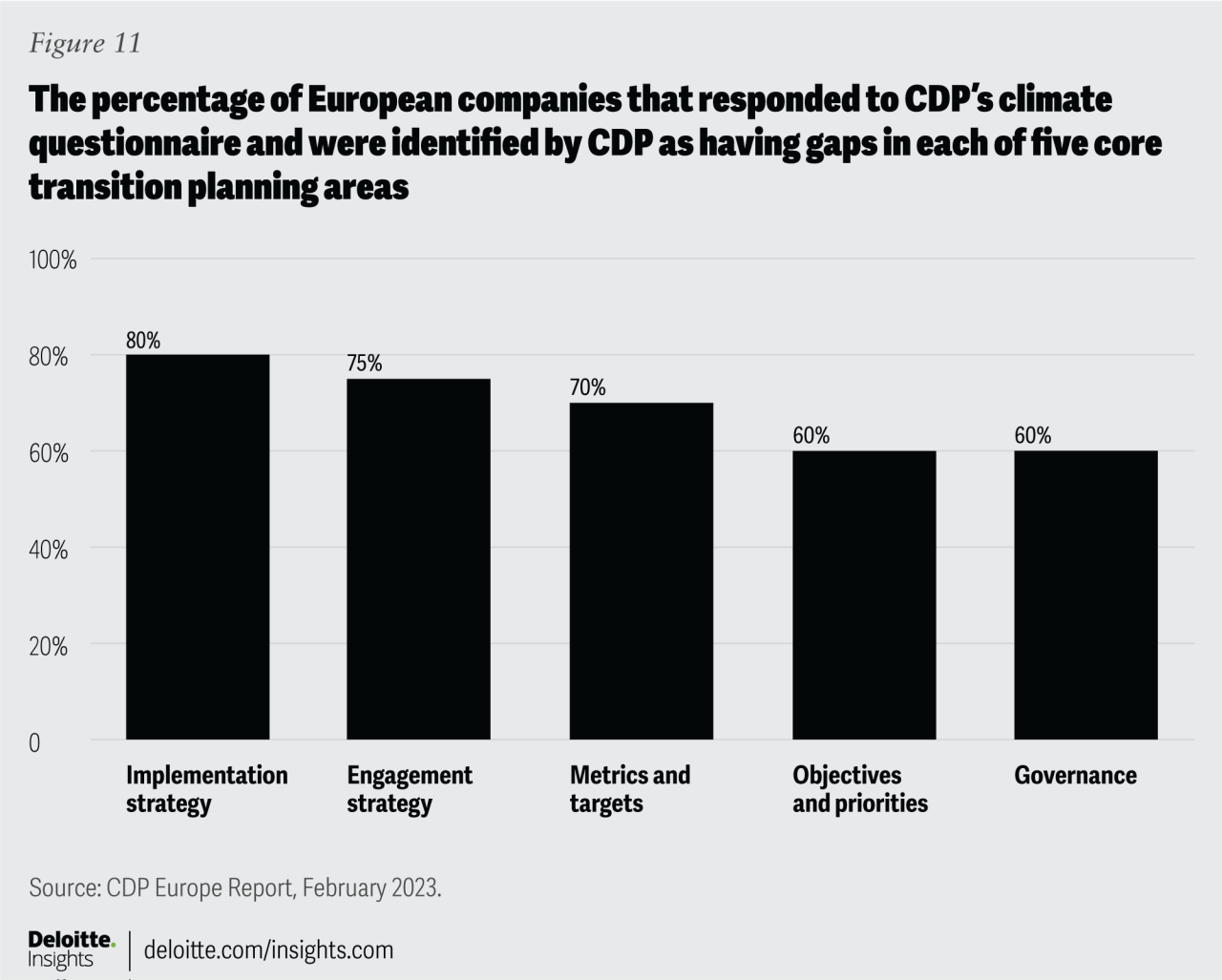

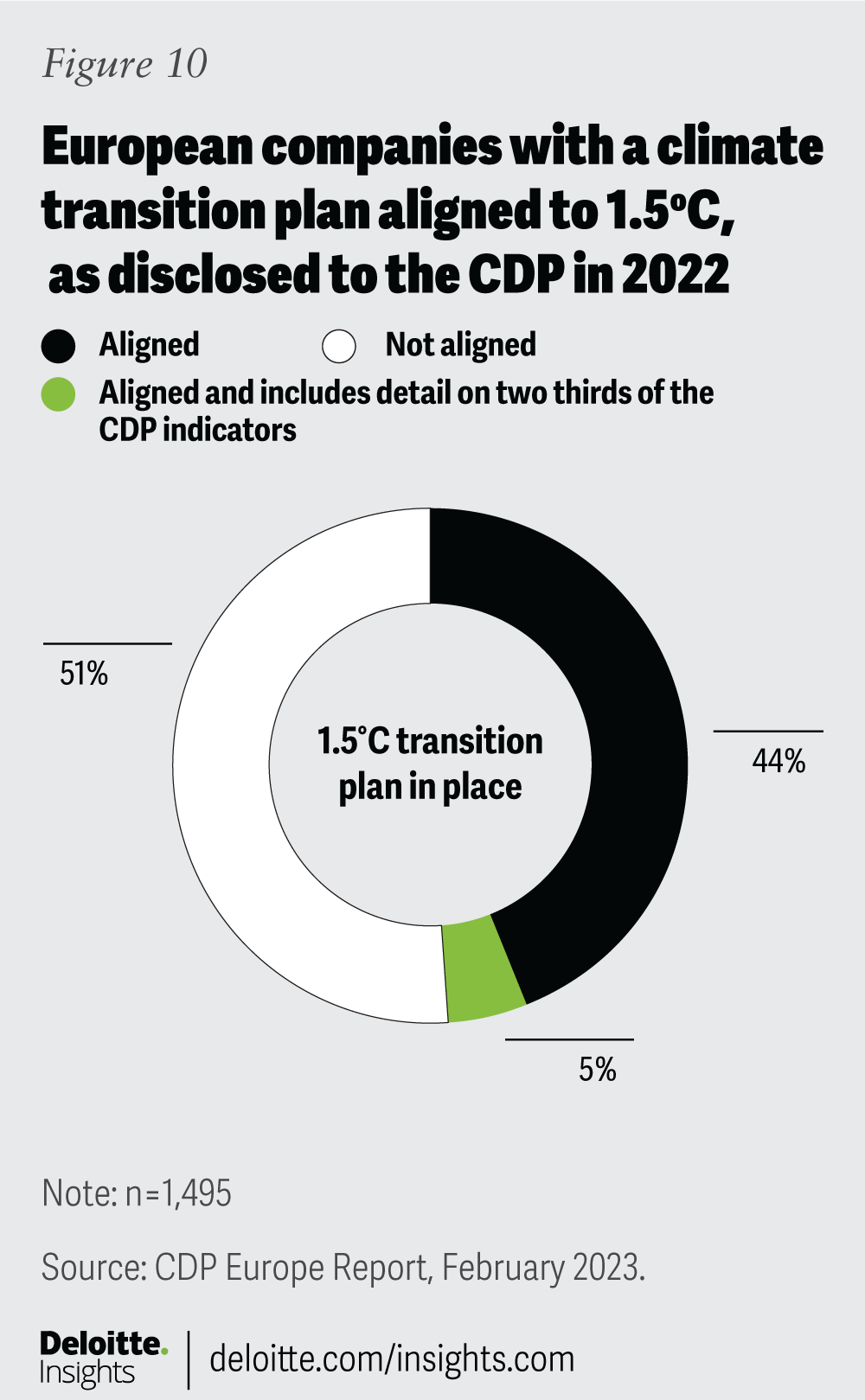

According to data disclosed in 2022 to CDP (a non-profit organisation that runs the global environmental disclosure system for investors, companies, cities, states and regions) from 1,495 mostly publicly listed companies headquartered in Europe, 49% have published a climate transition plan that is aligned with limiting global warming to 1.5 degrees Celsius. However, just 0.5% of these companies reported on all of the CDP’s 21 transition planning indicators and only 5% both reported on two-thirds or more of the indicators and have emissions reduction targets aligned with 1.5 degrees Celsius, leading CDP to conclude that companies still have a way to go to develop and disclose credible transition plans. Companies disclosed the least information on how they plan to implement their transition plan in their business activities and operations. Companies also struggled to publish a description of their engagement across their value chain and their net-zero and emissions reduction targets and progress made towards them.24

Praised for its corporate environmental transparency, a global luxury brand has been recognised as demonstrating best practice on setting and reporting meaningful climate targets. The company devised and now periodically reports on a transition plan that aligns with limiting warming to 1.5 degree Celsius. The transition plan is centred on the company’s commitment to achieving net-zero emissions by 2040 and is underpinned by Scope 1, 2 and 3 emissions targets verified by the SBTi.

To execute the transition plan, the company has reorientated its culture and governance to align with the priorities and objectives set out in its transition plan. The company has established board-level oversight of climate-related issues and has updated both board and management roles and responsibilities. Remuneration and performance objectives have also been updated, and a process for identifying, assessing and responding to climate-related risks and opportunities across the value chain has been integrated into existing risk management.

For further reading on how governance and culture can support the execution of transition plans and how regulators are increasingly focusing on this, please refer to our insights on this topic:

Enhancing governance and culture to support the net zero transition

Building an effective culture to support sustainability-related objectives

Changing consumer sentiment towards sustainability and a busy EU policy agenda on supply chains and circularity will force companies to rethink fundamental aspects of their business strategies and take action to transition from linear to circular economy models.25

Companies will need to focus on increasing the traceability of different nodes in their supply chains and, depending on the strategy they choose, ultimately implement reverse supply chain management systems to ensure products return to vendors or suppliers to be repaired, reused, recycled or remanufactured. This is an immense undertaking for which direction and support from business leaders is critical. However, if executed well it opens up the potential for companies to unlock new revenue streams and reduce costs in the long term. The upcoming regulatory changes relating to supply chains and circularity will act as a catalyst for this transition and provide clarity on how companies can navigate these complexities.

Circular Economy Action Plan (CEAP) initiatives are in full swing.26 During 2023 some of the all-important detail will emerge, together with the long-awaited implementation timelines. Navigating the complexities of the EU regulatory landscape, as well as having a good understanding of the interplay of relevant measures at the EU and national levels, will be crucial for companies operating in the EU or placing their products or services in the EU market.

New product design and performance measures will lead the transition to a circular economy. The EU aims to ensure that sustainable, circular, and non-toxic products and materials become the norm. With the Ecodesign for Sustainable Products Regulation (ESPR), which we expect to be adopted in the second half of 2023, the EU is introducing higher standards for companies in the design and performance of their products, and more detailed information requirements in the form of a Digital Product Passport (DPP).27 A significant amount of often new information will need to be transferred through the entire value chain to fulfil these requirements. The ESPR will be supplemented by legislation targeting specific product categories. Companies can expect that the first targeted regulations will become applicable in late 2024 or early 2025. Priority industries selected by the European Commission, such as batteries and vehicles, electronics and ICT, packaging, plastics, textiles and construction and buildings, are likely to play a crucial role in the roll out of the new requirements to other industries. The new Batteries Regulation, which is likely to gradually enter into force from 2024, outlines the most recent product-specific provisions driving the battery industry towards more circular operations.

In this context, companies should also stay abreast of potential rule changes to Extended Producer Responsibility (EPR) which will require producers to take financial and organisational responsibility for management of the waste stage in a product life cycle. Importantly, EPR rules are often designed for specific product groups and may vary across different Member States. The EU does, however, plan to introduce a harmonised regime for textiles.

The CSDDD is expected to introduce new measures requiring businesses to perform mandatory due diligence checks to identify and account for negative human rights and environmental impacts in the company's own operations, subsidiaries, and downstream value chains. Although the CSDDD is not likely to enter into force until 2026, the current draft bears some similarity to the German Supply Chain Due Diligence Law (SCDD) which came into force on 1 January 2023. The SCDD obliges German-based companies above a certain size to fulfil their human rights and environmental responsibilities throughout their operations and in their global supply chain. Large EU and non-EU companies operating in the EU in priority industries such as textile manufacturing or food production, among others, are likely to fall under the scope of the CSDDD and therefore could benefit from monitoring its implementation in Germany.

The initial actions companies should consider taking are:

“Companies tend to think about waste and pollution as a compliance issue but really it is the ultimate operational inefficiency – you are buying more than you need and have to pay to dispose of the waste that is left over.” – Tensie Whelan, Professor of Business and Society and the Director of the Center for Sustainable Business at NYU Stern School of Business

In 2018 Volvo Cars, a large EU-based automotive company, recognised that the traceability of critical minerals is one of the main challenges linked to sustainability and responsible sourcing faced by carmakers. They hired a tech company which provides traceability solutions using blockchain technology to map supply chains, detect anomalies, provide a verifiable chain of custody, and correctly attribute GHG emissions. Initially, the tech company established comprehensive tracking for all the cobalt used in Volvo’s electric vehicles (EVs). In the years that followed, it extended its tracking to all links in the supply chain and attributed key ESG metrics.

The tech company’s services enabled Volvo to evidence its claims of transparency, traceability, and responsible sourcing, thereby building trust between participants along the supply chain and with its customers. Volvo Cars is now well equipped to meet the upcoming requirements stemming from the new Batteries Regulation and to issue DPPs for its EVs.30

The changing regulatory and supervisory landscape for FS providers will have a significant impact on the cost and availability of financing for companies.

With the renewed sustainable finance strategy EU policymakers aim to mobilise sustainable investments in the transition to a low-carbon economy and mitigate sustainability risks.31 Companies outside the FS sector need to monitor these developments closely to understand the effect on their access to finance, whether from banks or capital markets.

Financial services sector leads the way Banks play a critical role in providing credit to the real economy, whether directly via lending or through their support for capital markets activity. In November 2022 the European Central Bank (ECB) set out its expectations and gave banks an 18-month deadline to formulate their implementation plans and take steps to integrate climate and environmental risk into their strategy, governance, business processes and risk management frameworks. The combination of their own transition plans and enhanced risk management capabilities has made banks pay closer attention to evaluating their climate-related exposures.

This recent ECB study indicates that the banking sector’s exposure to transition risks exceeds that of other security holders or creditor groups.32

Banks look to improve their green credentials

To gain insight into their portfolios, banks are collecting data on climate and environmental risks and monitoring risk indicators, often using available ESG ratings. Just like businesses in other sectors they are required to report and disclose more detail on their carbon footprints, including how green their balance sheets are, and they will look over time to improve their green credentials. Lenders may therefore seek to reduce their carbon emissions (taking into account Scopes 1, 2 and 3) through a combination of credit repricing and exclusion strategies that involve withdrawing from certain sectors or projects. We already see this trend evolving. Examples include thermal coal, oil sands and Arctic drilling projects.

The same trend is evident in other FS sectors. Many of the largest UK insurers, for instance, have announced plans to phase out gradually insurance coverage for certain carbon-intensive industries and projects. To avoid being excluded, companies need to have credible transition plans and be ready to provide them to banks and other FS providers.

Banks are being pressed by supervisors to engage proactively with companies. This will oblige banks to change the way they assess the risk associated with their counterparties, ultimately influencing available products, including revolving credit facilities (RCFs), their pricing, collateral valuations and the terms on which they engage with companies.

ESG factors play a more prominent role in credit rating assessments

In addition, although ‘green factors’ are not formally part of the capital requirements framework yet, banks already have to factor ESG risk into their capital risk assessments. 2023 may also see changes to the way credit rating agencies incorporate ESG factors into their assessments. These developments should benefit companies that are responding to climate change and adapting their business strategies accordingly and disadvantage those that are lagging behind. For example, investment grade companies which lose access to RCFs may not maintain a rating that enables them to issue bonds and this in turn might compromise their access to capital markets.

ESG-labelled funds face imminent reclassifications

In 2023 EU policymakers intend to provide further clarity on the requirements in the SFDR and the EU Taxonomy Regulation affecting FS providers, such as investment managers, pension funds and insurers. Imminent reclassifications of certain ESG-labelled funds may affect the companies these FS firms invest in and change the terms on which they are able to raise equity and/or debt. In the last quarter of 2022 several large asset managers reclassified around EUR 130 bn of SFDR Article 9 products.33

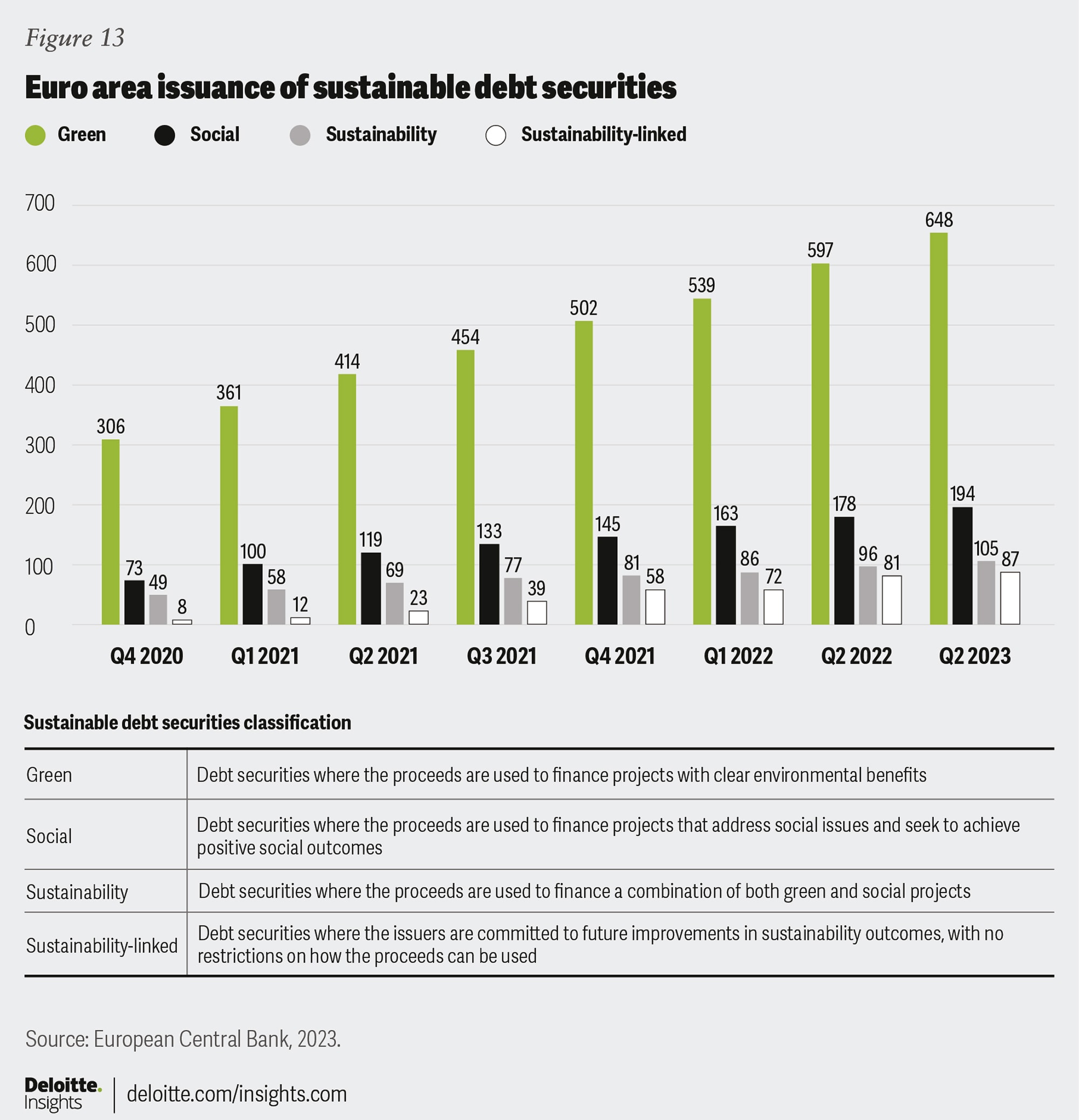

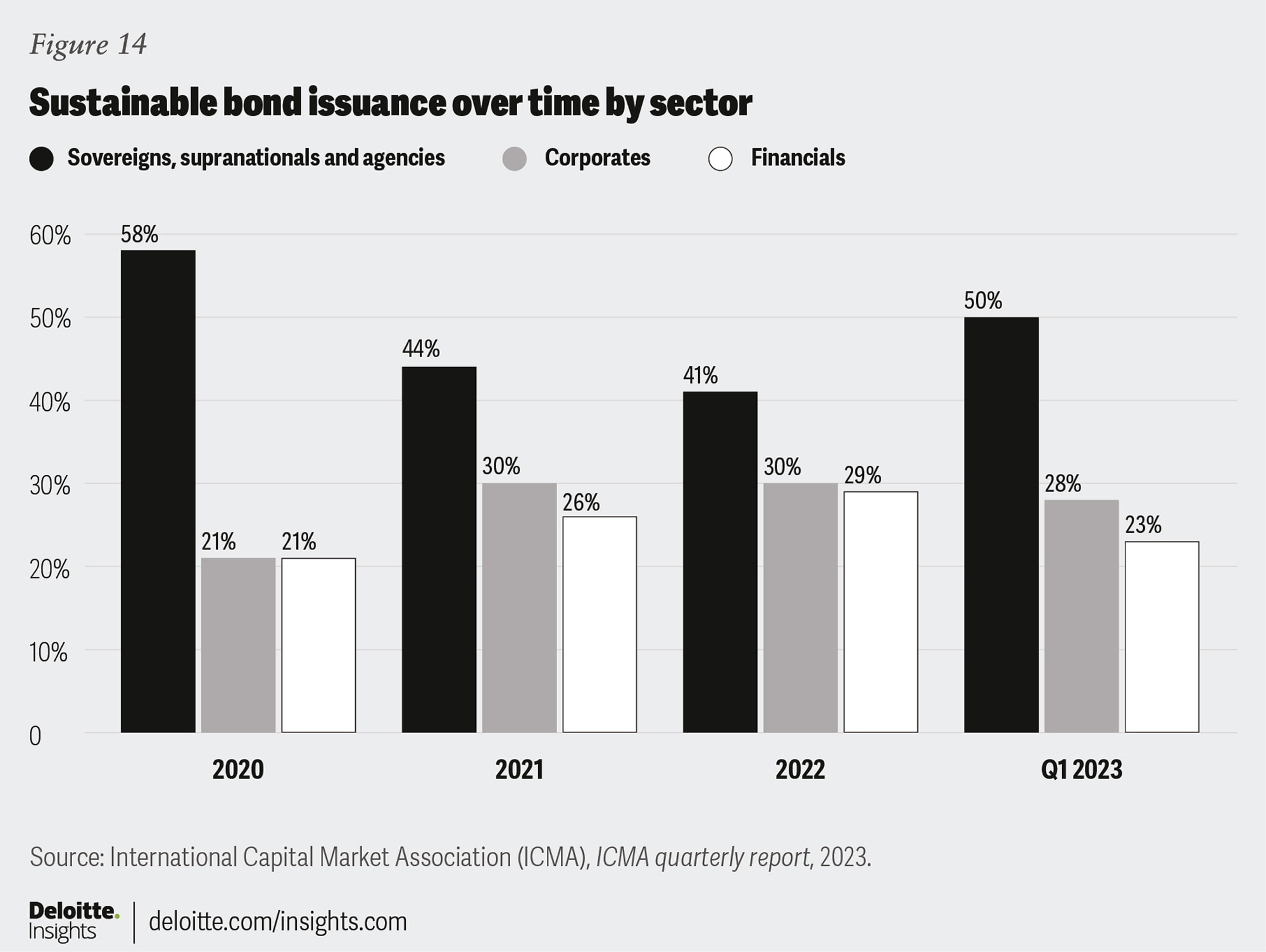

Green bonds attract attention

Although the market for green bonds is still relatively small, it is steadily growing. We see high demand for sustainable debt products among certain asset managers, insurers and pension funds.

The initial actions companies should consider taking are:

CBAM: Carbon Border Adjustment Mechanism

| CBA: Cost Benefit Analysis | CDP: Carbon Disclosure Project |

CEAP: Circular Economy Action Plan | CSDDD: Corporate Sustainability Due Diligence Directive

| CSRD: Corporate Sustainability Reporting Directive |

DPP: Digital Product Passport | ECB: European Central Bank | ESG: Environmental Social Governance

|

ETS: Emissions Trading System

| EPR: Extended Producer Responsibility | EV: Electronic Vehicles |

FS: Financial Services | GHG - Greenhouse Gas | GFANZ: Glasgow Financial Alliance for Net Zero

|

HDT: Heavy Duty Trucks | ICT: Information Communication Technology

| MDT: Medium Duty Trucks |

ISEAL: International Social and Environmental Accreditation | LCA: Life Cycle Assessment | PPA: Power Purchase Agreements

|

SBTi: Science Based Targets Initiative

| SCDD: German Supply Chain Due Diligence | SFDR: Sustainable Finance Disclosure Regulation |

SME: Small to Medium-sized Enterprise | TPT: Transition Plan Taskforce | RCF: Revolving Credit Facilities |

Deloitte, Deloitte 2023 CxO Sustainability Report.

View in ArticleFor information on the Carbon Border Adjustment Mechanism see: Mohammed Chahim, Jose Manueal Fernandes, Valerie Hayer, and Izabel-Helena Kloc, “Carbon border adjustment mechanism as part of the European Green Deal,” Legislative Train Schedule European Parliament, April 20, 2023.

View in ArticleEuropean Commission, Commission Staff Working Document, Impact Assessment Report, Accompanying the document Proposal for a regulation of the European Parliament and of the Council establishing a carbon border adjustment mechanism, July 2022.

View in ArticleInformation on REPowerEU Amendments see: Council of the EU, “EU recovery plan: Provisional agreement reached on REPowerEU,” press release, December 14, 2022; For information on the European Hydrogen Bank see: Legislative Train Schedule European Parliament, “European Hydrogen bank,” April 20, 2023; For information on the EU Green Deal Industrial Plan see: European Commission, A Green Deal industrial plan for the net-zero age.

View in ArticleDominik Ruderer, “Infrastructure Solutions: The power of purchase agreements,” European Investment Bank, Infrastructure Solutions, July 12, 2022.

View in ArticleDeloitte, “Decarbonising Road Freight: Getting into gear,” accessed May 25, 2023.

View in ArticleFor SMSG advice to ESMA on additional questions relating to greenwashing see: European Securities and Markets Authority (ESMA), Advice to ESMA: SMSG advice to ESMA on additional questions relating to greenwashing, March 16, 2023.

View in ArticleRecital 11 to Taxonomy Regulation EU/2020/852 -> Recital 11 to Taxonomy Regulation EU/2020/852 available at Recitals Taxonomy Regulation (lexparency.org)

View in ArticleRecital 7 of Commission Delegated Regulation (EU) 2021/1253 of 21 April 2021 amending the MiFID II Delegated Regulation (EU) 2017/565 -> Recital 7 of Commission Delegated Regulation (EU) 2021/1253 of 21 April 2021 amending the MiFID II Delegated Regulation (EU) 2017/565, available at Recitals Regulation (EU) 2021/1253 (lexparency.org)

View in ArticleStephen Farrell, Dan Furnell, Abi Dahl, James Staight, Greenwashing – Product Development Considerations for Financial Services Firms, Deloitte, May 25, 2021.

View in ArticleEuropean Commission, “Screening of websites for ’greenwashing’: half of green claims lack evidence,” press release, January 28, 2021.

View in ArticleDeloitte, 2022 Climate Check: Business’ views on climate action ahead of COP27, October 2022.

View in ArticleFor information on Directive 2019/2161 see: Daniel Dalton, Directive on better enforcement and modernisation of EU consumer protection rules – a New deal for consumers, Legislative Train Schedule European Parliament, April 20, 2023.

View in ArticleNetherlands Authority for Consumers and Markets, Guidelines Sustainability Claims, accessed May 25, 2023.

View in ArticleDanish Consumer Ombudsman, Quick Guide on environmental claims, December 2021.

View in ArticleFor information on UK Green Claims Code see: Competition and Markets Authority, Green claims code: Making environmental claims, September 20, 2021.

View in ArticleFor information on the Green Claims Directive see: European Commission, “Consumer protection: Enabling sustainable choices and ending greenwashing,” press release, March 22, 2023.

View in ArticleAccording to the European Environment Agency (EEA), life cycle assessment (LCA) is a process of evaluating the effects that a product has on the environment over the entire period of its life thereby increasing resource-use efficiency and decreasing liabilities. It has three key elements: (1) Identify and quantify the environmental loads involved (e.g. the energy and raw materials consumed, the emissions and wastes generated), (2) Evaluate the potential environmental impacts of these loads, and (3) Assess the options available for reducing these environmental impacts. For more on LCA, see: UNEP, “Life cycle assessment,” accessed May 25, 2023.

View in ArticleReZip, Comparative life cycle assessment (LCA), November 2022.

View in ArticleFor information on CSRD see: European Union Law, “Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting,” December 14, 2022.

View in ArticleFor information on ESRS see: European Sustainability Reporting Standards (ESRS), ESRS E1: Climate change, November 2022.

View in ArticleFor information on CSDDD, see: European Commission, “Proposal for a Directive on corporate sustainability due diligence and annex,” February 23, 2022.

View in ArticleEmissions are categorised into Scope 1, Scope 2, and Scope 3 emissions. Scope 1 emissions cover the Green House Gas (GHG) emissions that a company directly makes, e.g., by running heaters or vehicles. Scope 2 emissions are emissions a company makes indirectly, e.g., the source of energy used to run heaters or vehicles. Scope 3 emissions are the emissions the company is indirectly responsible for through its value chain, both upstream and downstream. For more on this, see: Deloitte, “Scope 1, 2 and 3 emissions: What you need to know,” accessed May 25, 2023.

View in ArticleCDP, Stepping Up: Strengthening Europe’s corporate climate transition, February 2023.

View in ArticleAccording to the European Parliament, circular economy is a model of production and consumption which involves sharing, leasing, reusing, repairing, refurbishing, and recycling existing materials and products such that the life cycle of products in extended. For more on the circular economy, see: European Parliament, “Circular economy: Definition, importance and benefits,” news release, accessed May 25, 2023.

View in ArticleFor more information on the Circular Economy Action Plan, see: European Commission, Circular Economy Action Plan: For a cleaner and more competitive Europe, accessed May 25, 2023.

View in ArticleFor more information on Ecodesign for Sustainable Product Regulation, see: European Commission, “Ecodesign for sustainable products,” accessed May 25, 2023.

View in ArticleFor information on the proposal for revision of EU Legislation on Packaging and Packaging Waste, see: European Commission, “Proposal for a revision of EU legislation on Packaging and Packaging Waste,” accessed May 25, 2023.

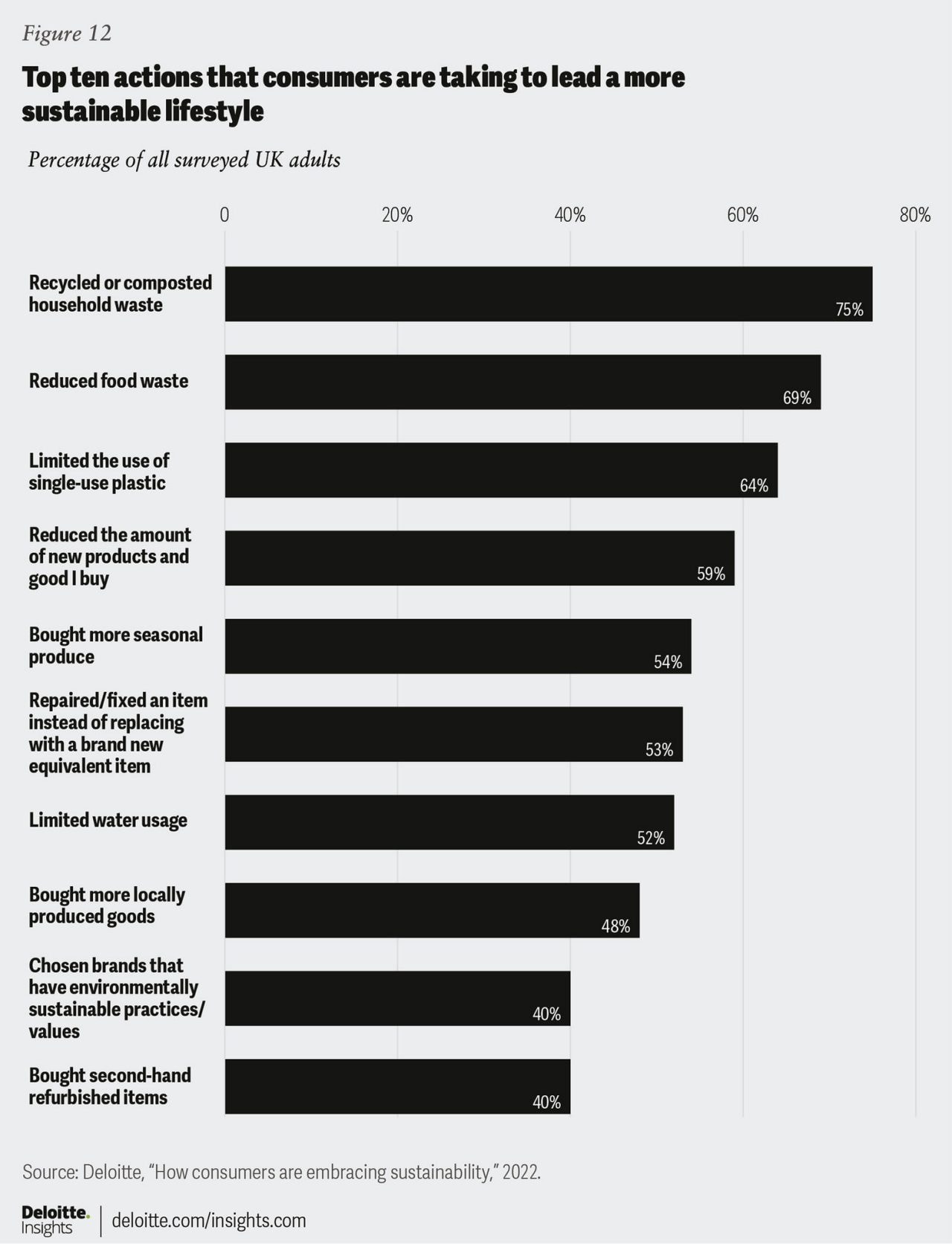

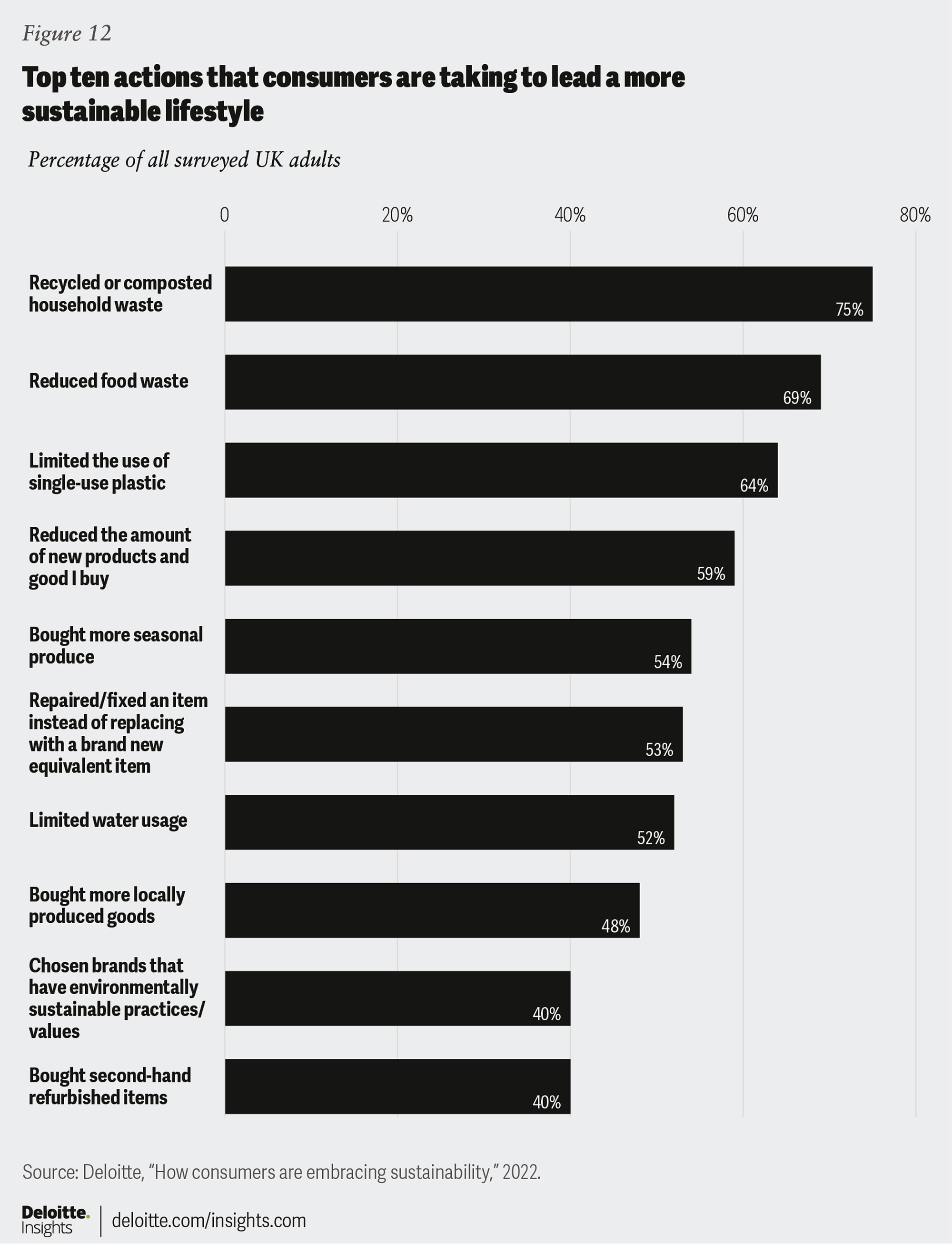

View in ArticleDeloitte, How consumers are embracing sustainability, 2022.

View in ArticleVolvo Cars, “Volvo Cars Tech Fund invests in blockchain technology firm Circulor,” press release, July 8, 2020.

View in ArticleFor information on Strategy for financing the transition to a sustainable economy, see: European Union Law, “Strategy for financing the transition to a sustainable economy,” June 7, 2021.

View in ArticleEuropean Central Bank, “Analytical indicators on carbon emissions," accessed May 25, 2023. available at https://www.ecb.europa.eu/stats/ecb_statistics/sustainability-indicators/data/html/ecb.climate_indicators_carbon_emissions.en.html#_Exposure_to_emission-intensive

View in ArticleESMA, TRV Risk Monitor: ESMA report on trends, risks, and vulnerabilities, No. 1, February 2023.

View in ArticleCover image by: Rovinya Sollitt and Mark Milward