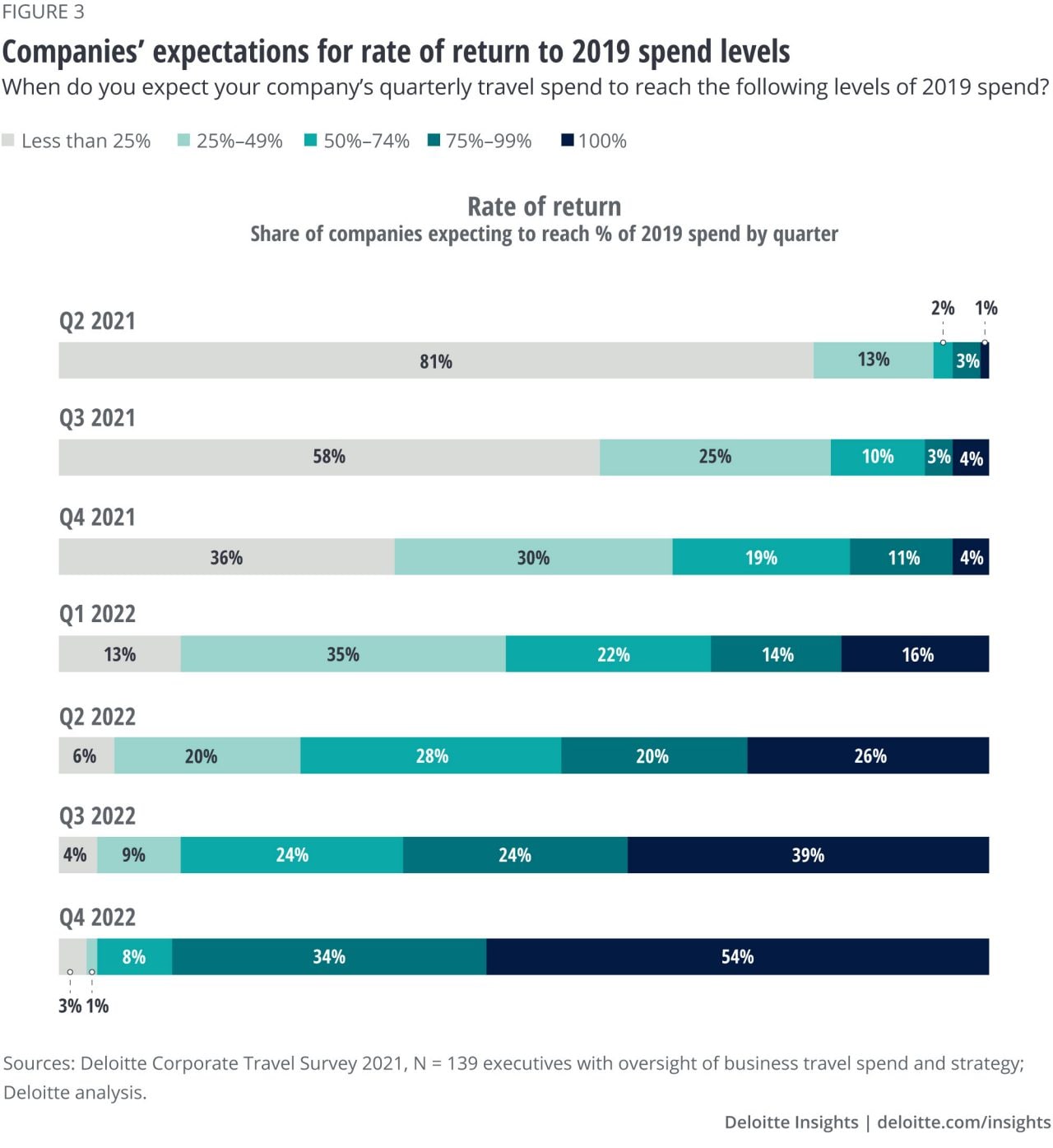

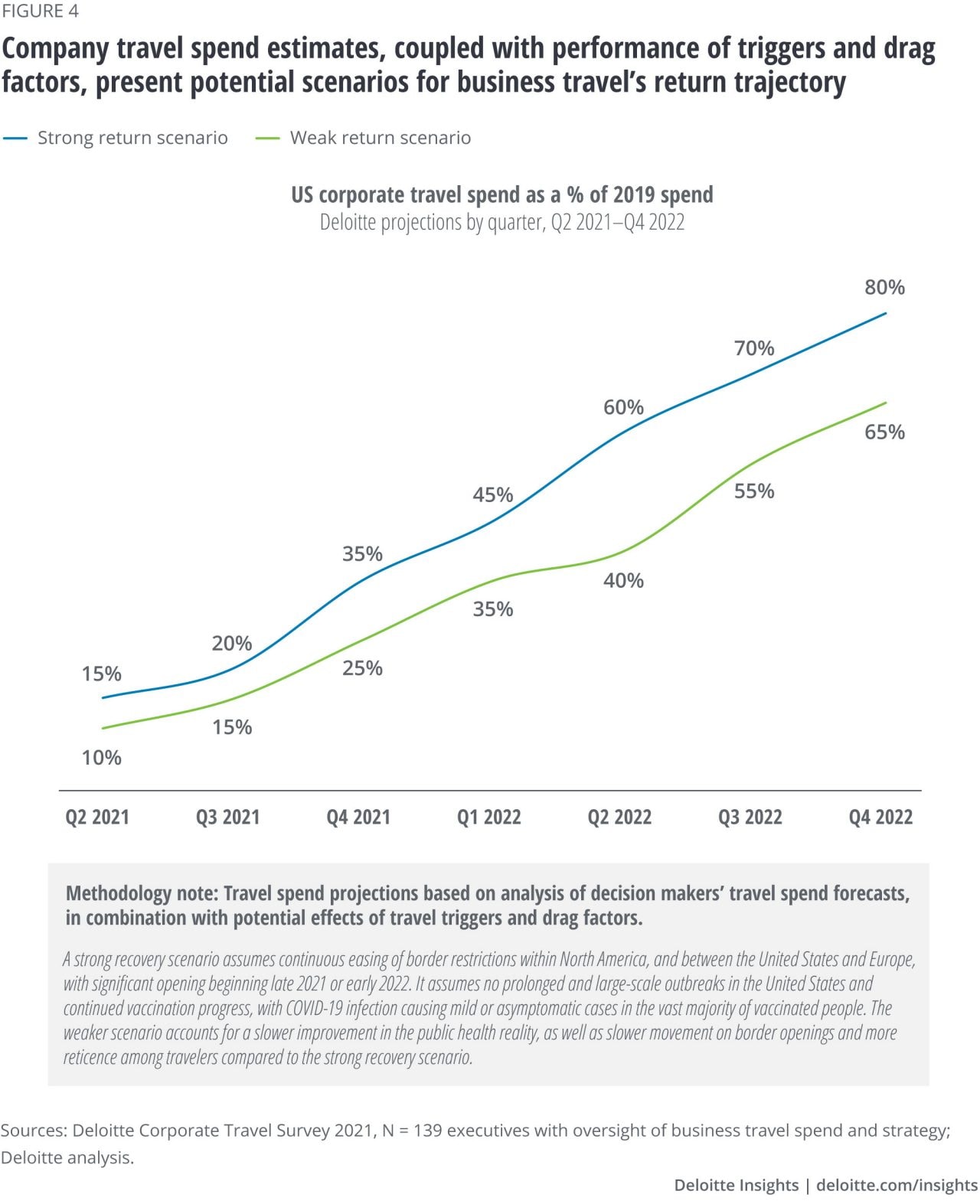

Q2/Q3 2021: Incremental improvement from pandemic lows

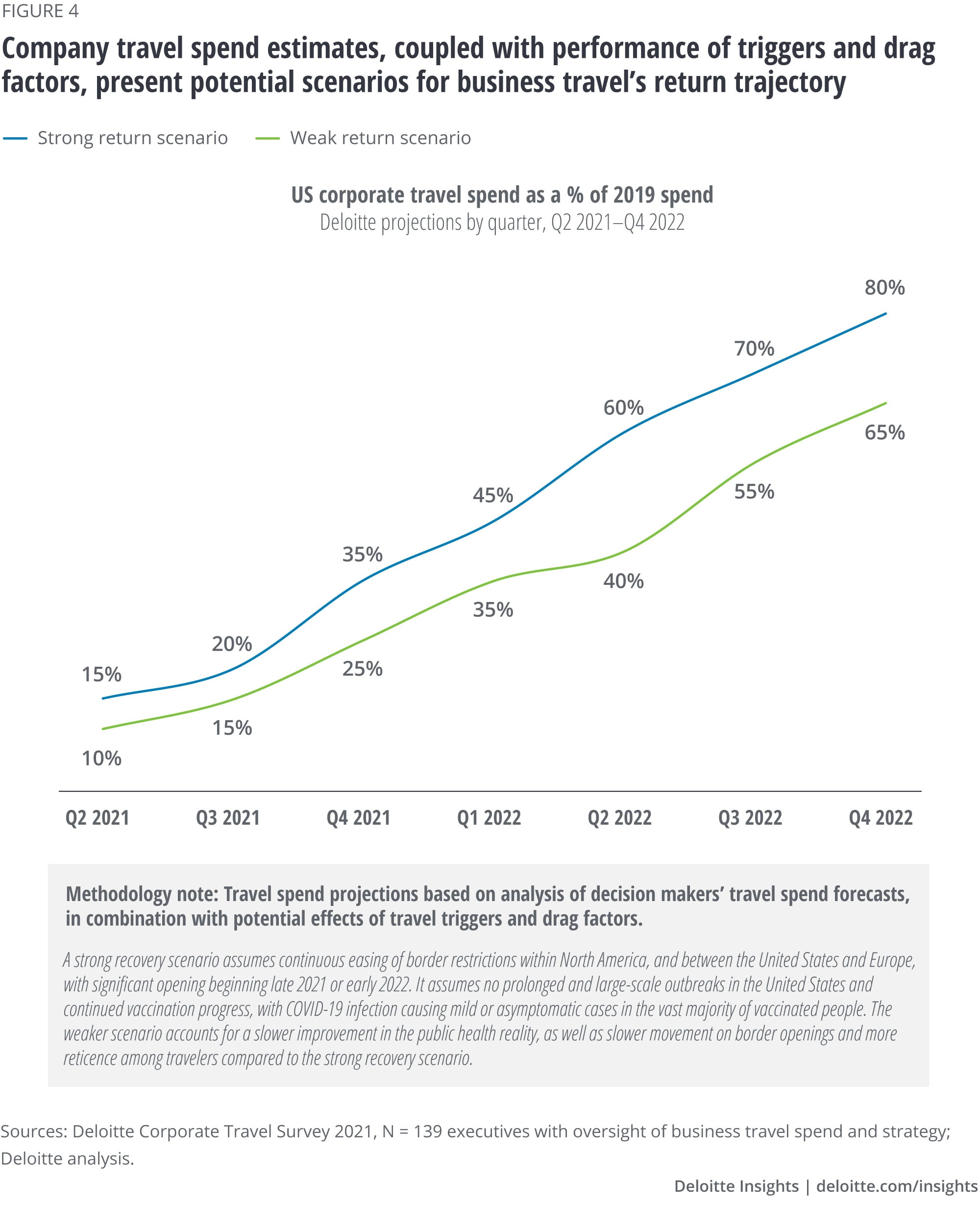

Q2 projected US business travel spend as a share of 2019 spend: 10%–15%

Q3 projected range of US business travel spend as a share of 2019 spend: 15%–20%

Companies have begun to loosen travel restrictions, no longer only allowing essential travel. Nearly all conferences remain virtual, while some trade shows and exhibitions return to a live or hybrid format. Domestic travel has become safer and easier, as states lift quarantine-on-arrival recommendations. As of April 2, the CDC changed its guidance to clear vaccinated people to travel.

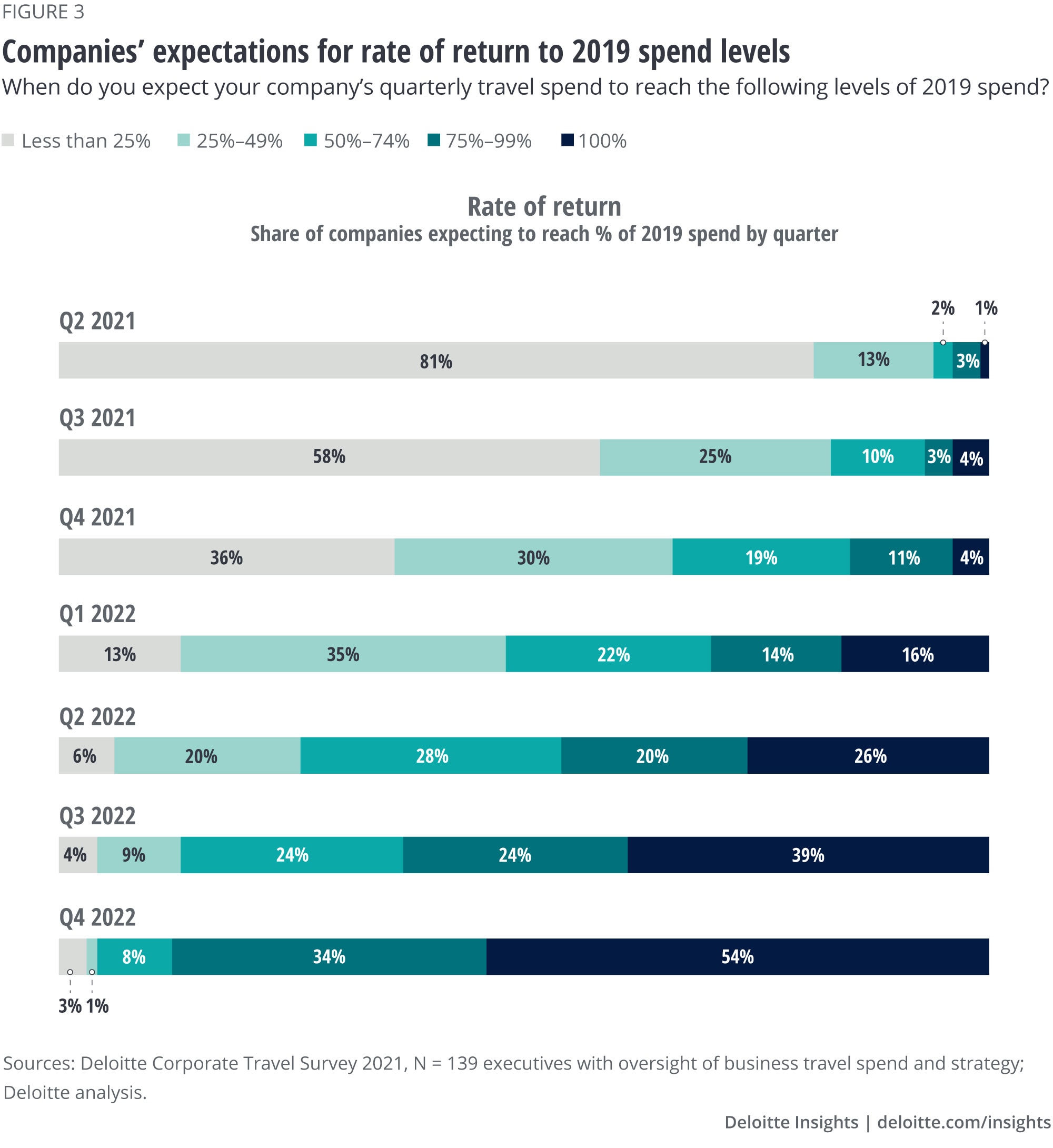

Many companies still require extra layers of approval for corporate trips, and travel volume has only grown slightly from the end of 2020. In Q2, less than a fifth of surveyed companies had reached 25% of 2019 spend. International travel remains all but prohibitive, with quarantine on arrival required in many countries regardless of vaccination status. The vast majority of conferences remain in virtual formats. In Q3, the number of companies expecting to reach at least a quarter of 2019 travel spend doubles, but fewer than one in five expect to reach 50% of 2019 spend. Much of the corporate travel happening in Q2 and Q3 2021 will be at the request of existing clients. Visiting sales prospects remain challenging, as most have yet to return to offices full time.

Q4 2021: Loosening the reins, first forays

Q4 2021 projected range of US business travel spend as a share of 2019 spend: 25%–35%

Many companies plan to significantly accelerate their return to offices in the fall. Travel managers have identified this shift, especially clients’ return to the office, as a top trigger for travel. For workers with children at home, resumption of in-person learning will also make travel more convenient. Higher office usage will enable more meetings, both internal and external. Many conferences will return to a live or hybrid format, but with attendance well below 2019 levels. Still, about a third of surveyed companies say travel spend will remain below 25% of 2019 levels and two-thirds below 50%.

Barriers to international travel could start reducing by this time, easing the quarantine burden of visiting countries in Europe, the Americas, and the Middle East. But corporate travel will remain largely domestic, with international trips limited to essential and client-requested travel.

Q1/Q2 2022: Quiet winter, green shoots in early spring

Q1 2022 projected range of US business travel spend as a share of 2019 spend: 35%–45%

Q2 2022 projected range of US business travel spend as a share of 2019 spend: 40%–60%

With the beginning of what could be the first full year without COVID-19 as a primary daily concern, most companies will remove pandemic-era executive approval requirements for domestic trips. But travel managers rank employee and client resistance to travel and in-person meetings as one of the biggest potential factors to slow the return. This resistance will likely reach its peak as a factor in the winter of 2021–22. Cold and flu season, as well as potential outbreaks of COVID-19 and its variants, will raise concern among potential travelers during a sensitive transition period. This will likely have a dampening effect on the last quarter of 2021 and the first of 2022.

Spring will bring more confidence and more competitive pressure to get in front of clients and prospects. A second season of live and hybrid industry conferences should enjoy better attendance than in fall 2021. Barriers to international travel should continue to come down, but cross-border trips will lag far behind domestic trips. Concerns about the risk and inconvenience of crossing borders will continue to drag down traffic on transatlantic routes, and Asia will remain difficult to visit. International industry events will bring back live formats, but struggle to attract overseas attendees. Additionally, COVID-19 outbreaks that would cause little concern for domestic travelers could result in a higher rate of cancellations for international trips.

Q3/Q4 2022: Approaching the new normal, but still not a full recovery

Q3 2022 projected range of US business travel spend as a share of 2019 spend: 55%–70%

Q4 2022 projected range of US business travel spend as a share of 2019 spend: 65%–80%

If US vaccinations continue to increase, and the vaccines’ effectiveness against major outbreaks and variants proves durable, travel managers expect a big release of pent-up demand in the second half of 2022. More clarity about both the health situation and the ongoing state of office versus remote work will better support both trips planned in advance and last-minute visits to seal deals and execute projects.

International travel will continue to improve, bringing better connectivity with many of the United States’ key trading partners. But much of Asia will still be difficult to visit. Reports suggest the Chinese government has already decided to keep its borders effectively closed through the end of 2022.4 India’s struggle with COVID-195 and Japan’s rocky experience as the Olympics host6 are likely to leave both countries with little political will to accelerate reopening.

Conferences will continue to evolve as organizers work to create formats that maximize return on in-person interaction, while integrating technology to enable virtual participation. The majority of surveyed companies are optimistic that their travel spend will reach 2019 levels by this time—nine in 10 expect to be at or above 75%. Just over half of the respondents expect to return within three years to 2019 spend levels.

By the end of 2022, US corporate travel may near its new normal, the level it will sustain for the next several years. Assuming significantly reduced quarantine on arrival for Europe, the Middle East, and the Americas, and several months of a stable health situation, US corporate travel could reach 80% of 2019 levels. This would represent more than 4x growth from where it stands in summer 2021, and more than 2x growth from the 35% projected for the last quarter of 2021. Still, all of the current barriers to robust corporate travel are complex and those working to remove them face significant challenges. If public health outcomes improve more slowly than expected, and solutions to enable international movement continue to encounter political roadblocks, corporate travel spend by the end of 2022 could be much lower. Reaching just 65% of 2019 spend levels would imply a scenario with still very limited international movement, as well as a stalled return on the domestic side.

Two shades of green: Sustainability and cost imperatives impede corporate travel in 2023 and beyond

Assuming a stable global health situation by the end of 2022, US corporate travel’s new normal will begin to take shape. Companies’ and workers’ approaches to post–COVID-19 travel will be clearer. Borders will likely be more open, though onerous border policies may remain in parts of the world. As the pandemic-related barriers to travel recede, second-order effects will become the more prominent headwinds to corporate travel growth.

While companies recognize that travel is crucial to business success, they will seek to hold onto some of the cost savings brought by the pandemic pause. Controlled travel growth will also contribute to another goal that has grown in importance in corporate America: reducing carbon emissions. Bottom-line and environmental priorities will be supported by technology and behavior changes brought on by more than a year of virtual-only meetings and events. The embrace of tech platforms for meetings and collaboration will mitigate the need for certain trips, and these platforms will continue to evolve to better meet some of the needs that travel used to fill.

Sustainability, budgets challenge full corporate travel return

As the threat of illness, hospitalization, and death from COVID-19 wanes, corporate travel demand will likely begin to bump up against two significant limiting factors: sustainability commitments and cost controls.

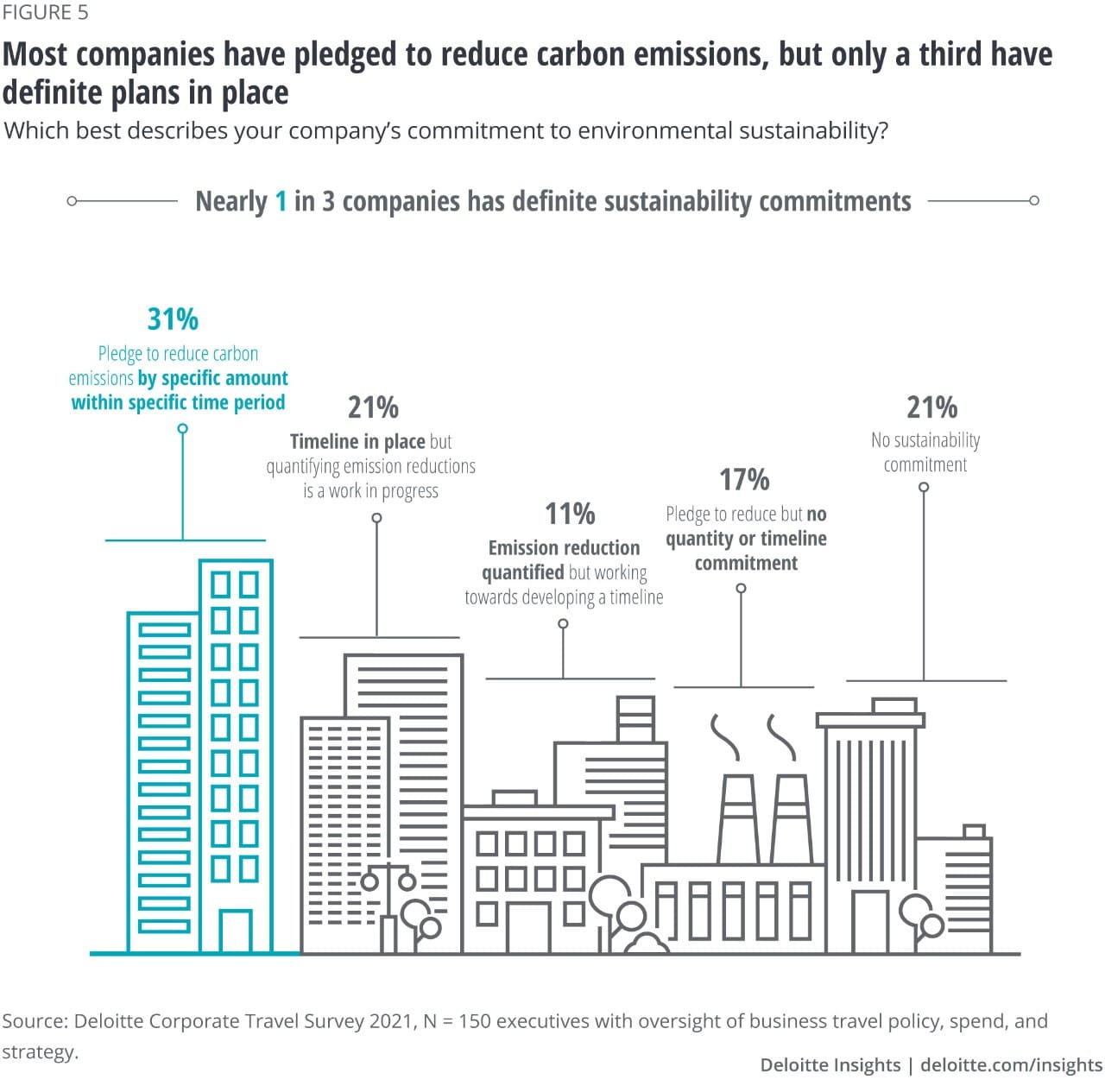

Sustainability has moved into the corporate mainstream, with more than 400 companies signing a pledge at 2021’s Davos World Economic Forum to decarbonize by 2050.7 This number comprises some of the biggest companies in the world, and smaller companies are making similar commitments.

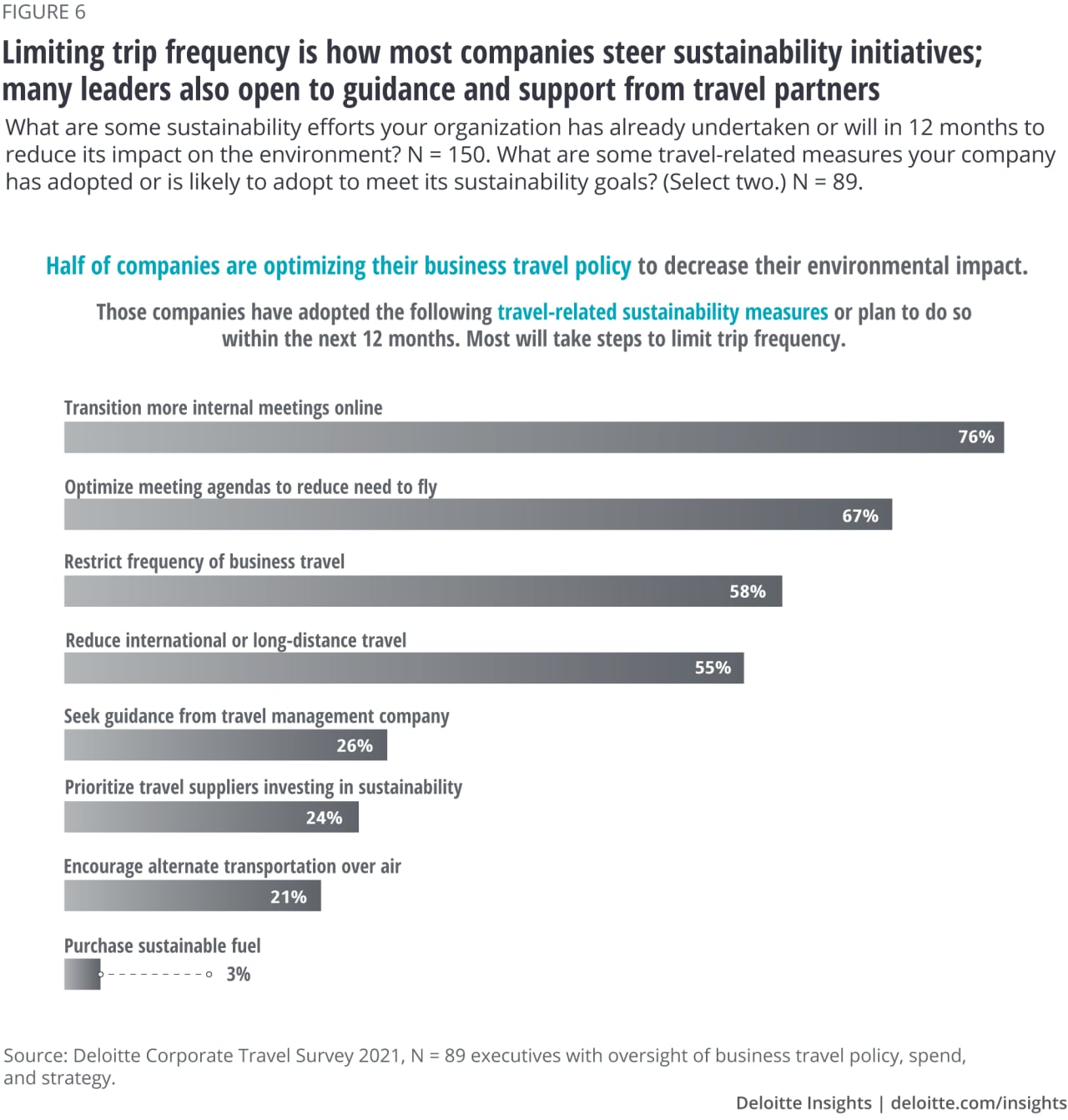

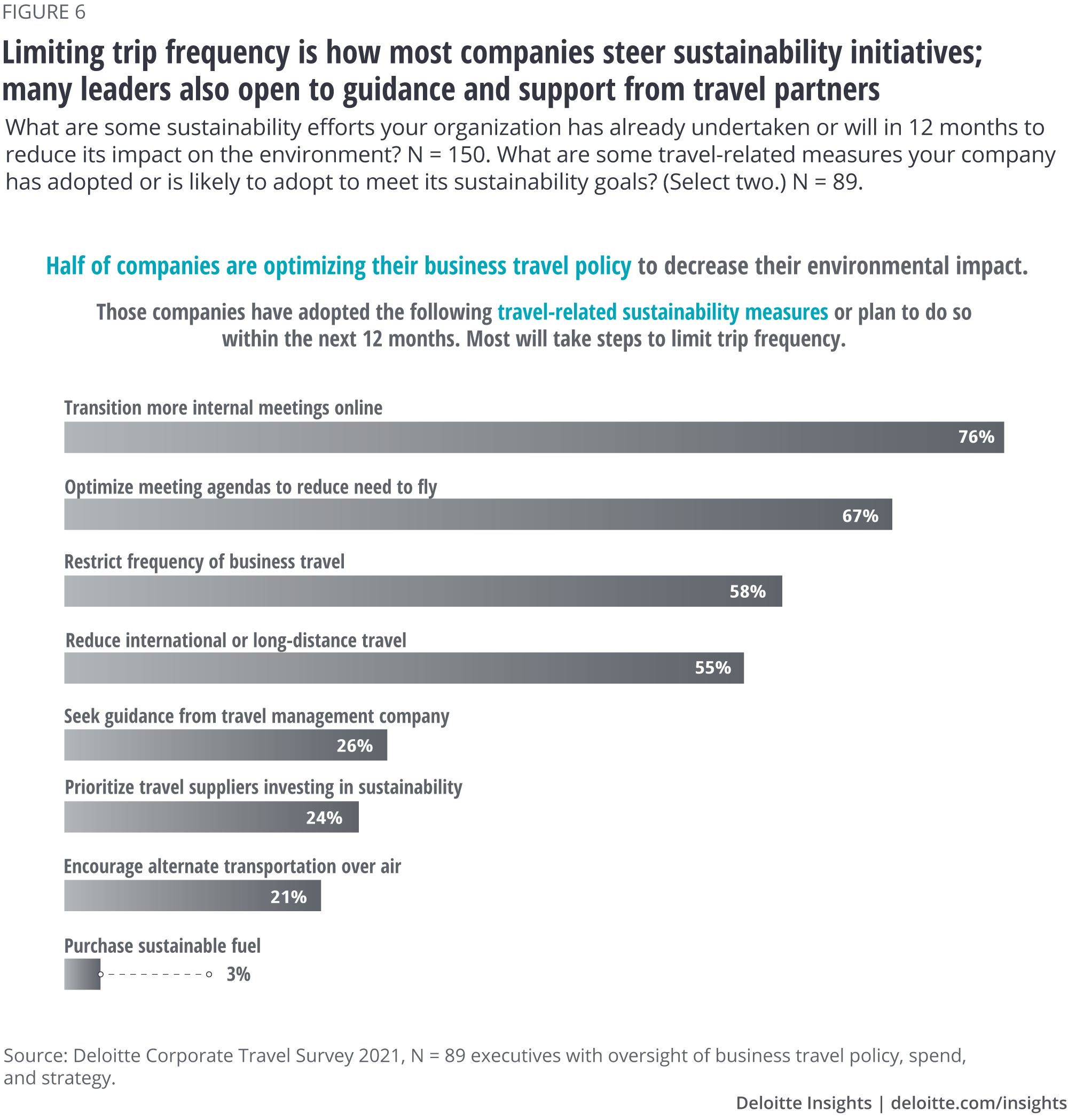

Nearly a third of travel managers surveyed report that their company has a stated commitment to reduce emissions by a certain amount within a specific time frame (figure 5). Altogether, 79% of companies have made some kind of pledge or are working toward one. This interest in sustainability brings some scrutiny for travel policies. About half of survey respondents say that within the next year, they plan to optimize business travel policy to decrease their environmental impact. Travel ranks among the top targets for corporate environmental harm reduction, along with reducing paperwork and greening supply chains.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}