Making ends meet: Innovating and partnering to jumpstart progress

Gleaned from the survey and analysis, following are some ideas developers should consider:

1. Integrating market-rate housing with other residential formats. This could include building nontraditional units such as microunits and coliving developments, which can accommodate two to three times as many households and command higher rent per square foot.9

2. Find ways to reduce materials costs. Developers can focus on manufactured construction techniques or use prefabricated materials, which can often lower materials costs.10

3. Explore alternative products to traditional units. For example, they can convert old motels into affordable housing or develop build-to-rent communities and manage them like a multifamily facility. In California, for instance, the state’s US$800 million Homekey program created the fastest expansion of supportive housing in modern state history. It converted 94 hotel properties into 6,000 new housing units for more than 8,000 people at nearly half the cost per unit for new development.11

4. Partner with municipalities in new ways. Developers should take advantage of incentives, look for opportunities outside of core locations, and continue to work with municipalities to promote projects with mixed-use development and repurposing older assets to include affordable units. Developers can educate municipalities on which incentives and changes in regulations would make it more achievable for them to build housing. Examples include transit-oriented development along key public transit systems and building in nontraditional mixed-use spaces (i.e., residential units above hotel, retail, or life sciences spaces).

5. Partner with other financial services firms and fintechs. Real estate developers can also partner with allies to help solve the housing affordability crisis, including banks or other emerging fintech solutions. These entities could be integral in promoting and offering products specific to affordable projects by providing more favorable terms. For example:

a. Bank of America recently introduced their Community Affordable Loan Solution, offering no down payment and no closing-cost mortgage advances to widen access to homeownership, especially to minority communities.12

b. US Bancorp announced their US$100 billion community benefits plan, increasing mortgage lending units by 20% and increasing investments in community development and affordable housing, among other initiatives.13

c. Home-equity investment providers like Point or HomePace plan to provide nontraditional financing to give buyers better access: fronting money for unattainable down payments in return for a future share in their home’s appreciation. The new owners could then buy back their equity at a later date.14

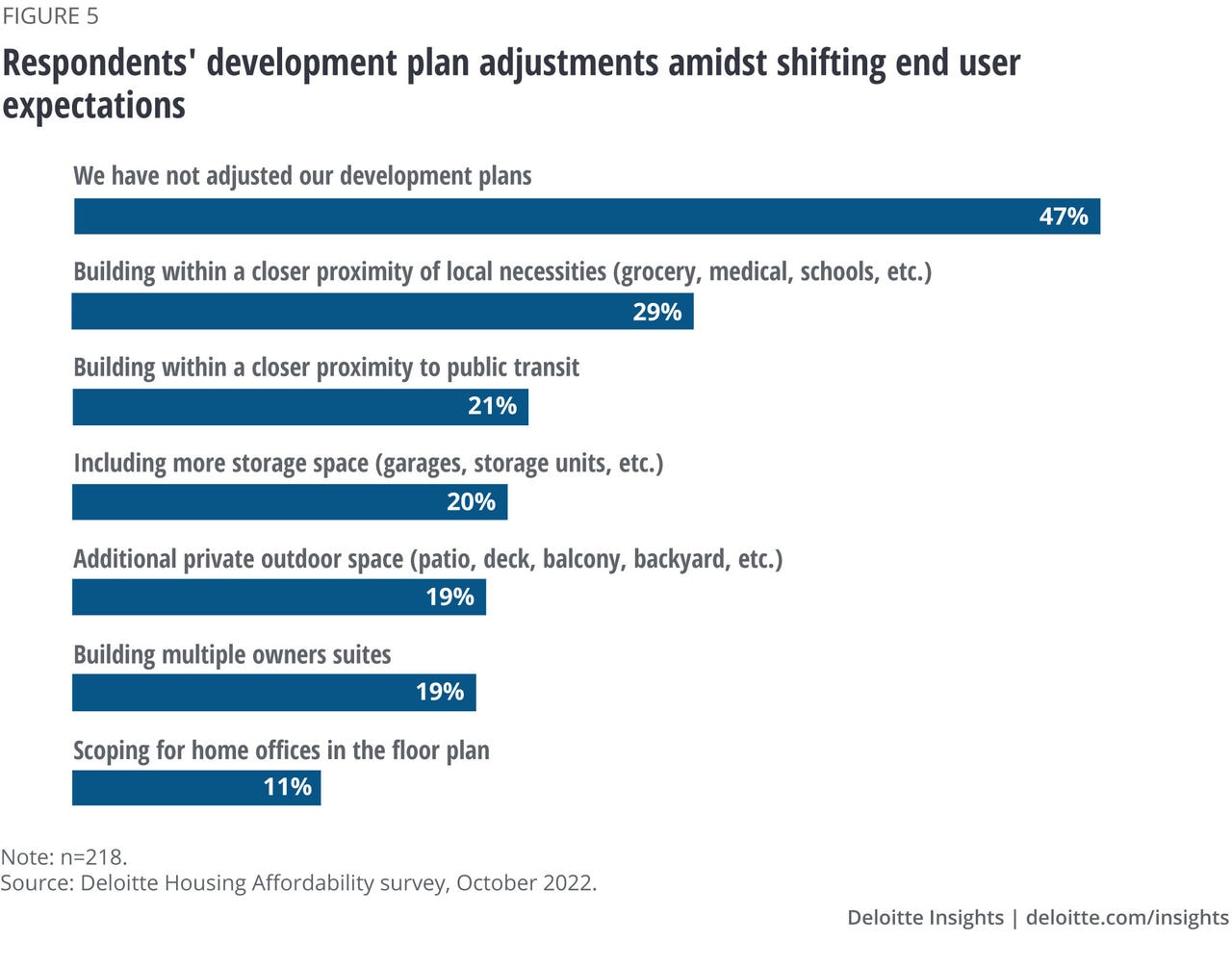

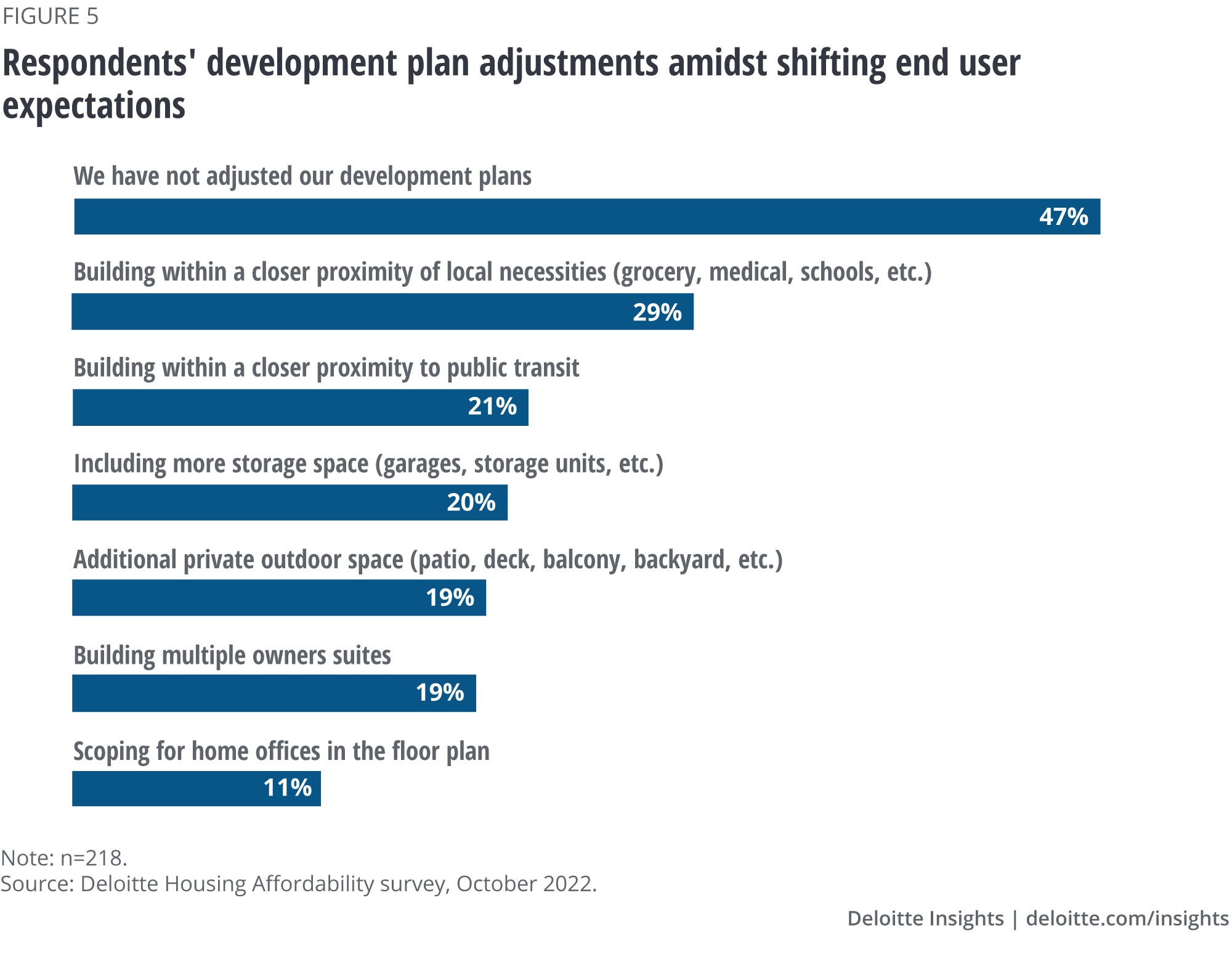

6. Consider end-user expectations. Developers should be mindful of end user expectations as they are seeking out home offices, garages, or space for a pet. Affordable housing occupiers look for different amenities than a market rate occupier such as location to public transit or multigenerational flex spaces (see sidebar).15

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}