2025 banking and capital markets outlook

As the banking industry adapts to a low-growth, lower-rate environment, banks can reinforce their foundation for sustainable growth with ingenuity and discipline.

How—and to what extent—will macroeconomic shifts impact US banks in 2025?

Key messages:

- Macroeconomic and geopolitical uncertainties should keep bank executives on their toes.

- Higher deposit costs will keep net interest income in check.

- Noninterest income could offer a bright spot for topline growth.

- Higher compensation expenses and technology investments should keep expenses elevated.

- Credit quality is expected to normalize but could edge higher in 2025.

Bank executives will be welcoming 2025 with mixed emotions, unsure how the year will unfold and reshape banks’ fortunes. While inflationary pressures have subsided and interest rates are dropping, subpar economic growth, continuing geopolitical shocks, and regulatory uncertainty will likely give bank CEOs anxiety. Adapting to a low-growth, low-rate environment will be a challenge. But many will be happy to close the chapter on 2024, a year that was remarkable in many respects.

The US economy will likely have performed better than expected in 2024, with annual GDP growth estimated to end at 2.7%,1 higher than forecast at the beginning of the year.2

However, in 2025, economic growth is expected to decelerate and interest rates to drop meaningfully. Deloitte’s latest United States economic forecast anticipates a soft landing, with US GDP likely to grow at 1.5% in its baseline scenario.3 Moderating consumer spending, a rising unemployment rate, and weak business investment could dampen growth. If technology adoption significantly boosts labor productivity, GDP growth may end up being a bit more positive at 1.9%. Although a recession seems unlikely, there is a small probability that GDP could grow at only 1.0%, if inflation remains stubbornly high and worsening geopolitical conflicts lead to increased sanctions and trade tariffs.4

The strength of the American consumer will be tested in 2025. Consumer spending could fall as consumer debt weighs on finances. Total consumer debt is now at an all-time high and has shot up to US$17.7 trillion as of second quarter 2024.5 This is happening when aggregate savings are also declining: The latest estimates suggest that pandemic-era excess savings were fully depleted by March 2024.6 Similarly, companies’ balance sheets may be less robust, as a result of declining cash positions and higher levels of debt maturity.7

In most scenarios, inflation should not be a pressing concern entering 2025. The Consumer Price Index is expected to get closer to the 2% target rate,8 possibly leading to another three or four rate cuts in 2025, which would bring the effective federal funds rate to between 350 and 375 basis points.9 As a result of lower inflation and declining rates, treasury yields should also drop, with short-term yields potentially falling faster than the 10-year yields. After nearly two-and-a-half years, the inverted yield curve should flatten and possibly revert to the normal upward sloping curve, where long-term yields are above short-term yields.

Similarly, as inflation comes down, central banks around the world will likely be tweaking their monetary policies and dropping their benchmark rates. For instance, the European Central Bank is expected to lower the interest rate to 2.75% by the end of 2025.10 The Bank of England and the Bank of Canada should also follow suit. The Bank of Japan, on other hand, may not have as much wiggle room, in striking a balance between inflation and growth, after a prolonged period of deflation. Overall, though, in the near term, a temporary divergence in rate movements across the major economies in 2025 can be expected.

Thriving in a low-growth, lower-rate macroeconomic environment will be a challenge

Banks’ most fundamental challenge will be attaining sustainable growth despite these macroeconomic headwinds. Bank leaders will need to make some tough choices to achieve this goal.

Net interest income in 2025 for the US banking industry should decline as deposit costs remain relatively high, per Deloitte’s estimates. As interest rates drop, banks may have to revisit their interest income strategies.

Loan demand is expected to improve, particularly for mortgages, as rates drop and demand increases. But credit card debt and auto loans may experience sluggish growth as consumers face greater financial pressures. In addition, the uncertainty around the interest rate trajectory could prompt some consumers to hold off on making big-ticket purchases, which could challenge banks’ consumer loan volumes. Meanwhile, corporate borrowing is expected to remain stable, but there could be an uptick in debt issuance and M&A, if macroeconomic and political uncertainty subsides.

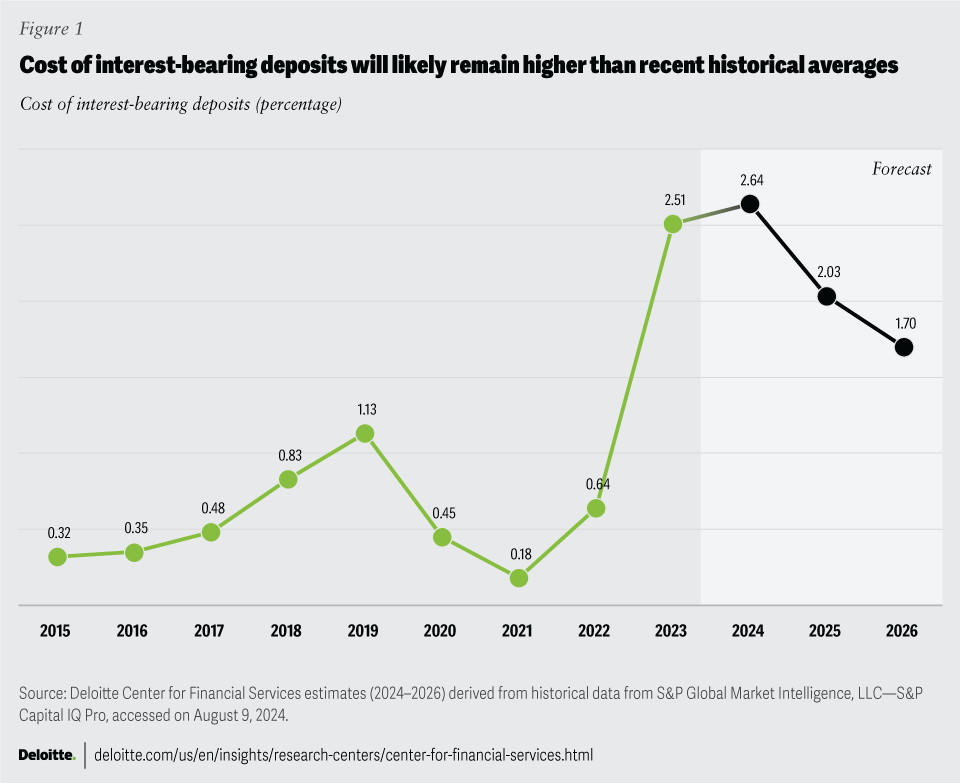

As for deposits, even as rates drop, the cost of funding may not decrease commensurately. According to Deloitte’s analysis, deposit betas will likely be less than in a typical downward rate cycle. Primarily, this is because the demand for liquidity from banks, and the reluctance from depositors to accept lower deposit rates, could continue to fuel the war for deposits. Although the deposit mix—between interest-bearing and noninterest-bearing deposits—might stabilize, and the aggregate deposit costs will likely be lower than at the end of 2024, deposit costs are estimated to be elevated at 2.03% in 2025 (figure 1), higher than the previous five-year average of 0.9%.11 At some banks, asset and liability management committees will be challenged to maintain the optimal balance between loan and deposit rates.

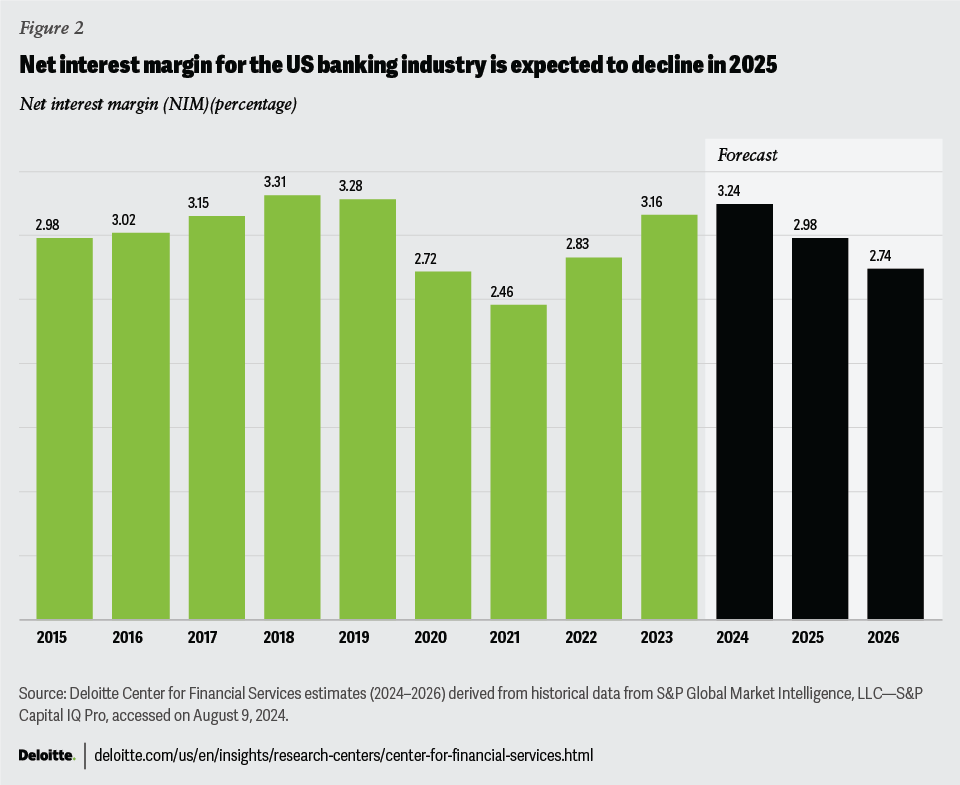

As a consequence, the industry may see a noticeable dip in net interest margin, settling in at around 3% by the end of 2025 (figure 2).12

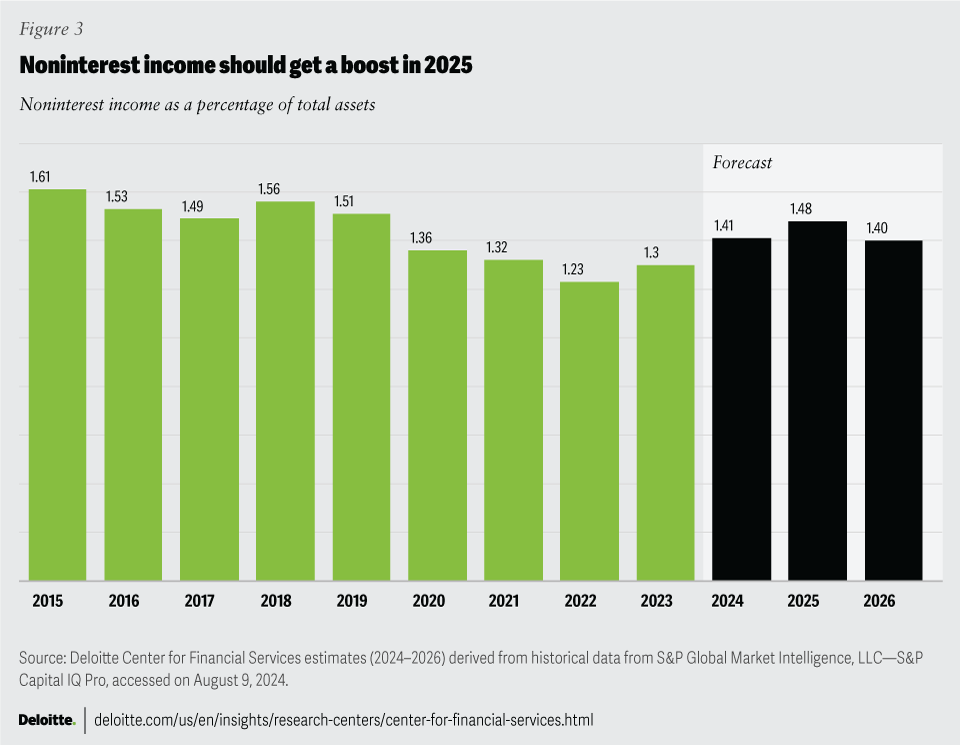

Other income from securities investments could be slightly higher as asset prices increase. Banks’ securities portfolios may improve with yields gradually coming down. But the bright spot should be investment banking fees, as M&A and issuance activities continue to grow. Asset management fees could also see an overall uptick. The lower rate environment could also lead to higher refinancing fees for many banks. Overall, noninterest income as a percentage of average assets is estimated to increase to nearly 1.5%, based on Deloitte estimates, the highest in the last five years (figure 3).13

Banks have had to deal with a surge in costs from higher compensation expenses and investments in technology, along with inflation. Growing noninterest income should also lead to higher compensation expenses in the form of incentives and performance bonuses. Overall, expenses are expected to remain higher in part because banks will need to prioritize tech modernization and retaining high-quality talent.

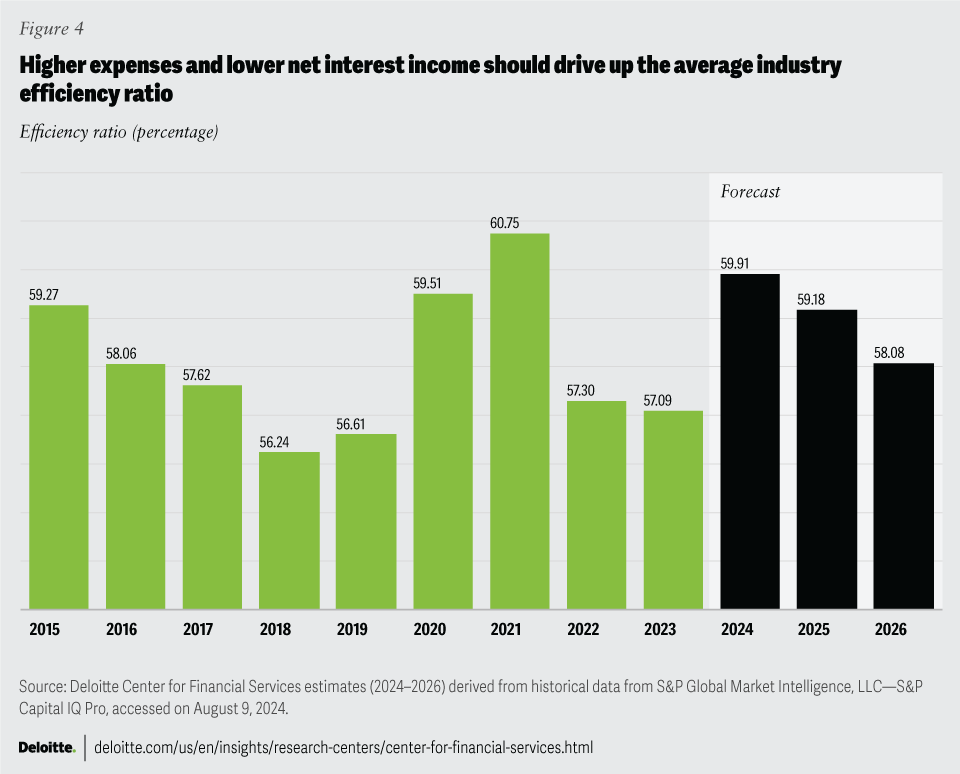

Consequently, the industry’s average efficiency ratio may hover around 60% in 2025 (figure 4).14 Expense management will be a major priority; banks will need to focus on pulling the right levers to keep costs under control and, at the same time, help pave the way for sustainable growth.

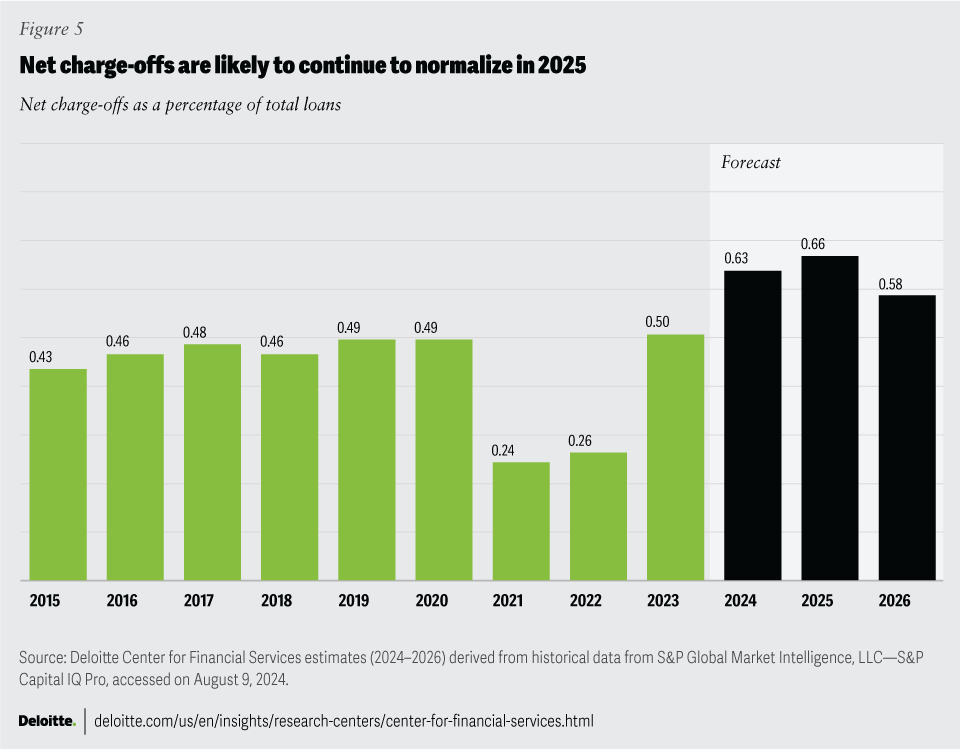

Credit quality overall is expected to return to normal, with delinquencies and net charge-offs increasing modestly from 2024 levels. While lower rates may boost demand for mortgages, credit losses in consumer loans could be a sore point in 2025. Delinquencies will likely rise in credit card and auto loans as consumers’ balance sheets weaken. Credit card loans have the highest 90+ day delinquency rate among all loan categories (1.69% as of second quarter 2024), and the highest net charge-off rates (4% as of second quarter 2024).15 Still, they are much lower than what they were in the aftermath of the 2008 financial crisis.

The commercial real estate (CRE) sector, particularly the office segment, continues to remain in distress, with regional banks possibly facing the brunt of potential loan losses. Some banks may opt to continue reducing their exposure to troubled CRE assets and reposition their balance sheets.

As a result, the overall net charge-off rate is expected to reach 0.66% in 2025 (figure 5), the highest in the last decade but significantly lower than the 2008–2009 crisis (2.6%).16

Large, diversified banks will likely perform better

Overall, in 2025, diversified banks could have an advantage from multiple revenue streams. Some large banks may reduce deposit rates in line with rate declines; their stronger brand presence and higher liquidity could provide them with a buffer to remain attractive and competitive. Midsize and regional banks could face tougher competition in modifying deposit rates. The cost of interest-bearing deposits remains high for such banks at 3.15% as of second quarter 2024.17 Deposit betas are expected to be low for them when rates decline.

Meanwhile, credit card firms could especially benefit from rising credit card loans. Other payments firms will likely see modest or flat growth in revenues. But they face the prospect of rising delinquencies.

Banks focused on capital market activities could also see stronger performance but also higher compensation expenses.

Larger banks (global systemically important banks and super regionals) already have greater buffers to manage through loan losses. A few midsize and regional banks could face a tougher environment due to concentrated exposures to sectors like office space real estate. In fact, banks with assets between US$10 billion to US$100 billion have the highest CRE loans as a percentage of risk-based capital (199% as of second quarter 2024).18 This is in stark contrast to banks with assets of more than US$250 billion (54% as of second quarter 2024).

Global perspectives

In Europe and Asia, rates are expected to come down as inflation cools off. But slower economic growth will impact banks’ prospects. Many European banks could find it hard to adjust to a low-rate environment, and their profitability will likely suffer more than banks elsewhere.19 The stronger European investment banks will look to challenge US banks’ dominance in dealmaking and issuance activities.20 In the Asia-Pacific region, banks operating in high-growth emerging markets should experience stronger results. However, central banks’ timing in cutting rates across these countries will likely test banks’ resilience and growth potential.

Strengthening the foundation to achieve growth

Banks will have to contend with a more challenging set of macroeconomic conditions in 2025: While the interest rates will be lower, the economy may grow at only a modest pace, and there should be normalization of the credit cycle. The exact configuration of these outcomes may not be crystal clear at this point, but no matter the scenario, banks should be adaptive and respond quickly to the pace of change.

Many banks will be looking to recalibrate their business models. On the positive side, banks may improve their profitability by reducing excess capital, which they may have accumulated in preparation for stricter capital requirements. But they will need to be creative and find ways to boost noninterest income, shed technical debt so they can realize the promise of becoming an AI-powered bank, and exhibit a new discipline around cost management.

In addition to the question of how banks should respond to macroeconomic forces, answering the four questions below could strengthen their foundation for sustainable growth:

- How could the Basel III Endgame re-proposal impact the banking industry?

- What actions can banks take in 2025 to boost noninterest income?

- Will the promise of an AI-powered bank accelerate tech modernization?

- Why are banks’ efforts to manage costs typically unsustainable, and what should they do about it?

In the following chapters, we address these questions in detail and offer some guidance on how banks can prepare for 2025.

How could the Basel III Endgame re-proposal impact the banking industry?

Key messages:

- The Basel III Endgame re-proposal suggests lower capital requirements than the original proposal; however, these rules have not yet been finalized.

- Banks are likely to continue decreasing their excess capital to optimize their balance sheets, as well as engage in financial transactions to reduce capital needs.

- The likelihood of bank M&A may increase among banks with less than US$250 billion in assets.

- Other countries are adopting their own Basel III requirements, which may impact bank competitiveness around the world.

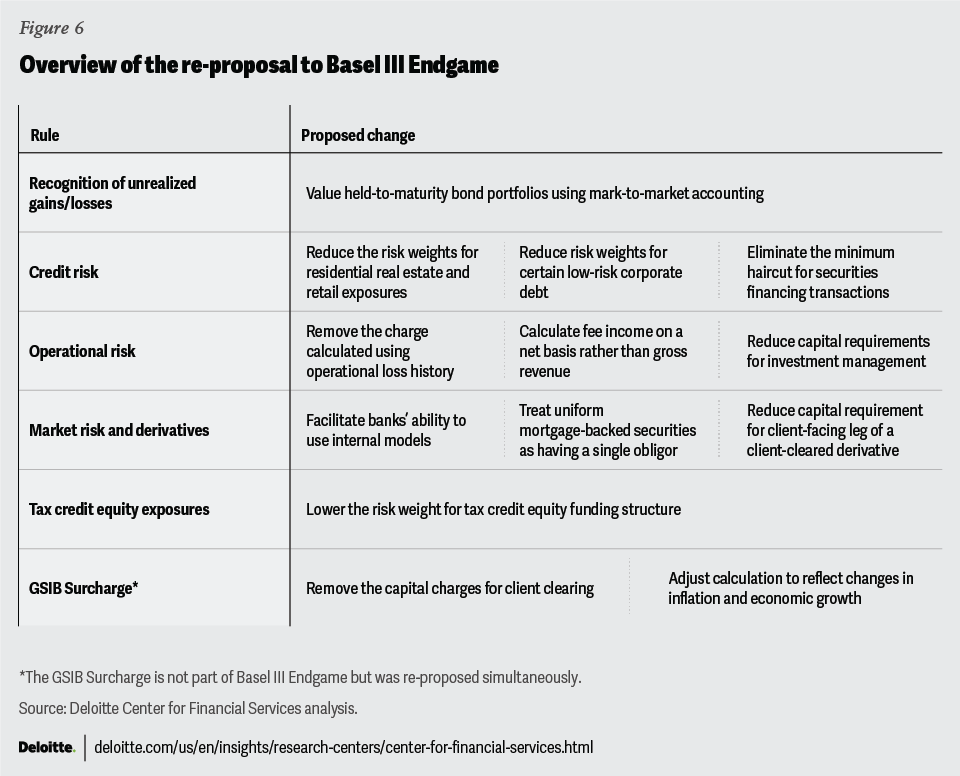

The re-proposal of the Basel III Endgame, released in fall 2024, would lower banks’ capital requirements compared to the proposal released in 2023. Although the largest banks could still face stricter capital constraints, banks in general are expected to perform better due to relaxed regulatory rules and reduced uncertainty.

In a speech delivered on September 10, Federal Reserve Vice Chair Michael Barr outlined “key broad and material changes to the original proposal” that he will recommend to the Federal Reserve Board.21 These changes are collectively estimated to result in a 9% increase in common equity tier 1 for global systemically important banks (GSIBs). Another significant change would be the retention of the tiering approach to regulation, which tailors regulatory standards to the size of the bank. As a result, GSIBs and banks with more than US$250 billion in assets will face stricter capital rules compared to banks with assets between US$100 billion and US$250 billion, known as Category IV banks. Some other important takeaways include:

Overall, the proposed changes remove potential negative impacts on many US banks’ business models. The re-proposal eliminates some of the stricter standards, known as “gold-plating,” which were higher than those recommended by the Basel Committee.

Although the newly proposed rules are less stringent than the original rules, further changes are still possible. After the Federal Reserve releases the rules, there will be a 60-day comment period. The revisions are supposed to be jointly agreed upon with the Federal Deposit Insurance Corporation (FDIC) and Office of the Comptroller of the Currency (OCC), which have yet to vote on them.22

Additionally, some members of Congress have suggested they might intervene through the Congressional Review Act.23 The situation remains dynamic, so banks will want to closely monitor developments.

Optimizing capital for new regulatory standards

There are signs that banks are already preparing their balance sheets for the re-proposal of capital requirements. Banks are redeeming preferred shares to reduce capital and boost return on equity.24 Over the past several years, banks accumulated a capital surplus in preparation for stricter capital rules. Now, bank executives are reducing this excess capital to improve financial performance through measures such as share buybacks.

The timing of the re-proposal could be advantageous as banks face increased lending competition from nonbank financial institutions. Increased capital requirements raise the cost of lending for banks, which are adapting to the growth of private credit.25

Executing financial arrangements to reduce capital needs

In addition to reducing excess capital, banks are engaging in methods to lower overall capital retention. The Basel III Endgame rules are expected to further encourage banks to engage in more credit risk transfers (CRTs). Banks with assets exceeding US$250 billion have the strongest incentives to pursue these types of transactions due to higher capital requirements.

Many banks have already recognized the benefits of these transactions. Regional US banks, such as Huntington Bancshares and Ally Financial, have explored CRT deals allowing them to reduce risk-weighted assets and thereby recycle capital more quickly.26

Banks are also entering into forward-flow arrangements. These partnerships allow banks to maintain ownership of the customer relationship while transferring interest payments and credit risk to private credit firms. For instance, KeyCorp has arranged a deal to transfer its card portfolio to an alternative asset manager.27

Recalibrating the deal calculus to scale strategically

The Basel III Endgame re-proposal may have less impact on bank M&A across the industry than originally envisioned. However, since the re-proposed rules primarily target banks with assets over US$250 billion, Category IV and midsize banks with less than US$100 billion in assets may still be likely to engage in dealmaking.

For these banks, achieving scale remains a fundamental driver of the deal calculus. But the focus is likely to shift away from achieving economies of scale to reduce regulatory costs associated with becoming a bank with more than US$100 billion in assets. Instead, banks might emphasize diversifying their portfolios, expanding into new markets, and acquiring low-cost, stable deposits.

Global considerations

The Basel III Endgame will likely have a large impact on banks across various jurisdictions, including the United Kingdom and the European Union, where it is referred to as Basel 3.1. Although the Basel Committee’s recommendations are intended to serve as internationally agreed-upon minimum standards, individual regulators have the discretion to diverge from and exceed these standards within their respective countries’ regulations. In fact, some commentators have noted that this discretion can lead to a “race to the bottom,” where regulators might weaken their rules to remain competitive.28

The Federal Reserve’s re-proposal may prompt other regulators to delay and soften their own rules. For instance, the United Kingdom, which originally set July 2025 as its implementation date (the same as the former US implementation date), has now postponed it to January 2026.29 The Prudential Regulatory Authority (PRA), the UK’s banking regulator, announced revisions in September that would have less than a 1% impact on capital requirements, which is less stringent than originally proposed.30 Importantly, the PRA stressed that these rules would align with global standards. Similarly, the EU Commission has stressed the need for “an international level-playing field” for banks, signaling that it might also weaken its rules if other jurisdictions are perceived as less stringent.31

Banks may want to reconsider their global strategies as different jurisdictions finalize their regulatory rules. Furthermore, some banks may not be optimally structured, which can limit their efficient use of capital.32 For example, banks may find opportunities to book business in different jurisdictions to better enhance their capital utilization.

What actions can banks take in 2025 to boost noninterest income?

Key messages:

- Banks should focus more on boosting noninterest income to compensate for challenges in growing net interest income.

- Using the following strategies may help banks achieve this goal.

- Retail banking: Implementing pricing innovations like service bundling and tiered accounts.

- Payments: Increasing transaction volumes via new channels and expanding value-added services.

- Wealth management: Emphasizing the value of personalized advice, enhancing the customer experience, and revising fee structures.

As discussed earlier, banks’ net interest income will likely face pressure in 2025; deposit costs are expected to remain elevated despite rates coming down. As a result, banks may want to prioritize boosting noninterest income.

For more than 20 years, many banks have worked to diversify revenue through noninterest income.33 However, their success has varied.

The proportion of noninterest income to total income for the US banking industry in the last 10+ years has averaged 35%, with very low overall growth.34 That said, noninterest income product lines require minimal capital and tend to be more profitable than business that relies on interest income.

Banks have several options to grow noninterest income. Among them:

- Increase volume in transactions, customers or customer segments, or new geographic markets;

- Offer new services to generate additional income; or

- Implement new pricing strategies, such as charging for services that are currently free, designing new pricing models, or bundling or unbundling services.

The exact strategies to adopt may vary by business type, customers’ price sensitivity and the nature of the demand function, and the regulatory compliance requirements.

Thinking ahead for 2025, banks may want to reevaluate their noninterest income strategies, especially in the following business lines: retail banking, payments, wealth management, and investment banking and capital markets.

Retail banking

For many banks, service charges, such as those for monthly services, overdrafts, nonsufficient funds, and ATM transactions, make up a sizable portion of total noninterest income.35 This revenue stream may be less reliable in the years ahead because regulators seem keen to limit banks’ service charges as part of the broader effort by the Consumer Financial Protection Bureau (CFPB) to “rein in junk fees.”36 For example, the CFPB has proposed a cap on overdraft fees as low as US$3.37

In response, some banks may start charging for formerly free services, such as checking account maintenance.38 However, this comes with some risks: A few banks were forced to roll back such fees due to customer backlash and regulatory scrutiny more than a decade ago.39

So, what new strategies should banks implement to grow fee income in retail banking?

Options include adding services, such as embedded advice; bundling different services; tiering pricing based on account offerings; and developing finer customer segmentation based on data such as lifestyle or spending habits. To achieve these goals, banks will need to gain a deeper understanding of customer needs and price sensitivity, and equip themselves with robust customer data and more effective targeted marketing.

Payments

Fee income generates well over US$100 billion for US payments companies, as per Deloitte’s analysis. A 2022 Federal Reserve study concluded that fees, excluding interchange fees, make up 15% of the total profitability for credit card issuers.40 Payment networks, meanwhile, earn almost all their revenues and profits from fees.41

But increasingly, this business is facing challenges like declining transaction margins and greater regulatory pressure on credit card late fees. Merchants are also fighting back against interchange fees by incentivizing customers to use low-cost payment methods, such as point-of-sale (POS) account-to-account (“pay-by-bank”) payments.42 And, of course, competition from bigtechs and fintechs is also growing.

To boost fee income, payments companies can consider:

- Increasing transaction volumes by enabling seamless and secure transaction flows; and

- Delivering more value-added services to merchants and customers on top of those transactions.

Card issuers can grow co-branded deals from traditional categories, such as travel and groceries, to new spend verticals and channels like in-app gaming purchases and social commerce, respectively, to grow their share of consumer wallet.43

Additionally, working with merchants to enable secure payments and expand options via different instruments can allow payments institutions to alleviate customers’ concerns, process higher transaction volumes, and grow revenues. A recent study by Adyen found that 55% of surveyed customers will abandon a purchase if they cannot pay with the instrument of their choice. On the other hand, in the same survey, 25% of respondents feel more unsafe while shopping today than they did a decade ago due to the perceived rise in payments fraud.44

Payments companies could also help generate additional fee income by offering value-added services; they could, for example, provide accounting services to small and midsize business clients. Meanwhile, payment networks could continue to grow their data and risk management solutions. Mastercard posted 19% year-over-year growth in its value-added services and solutions vertical, to US$2.6 billion in second quarter 2024, which was largely driven by its cybersecurity solutions.45

Wealth management

Wealth management has been a bright spot for many banks in recent years.46 But, it appears, much of this growth has come from increased assets under management, driven largely by overall market gains and net inflows.

There is still room to grow, though: Top banks only have a 32% market share of the total wealth management market globally.47 But these opportunities could be harder to exploit than before, due to increasing competition, commoditization of advice, and widespread customer dissatisfaction with fees.48 Regulators are also focusing their attention on fee transparency.

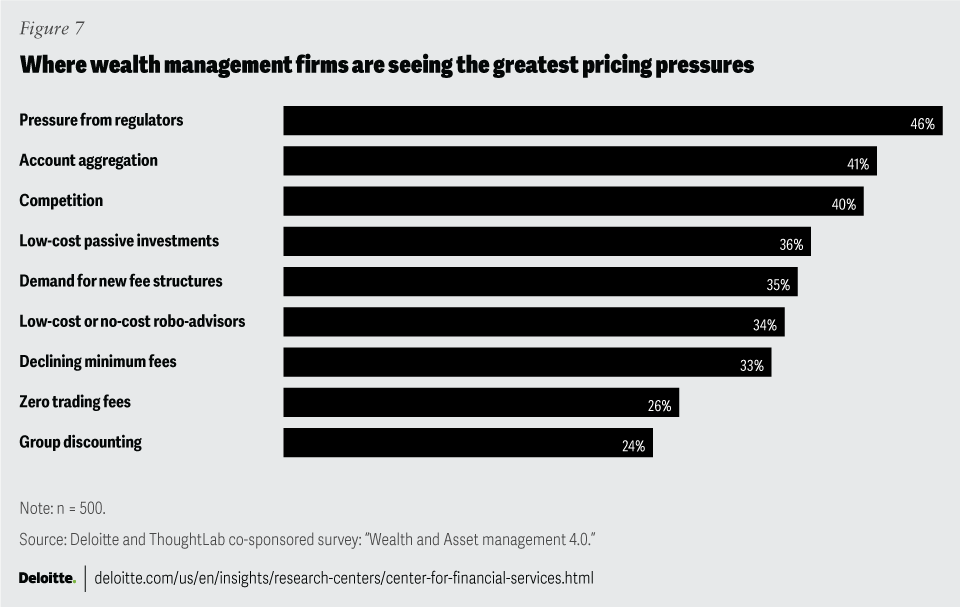

As a result, wealth managers are facing increasing calls for fee compression, according to the Deloitte Global co-sponsored survey with ThoughtLab, Wealth and Asset Management 4.0 (figure 7). However, this is not happening across the board.49 It is most evident among the more “vanilla” areas of wealth management, such as passive investment strategies, where it is more difficult to justify a high fee.

Clients also seemed dissatisfied with fees. Only 36% of respondents in the survey were happy with their fee structures, with wealthier clients being the least satisfied.

So, how can wealth management firms grow their fee income and be less subject to the vicissitudes of the market?

Reiterating the value of advice to clients, either in in-person interactions or through digital interfaces, and expanding the domain of advice beyond core investment advice to areas such as tax, estate planning, or long-term care can be a first step. A recent Deloitte survey of wealth chief investment officers revealed many are updating their platforms to integrate these additional services.50 The survey results also suggest clients are willing to pay for advice.51 Firms should aim to surpass customer expectations at all levels, by personalizing their experience, resolving potential problems proactively, or making the onboarding journey seamless. A modern technology architecture should play an important role here.

Wealth managers can also offer more tailored products and services, such as in the area of alternative investments. Firms could also benefit by incentivizing advisers to cross-sell other banking products, such as loans and deposit accounts.52 Finally, firms can explore revising pricing orthodoxies and redesigning fee structures to align with customer preferences.

Investment banking and capital markets

US banks’ recent earnings show capital markets revenues are mounting a comeback, thanks to a renewed M&A pipeline, greater demand for capital from companies as well as private equity sponsors, and elevated trading volumes. These income streams may only get stronger in 2025 if there is greater market activity.

Despite this positive outlook, capital markets firms may need to consider unconventional options to grow fee income.

For instance, some banks are already looking to gain a larger share of fees paid out when a deal collapses due to regulatory challenges. These breakup fees have typically been 15%, but large institutions in Europe and the United States are reportedly beginning to seek 25% for large transactions.53 They are also seeking higher fees for fairness opinions in the form of “announcement fees,” which are paid out when new deals are announced.

Some firms could also consider targeting smaller deal sizes, such as mid-market deals, which could provide repeat business and opportunities for fundraising private equity buyouts. Expanding into new geographic markets, both domestically and abroad, is another potential opportunity to drive growth. For instance, many banks expect a spike in mergers and equity issuance in Mexico due to the proliferation of nearshoring and other foreign investments.

Some banks should also look for new partnership opportunities with private equity firms, especially given the sizable dry powder they have right now. Specifically, a significant driver of deal activity is expected to come from private equity firms as valuations stabilize or increase, and there are greater exit opportunities.54

Global considerations

Banks outside the United States may face similar challenges in growing fee income, although the exact dynamics may vary based on the regulatory regime, market conditions, and customer preferences. For instance, the Asia-Pacific region is where wealth accumulation is the strongest, offering opportunities for both domestic and foreign firms.55 As for payments, there are a number of avenues to generate more fees from greater transaction volumes and value-added services.

Will the promise of an AI-powered bank accelerate tech modernization?

Key messages:

- The promise of an AI-powered bank can serve as a catalyst to accelerate technology modernization.

- Resolving long-standing technical debt is fundamental to successfully deploy AI across their organizations.

- Maximizing returns on cloud investments and upgrading their data infrastructure should be another major priority.

- Banks should also continue to balance the adoption of traditional AI and generative AI.

Aspiring to be an AI-powered bank

The transformative potential of AI in banking is swiftly becoming a reality. Rapid advancements in both traditional and cutting-edge AI technologies are set to revolutionize the delivery and consumption of banking services. According to a 2024 Citigroup report, AI could propel global banking industry profits to a staggering US$2 trillion by 2028, reflecting a 9% increase over the next five years.56

Imagine an AI-powered bank: an institution that can seamlessly integrate the latest in machine learning, neural networks, natural language processing, and generative AI tools. Leaders of an AI-powered bank not only understand that superior AI capabilities are essential for survival; they also use them as a key differentiator. Their bank employs AI responsibly to drive transformative activities and outcomes across the enterprise. It also focuses on reengineering the governance structure and processes, as well as its talent models, to extract the maximum value of its AI investments.

Many banks seem convinced of the potential of AI, but they struggle with how best to scale, make it productive, and fit within existing budgets. At the same time, many institutions are grappling with “change fatigue.” They know they should modernize their tech and data infrastructure more quickly and invest more. In Deloitte’s State of Generative AI in the Enterprise: Quarter three report survey, only one-quarter of banking respondents said their data management platforms are highly or very highly prepared to adopt generative AI tools and applications.57

But deploying AI more widely and successfully will not happen unless leaders more firmly address how, and to what extent, their banks continue to rely on disjointed and antiquated legacy technology infrastructure, contributing to technical debt. While many banks have been slowly but surely chipping away at their tech debt, it has been an albatross around bank leaders’ necks for at least three decades. While many banks are already well along the digital transformation journey, it may not be happening at the pace they would like.

To realize the promise of an AI-powered bank, how can banks overcome their tech debt? Modernizing the core banking infrastructure could be addressed head-on with greater energy and focus.

Getting more value from traditional AI and embracing generative AI

To harness the full power of AI, banks should balance the adoption of “traditional” AI (models performing preset tasks using predetermined algorithms and rules) and the “new” generative AI that produces new content. While developments in large language models may be garnering the most buzz, many banks can do more to use the predictive power of traditional AI to advance business outcomes.

JPMorgan is investing in generative AI and other emerging technologies, such as quantum computing.58 The bank acknowledges, however, that it still plans to extract more value from more foundational forms of machine learning. In May 2024, the bank revealed that a solution built to nudge customers who abandon a product application using AI resulted in a 10% to 20% boost to completion rates, for example.59 Even smaller, community banks are implementing AI tools. For instance, BAC Community Bank in Stockton, California, which has about US$800 million in assets, launched an AI-powered app that answers user questions and assigns a nearby banker to serve as their point of contact.60

Concurrently, as generative AI is deployed to unleash a new wave of productivity, 2025 could be the inflection point. It could be the year when banks move from experimentation to commercialization across the enterprise, from software engineering to fighting financial fraud.

As banks push ahead with generative AI pilots, they will likely begin shifting from closed-source models that are typically built in-house or supplied by tech vendors to open-source models that use publicly available code.61 These banks may want more control over the design and application of their generative AI software, as well as their data exposure.62

Embedding trust across the AI life cycle

Banks walk a fine line working to deliver on the promise of AI while managing the emerging risks from new technologies. Investments in generative AI risk mitigation and governance tend to be particularly underfunded relative to enterprise spending on research and development for large language models, according to research from the Deloitte AI Institute.63

Challenges arising from AI and generative AI can include biased or unfair outcomes, lack of transparency into model behavior, IP infringement, and insufficient data privacy. A trusted and secure framework for AI can provide assurance that models are fair and impartial; robust and reliable; transparent and explainable; safe and secure; accountable and responsible; and respectful of privacy.64

These pillars of trustworthy AI should be embedded into each stage of the AI life cycle, beginning with readiness assessments and carrying through development, testing, remediation, and continuous oversight. To facilitate AI trust by design, banks should instill guardrails into each process underlying model ideation, development, and implementation. Banks could benefit from a cross-functional group containing specialists in legal, compliance, information security, IT, data, and strategy that collaborates on establishing clear governance and escalation channels that include processes for triggering other risk functions as needed.

It is also key that banks assess risks that may be unique to their organization, such as how to monitor “shadow AI”—the unsanctioned use of outside AI tools—as well as the degree of oversight needed to supervise models, products, and interactions between AI and end users. Finally, being realistic about which test cases are not feasible for AI, such as business-critical functions executed on core platforms, can be key to retaining trust.

Banks with more limited tech budgets can also consider deploying small language models that operate with fewer parameters and are less cost-prohibitive to build and maintain. Since small language models are typically built on publicly available code using a narrower data pool, banks can train them on specific tasks and more quickly adapt them to internal applications, such as summoning product details and processing minor transactions.65 In addition, smaller banks can benefit from joining consortiums that pool resources and collaborate on best practices for developing an AI playbook.

Strengthening the core to facilitate tech transformation

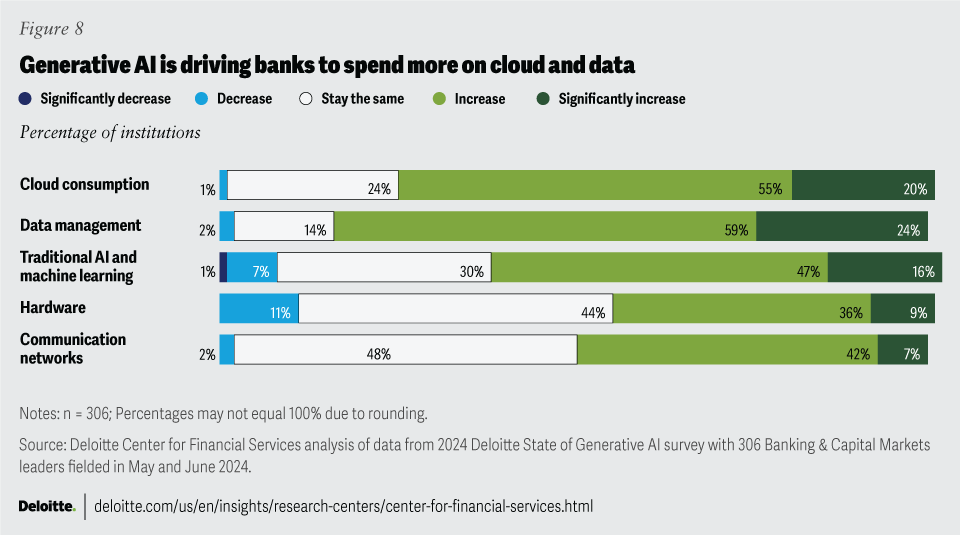

In a 2023 Forbes Insights report, nearly six out of 10 banking leaders surveyed consider legacy infrastructure to be the top challenge impeding their organization’s business growth.66 This underscores the push for banks to accelerate their modernization efforts to fully harness the transformative power of AI. As of June 2024, more than three-quarters of banks plan to increase investments in data management and cloud consumption to advance their enterprisewide generative AI strategy, according to Deloitte’s State of Generative AI in the Enterprise: Quarter three report survey.67

But bringing these mainframe-based “zombie” cores that may no longer support key functionalities into the modern era could remain an uphill battle in 2025.68 Since a full replacement of these core systems is often a cost-prohibitive, multi-year endeavor, some banks may “feel like hostages” to their legacy technology, Acting Comptroller of the Currency Michael J. Hsu noted in a May 2024 address.69 In addition, some banks may be hesitant to transition to next-generation systems, which tend to be offered by “newer, less-proven core providers,” according to the Federal Reserve Bank of Kansas City.70

No doubt, many banks have already made progress in modernizing their core systems. But shedding tech debt to achieve the full promise of AI will likely require the pace of core modernization to accelerate. This may not call for a rip-and-replace strategy; banks still have many tools at their disposal to incrementally modernize their cores. Zions Bancorporation in Salt Lake City, for example, spent over a decade incrementally converting its core systems. It started with its consumer loan software, then moved on to commercial and construction loans before concluding with its deposit platform.71

Another option could be to wrap the legacy core in a service and innovation layer, interfacing with next-generation systems through APIs.72 This layer can help banks shift more transactions from batch to real-time processing, as well as more easily integrate with third parties.

But it is perhaps generative AI that may prove most valuable in upgrading legacy mainframes at scale. Some generative AI prototypes, for example, are being trained to rewrite the 1960s-era code that underpins older cores to be compatible with modern software.73 Generative AI tools may also be used to assess the current state of banking systems,74 prepare data for core conversions,75 and automate integration of microservice-based applications.76

A big part of core systems modernization is the investment in cloud migration and a more robust data infrastructure (figure 8).

Continuing cloud migration is key to effective AI integration

One cannot achieve the full promise of an AI-powered bank without cloud as the underlying infrastructure. Scaling the migration to cloud is an imperative; however, it is becoming more complex. Determining the optimal mix of public versus private cloud is a fundamental question. Scaling cloud investments should entail a targeted strategy that accounts for ease of transfer, operational risks, and a timeline for “end-of-life” software wind-downs.

In addition, to get the maximal value from cloud, one should also consider the economics. More banks are adopting a financial operations (FinOps) approach to managing costs while maximizing return on cloud investments. This cross-functional framework can help track unused resources, identify commitment-based discounts, and indicate when resources should be moved back on-premises, a process known as cloud repatriation.77 These processes are gaining traction. As banks weigh trade-offs between public and private cloud workload migrations, they face heightened scrutiny of their hybrid cloud budgets in relation to overall IT spend.78

Cloud providers are increasingly offering AI solutions to appeal to banks, especially small banks. Bank leaders should weigh the pros and cons of this decision, including the potential for vendor lock-in. In light of this, some may decide developing their own AI models could be a better option.

Preparing for data’s moment in the spotlight

Similarly, an AI-powered bank cannot reach full potential without robust, modern data. But the current state of the data infrastructure at many banks is not up to par, and many of these institutions realize this.79 Revamping the disparate, complex data systems may not be easy, however, because of fragmentation, incompatibility of data formats, and the difficulty of access to data.

Banks can take a few steps to upgrade their data infrastructure to deploy AI securely and effectively. To assess data readiness, banks should consider whether the data that will train AI models is consistently available, of high quality, properly structured, and aligned to project objectives.80 Since many banks are likely to have data fragmented across multiple repositories, they may need to develop integrated data pipelines. Migrating data to a centralized cloud-based platform is one option to reduce silos. Banks can also consider data integration processes that bridge the gap between diverse data sources. For example, tech teams have long used Extract, Transform, and Load (ETL) processes to send data from source systems to a data warehouse.81 They can spur additional movement of data by using Reverse ETL, which synchronizes data from multiple sources and delivers it to software for sales, marketing, and customer service.82

Global considerations

Aspiring to be an AI-powered bank is a global phenomenon. As a result, the push to accelerate core system modernization should be no different for banks outside the United States.

European banks have made progress upgrading their core banking systems due to regulatory requirements for cashless transactions.83 They have also been investing in digital transformation to comply with rules on open banking and customer authentication for electronic payments.84 Meanwhile, many banks in the Asia-Pacific region still rely on decades-old legacy systems, although financial institutions in countries such as Australia and Singapore are spending more on technological upgrades.85

Many foreign banks lag the United States in adopting emerging technologies, particularly cloud migration.86 If they continue to lag in transformation investments, they could risk diminishing their market positioning. Having said that, how different jurisdictions choose to regulate tech-enabled solutions and AI could provide more favorable conditions for banks in certain geographies.87

Why are banks’ efforts to manage costs typically unsustainable, and what should they do about it?

Key messages:

- Since revenue growth may remain elusive, cost management should continue to be an imperative for many banks.

- Finance executives should make sustainable cost transformation an ongoing discipline.

- Fostering a cost-conscious culture can fuel productivity, scalability, and resilience.

- Banks should focus on scaling AI and automation applications to reduce inefficiencies.

- Integrating risk controls can make cost reductions more sustainable.

Banks are struggling to get their costs under control, and the imperative to bring down expenses should only intensify as revenue growth is expected to remain elusive in 2025.88 Many banks will likely need to make tough choices on how to allocate spending to generate additional savings and preserve profitability.

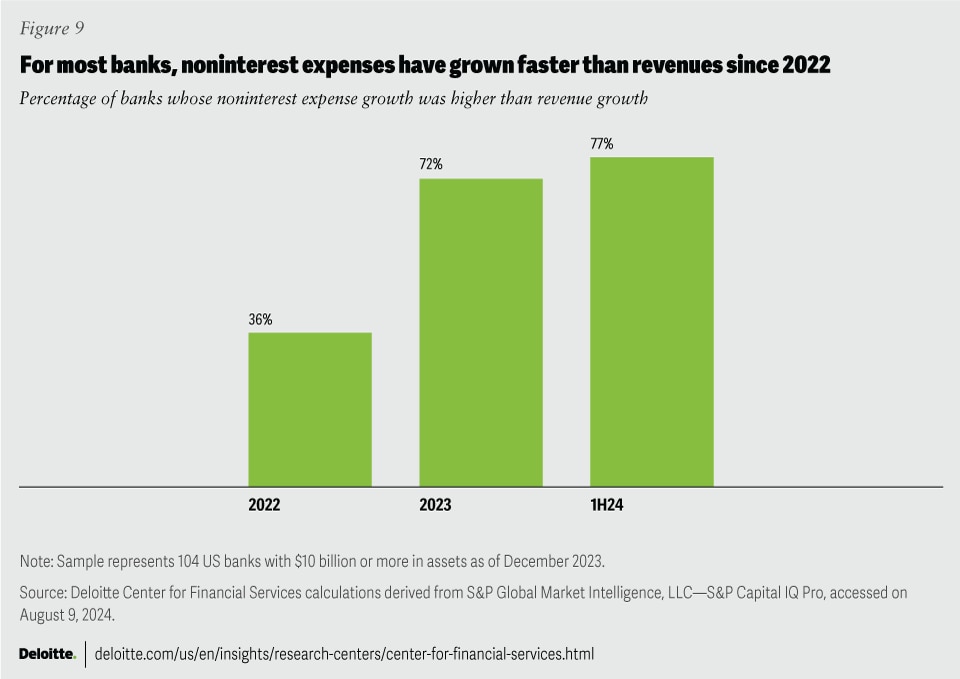

Over the last few years, growth in total noninterest expenses has outpaced net revenue growth for banks with more than US$10 billion in assets (figure 9), and this trend could continue. In second quarter 2024, the three largest US banks raised their full-year expense targets by US$4 billion compared to their estimates at the beginning of the year.89 Meanwhile, the core drivers of these swelling budgets—compensation, regulatory compliance costs, and technology investments—appear unlikely to decline dramatically anytime soon.

Among US banks with more than US$10 billion in assets, compensation expenses grew 4.1% year over year, to US$149.6 billion in the first half of 2024.90 This was mainly due to performance-linked rewards in revenue-generating businesses, such as trading, wealth management, and investment management. At the same time, banks are paying huge sums to attract technology talent in fields such as machine learning and generative AI.

Compliance and remediation costs also remain elevated. They may, in fact, go up with new regulations, such as open banking, Basel III Endgame, and debit card swipe fees,91 coming into effect in 2025. For instance, a 2024 LexisNexis Risk Solutions study indicated that the cost of financial crime compliance has increased for 99% of financial institutions in the United States and Canada, reaching US$61 billion. This data includes banks’ spending on technology software, such as know-your-customer and anti-money-laundering software and updates, and infrastructure to manage regulatory expectations.92

And, as for technology-related expenses, which make up a significant portion of noninterest expenses, many banks have been increasing their investments for both “run the bank” and “change the bank” initiatives.93

Why are efforts to rationalize costs often unsuccessful in the long term?

Nevertheless, to curb cost increases, a number of banks have announced formal plans in the recent past. Citigroup, for example, is taking drastic steps to simplify its organizational structure and exit noncore markets, in part to manage expenses.94 Similarly, Truist aims to improve operating leverage by restructuring businesses, consolidating its branch network, and rationalizing headcount.95

However, a reality is that many cost savings initiatives tend to fall short of expectations. In a recent Deloitte MarginPLUS survey, 56% of the 25 global banking and capital markets executive respondents in the sample stated their institutions did not achieve even 50% of their cost savings targets last year.96 And, in fact, only one respondent indicated their institution unlocked 100% of their savings targets or more.97

Among the banks surveyed, 50% named “challenges with technology infrastructure” as a challenge achieving long-term cost control.98 Deriving insights from huge volumes of data that provide a comprehensive view of how costs manifest in day-to-day processes can be another opportunity. As a result, banks may make cost-cutting decisions that do not address the underlying drivers of operational costs.

Banks aim for more sustainable cost transformation

So, how can banks achieve more sustainable cost savings? Consider the following levers.

Tap the benefits of cost transparency

According to the Deloitte MarginPLUS survey, nearly one-half of the 25 global banking and capital markets respondents in the sample plan to conduct an enterprisewide analysis of cost structure before deploying an expense management program to realize savings by 2026.99

But doing an analysis of cost structure, as in the case of activity-based costing (ABC), which provides a detailed accounting view of where and how various costs are incurred in every activity or process, may not be enough. Cost transparency, as a discipline, can offer banks an operational perspective on why the underlying costs are elevated. For example, senior bankers in a loan underwriting division may be doing work that falls outside the scope of their roles, which could make downstream actions more expensive to execute. While ABC may highlight the elevated costs of the underwriting division, cost transparency can show why spending may not be manifesting in commensurate value.

When used complementarily, cost transparency with ABC can assist executives to diagnose both the root causes and symptoms of their elevated cost base. These insights can inform executives how to better deploy resources and reduce costs sustainably. Finance executives, working with operational teams, may be well suited for this exercise, given their expertise in modeling and access to organizational data. They can also conduct surveys to gather additional metrics that can be cross-referenced in financial models, such as how much time employees spend using applications and for what purposes.

Scale automation and AI to reduce costs and bolster productivity

Banks should also accelerate the adoption of automation and machine learning tools to digitize manual and paper-based processes. Large language models, in particular, can free up resources and enable staff to spend more time on value-added interactions. According to Deloitte’s State of Generative AI in the Enterprise: Quarter three report survey, more than half of banking executives indicated that they want to improve productivity with generative AI, and 38% of executives expect the added efficiencies to reduce costs.100 Yet, there is still enormous potential to create additional efficiencies and cost savings from scaling machine learning applications further.

Integrate risk controls into change initiatives early

Embedding risk and compliance into the early stages of transformation initiatives can also make cost reductions more sustainable, especially since regulators continue to evaluate banks and issue fines for past violations. For example, by installing guardrails in the development of AI models for credit decisioning, banks can help mitigate the risks of algorithmic bias and lack of transparency. Taking this step can also help provide assurance that new launches have been designed securely. Similarly, when updating control frameworks to meet regulatory requirements, banks can look for opportunities to eliminate inefficiencies that raise labor and operating costs.

Maintain a robust execution discipline

Expense control is important to a cultural mindset of continuous improvement. To achieve lasting outcomes, cost-mapping models should be consistently updated as the bank acquires or sunsets applications or undergoes a reorganization. Executives can then monitor cost changes over time and how they contribute to performance outcomes to understand the reason for unexpected fluctuations.

Meanwhile, having a strong execution discipline should help banks prevent costs from creeping back up in the future. Continual tracking of outcomes against business goals will be important to keep the cost of transformation in line with proposed budgets. And lastly, accountability is key. Leaders should hold teams accountable for missing their cost targets, even if they reach other milestones and complete projects on time.

Global considerations

European banks may face even greater pressure to manage operating costs. In 2024, 15 out of 26 large European banks are expected to see cost growth surpass revenue growth, which is 12 banks more than in 2023.101 In response, some European banks are committing to stronger cost discipline as they head into 2025. For instance, according to Deutsche Bank’s second quarter 2024 earnings release, the bank is advancing on its US$2.8 billion Operational Efficiency plan; it realized US$1.3 billion in savings by second quarter 2024 by making progress on optimizing its platform in Germany and reducing headcount.102

UK banks are also likely to tighten their belts in 2025 because the central bank has signaled more rate cuts in the near future.103 Some banks are deploying short-term measures, such as asking their workforce to reduce travel costs.104 And some are exploring strategic cost transformation initiatives to manage expenses over the medium term. For instance, Standard Chartered has reserved US$1.5 billion over the next three years for its “Fit for Growth” program to achieve longer-term cost reductions.105 Since the United Kingdom has rescinded EU rules on capping investment bankers’ bonuses, UK banks are also likely to shift some of their compensation costs from fixed to variable payouts to retain high-performing talent and manage their costs through economic cycles.106

Paving the path to future success

This report addresses five critical questions that bank executives should prioritize in 2025—a year that could be pivotal in many respects. But it’s important to recognize that other priorities, such as accelerating the transition to a green economy and revamping talent models for an AI-driven future, will also demand attention.

2025 could be a defining moment for establishing sustainable growth in the banking industry. The strategic actions taken now could be the catalysts that propel banks toward a brighter, more resilient future. By responding decisively, banks can ensure that the path to success is not just aspirational, but achievable.

Methodology

This report is based on input from Deloitte’s subject matter specialists, extensive secondary research, and proprietary forecasts.

In particular, the team used historical data from S&P Global Market Intelligence, LLC – S&P Capital IQ Pro to analyze banks’ financial performance and applied statistical methods such as regression analysis to forecast various banking metrics. Data from multiple Deloitte proprietary surveys were also used to bolster insights.

Continue the conversation

Meet the industry leaders

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

We want to hear

from you!

Complete a brief survey to provide your views on thought leadership content.