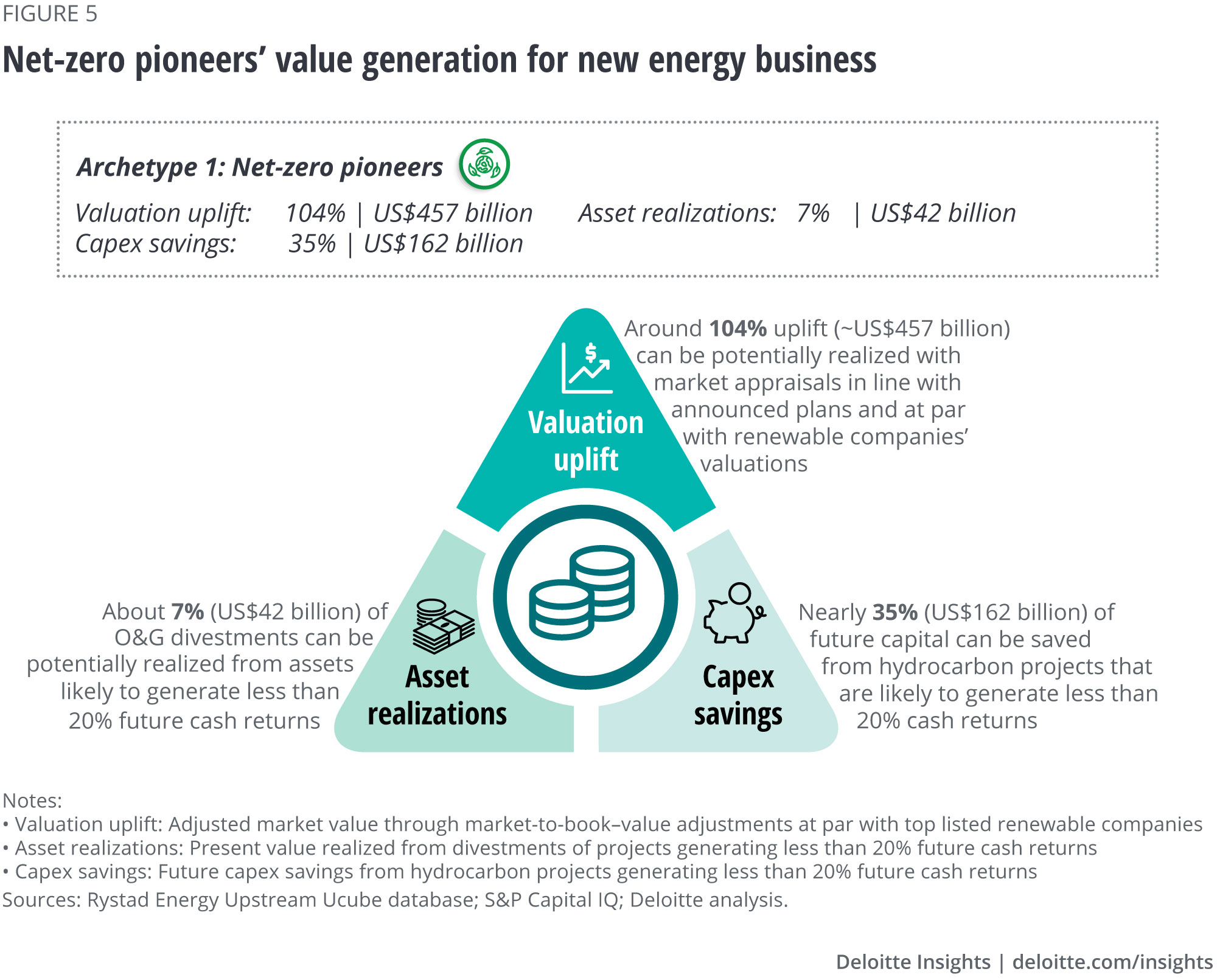

Net-zero pioneers

Going green can help pioneers overcome multiple challenges, including negative image, capital constraints, trickling flow of incoming talent, and improved access to low-cost finance. In fact, funding costs of low-carbon O&G debt issuers in North America are 75 basis points lower than that for carbon-intensive borrowers with an additional six years on the bond tenor, providing greater capital raising flexibility.27

As the novelty of going green matures, low-carbon technologies evolve faster-than-expected, and keen competition emerges among the commercially viable ones, pioneers could be judged and differentiated on how well they can make good on early green bets. Rightly so, about 80% of surveyed senior O&G executives that identify as net-zero pioneers highlight technology evolution as their topmost challenge. They need to be alert to opportunity and agile in pursuing it, while balancing gains and risks by adopting flexible partnerships and hybrid technology models or empowering low-carbon ventures.

Further, divesting the pioneers’ hydrocarbon assets in an improved price environment would be favorable but could give rise to a dilemma as buyers with poor carbon profiles emerge. Selling assets to such buyers may result in a net-addition, not net-zero, to the environment and would lead to negative reactions from stakeholders, investors, and even regulators, as noticed when a major oil company divested assets to Scotland’s largest carbon emitter or in another case, to a closely held, “almost invisible” operator.28 Sellers need to live up to their social obligation of responsible divestment, where they don’t make an asset’s lifetime emissions a buyer’s problem and simply move on.

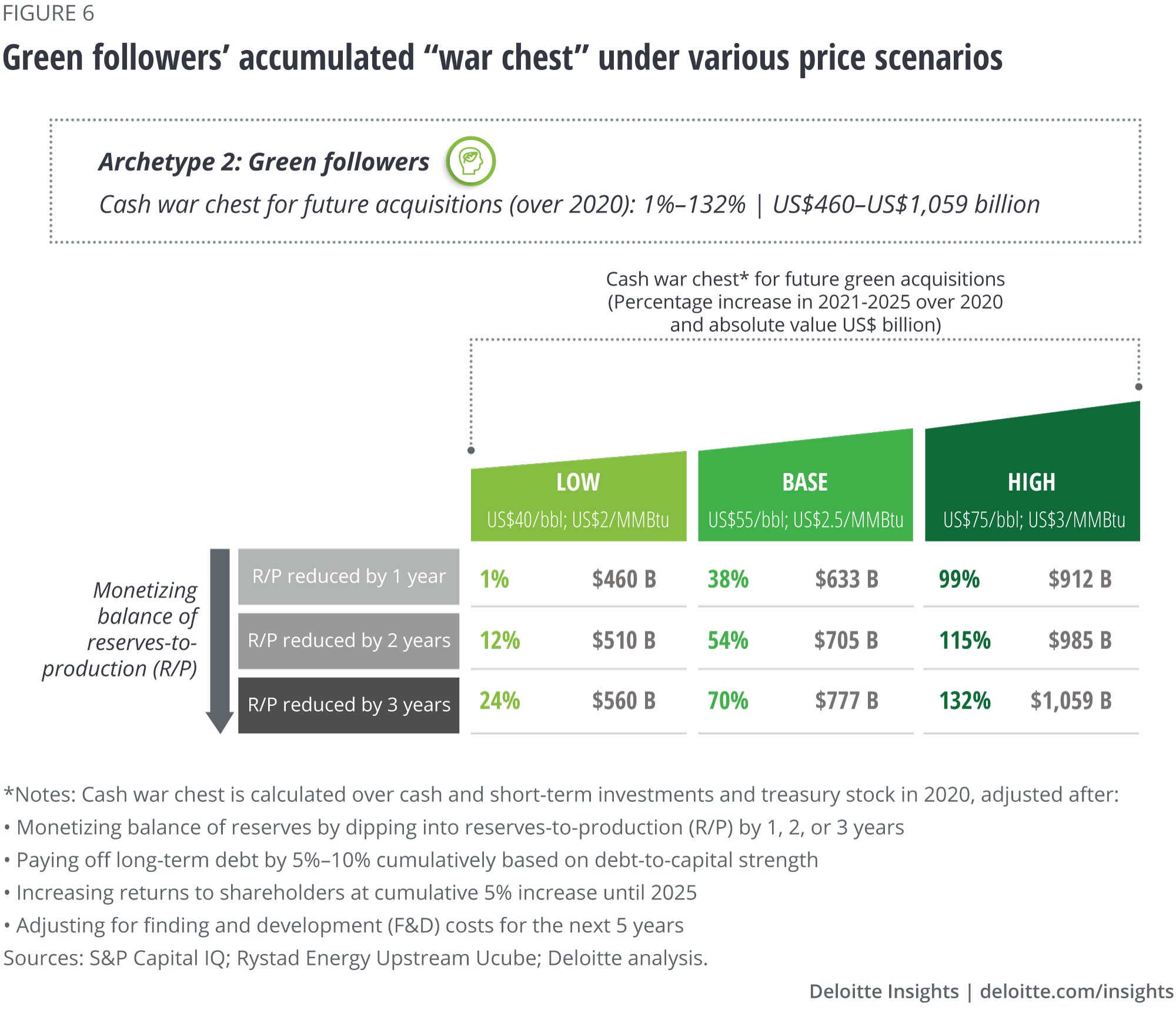

Green followers

A watchful wait strategy can help green followers gradually build the future “green” capital required, ride out the nascent green experimentation phase, and maximize hydrocarbon value at higher prices. They can also zero in on scalable economical bets, which aren’t fragmented and crowded with upstarts, as currently seen in the solar PV and onshore wind space. These technologies are seeing 95% of global annual capacity additions, with internal rate of return (IRR) hovering around 6%–7% for solar PV and 9%–10% for onshore wind (as against many oil projects delivering more than 15% IRR at US$50/bbl).

Capturing the above band of IRRs or picking a more competitive new energy solution altogether would require much more than hard dollars from green followers. Leveraging existing hydrocarbon infrastructure for new energy solutions (e.g., offshore wind), establishing a new corporate structure to commercialize low-carbon technology portfolios, building an extensive energy trading and marketing experience, identifying corporate PPA opportunities, and entering into strategic partnerships especially on the transportation and storage front of green energy (aka new midstream) could be some starting points for green followers. For instance, Quidnet Energy and Emissions Reduction Alberta (ERA) partnered to develop an ultra-low-cost form of hydroelectric energy storage, using technical O&G expertise of well-drilling and high-pressure pumping to store renewable energy in shale formations.29

Right messaging and a clearly communicated strategy, maximizing or maintaining shareholder returns, and engaging with M&A advisers and strategists early on can effectively help build out these opportunities. Timing the cycle may not be the only point—timing companies’ readiness is important as well.

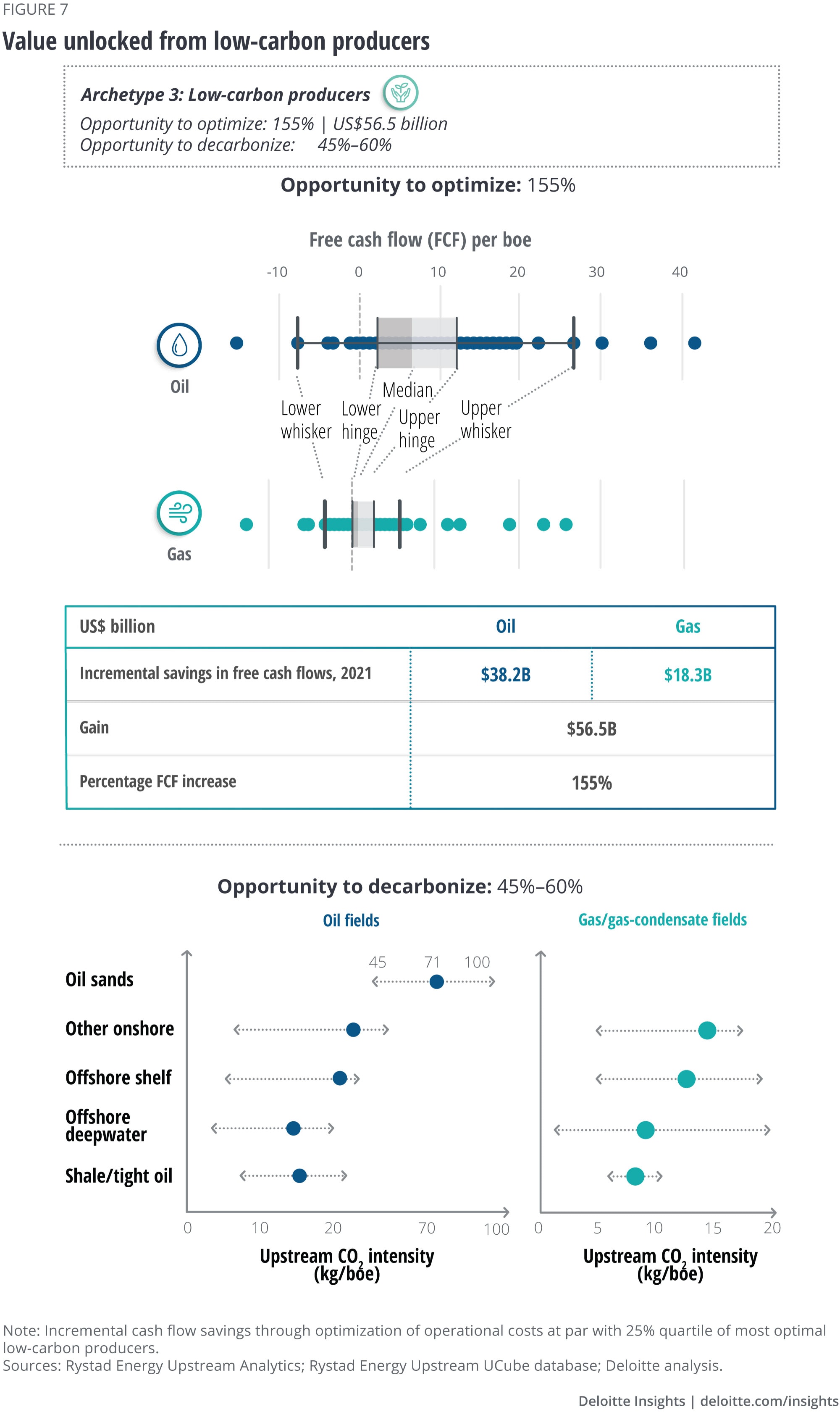

Low-carbon producers

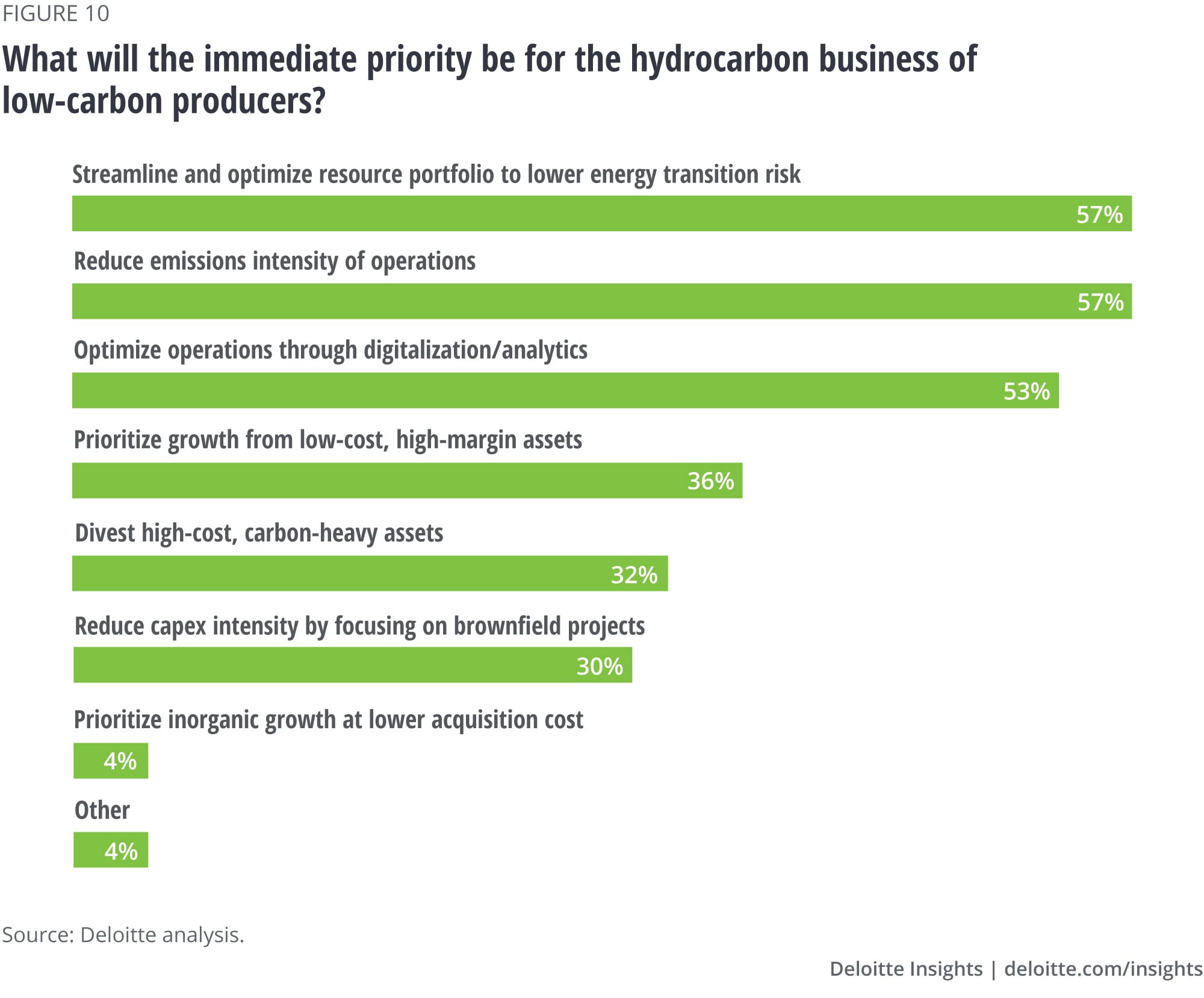

Low-carbon producers have to balance economics (operational efficiency) and environment (decarbonization) to be a lean machine from day one and create a domino effect in the long term. Any investments they make in automation, energy efficiency, advanced leak detection, quantification technology, etc. serve this dual purpose. In fact, about 55% of surveyed producers’ immediate priorities for their hydrocarbon business are to reduce the emissions intensity of operations, streamline resource portfolio to lower the energy transition risk, and optimize operations through digitalization/analytics (figure 10).30 For instance, a major international E&P is defining its operational performance as a function of both, lower cost of production and lower emissions intensity, and has been trading ahead of analysts’ net asset valuations due to its combination of low-cost, low-emitting, and higher-yield assets.31

Going forward, companies should bring more than just an engineering efficiency mindset to develop their business and grow innovatively. There is big value, for instance, in shaking up the status quo to become innovative marketers. Lundin recently made headlines for its sale of the world’s first certified carbon-neutral oil from its Edvard Grieg field, which has five times less CO2 per barrel of oil than the world average.32 The company aims to achieve full carbon neutrality of all its production by 2025.33

The way forward is to keep doing more—in other words, using stakeholder pressure to achieve best-in-class results (operationally or ESG-driven). Metrics of project evaluation, performance assessment, and reporting transparency have to evolve and go beyond “this is how we operate.” Producers that balance all three—portfolio, business optimization, and emissions—can truly unlock value on this path.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}