{kind=link}

{kind=link}

{kind=link}

{kind=link}

The future of power has been saved

The authors would like to thank Hilmar Franke and Dr. Florian Klein, who contributed both their industry experience and their methodological excellence to the study.

Cover image by: Mark Milward.

The European Union (EU) announced the European Green Deal in December 2019, reinforcing its commitment to the Paris Agreement on climate change and setting the ambitious target of becoming the world’s first climate-neutral continent by 2050. Although emissions from power generation in the EU dropped by nearly 30 per cent over the past ten years, the sector still produces almost one-third of the direct CO2 emissions.

Rapidly falling costs for a range of clean technologies and the promise of widespread electrification place power generation at the heart of the European energy transition. However, while the future brings opportunities for utilities and power generators, it also presents a set of challenges:

• power-generation fleet is ageing; many nuclear and thermal power plants are nearing the end of their lifetime and need to be replaced or refurbished

• first generation of wind turbines is also reaching the end of its operational lifetime and will soon be decommissioned

• coal remains the backbone of power generation in several countries; this is no longer consistent with environmental objectives

• solar and wind generate highly variable amounts of energy, which pose threats to system stability and reliability.

Moreover, the turbulent 2010s scarred the balance sheets of power companies, creating an environment of risk aversion reflected in low investments. Policymakers need to strike a careful balance between fostering clean technologies and keeping electricity affordable for households and industry alike.

As with all major challenges – such as addressing mass migration or fighting COVID-19 – European societies encompass a complex set of competing and fiercely debated viewpoints. The energy transition is no exception, and the dominating mindset will have a huge impact on the final shape of the transformation.

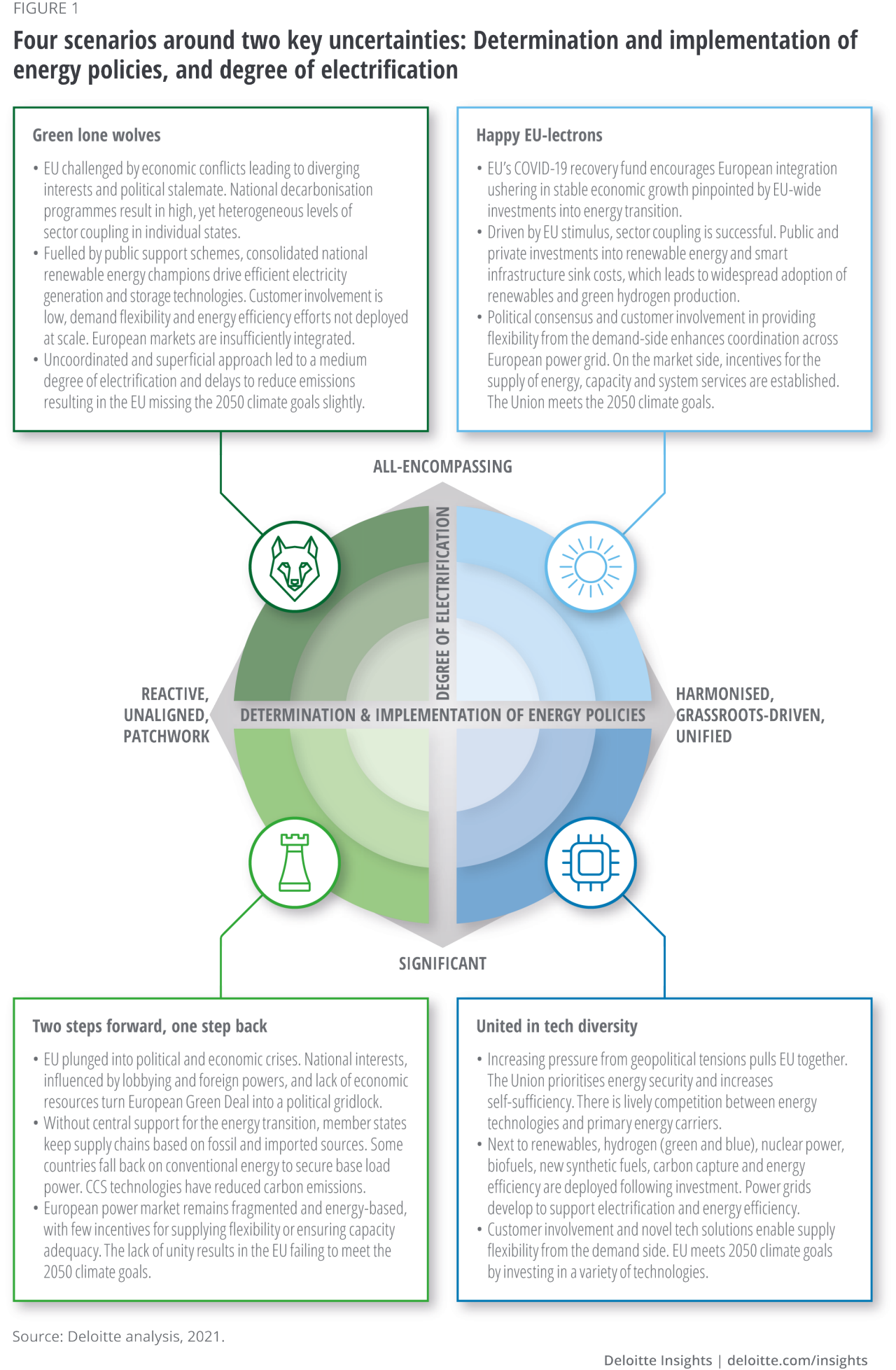

Against this backdrop, four distinct scenarios were assessed (figure 1). Each depicts an alternative pathway along which the European power sector could travel depending on how underlying economic, regulatory, societal and technological drivers unfold. The objective of the scenarios is to stimulate debate and illuminate strategic decision-making, not to give an exact and accurate prediction of the future.

The scenarios centre around two key uncertainties. First, the determination and implementation of energy policies reflect the balancing of economic realities by policymakers, societal mindset and environmental objectives. Second, the degree of electrification reflects the role of electricity in decarbonising energy end uses. What might sound more like a finding than an assumption is in fact a bundle of policy choices and societal preferences that puts electricity in the pole position – or not.

First, the main economic, environmental, policy, social and technological trends relating to power demand were identified. These were clustered according to relative importance and level of uncertainty. Some relevant trends feature in all scenarios, such as the cost-efficiency of renewables, the prevalence of external taxes, etc.

Relevant but uncertain factors that define differences between the scenarios include electrification of different end-use demands, network infrastructure investments, political coordination and ambition among different European states, and the regulatory push for the energy transition overall. These were condensed into two axes: Degree of Electrification and Determination of Energy Policy.

Based on these axes and their uncertainty level, four different but equally consistent scenarios were constructed. Each represents a plausible future of the European power system (figure 1).

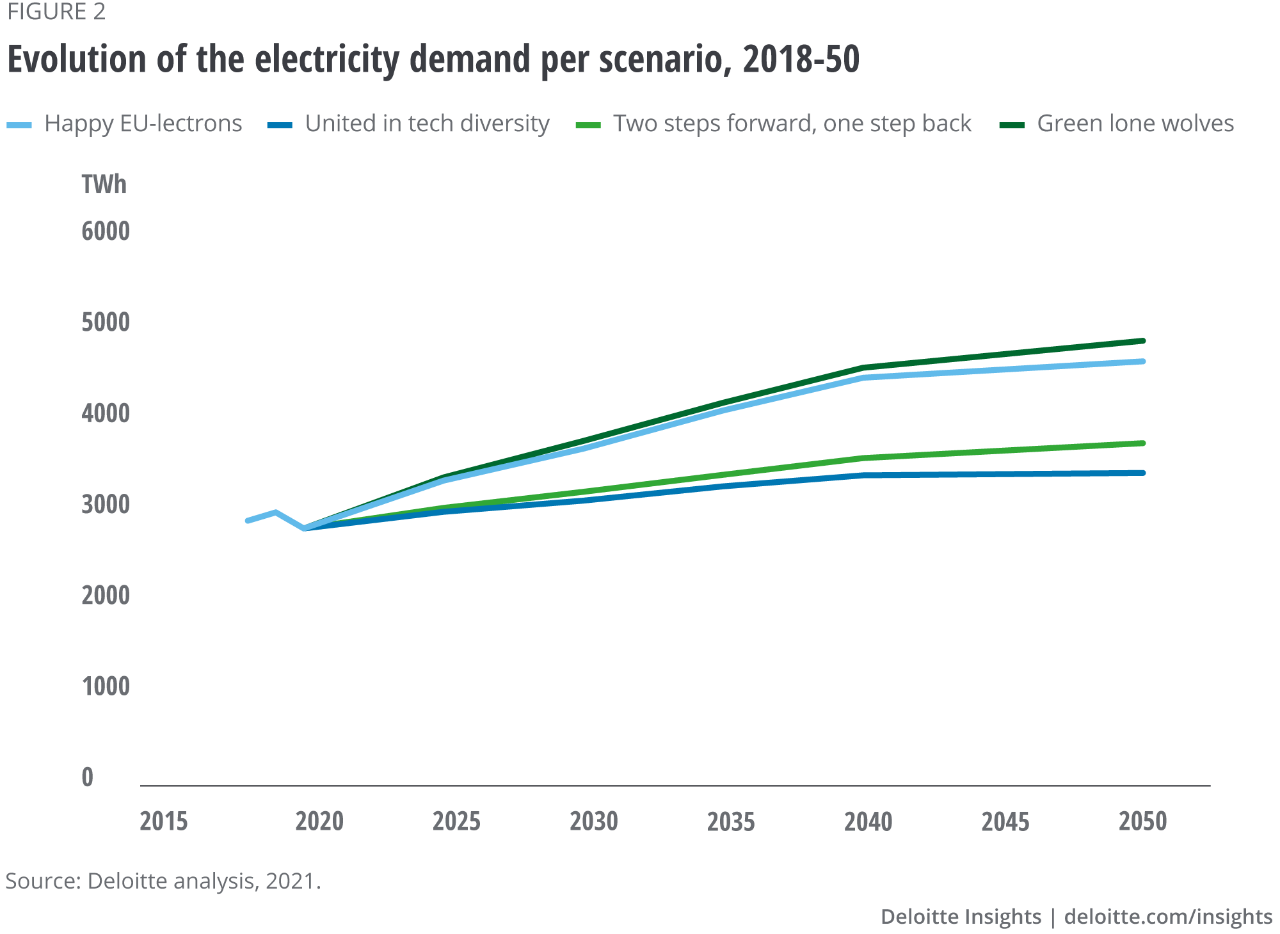

Electrification features prominently in all scenarios, but it is only in the “Happy EU-lectrons” and “Green lone wolves” scenarios that it takes a lead role. This means that electricity demand is set to grow over the next three decades; however, the increase could range from 10 per cent to 75 per cent (figure 2). Electricity demand evolution is, therefore, one of the biggest uncertainties for the power sector.

This is due to the interplay of a multitude of drivers. New end uses, such as electric vehicles, production of hydrogen via electrolysis or deployment of heat pumps and other electric heating solutions, put upward pressure on power demand. However, fuel cells will fight for market share in the transport sector. Hydrogen could possibly be produced at a competitive cost from fossil fuels with carbon capture and storage (CCS) also, while huge energy efficiency potentials are still untapped today. These drivers could tame power demand significantly.

There is currently 950 GW of power-generation capacity operational in the EU. By 2050, the capacity could top 2200 GW – the outcome of the “Happy EU-lectrons” scenario – if a combination of strong electricity demand and a supportive environment for renewables prevails. A more technology-neutral future – “United in tech diversity” – could still see installed capacity grow by a third over the next 30 years. In other words, the uncertainty range for power-generation capacities in the period to 2050 is 1000 GW. However, all signs point towards growth.

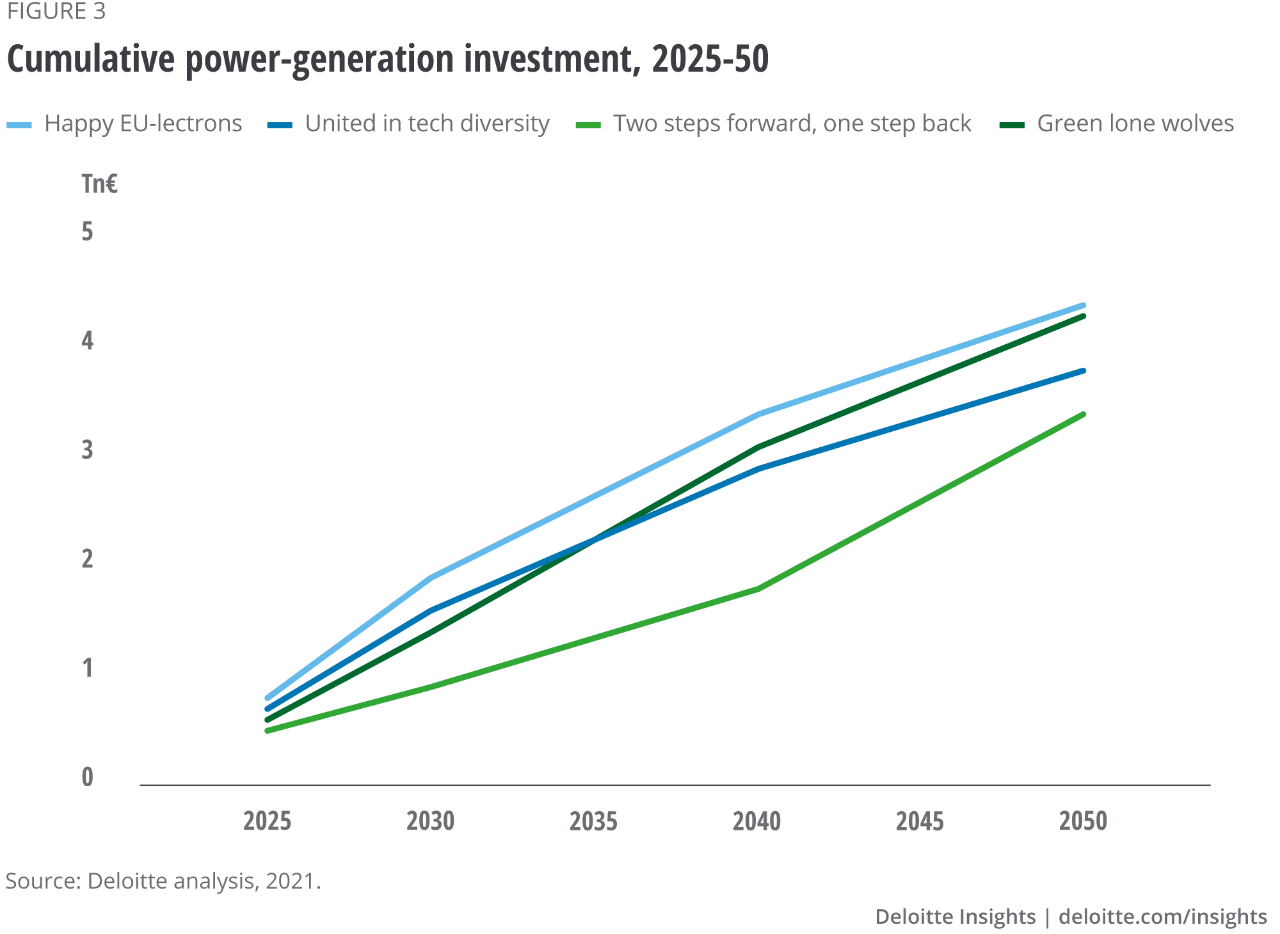

When it comes to investments, the industry needs to prepare for a triple whammy:

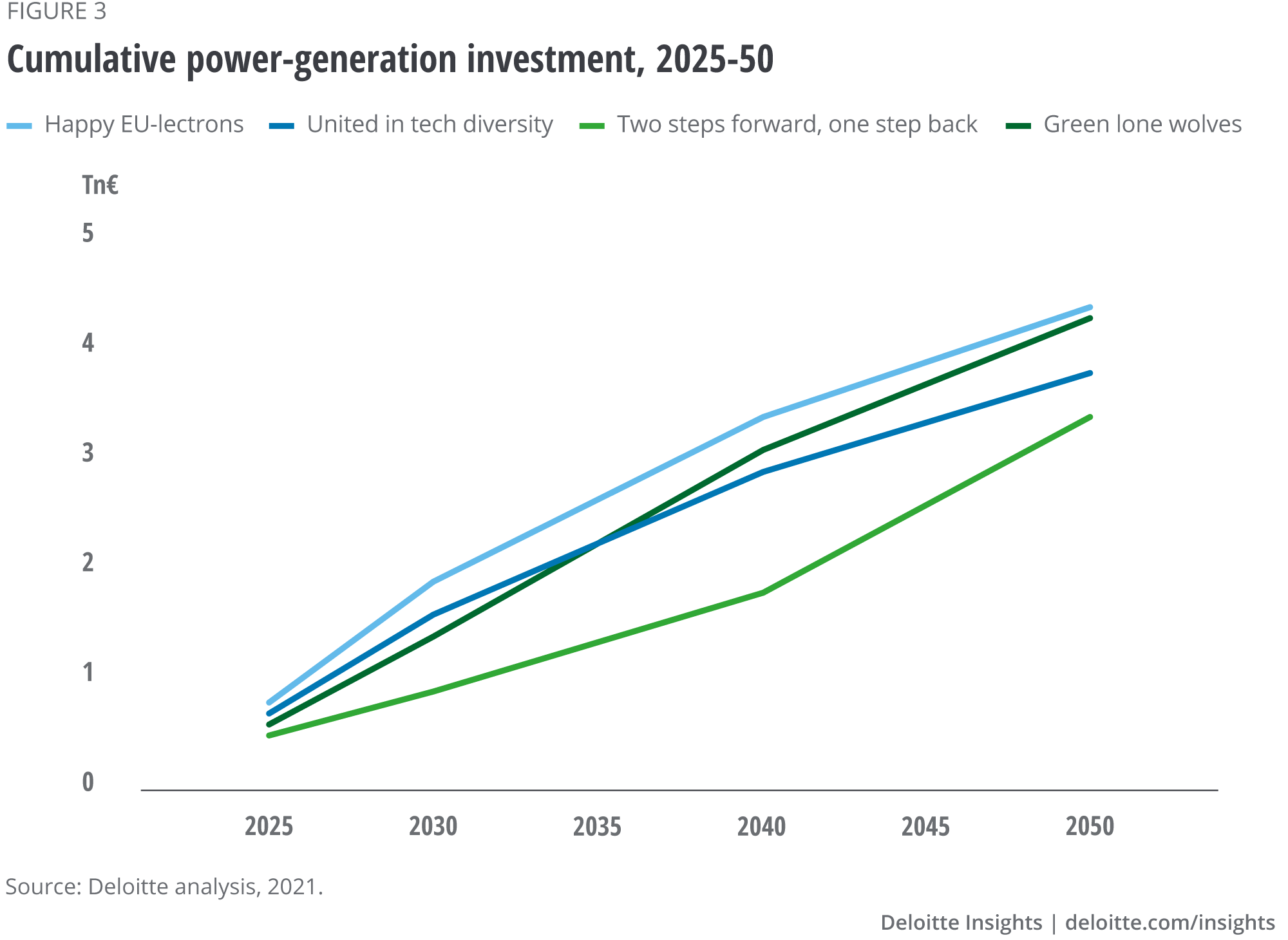

The ongoing development of renewables will see costs fall, while other new technologies, such as batteries, are at the beginning of their development. Falling capital cost for new installations of this technology should, therefore, take some strain off investment needs. Yet, in our outlook, between EUR 3.5 trillion and EUR 4.5 trillion needs to be mobilised over the next 30 years for power generation alone (figure 3). A similar amount will be needed for network infrastructure, so the full scope of the challenge is significant.

The cost reduction for renewables has not yet reached the end of the road; however, investment needs will remain a major challenge.

The “Two steps forward, one step back” scenario is the least favourable for renewables, but even here power generation from solar PV will grow at least fivefold. In the “Happy EU-lectrons” scenario, a world in which renewables thrive, power generation from solar could soar elevenfold to reach more than 1200 TWh by 2050.

Onshore wind generation also grows strongly with output in the “Two steps forward, one step back” scenario reaching 340 TWh, despite NIMBY (“not in my backyard”) concerns slowing deployment. In the “Happy EU-lectrons” scenario, where society has a benign view on widespread wind turbine roll-out, it is projected to reach 1000 TWh.

Offshore wind faces the biggest uncertainty. As it is the most capital-intensive of the key renewable energy technologies, it is more exposed to the economic environment. The output varies between 1100 TWh (corresponding to over 400 GW of capacity) in the “Green lone wolves” and “Happy EU-lectrons” scenarios and 200 TWh (80 GW of capacity) in the “Two steps forward, one step back” scenario.

Power generation from natural gas-fired power plants increases in all but one scenario (“Happy EU-lectrons”) underscoring the important role gas may play as a transition fuel. In that scenario, natural gas faces a ‘golden decade’ through to the early 2030s, as it fills the void left by the coal phase-out. Although the least carbon-intensive of fossil fuels, the long-term future of natural gas is closely tied to the availability of CCS technologies, which develop – in certain countries – in all scenarios, except the “Happy EU-lectrons”.

Many nuclear power plants in Europe were built in the 1970s and 1980s and will reach the end of their lifetime over the outlook period. In addition, some countries (for example, Belgium, Germany and Switzerland) have announced phase-out plans for their nuclear capacity. This decline of capacity is to a degree countered by new programmes in some countries, notably those in Central and Eastern Europe. As such, power generation from nuclear is projected to decline in all scenarios. However, the policy support that nuclear enjoys from some governments, and the possibility it offers to produce large amounts of low-carbon electricity, renders the technology relatively resilient at a European scale.

Another important commonality of the four scenarios is the terminal decline of coal-fired power generation in Europe. After coal phase-out plans were announced all over Western Europe, coal faces policy headwinds in Central and Eastern European countries that have not yet mandated a formal coal exit. Hence, even in a scenario with modest climate ambitions, new coal is not on the cards.

As the contribution from variable renewables to energy generation grows, the system needs to become more flexible in terms of handling demands. There is a large variety of technologies that can deal with (net) load fluctuations and provide system services. These include, for example, gas turbines, batteries, demand-side management or vehicle-to-grid.

Which set of technologies is best suited depends on the scenario: in those with a high degree of electrification – “Green lone wolves” and “Happy EU-lectrons” – wind and solar combined become the largest source of power generation after 2035, and there remains relatively little gas capacity in the system to provide flexibility. Utility-scale batteries thrive in this environment. By 2050, in the “Happy EU-lectrons” scenario, some 100 GW of battery installations – more than the nuclear capacity available today – are scattered across Europe and help balance the grid.

In contrast, the “United in tech diversity” scenario leaves little room for batteries. Fast-ramping gas turbines, supported by a range of flexible technologies on the demand side, ensure the reliability of electricity supply at times of fluctuating renewable power production.

Electric vehicles (EV) are moving to the pole position in the transport sector (at least for passenger cars). Many European governments have announced bans on sales of passenger vehicles with internal combustion engines: for example, the Netherlands from 2030 and France from 2040 onwards. The roll-out of charging infrastructure is also well underway, supported by various national subsidy schemes for the installation of home chargers.

As such, e-mobility adds between 180 TWh and 840 TWh to electricity demand in our outlook, depending on how quickly EVs gain market share and what type of EVs customers prefer. By 2050, more than 220 million EVs could be on Europe’s roads (for example, in the “Green lone wolves” scenario). Even under cautious assumptions on EV uptake – the “Two steps forward, one step back” scenario – EVs may exceed the 50 million mark by 2050.

Another technology burgeoning today and that features prominently in the scenarios is the production of hydrogen via electrolysis. Electrolysers, powered predominantly by renewable electricity, could add up to 840 TWh to electricity demand over the next three decades. Some 230 GW of electrolyser capacity produces renewable hydrogen for end uses that are particularly hard to decarbonise in the “Happy EU-lectrons” scenario. Low-carbon hydrogen can also be produced from fossil fuels in combination with CCS.

Unlike the “Happy EU-lectrons” scenario, “United in tech diversity” combines low-carbon and renewable hydrogen to decarbonise end uses more comprehensively with hydrogen and limit the demand for electrification. Only the “Two steps forward, one step back” scenario sees sluggish uptake of electrolysis (around 30 GW by 2050). Hydrogen remains a relatively expensive decarbonisation option, and this scenario underscores that development of this technology hinges on a clear and conscious policy decision to provide the necessary support.

CO2 prices reflect climate ambitions in the four scenarios. They are highest in the “Happy EU-lectrons” scenario (EUR 170/tonne in 2050), followed by “United in tech diversity” (EUR 150/tonne). These two scenarios rely on the EU Emissions Trading System (ETS) as the key mechanism to provide decarbonisation incentives. The success of the EU ETS depends on strong European cohesion and a coordinated approach to continue strengthening the mechanism.

This support is missing in the “Green lone wolves” and “Two steps forward, one step back” scenarios. CO2 prices reach EUR 100/tonne by 2050 in the “Green lone wolves” scenario as a ‘coalition of the willing’ supports the mechanism while others refrain from its use. Similarly, CO2 prices of EUR 50/tonne (as reached in the “Two steps forward, one step back” scenario by 2050) provide limited incentives for decarbonisation but also keep distortions of industrial competitiveness to a minimum in a globalised economy.

Prices in today’s electricity market are determined by the interplay of a relatively price-responsive supply side (a power plant does not produce if the electricity price does not cover its variable cost) and a very inelastic demand side (most electricity consumers cannot observe real-time power prices). The scenarios suggest that the relative price responsiveness of demand and supply are set to invert. Especially in scenarios with a strong expansion of variable renewables – where generation becomes largely weather-dependent, it is the demand side that increasingly reacts to changes in the value of electricity. Demand-side response, smart grids and vehicle-to-grid are all called upon when the classic supply-side flexibility (gas turbines and batteries) has reached its limits.

In practice, this means the volatility of hourly electricity prices continues to rise. This finding holds for all scenarios although the magnitude of price swings varies considerably. Keeping a significant amount of gas-fired capacity in the system – as is the case in the “United in tech diversity” and “Two steps forward, one step back” scenarios – acts as an effective volatility brake.

The successful electricity trader of the future will, therefore, not only be versed in quantitative methods but also meteorology. As the coal exit progresses, the average price level in our scenarios is largely determined by the combination of natural gas price, CO2 price and the call on gas-fired power plants to serve demand.

The successful electricity trader of the future will, therefore, not only be versed in quantitative methods but also meteorology.

None of the scenarios should be interpreted as an obituary for the energy-only market. However, whether the energy-only market can deliver the necessary investment incentives is not clear either; this depends less on market fundamentals and more on the ability of power companies to hedge extreme volatility and exposure to potentially long periods of low prices. Although the energy-only market is consistent with our analysis, our modelling points to a greater reliance on remuneration for a range of system services.

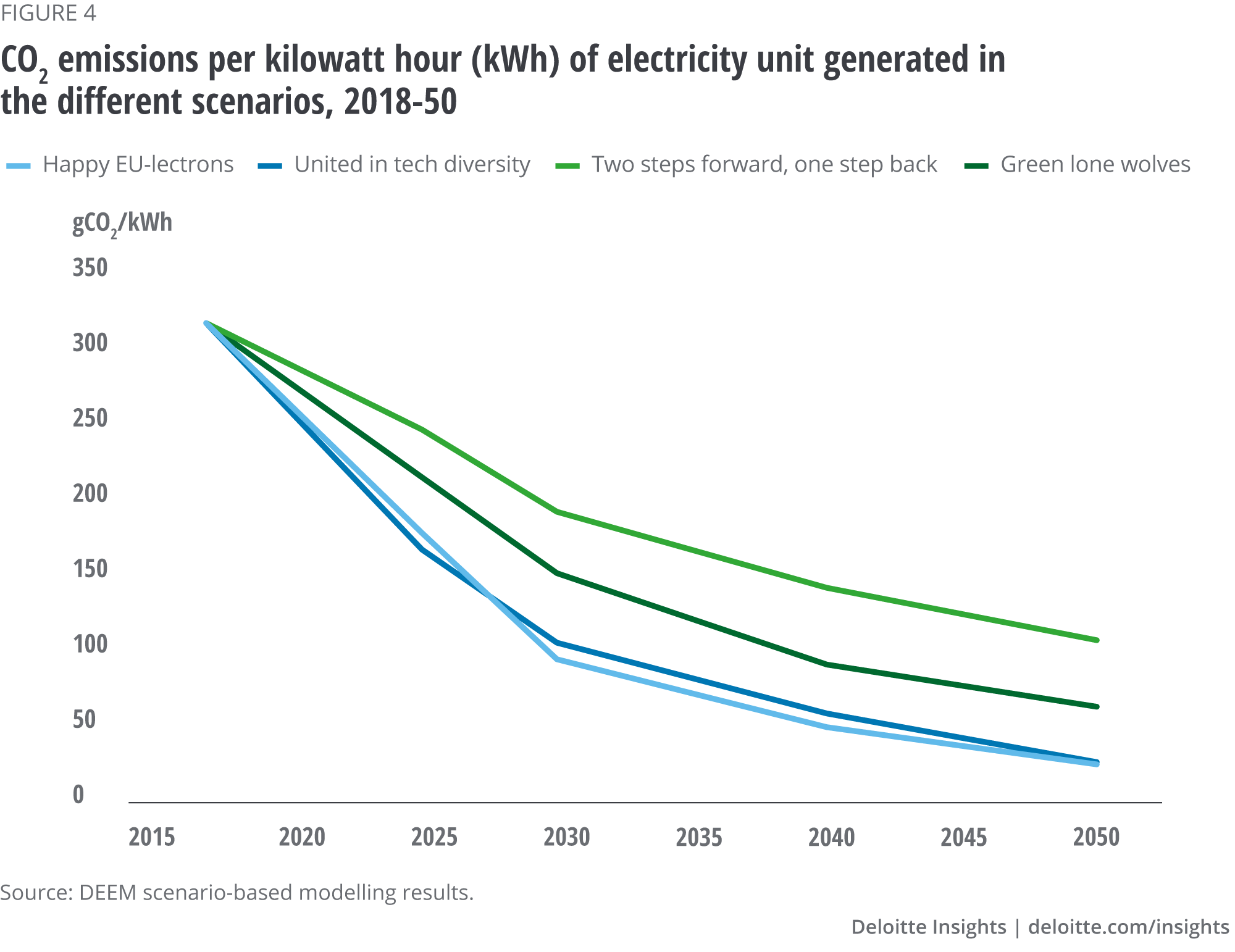

How do the four scenarios fare in terms of deep decarbonisation and delivering on the European Green Deal? The good news is that all scenarios project a marked drop in the CO2 emissions intensity of power generation in Europe (figure 4). Even in the “Two steps forward, one step back” scenario, in which tackling climate change is not a priority, emissions intensity falls by two-thirds to just over 100g CO2/kWh by 2050.

Phasing out coal plants – either due to ageing infrastructure or mandated by policy – essentially allows the power sector to decarbonise ‘by default’. However, this is no reason for complacency: even 100 gCO2/kWh is four times too high for reaching the EU’s climate ambitions. An emissions intensity to the tune of 25 gCO2/kWh is a widely accepted benchmark for Paris Agreement-compliant power sector decarbonisation. This level is reached in both the “Happy EU-lectrons” and the “United in tech diversity” scenarios, albeit with vastly different means, emphasising that many roads lead to Paris.

All four scenarios presented here are plausible, coherent and realistic. This is how they are best used: as a stress test, to play devil’s advocate or as inspiration for strategic decision-making. As such, the objective was also to cover the bulk of the uncertainty range along four distinct paths. What are the main ideas to take away from comparing these four vastly different power sector prospects?

The authors would like to thank Hilmar Franke and Dr. Florian Klein, who contributed both their industry experience and their methodological excellence to the study.

Cover image by: Mark Milward.