Article

Semiconductor Industry Series

Fighting an unprepared battle – Rethinking auto semiconductor strategy in an uncertain era

Deloitte released Semiconductor Industry Series: Fighting an unprepared battle – Rethinking auto semiconductor strategy in an uncertain era. The improvement of underlying technologies are driving transformations in the semiconductor industry, and the rapid development of intelligent vehicles is quietly changing the business and operation models of the automotive industry. The pandemic-induced chip shortage catalyzed the evolution of automotive industry, which also brought unprecedented attention from all players in the ecosystem including governments, industry stakeholders, manufacturers, and even end users. It is particularly critical for OEMs and semiconductor companies, especially local ones, to recognize the need for capability transformations. Going forward, the ability to secure semiconductor supplies to avoid disruptions is a strategic consideration every company should contemplate in the future.

The whitepaper focuses on following four topics:

Overview - New Underlying Technologies Drive Global Semiconductor Transformation, with Strong Demand among Industry Verticals

Insights - The Automotive Industry Is Ready to Embrace Future Opportunities, but Chip Shortage Will Persist in the Short Term

Outlook - Future development trend and Prospect of Automotive Semiconductors

Stratgy Formulation - Reshape the Value Chain of the Automotive Industry and Create a Thriving Ecosystem

Overview:New Underlying Technologies Drive Global Semiconductor Transformation, with Strong Demand among Industry Verticals

Technology Development Drives High Growth in Semiconductor Industry

As underlying technologies such as 5G and IoT continues to mature, they will drive the electrification and intelligent empowerment among downstream verticals and facilitate the steady growth of demand in the global semiconductor industry. The market size of global semiconductor industry is expected to reach USD 630 billion by 2025. Along with technology advancement, several verticals including automotive, industrial, communications, and consumer electronics sectors will undergo industry-wide transformation, which will contribute to further demand for semiconductors. Forecast has shown that chip demand from automotive industry, which expected to grow at 10% CAGR in the next 5 years, will be the main driver of the industry demand.

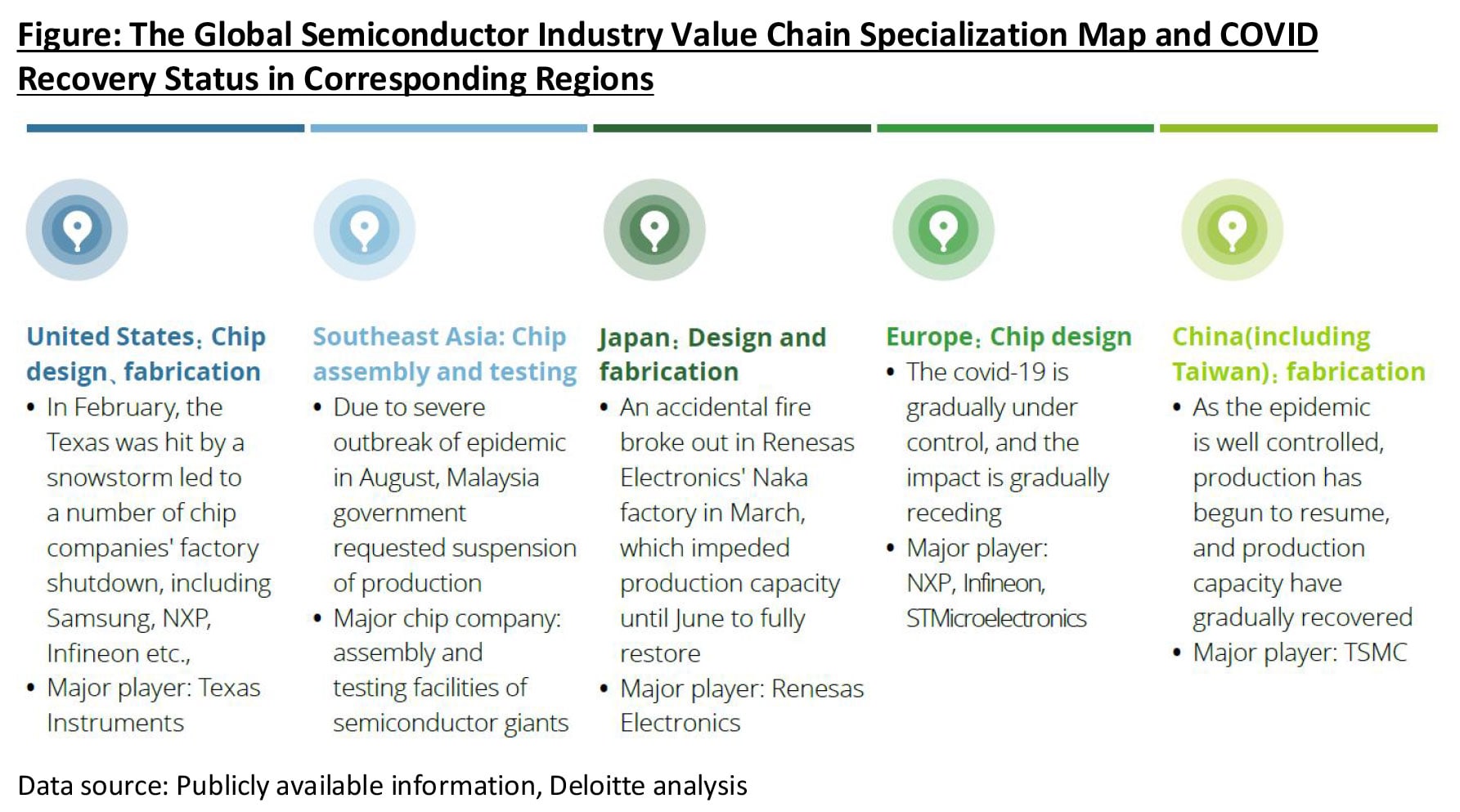

Black Swan Event Constrains Supply-Side Capacity

The spread of COVID-19 since 2020 led to factory shutdowns worldwide. Despite the gradual recovery from the pandemic and subsequent factory reopening, supply-side capacity is still constrained since nations are at different stages of recovery from the pandemic, which restricts capacity.

At the same time, the pandemic stimulates downstream market demand, leading to the peak production capacity of semiconductor enterprises. In the face of strong demand, the imbalance between supply and demand has caused a demand gap.

- Working from home as a result of pandemic has driven the demand for electronic devices such as smart mobile, computers, tablets etc.

- During 2020, global silicon wafer shipment grew by 13.9% compared to 2019, reaching a record high. With the continued pull from downstream demand, average foundry utilization has reached 95% as of Q3 2021, implying limitation in near term capacity expansion.

The semiconductor industry is highly cyclical. The Global Semiconductor Inventory Index is less than 0.9 as of Q2 2021, indicating the global market is in a period of severe shortage.

Insight:The Automotive Industry Is Ready to Embrace Future Opportunities, but Chip Shortage Will Persist in the Short Term

Demand for New Energy Vehicles Will Contributes to Growth of Automotive Semiconductors

- Adoption of electrification and intelligent technologies boost demand for automotive semiconductors

The number of global new energy vehicle sales are expected to exceed 21 million units by 2025, with a five-year compound growth rate of 37%. In addition, the pandemic did not stop future development characterized as CASE (Connected, Autonomous drive, shared service, electrification). The NEV penetration rate of FY2020 shows strong growth among different countries despite the impact of covid-19 pandemic. Based on development goals set force by different countries, new energy vehicles is expected to steadily penetrate markets worldwide.

China is the world’s largest market for new energy vehicles with the highest level of car ownership and acceptance towards intelligent cockpit and autonomous driving.

Features such as intelligent cockpit and autonomous driving have become the key indicator among customers to determine the attractiveness of new energy vehicles in China. With further development of vehicle electrification and autonomous driving technologies, auto-semiconductor is becoming increasingly important.

However, affected by the coronavirus outbreak auto makers lowered demand forecast, hence reduced orders for chip production. At the same time, a surge in consumer electronics demand.

- Mismatch between constrained supply and soaring demand was the biggest trigger for auto-semiconductor shortage in the short term. During the same period, the pandemic stimulated demand for consumer electronics, which took over chips from OEM order cancellations.

- In the first quarter of 2020, for example, global shipments of laptops, TVs, mobile phones, automobiles and servers have increased significantly, with shipments of laptops rose more than 35%. In order to cope with surging demand, OEMs shifted their manufacturing capacity almost entirely to the production of consumer electronics, resulting in the plummet of automotive shipments.

From the supply side, the overall production capacity of automotive-graded semiconductor production line is limited, and manufacturers' willingness to expand capacity for the production line is relatively weak.

- Compares to 200mm wafers, 300mm wafers are mainly used for the production of consumer electronics products including computers, tablets, smart phones; however, since the 300mm wafer production line enjoys higher efficiency, covering a wider range of downstream use cases, foundries invest heavily in 300mm capacity.

- For instance, the production of analog chips is 40% cheaper using the 300mm capacity and in turn bolster gross margin by 8%.

Compared to the overall semiconductor industry, shortage of auto-semiconductors is particularly prominent. According to the forecasts, global vehicle production will be reduced by 8.1 million units in 2021, bringing a total economic loss of $210 billion dollar, with the Chinese market expected to lose about $26 billion dollar.

Domestic Substitution will be An Unstoppable Trend Given Long Term Demand

The primary reason for the current semiconductor shortage is the mismatch between auto-semiconductor market demand and supply in the pandemic environment; therefore, the most effective solution is to expand capacity. However, given the 1-2 years lead time to expand capacity in the semiconductor industry, the shortage is expected to persist until the second quarter of 2022.

In the short term, we have observed a series of responses from traditional OEMs, new entrants and domestic OEMs to alleviate production pressure from semiconductor shortages, with key measure including temporary chip substitution and feature reduction. Although OEMs have come up with various solutions, none is sustainable in the long run. Both temporary chip replacement and feature reduction will further increase R&D cost and reduce consumer confidence to make a purchase.

In the medium to long term, the degree of shortage and response strategy will be different for various types of auto-semiconductors, depending on the level of technology barriers.

- Microcontrollers (MCUs) are in the highest shortage and there are challenges to recovery.

- The shortage of power semiconductors (IGBT) is expected to ease in the medium term.

- The shortage of analog chips for power management and other categories is gradually easing.

Outlook:Future development trend and Prospect of Auto-Semiconductors

Trend 1: Demand for intelligent vehicles drives the value of semiconductors

Compared with traditional ICE vehicles, new energy vehicles increasingly utilize more chips. Take autonomous driving as an example, the higher the level of autonomous driving, the more sensors are required. L3 level autonomous driving carries an average of 8 sensor chips, while the number of sensors required from L5 level autonomous driving reaches 20. By the same token, the degree of information processing and data storage done by vehicles is positively correlated with the level of maturity of autonomous driving technologies, which builds up demand for more control and storage chips onboard. Statistics have shown that the average number of chips in new energy vehicles will reach around 1,459 by 2022, further outnumbering chips installed on traditional ICE vehicles.

Trend 2: Electrically-powered new energy vehicles have higher requirements for electronic components power management and power conversion requirements, which boosts the value of automotive semiconductors

As autonomous driving technology matures, the price of semiconductors in a single vehicle will also rise. According to statistics, the value of automotive electronic components BOM (bill of materials) will increase significantly by 2025, fueled by electronic components used in battery management system and electric powertrain (e.g. inverters, powertrain domain controller DCU, various sensors, etc.).

Trend 3: Domain-centralized Powertrain Electrical and Electronic Architecture drives structural shift in auto-semiconductor

Since the number of ECUs and sensors in the vehicle rises, the cost of the vehicle wiring harness and the difficulty of wiring increase dramatically. It is necessary to reshape automotive electrical/electronic hardware architecture from traditionally distributed model towards more "centralized, lightweight, streamlined and scalable" approaches.

Strategy Formulation : Reshape the Value Chain of the Automotive Industry and Create a Thriving Ecosystem

Policies to Bolster Chip Industry and Make Up for Shortcomings

The Chinese government has devoted its efforts in supporting the semiconductor industry. Throughout the evolution of the industry, government and relevant authorities are increasingly involved with the following key roles: Policy Enabler, Cultivator of Local Champions, Industry Development Strategy Architect and Resource Consolidator and Industry Standard Setter.

OEMs Leverage Different Business Models to Secure Their Supply Chains

Domestic OEMs and semiconductor companies are focusing on developing automotive-grade IGBT semiconductors at the moment before tackling MCU semiconductors, which needs higher technical requirement and industry standard. Companies have adopted two different approaches: self-sufficient strategy and equity investment strategy.

Collaboration among Ecosystem Players to Facilitate High-Quality Growth

The construction of the ecosystem depends on the transformation of the core capabilities of enterprises. In summary, companies should focus on the business model transformation, new capabilities acquisition, digital transformation, and talent development.

Concluding Remarks

The current shortage of automotive semiconductors reflects the vulnerability of its global supply chain. The stable and secure supply of auto-semiconductor is becoming increasingly important. As the "CASE" transformation of the automotive industry continues to advance, semiconductors will enjoy significant improvement both in terms of quantity and performance. Domestic semiconductor companies are expected to embrace a period of rapid growth thanks to support from the government, who deems the localization of automotive-grade semiconductors as a strategic mandate. For all players in the automotive ecosystem, it is important to deepen collaboration and form an open, diversified partnerships to jointly address industry challenges and changes onward.

The journey to realize self-sufficient auto semiconductor epitomizes China's transition from "high growth" development to "high quality" development. The future industry landscape will be volatile, uncertain, complex, and ambiguous. As the boundaries of various industries blur, an open ecosystem and collaboration will be the key winning strategy in the future. All players should work together to build a new ecosystem and stay proactive in the wave of transformations.