Article

Asia Pacific Private Equity 2024 Almanac

Published date: 5 March 2024

Private Equity (PE) plays a pivotal role in the health and growth of economies around the world, and nowhere more so than in Asia Pacific. The share of PE dry powder in Asia Pacific is disproportionately large relative to the region’s PE volumes: Asia Pacific PE dry powder is 23.7% of the global total whereas Asia Pacific PE deals only accounted for 15.2% of global PE deals in 2023 – a clear indication of the increasing momentum of PE capital deployment in the region.

Deloitte is deeply committed to supporting the industry and enjoys a privileged position as a trusted value creation advisor across the end-to-end PE ownership cycle to many of the leading participants in the market – be it deal origination and due diligence or operational consulting through to fund valuations and audits. This exposure and our extensive experience across the sector put us in a strong position to develop unique insights and perspectives on the market and to provide analysis and commentary on market trends and trajectories.

Our aim in producing this Almanac is to provide both a detailed and comprehensive picture of PE activity across Asia Pacific in 2023, and an analysis of the overarching themes that emerged. We have striven to present those trends within the context of recent market history and have also cast our gaze into the future to explore some of the likely trends and influences that we believe will drive activity in the coming year.

Key points of Asia Pacific Private Equity 2024 Almanac

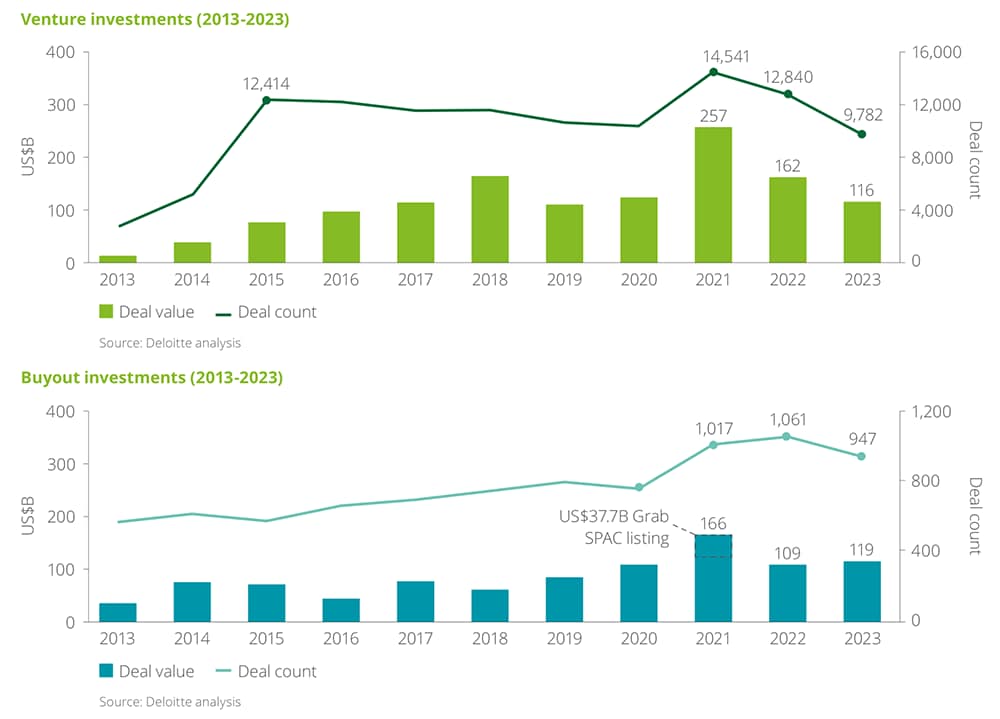

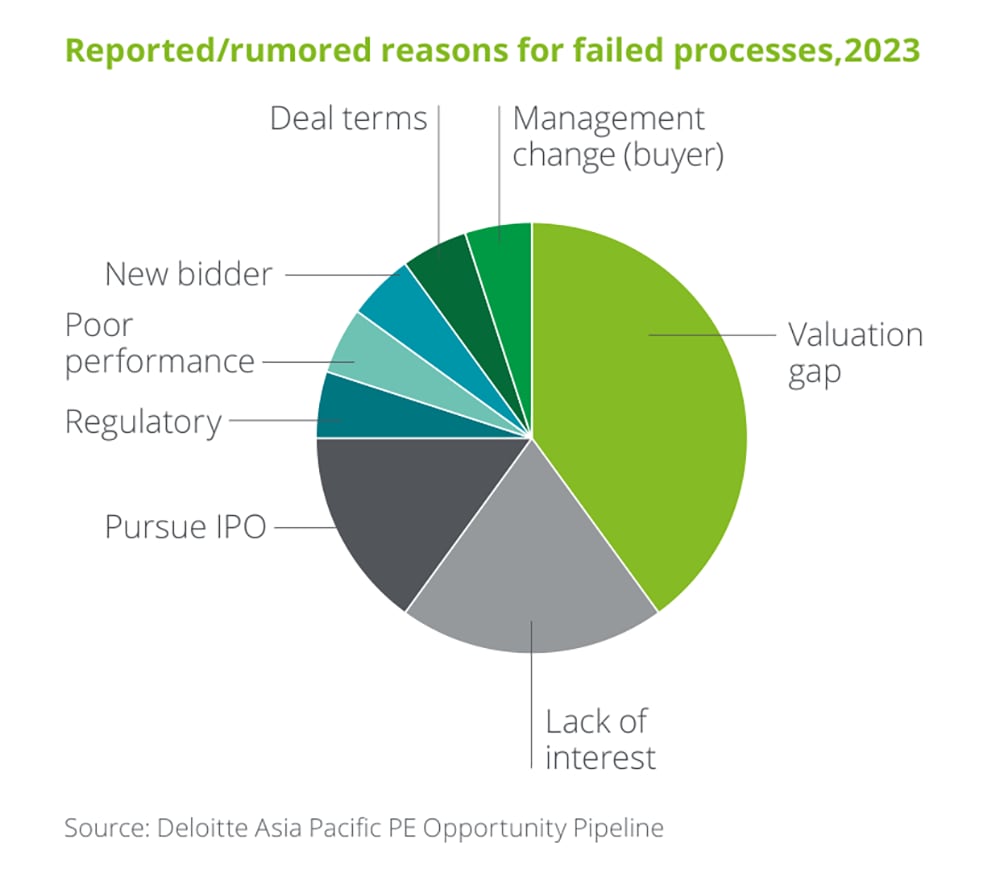

- 2023 was a challenging year for PE: sentiment was low, with an unusually high number of failed deals and transaction volumes down (buyout investments dropped from 1,061 deals in 2022 to 947 in 2023); processes took longer and exits remained challenging (US$60B compared to US$63B in 2022). But despite this, transaction value remained effectively flat (buyout investments of US$119B compared to US$109B in 2022) with a large proportion reflecting portfolio management.

- While operational performance has returned, PE exit valuations have not. Higher interest rates and greater macro-environment uncertainty are eating into the potential returns for financial buyers, whose target hurdle rates have not changed. Inevitably, higher financing costs are driving buyers to lower their potential entry prices, effectively adding a hurdle-rate handicap to valuations.

With many deal processes foundering on this handicap, PE funds are employing softer but slower approaches to asset sales – and different kinds of deals – to avoid the practical difficulties and negative perceptions that accompany a failed process. These dynamics may favour both strategic sellers, for whom price is not the only concern, and strategic buyers, who often require more time to complete a deal. Meanwhile, PE buyers, can make use of less stringent process timelines to explore creative structuring to help bridge the persistent bid-ask valuation gap with sellers, such as partial deals with earn-outs, synergies with existing portfolio, or hybrid debt/equity solutions.

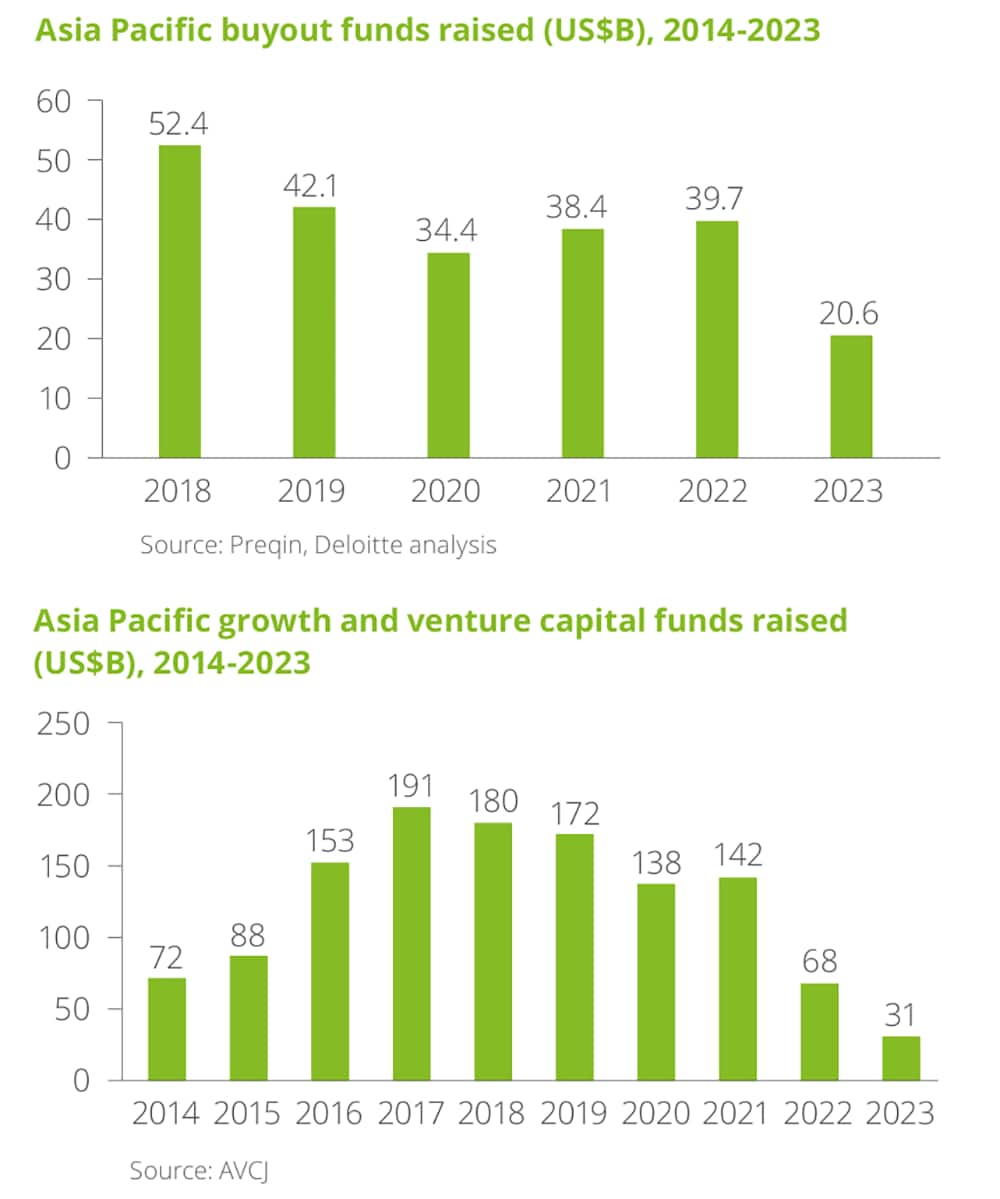

- The fundraising ‘stalemate’ drastically reduced the number of funds closed (385) and dry powder raised (US$63.2B) for Asia Pacific PE funds across strategies (buyout, VC, secondaries, fund-of-funds, and special situations) – a ten-year-low. The longer this stalemate continues, the more vintages that will exist with a limited set of buyout funds. This will mean that as GPs move into exit mode for their older vintages in two, three or four years, there may be meaningfully fewer funds in investment mode competing for deals.

- Interest in China is at a relatively low ebb, at least by recent standards, and PE investors’ view on, and strategies for, China have become varied and divergent. Looking ahead, the same denominator effect that is currently keeping LP money away from PE funds to preserve asset-class diversity in portfolios may serve to push LPs back into China in order to preserve geographic portfolio diversity. In fact, many believe the market has already hit peak pessimism for China and, for those able to invest with conviction, this may be a good time to put money to work there. Either way, investors will not be able to ignore the world’s second-largest economy in their global portfolios.

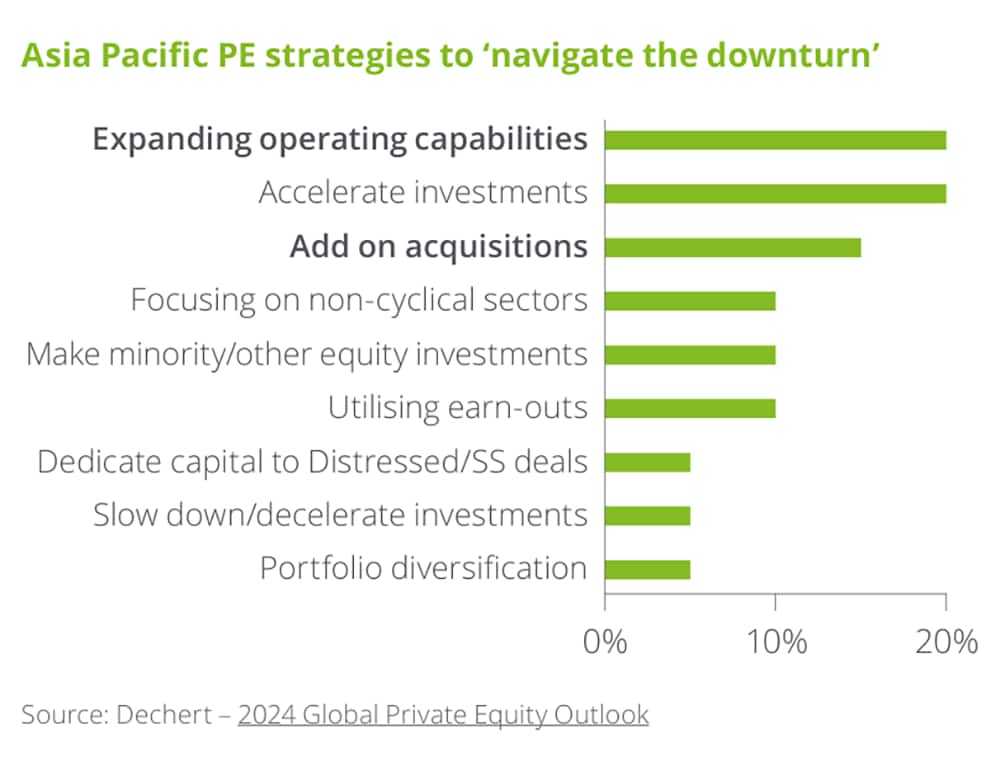

In the face of low transaction volumes and the challenge in achieving satisfactory exit valuations, PE funds are increasingly focusing on driving value through operational improvement and funding dividends via more ambiguous liquidity strategies including continuation funds, partial exits, and strip sales or portfolio sales to secondary funds or fund-of-funds.

We hope you find this both useful and thought-provoking and would welcome the opportunity to contact us to discuss our findings and perspectives in more detail.