Article

China LSHC Industry Survey:2025 State of Industry in China

Published date: 10 March 2025

Deloitte China Life Sciences & Health Care (LSHC) team has conducted the 6th annual “State of industry” survey for the LSHC market in China during January 2025, and we would like to thank the 125 participants this year.

This annual survey covers a number of areas and should be read as a ‘State of Industry in China’, as it covers performance, outlook but also business model and other operating processes changes needed to cope with our environment in China.

China LSHC Business Outlook & Considerations

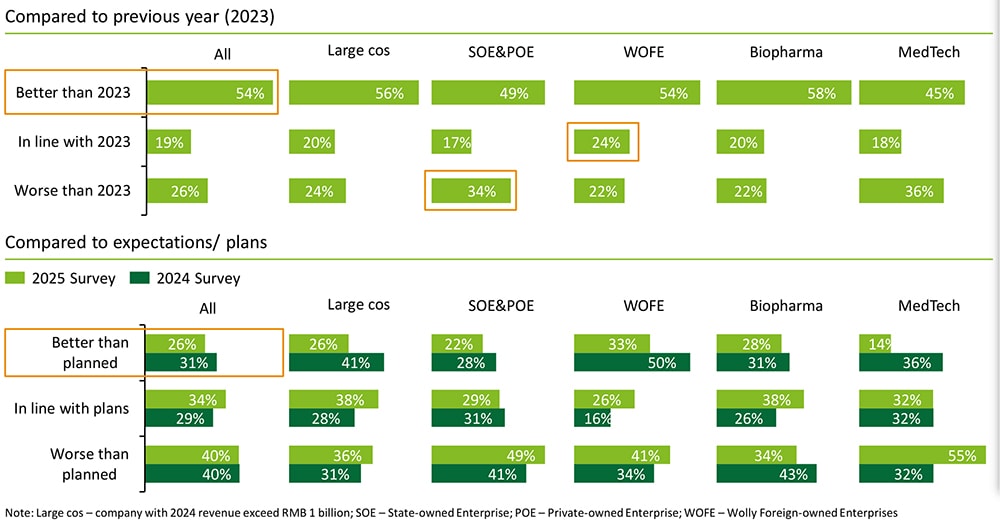

Majority (54%) of companies saw their business performance in 2024 exceeding the prior year 2023, a combined 60% reached plan or better (same as last year) – yet 40% came out worse than expected. To note is, that companies in the Medtech segment experienced a performance significantly lower than expected, compared to the Biopharma’s.

The continuously shortening of the overall economic value cycle and pricing remained the most critical factor for all stakeholders, and launching innovative drugs and technologies was the key focus. Besides, ‘Going-out’ remained important with rising attention to enhanced BD efforts for both local and foreign players.

Q: How did your company perform (top line) in 2024?

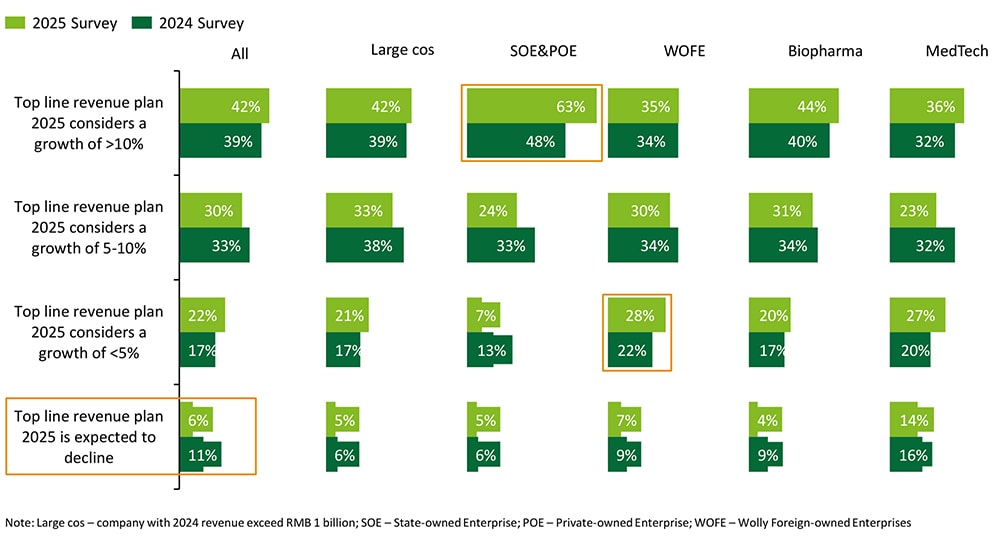

For the 2025 outlook, only 6% are expecting their business to decline, however, Medtech companies have a significantly different expectation as nearly 14% are expecting a decline. Local industry players show the most ambitious and bullish, while foreign companies are showing an unchanged expectation, with 65% expecting a growth higher than 5%. But in details, one can read that overall cautiousness prevails, as more foreign companies consider a growth outlook up to 5% only, while a year ago expectations were higher to growth beyond and up to 10%.

Q: How do you foresee your China business outlook 2025?

New regulatory and technology impact

The survey crystalizes once again, that the regulatory framework has become more critical to both local and foreign players in China. Nearly half of respondents feel the regulatory framework in China has intensified during 2024, particularly to large and local players. Then, the escalating impact of data privacy concerns and export restrictions is contributing to further emphasis in the development of C4C solutions.

Also important to note is that, the boom of AI and various smart technologies is impacting all players throughout the total value chain (page 16 of report). For SOE/POE players, the use of new technology and global partnering is more critical than market access (funding of R&D).

New business investment shifts

The development of ‘new channels’ remains crucial for all stakeholders, especially for local players. As we are seeing intensified local competition as domestic innovation capabilities are elevating, we have also seen a wave of investments throughout the value chain. Around two-third of respondents have indicated to have increased R&D localization efforts, and over two-third of respondents have increased overall supply chain localization investment, particularly local players. (Page 19 of the report)

As China continues to be a favored investment destination given its market size, yet many are now adopting a more cautious approach. Local players are seeking for new assets and partners under the ‘going-out’ trends and higher commercial pressure. The ROI assessment for investments in China become increasingly crucial for all, ensuring the right R&D investment and import of ‘originally’ innovative assets are the top priorities. (Pages 21 to 22 of the report)

In conclusion

Going forward crafting a more precise value proposition, becomes essential in order to win in the China market. Companies are exploring new value creation methods and embracing flexible partnerships and deal models, perceived as important to long-term success in China. All industry players in China, will need to reassess their market strategy, to develop a China-tailored approach for managing the lifecycle of innovative assets and ensure to strengthen digital capabilities, to fully utilize local smart technologies. This strategy refresh is critical and essential for market victory in China.

A total of 125 valid questionnaires were collected from industry executives and investors, among who nearly 70% are C-level and above. The majority of the company types are WOFE and POE (accounted for 56% and 25%respectively), and the industry sectors mainly covered from biopharma to distributors (accounted for 90% in total). Among all the companies surveyed, over half of them with revenues more than RMB 1 billion.

Note: [1] Large cos: company with 2024 revenue exceed RMB 1 billion; [2] SOE: State-owned Enterprise; [3] POE: Private-owned Enterprise; [4] WOFE: Wholly Owned Foreign Enterprise; [5] HC: Healthcare