Analysis

Future of Trust Survey Results in China LSHC Industry

Published: 11 January 2022

2021 Survey for Future of Trust in China LSHC Industry

- The survey was conducted from 1st to 15th November 2021

- Engaged a total of 68 China based life sciences & healthcare (LSHC) operators and investors

Trust: Key stakeholders and their perceptions

Which stakeholder’s trust is most important for your company’s success in China

Insights

- In this highly regulated industry, external stakeholders are leading in importance, and the most important stakeholders are government authorities & regulators

- Medical practitioners, essential for successful product adoption and usage are highly ranked as well

- Reliance on ‘Media’ as a resource to build trust is considered to least effective

- For domestic (SOE & POE) companies, interesting to note a slight gap in importance: staff & employees, exec. committee mgt. team members, board members, and media

- CEOs take the trust from staff & employee and patients more importantly compared to others

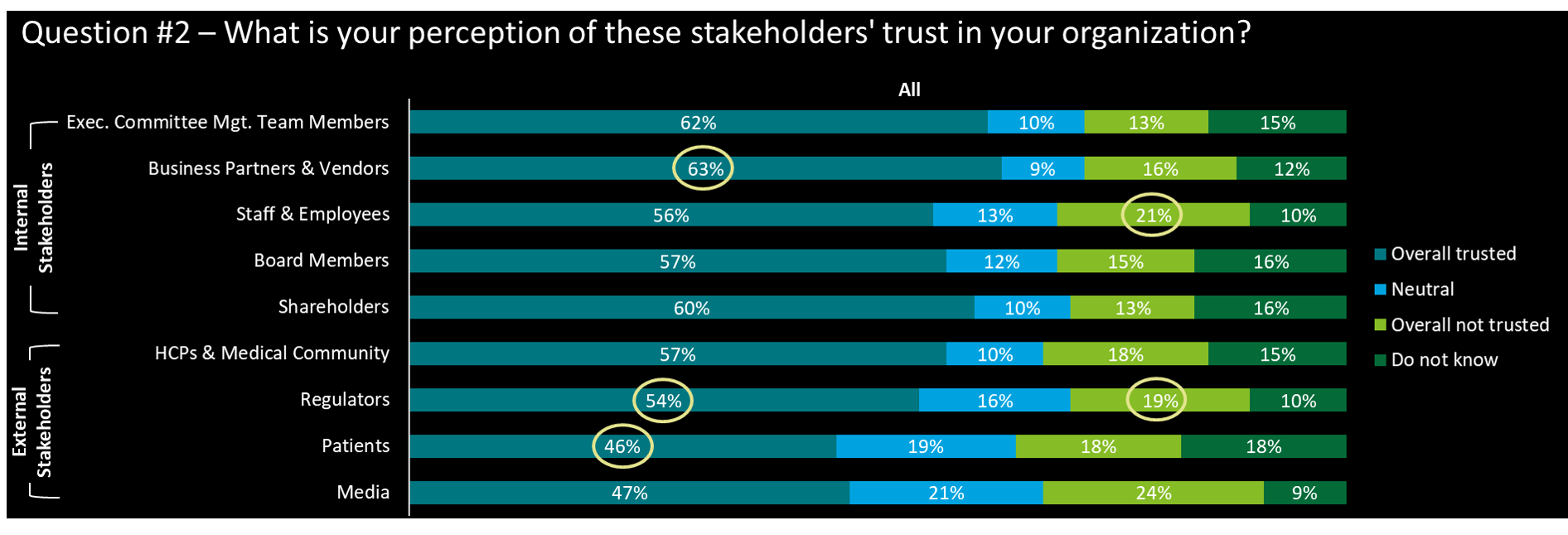

The opposite view: How is your organization viewed

Insights

- Business partners have the highest trust assessment in the organization, as many organizations have formal processes to select their partners

- Regulators and patients – are among the lowest rankings of perceived trust (however, CEOs ranked regulators’ trust at 66%, indicating better trust perception)

- Employees & staff have the 2nd highest mistrust perception

- We have noted that among those that selected ‘Do not know’, ca. 34% are C-level respondents, which indicates a number of companies have no – or at least unknown - internal risk (trust) assessment maps in place

- From the industry perspective, med-device cos perceived overall higher trust from all types of stakeholders compared to pharma cos and all others

- Surprisingly, the perceived ‘not trust’ from Regulators by pharma cos (22%) is distinct from med-device cos (7%) (C-level’s have by 18% only)

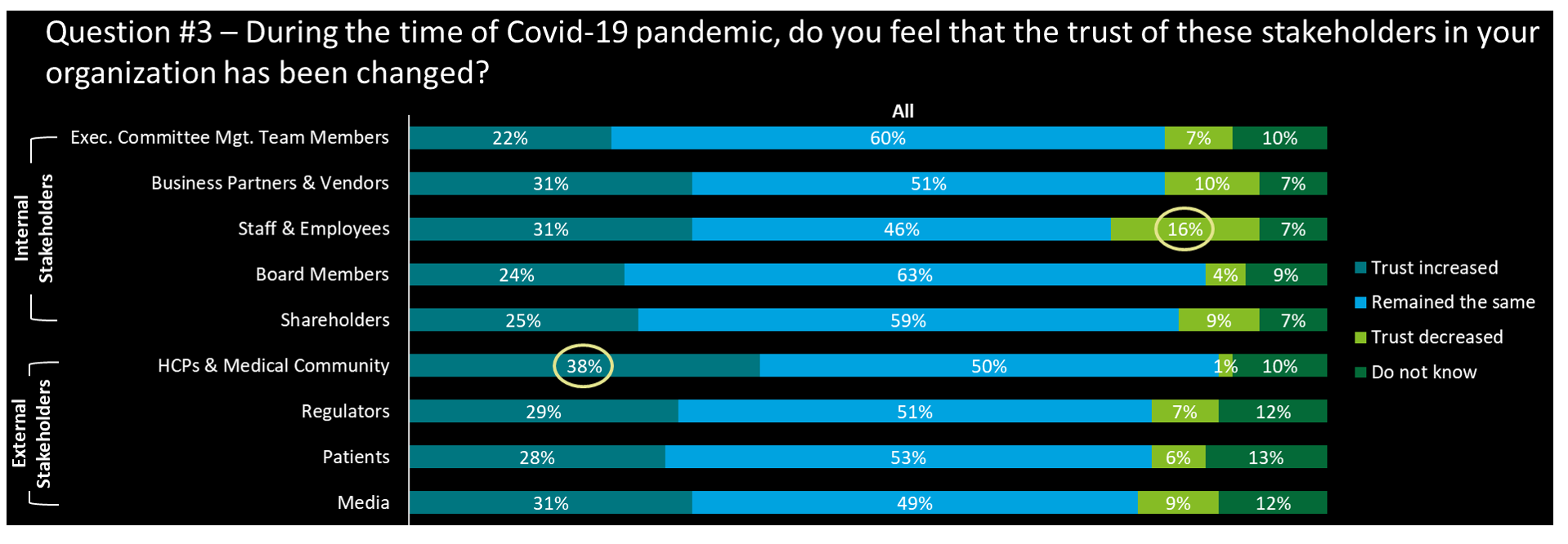

How has Covid-19 time impacted the trust from stakeholders

Insights

- In general, the COVID-19 pandemic made less impact on the trust changes across all types of stakeholders with around 50% of respondents all choosing ‘remained the same’ for all types of stakeholders

- The trust in ‘HCPs & medical community’ has the highest ratio in ‘trusted increased’ and lowest ratio in ‘trusted decreased’ at the same time, thanks to the fast-response and great contribution from LSHC players that supported a lot to HCPs and medical communities regarding the disease control

- Trust from staff & employees shows the highest decrease, linked to the work habits adjustments that were implemented during Covid-time. However CEO’s have responded (56%) that trust from their staff & employees has by large ‘increased’ (and 0% decreased)…. An interesting misalignment

- JV has the highest ‘trust decreased’ ratio (33%) in business partners & vendors, staff & employees, and shareholders, which is quite the opposite to large cos and WOFEs, showing that the trust management from internal stakeholders for JV still needs to be improved

Trust: Actions and resources to manage

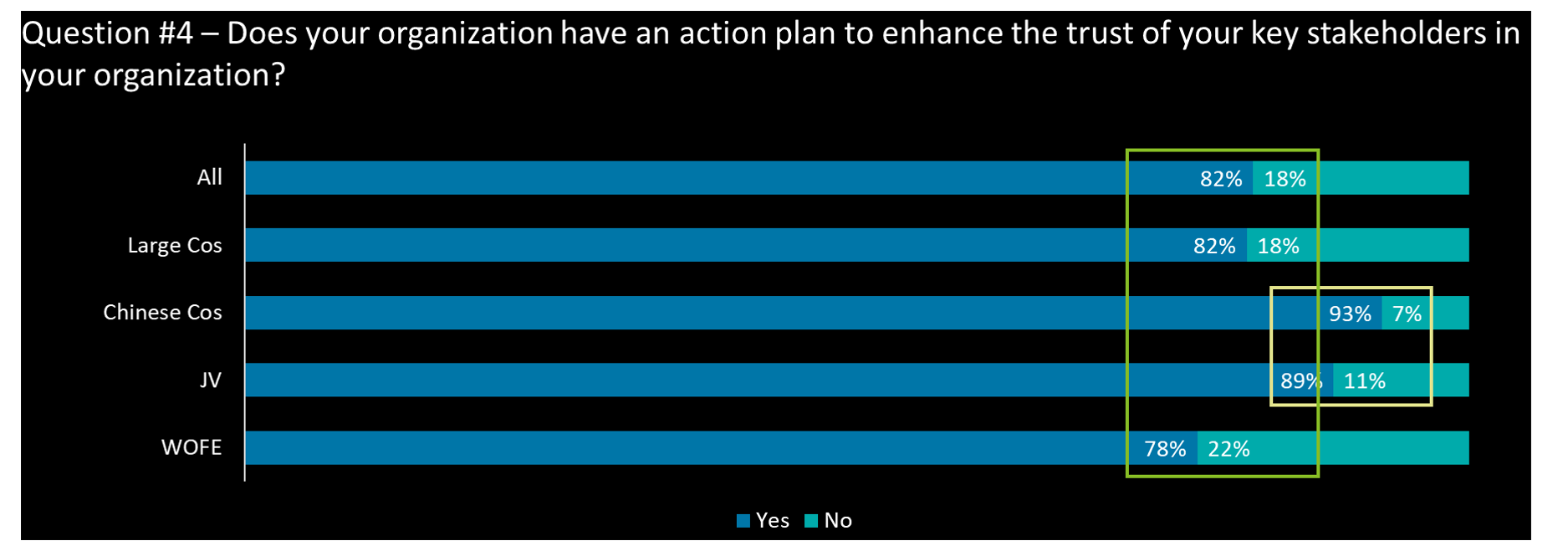

What are organizations doing to enhance trust

Insights

- Overall, most respondents’ companies (82%) have plans to enhance the trust of key stakeholders; WOFEs seem to be lagging behind – i.e., 10 out of 45 have responded negatively

- For all respondents, there is alignment with the stakeholders considered critical for success and an action plan: Regulators and HCP’s

- Domestic companies (SOE & POE) rank ‘Patients’ as their 1st priority action

- Large companies, pharma cos, and WOFEs have recognized ‘staff & employees’ as critical for the trust related action plan going forward

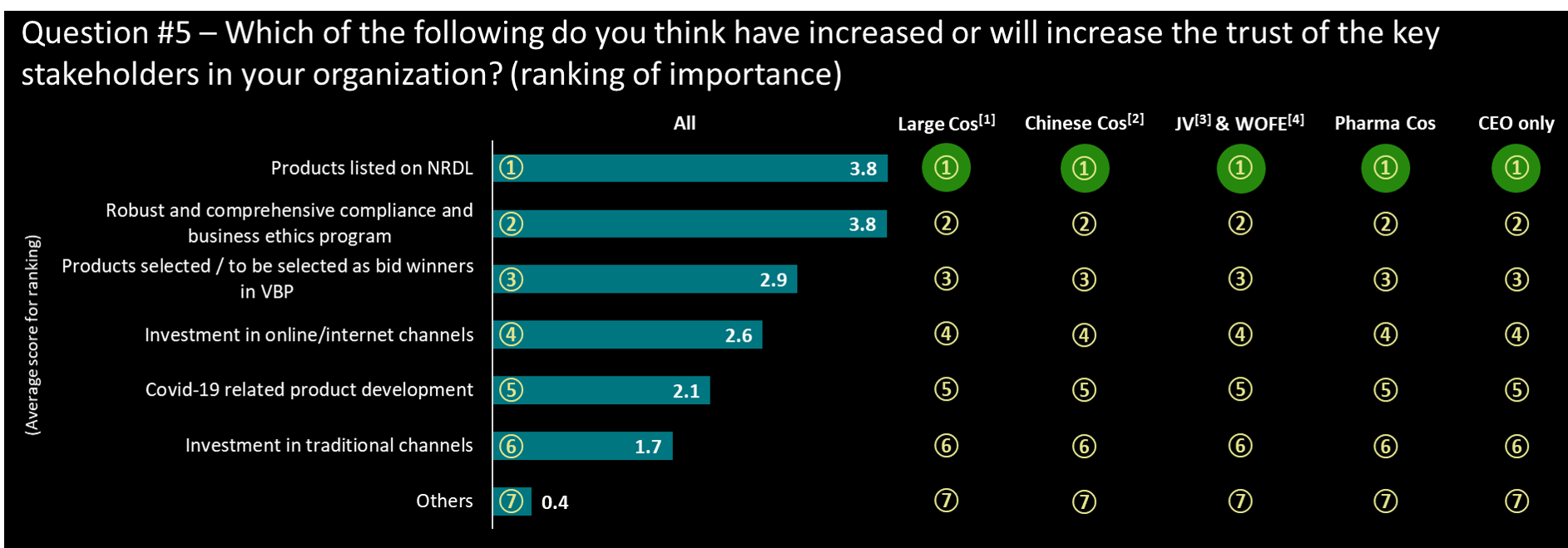

What external trust element will influence stakeholders

Insights

- NRDL listing and internal compliance programs are the top two key drivers in enhancing the trust of the key stakeholders for all respondents

- CEOs make the exact same assessment and ranking

- Investment in traditional channels (Hospitals, offline…) is perceived having the least impact on increasing trust with stakeholders

- Others topics mentioned included: increase physical engagement, promote more local R&D innovation or build stronger CSR projects

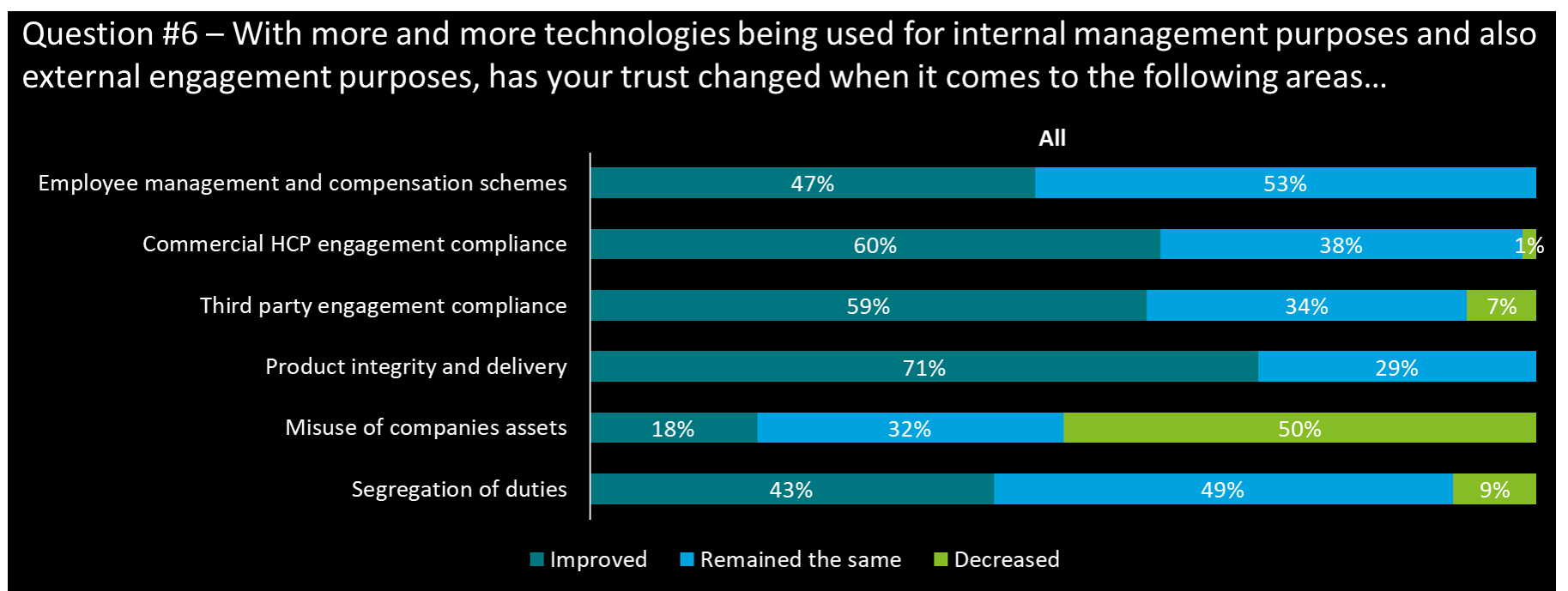

Does technology help in improving trust

Insights

- Targeted compliance programs (HCP, 3rd Party engagement) have increased trust in processes and behaviors. However a majority of CEOs (only) evaluate that the compliance programs have actually remained the same with new technologies.

- Product integrity and delivery stands out for the use of more technologies to increase trust (tracing, proof of origin …)

- The misuse of corporate assets has very significantly decreased with the roll out of monitoring technologies

- CEOs interestingly view that the HCP engagement with new technology has not modified the trust in the relationship (56% remained the same); In contrast, their view in product integrity and delivery with new technology has improved the trust significantly (89% with trust improved)

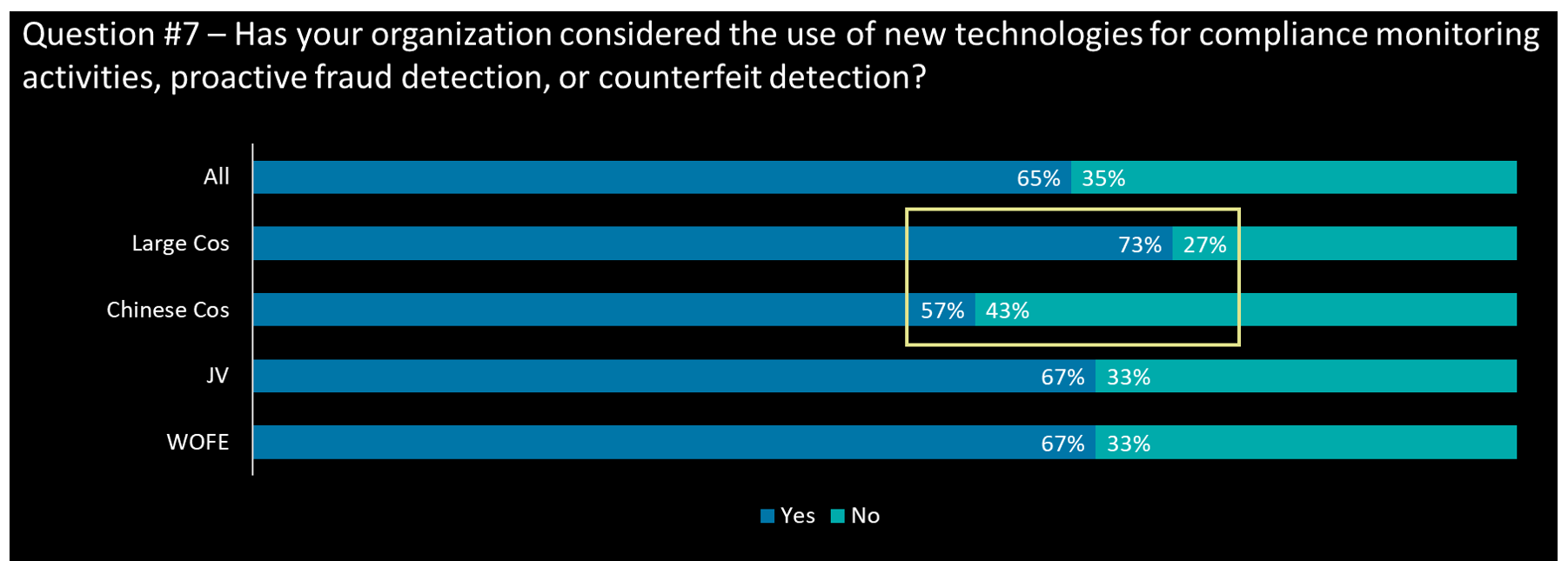

How do you expect to use technology going forward to increase trust

Insights

- Over half of all respondents’ companies have considered the use of technologies for compliance and fraud related monitoring; large cos have the highest proportion while Chinese cos have the lowest in the new technology adoption consideration

- Nearly 70% of respondents’ companies prefer to apply advanced analytics related technology, especially for JV (83%)

- Chinese cos and JV are having a higher willingness in adopting robotic process automation as they usually run local manufacturing sites in China

- Over 55% of large cos and WOFE have applied or planned to apply while less than 40% in Chinese cos and JV

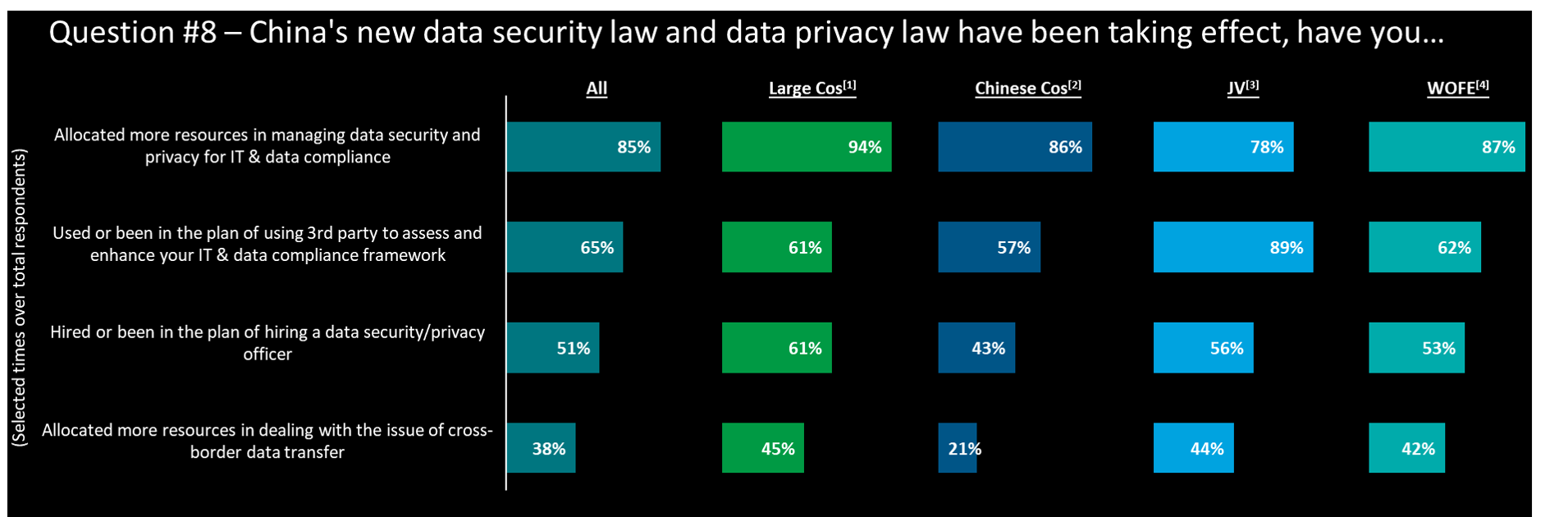

How does China’s data regulatory framework impact

Insights

- The new data security law and data privacy law have significantly increased the resource allocation in IT & data compliance. For Pharma Cos (34/37) emphasize this area as the highest priority.

- Unsurprisingly, foreign invested companies (JV & WOFE) are focusing significantly on x-border data & IT arrangement. CEO’s (only) responses seem to indicate that they believe this is already dealt with appropriately (only 10% cite this as a priority)

- Partnering with 3rd parties and investing into specific resources, i.e., ‘Chief Data Officer’ is top in mind for many

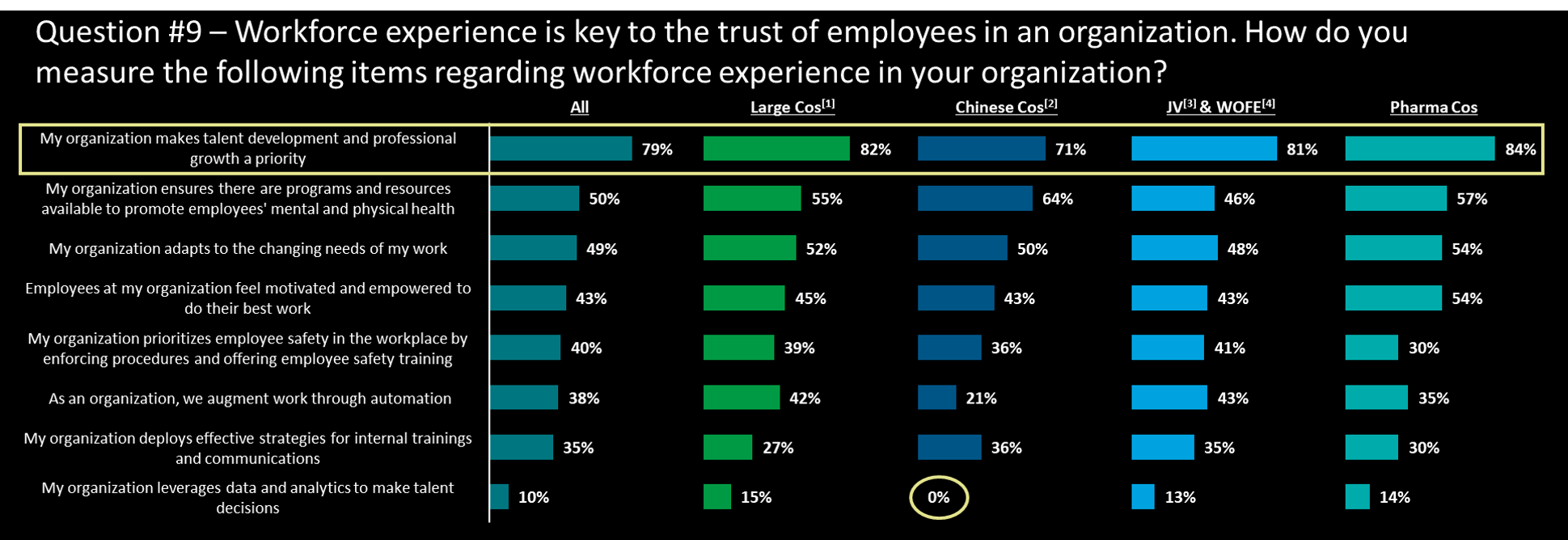

Talent and trust – is this a management priority?

Insights

- The caring (50%) and development (79%) for talents are the top priority for all types of companies, especially in professional growth

- Pharma cos has the highest % (54%) in the employee motivation in works, contrast from the % in JV (22%)

- On the other hand, pharma cos have the lowest % (30%) in the workplace safety, where JV&WOFE has the highest % (41%), showing a different focuses in workforce management

- Surprisingly, all types of companies are having the lowest % in leverages data in talent decisions, especially 0% in Chinese cos

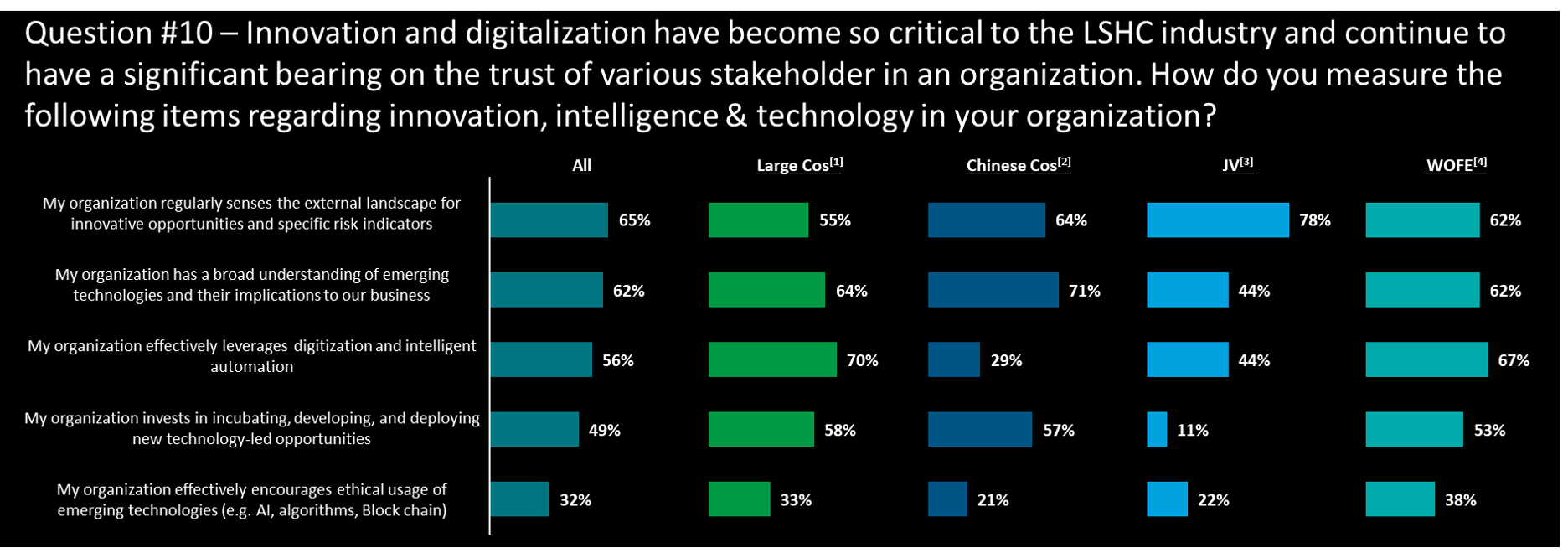

Innovation and trust – is this a management priority?

Insights

- Over 60% of companies are regularly sensing the digital innovation opportunities and implications to their works, especially in large cos (55% & 64%), Chinese cos (64% & 71%), and WOFE (62% & 62%) yet only 44% of JV thinks their companies have a board understanding in digit-tech implication

- In addition, JV also has an extra low % (11%) in investment in new tech-led opportunities, which may result in a latter in capturing the digitalization opportunity compared to others

- Chinese cos have an extra low % (29%) in digitization and intelligent automation while large cos and WOFE have over 65%, making a clear differentiation in automation development among company types

Notes: [1] Large Cos – Companies with revenue larger than 2.5 Bln RMB; [2] Chinese Cos – Chinese state-owned enterprises and private-owned enterprises; [3] JV – Joint venture with foreign investment; [4] WOFE – Wholly foreign-owned enterprise; [5] NRDL – National Reimbursement Drug List; [6] VBP – Volume-based Procurement

Summary Insights and the future

Key insights summary

- Regulators ranked as the most important stakeholder in terms of trust yet was the last second one in terms of perceived trust, i.e., just 50% of respondents believe regulators trust their organizations.

- To CEO respondents, Staff & Employees was ranked the 2nd important stakeholders but assessed this group to be the one with lacking trust as most.

- Despite the new-tech in compliance is ranked 2nd for trust enhancement, over 50% of CEO respondents believe it didn’t improve the trust in the HCP and third-party compliance activities.

- Pharma cos are ranked as 1st in employee motivation and empowerment, yet it also ranked the 1st in trust decreased during the pandemic for Staff & Employees.

- Med-device cos believe that they have perceived trust from internal stakeholders over external ones, yet they value the external trust more important for business success.

- For nearly all CEO’s (8/9) and a large majority of all respondents (70%), the use & deployment of new technologies increases the trust in drugs (integrity & delivery).

- 90% of Pharma and large cos are allocating more resources to data security and privacy compliance, while only 40% consider cross border data exchange requires more resources.

- Chinese cos are ranked as the last place in automation deployment across both workforce (21%) and digitalization (29%).

Future outlook

The trusted relationship with external stakeholders[1] are essential to all LSHC players in China

- Similar to many countries, China market is highly policy-driven, and regulators have been particularly active in recent time, requiring even more attention than ever to build trust with industry players (NRDL[2], VBP[3], etc.).

- External stakeholders (except media) are the most valued ones to LSHC players for trust relationships, yet with a relatively weak trusted relationships, driven by compliance & business ethics issues.

The trust with government authorities, HCPs, and patients are gaining more attention resulting from the speed up of the ‘Healthy China 2030’ plan

Notes: [1] External Stakeholders – HCPs & Medical community, Media, Patients, Regulators; [2] NRDL – National Reimbursement Drug List; [3] VBP – Volume-based Procurement

The new technologies have led to a differentiated trust landscape for various stakeholders

- China LSHC players are aiming to increase trust through new technologies, such as IT and data compliance, advanced analytics for fraud, counterfeit detections, etc.

- The rapid digital development has raised the trust issue in clinical data security, patient privacy protection, ethical usage of emerging technology.

With patients becoming ‘technology savvy consumers’ , digital technology will continue to raise the concern in data privacy and require highest attention to safeguard that trust

Employee trust while creating a healthy environment for both employee and company to grow

- From the study, most LSHC companies have their own focuses on enhancing the workforce experiences, aiming to shape an environment and phenomenon for talent development and professional growth.

- To enhance the trust from staff and employees, companies are supporting the employees in adapting to the rapidly changing China LSHC market in both skillset level up and their mental and physical health.

Talents are the foundation of the company, timely adjusting the employee development plans is the necessity to secure the staff and employees’ trust