News

IRD's latest views on Foreign-Sourced Income Exemption (FSIE) regime

Hong Kong Tax Newsflash

Published date: 17 July 2024

The Inland Revenue Department (IRD) has recently updated its website, incorporating a number of frequently asked questions (FAQs) and illustrative examples regarding the Foreign-Sourced Income Exemption (FSIE) regime. These updates reflect the IRD’s latest views on the application of the FSIE regime. This newsflash highlights some of the key FAQs that taxpayers should pay attention to.

Tracking of FSIE income used for acquiring overseas property

The IRD clarifies that if a specified foreign-sourced income (FSIE Income) is used to acquire an overseas property, whether movable or immovable, and that property is subsequently sold, the sales proceeds will still be regarded as the original FSIE Income. Hence, these funds must be tracked. When the sales proceeds are remitted to Hong Kong, the original FSIE Income would be regarded as received in Hong Kong and chargeable to profits tax in Hong Kong in case the conditions for tax exemption1 are not satisfied. On the other hand, the foreign-sourced disposal gains or losses arising from the subsequent disposal of such property would be considered as separate FSIE Income.

Our comments

Given that movable and immovable property effectively encompasses all types of assets, including shares or equity interests, the use of FSIE Income for the acquisition of any asset is thus subject to tracking if the tax exemption condition is not met in the year of accrual. According to the IRD's latest view above, it appears that continuous tracking of the FSIE Income would be required, no matter how many times such unremitted proceeds are reinvested to acquire other property. The original FSIE Income would be taxable when the funds are subsequently received in Hong Kong even though the subject income was accrued many years ago, regardless of the time bar period. The tracking becomes even more complex if the property is sold and the proceeds are used to acquire other property, resulting in another FSIE Income (i.e., disposal gain). In practice, it is challenging to keep track of the fund from FSIE Income after it has been used to acquire other property. The tracking obligation is onerous and would increase the compliance burden of taxpayers. We hope the IRD will take a pragmatic approach and consider providing a time limit or restrict the number of subsequent transactions for tracking purpose.

Pure equity-holding entity2 status not accepted for part of a year

IRD clarifies its position on determining whether a company is a pure equity-holding entity when its status is changed during the year. The scenario presented involves Company A which initially held certain debts and equity interests. During the year ended 31 December 2023, Company A disposed of all the debts and only held equity interests afterwards.

The IRD’s position is that since the company held debts at some point during the basis period of the year of assessment, it could not be regarded as a pure equity-holding entity for that year of assessment, even though all the debts were disposed before the year-end. Thus, the reduced economic substance requirement would not apply to it.

Our comments

Holding of debts at any point within the basis period of the year of assessment would taint the pure equity-holding entity status for that year of assessment. Taxpayers should ensure that they maintain adequate economic substance for that year, as the reduced economic substance requirement would not apply to them in such cases.

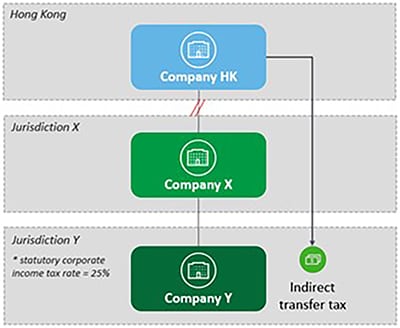

"Subject to tax condition" taking into account of foreign tax on indirect transfer

Company HK disposed of its equity interests in Company X, located in Jurisdiction X, resulting in an indirect transfer of Company Y in Jurisdiction Y. Consequently, Company HK is subject to indirect transfer tax (which is a corporate income tax) on the indirect disposal in Jurisdiction Y. The statutory corporate income tax rate in Jurisdiction Y is 25%.

The IRD indicates that in determining whether the “subject to tax condition3” is satisfied, the tax may not necessarily be charged in the jurisdiction where the investee entity is located. As such, the corporate income tax charged in Jurisdiction Y on the indirect transfer of Company Y, resulting from the disposal of equity interests in Company X, would be taken into account in determining whether the "subject to tax condition" is satisfied in respect of the disposal gain arising from Company X. Given that the headline tax rate in Jurisdiction Y is higher than the reference rate of 15%, the "subject to tax condition" would be regarded as satisfied.

Our comments

We welcome the IRD’s position in taking into account of the foreign tax on indirect transfer for the purpose of the "subject to tax condition".

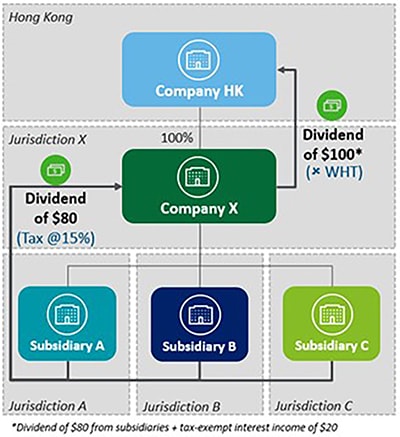

Apportionment approach not allowed for "subject to tax condition"

Company HK received a dividend of $100 from its wholly-owned subsidiary, Company X, which is located in Jurisdiction X. The dividend was not subject to any withholding tax in Jurisdiction X. The underlying profits out of which the dividend was distributed by Company X to Company HK consisted of:

a) dividend received by Company X from its subsidiaries in the amount of $80, which had been subject to corporate income tax at a rate of not less than 15% in a territory outside Hong Kong; and

b) interest income of $20 which was tax-exempt in Jurisdiction X.

The IRD considers that the "subject to tax condition4" would not be regarded as met in this case for the following reasons:

i) The subject dividend was not subject to tax in Jurisdiction X.

ii) The amount of the underlying profits (i.e., the profits of Company X) of the subject dividend which had been subject to a qualifying similar tax (i.e., $80) is smaller than that of the subject dividend (i.e., $100).

iii) There is no information showing that any related downstream income of the underlying profits (i.e., profits of Subsidiaries A, B and C) had been subject to tax.

The IRD will not allow an apportionment approach by accepting the portion of dividend that was paid out from item (a) above (i.e., $80) as having met the "subject to tax condition".

Our comments

In the above example, even though a portion of the underlying profits (i.e., dividend $80) have been subject to tax in a territory outside Hong Kong, the IRD adopts an "all or nothing" stringent approach with no room for apportionment. The entire amount of the subject dividend (i.e., $100) fails to meet the "subject to tax condition" and hence not qualified for the participation exemption. Taxpayers should be mindful of the "subject to tax condition" when determining the amount of dividends to be distributed.

FSIE regime has been implemented for more than 1 year. More and more complications arise. The IRD continues to provide updated guidelines. We will keep track of the updates. Taxpayers should seek professional advice in handling their FSIE matters.

1 Tax exemption conditions refer to economic substance requirements, participation requirements or nexus requirements.

2 Pursuant to Section 15K(3), pure equity-holding entity means an entity that only holds equity interests in other entities, and only earns dividends, disposal gains and income incidental to the acquisition, holding or sale of such equity interests.

3 The "subject to tax condition" is an anti-abuse rule under the participation exemption. If the FSIE Income is a gain derived from disposal of equity interests in an investee entity, the participation exemption only applies if the disposal gain is subject to a qualifying similar tax in a territory outside Hong Kong at an applicable rate of at least 15%.

4 Where the "subject to tax" condition is to be met in relation to a dividend, the dividend, the underlying profits or related downstream income of the profits is subject to a qualifying similar tax outside Hong Kong, the amount or aggregate amount of such profits or income must be equal to or larger than the amount of the dividend.

Tax Newsflash is published for the clients and professionals of Deloitte Touche Tohmatsu. The contents are of a general nature only. Readers are advised to consult their tax advisors before acting on any information contained in this newsletter.

If you have any questions, please contact our professionals:

Authors

Doris Chik

Tax Partner

+852 2852 6608

dchik@deloitte.com.hk

Carmen Cheung

Senior Tax Manager

+852 2740 8660

carmcheung@deloitte.com.hk

Kiwi Fung

Tax Manager

+852 2258 6162

kifung@deloitte.com.hk

Tax & Business Advisory

Southern Region Leader

Jennifer Zhang

Tax Partner

+86 20 2885 8608

jenzhang@deloitte.com.cn

Southern Region Deputy Leader

Raymond Tang

Tax Partner

+852 2852 6661

raytang@deloitte.com.hk