Article

CBAM and its implications for companies in China

Sustainability Spotlight Series No.50

Publish Date: 10 October 2022

Background

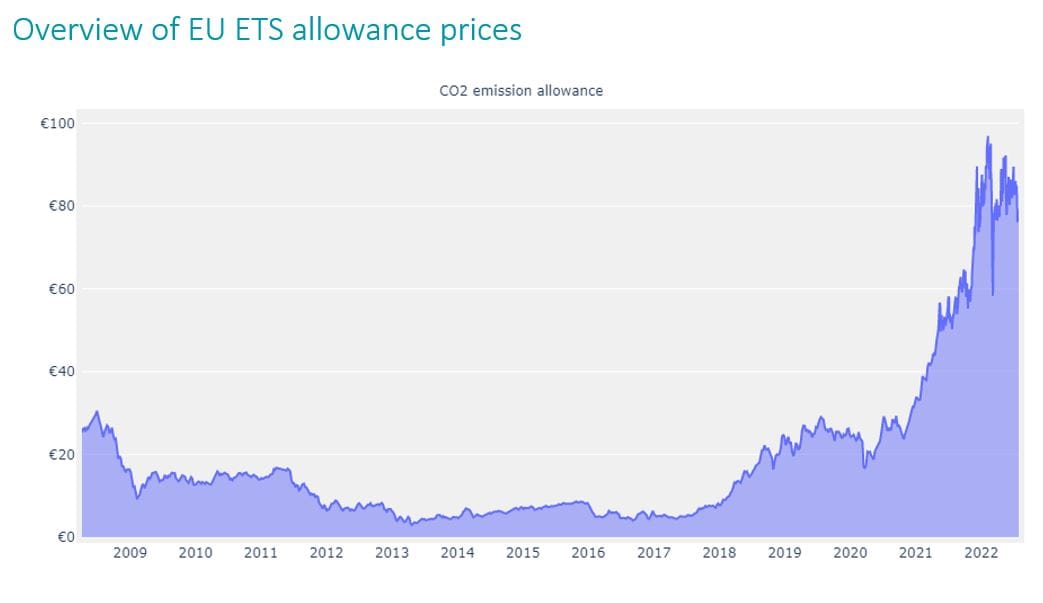

The Paris Agreement gives countries the flexibility to set their own targets (NDCs, nationally determined contributions) to meet global climate goals. This approach bought countries together, but also created asymmetry between countries and their respective efforts to address climate change. As the European Union (EU) pushes forward with its ambition to reduce emissions by 55% by 2030 its emissions allowance costs are increasing to EUR 80-100 per tonne. As carbon prices look set to grow further and the need for greater long-term investment in low carbon production increases, the EU Carbon Border Adjustment Mechanism (CBAM) is intended to level the playing field between EU industries and importers and reduce the risk of carbon leakage (i.e. emissions increasing from the relocation of production to countries with less restrictive policies).1

What can importers expect?

Intended to start on 01 January 2023 (in less than five months), the European Commission’s (EC) proposed CBAM will eventually introduce a carbon price on imports, mirroring emissions allowance prices faced by EU industry operating under the EU Emissions Trading Scheme (ETS). In other words, importers pay a carbon price equivalent to the amount they would have paid if the goods had been produced under the EU ETS rules. If importers can show that a carbon price has already been paid then that amount can be deducted from the CBAM charge.

Source: https://sandbag.be/index.php/carbon-price-viewer/ (01 August 2022)

Source: https://sandbag.be/index.php/carbon-price-viewer/ (01 August 2022)

The Commission has proposed a 3-year phase-in period. Until 2025, CBAM will focus on monitoring and reporting. Full implementation will begin in 2026.

The proposed key design features of the CBAM include:

- Only imports to the EU are covered. There are no export rebates.

- Five sectors are proposed at the first stage: cement, steel, electricity, aluminum and fertilizers.

- Importers have to surrender CBAM certificates (priced on the basis of EU ETS allowances) equal to the embedded emissions in their imports.

- The CBAM will replace the free allocation of EU ETS allowances currently provided to EU industries in the covered sectors – this will occur gradually while the CBAM is phased-in.

- Countries that are linked to the EU ETS are exempt.

- Direct emissions (Scope 1) are covered as well as emissions from input goods deemed to be within the boundary of the production process (partial Scope 3). Indirect emissions from electricity (Scope 2) are not covered, although this may change later.

Embedded emissions (and consequently the adjustment price) will be determined based on the actual verified emissions at installation level. If this information is not available then default values will be applied set at the average emissions intensity of each exporting country for the relevant type of good. If this is not possible then the average emission intensity of the 10 per cent worst performing EU installations for that type of good will be applied instead.

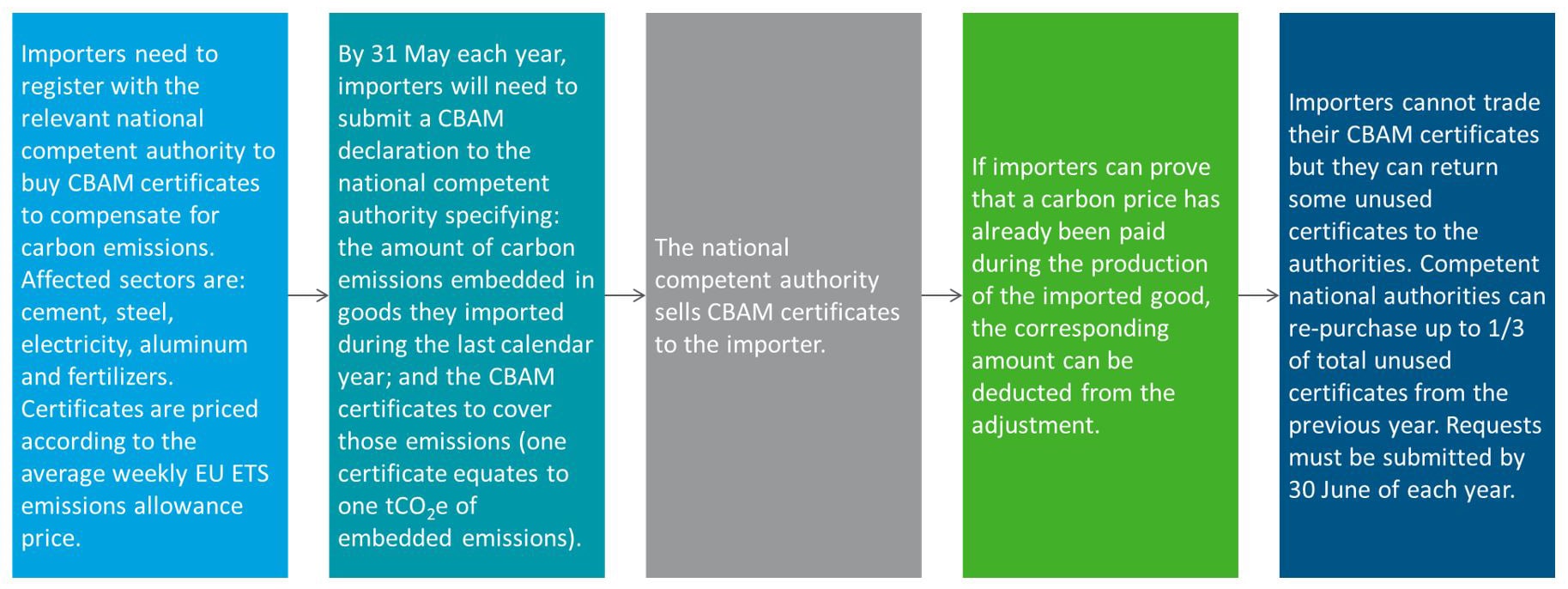

Overview of the CBAM process

Will there be any changes before 01 January 2023?

On 22 June 2022, the EU Parliament adopted a more ambitious position on the CBAM. Some of their key proposals are to expand its scope of products (to also include organic chemicals, plastics, hydrogen and ammonia), to include indirect emissions (emissions from electricity used during the production process), to start full implementation earlier and provide financial assistance to least developed countries.2

Although the EU is currently facing serious economic headwinds, the legislative process is well underway giving it momentum that would be difficult to alter; however, it may be challenging to accommodate many of the measures put forward by the EU Parliament at this moment – although they do provide a sense of CBAM’s future direction.

Impact to China’s trade with the EU

China has 2nd most trade covered under the CBAM (after Russia). This represents less than 2% of China’s exports to the EU or €6.5 billion in 2019. The impact could become more significant though if (or when) the scope of covered products expands.

Whilst relatively small at this stage and the cost of CBAM may be passed on through increased prices, there is opportunity for low carbon producers in China. For instance, steelmaking technologies in China, such as the direct reduction of iron (DRI), could profit from the CBAM, whilst higher-carbon technologies, such as the blast furnace-basic oxygen furnace (BF-BOF), which are more common, are likely to face CBAM costs. 3

It is worth keeping in mind that whilst the EU will become the first to put in place a CBAM other countries may follow. The United States4, United Kingdom5, Canada6 are all reportedly exploring similar options. In the case of the UK and Canada, they both have cap-and-trade schemes with carbon prices that are set to increase. Looking further ahead, China, South Korea, Japan and South Africa are also implementing their own carbon pricing mechanisms7 and may begin to take more interest in CBAM solutions to regulate trade as their carbon prices rise.

Impact of China’s emissions trading scheme (ETS)

Whilst China’s ETS would count as an explicit carbon price, it is currently unclear how it could be credited given that it’s an intensity-based cap. Also, the effected sectors are only covered in a few regional ETS regimes and not covered under the national ETS, which only covers electricity.

Verification of emissions

Efficient, low carbon manufacturers may prefer to have the level of embedded emissions in their products to be based on actual emission levels rather than use the proposed default values. This would need to be verified by an accredited verifier though. For this reason, production installations can request to be registered in a central EU database. For goods produced in these registered installations, the importer may use verified information that has been disclosed to them to fulfil the verification obligation. This can be used by importers for their declarations for five years.

Verifiers already accredited under the EU ETS will be considered accredited verifiers under the CBAM. National accreditation bodies in EU Member States may accredit additional verifiers after checking their capacity to perform CBAM verifications.

Our recommendations

Importers of products covered by the CBAM are strongly advised to prepare for the reporting obligations that will likely take effect from 01 January 2023.

A carbon assessment of the affected products is recommended; along with the establishment of responsible CBAM business functions, and a system for the calculation of emissions embedded in the production of the affected products, including supply chain, so reporting obligations can be met. This should also include (where possible) the indirect emissions created during the production process of these products.

1. EU, Proposal for a carbon border adjustment mechanism, 2021

2. European Parliament Press Release, Parliament pushes for higher ambition in new carbon leakage instrument (accessed on 01 August 2022)

3. China Dialogue, ‘CBAM’ carbon levy will only hit a fraction of Chinese

exports to EU (accessed on 01 August 2022)

4. U.S. Chamber of Commerce, Border Carbon Adjustment Principles (accessed on 01 August 2022)

5. House of Commons Environmental Audit Committee, Greening imports: a UK carbon border approach (accessed on 01 August 2022)

6. Government of Canada, Exploring Border Carbon Adjustments for Canada (accessed on 01 August 2022)

7. World Bank, State and Trends of Carbon Pricing 2022 (accessed on 02 August 2022)