Article

2023 insurance outlook

Global insurance industry at a crossroads to shaping long-term success

Over the last few years, most insurance carriers have demonstrated remarkable flexibility and resilience in overcoming a host of obstacles, especially the impact of the pandemic and the economic fallout from the Russia-Ukraine conflict. Systems and capabilities were improved, while agile talent and technology strategies paid off. But is the industry ready for emerging challenges heading into 2023 (and beyond)? The road ahead is dotted with multiple hurdles—rising inflation, interest rates, and loss costs; the looming threats of recession, climate change, and geopolitical upheaval; and competition from InsurTechs and even noninsurance entities such as e-tailers and manufacturers, to name a few. This is no time for carriers to be satisfied with the adaptations they’ve had to make.

Download the 2023 insurance industry outlook to learn more.

Instead, they should be building upon the momentum they’ve achieved to maintain an ongoing culture of innovation while making customer-centricity the focal point of the industry’s standard operating model. Our research suggests that they should start shifting their focus from basic operational transformation—such as transitioning to cloud—to fully realizing the value and benefits of infrastructure and technological upgrades; move from responding to the requirements of regulators and other industry overseers to more proactively anticipating and fulfilling distributor and policyholder expectations; and broaden their historical focus from risk and cost reduction to prioritize greater levels of experimentation and risk-taking that drives ongoing innovation, competitive differentiation, and profitable growth.

Here are some of the key findings from Deloitte’s 2023 insurance industry outlook:

Inflation hampers nonlife profitability even while boosting prices, top-line growth

While property-casualty price hikes were among the drivers pumping up premium volume and sending US consolidated surplus over the US$1 trillion mark for the first time, inflation is driving loss costs even higher and faster in most markets, undermining underwriting profitability. As of May 12, average replacement costs were up 16.3%—nearly twice the Consumer Price Index rise.

But opportunities abound for proactive nonlife players

The reinvention revolution in the small-business insurance market, the global transition to green energy and related insurance products, coverage for emerging exposures among intangible assets such as cryptocurrency, nonfungible tokens (NFTs), and virtual activities on the metaverse, all point toward plenty of room for growth.

Life insurers transformation likely key to sustainable growth

The pandemic-driven surge in premium growth since 2020 appears to be waning driven by obstacles like inflation-driven disposable income pressure and financial market volatility.

Carriers should respond to economic pressure and COVID-19–related uncertainties with proactive measures like doubling down on their pandemic-spurred digital enhancements, introducing new products, services, and distribution options, or by seeking out previously underserved customer niches.

Group insurers are getting innovative amid shifting dynamics

To facilitate portfolio expansion, many insurers are beginning to develop partnerships with other providers as well as third-party vendors.

Development of “as-a-service” solutions offers another potential competitive advantage group insurers can explore.

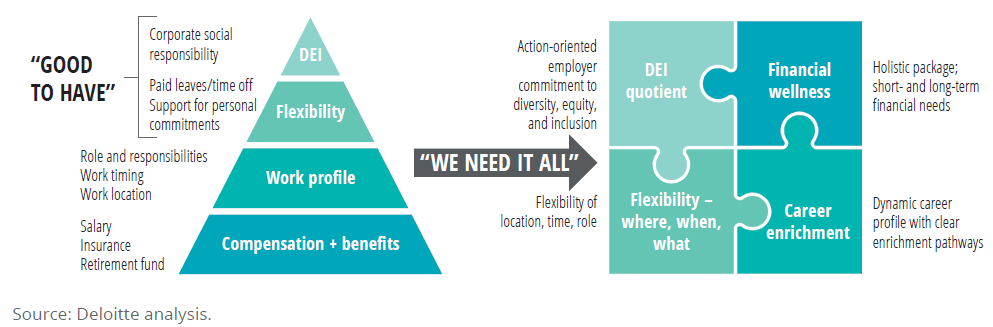

Insurers are reinventing workplace strategies and culture as talent war intensifies

Forced virtualization of work during the pandemic has fueled revolutionary changes in employee expectations and upended many traditional employment models (figure 1).

【Figure 1】 Change in employee expectations has pushed the "good to have" parameters to the "we need it all" bucket

Carriers may struggle to fill and retain their workforce through 2023 unless there are some novel changes implemented to underlying culture that help these organizations to be potentially simply irresistible.

Technology infrastructure has improved, but focus needs to shift to value realization

Many carriers are benefiting from the technology transformation being driven by InsurTechs, especially the point solutions offered by enabling startups in underwriting, claims, and online distribution platforms, among other customer-facing functions. In terms of cloud adoption, insurers should start integrating their systems and data while leveraging cloud capabilities to achieve greater customer-centricity. Focusing on microimprovements utilizing industry cloud applications specific to their business could be a great next step.

Time to make environmental, social, and governance (ESG) a competitive differentiator

Insurers are likely to be judged not just by plans laid out in their annual sustainability reports, but by how their initiatives actually limit the impact of climate change and other nascent systemic environmental risks while addressing carbon emissions at the source; diversify their leadership and workforce; enhance inclusivity of their products and services; and increase transparency and accountability in their governance structures.

More needs to be done to step up diversity, equity, and inclusion (DEI) efforts

While many insurers are taking steps to diversify their workforce, large gaps remain in the industry as a whole—particularly at the executive level. Much needs to be done in diversifying their workforce and customer base, increasing access to insurance products and services in underserved communities and market segments, making a wider range of voices heard in leadership circles, as well as creating a more inclusive organizational culture.

Interested in a deep dive?

Download the 2023 insurance industry outlook to learn more.

Holger Froemer

Partner, Deloitte Tohmatsu Consulting LLC