{kind=link}

{kind=link}

{kind=link}

Japan has been saved

Cover image by: Jaime Austin

After witnessing a decline in economic growth in Q3 2021, Japan is poised for a firmer recovery in Q4, which should continue into next year. Policymakers ended the state of emergency for all prefectures in September, paving the way for more in-person economic activity. Consumer spending likely continued its recovery into Q4 after reversing declines in September.1 Prime Minister Fumio Kishida’s party retained its majority in the lower house of the Diet (parliament), which should support additional fiscal stimulus measures. These measures ought to boost consumer spending as they should include cash transfers to families and a moratorium on consumption tax hikes that have restrained spending. Low inflation could also help consumer spending in the near term, but inflationary pressures are building relatively quickly. The chip shortage is expected to keep the manufacturing sector from reaching its potential this year, but a weak yen and stronger global demand should boost exports relative to imports next year.

Japan’s election at the end of October resulted in the ruling party retaining its majority in the lower house of the Diet.2 The better-than-expected outcome for prime minister Fumio Kishida’s party has practically cleared the way for his economic agenda. The prime minister has pivoted away from his predecessors’ “Abenomics” economic policy that balanced fiscal spending with higher consumption taxes. Instead, Kishida is more focused on reducing inequality and reviving the economy before restoring fiscal balance. During his campaign, he said he would not implement a consumption tax in the next 10 years,3 and proposed raising taxes on investment income for high earners, though he said this will come after implementing other more-pressing economic policies.4

On November 19, Kishida’s cabinet approved a larger-than-expected 55.7 trillion-yen fiscal stimulus package that will still need parliamentary approval. The package includes more funding for universities and digitalization of rural areas to raise productivity growth. It also includes money to raise semiconductor manufacturing capacity, which could improve the country’s economic security.

The prime minister’s focus on reducing inequality has put improving wage growth front and center. The package includes tax breaks to encourage companies to raise wages.5 It will also raise wages for some public sector workers6 in the hope of encouraging the private sector to boost wages so as to remain competitive.7 However, raising wages could prove to be challenging. Wage growth in Japan has been incredibly weak, with nominal wages today still lower than they were in the late 1990s.8

In addition to raising wages, direct cash transfers are part of the bill, with 100,000 yen going to children 18 years or younger, in households earning less than 9.6 million yen per year.9 A reinstatement of the Go To Travel campaign that subsidizes domestic travel is also included. This campaign, although successful in raising demand for travel and related services, was ended due to the spread of the virus. Now, with relatively high vaccination rates, the campaign can continue with fewer risks. Roughly 30.8 trillion yen is left over from the previous stimulus package, which can be used for these new initiatives.10 The additional spending will have to be funded through bond issuance, adding to an already-high national debt.

If implemented, policies that raise wages, transfer cash to households, and subsidize travel expenditures will all support much-needed consumer spending. Although even without those policies, consumer spending is poised for a rebound. After four months of consecutive declines, real household expenditures increased 5% between August and September11 despite states of emergency still in place in parts of the country. In October, the au Jibun Bank Japan Services Purchasing Managers’ Index (PMI) jumped to 50.7, the first reading above the critical 50 threshold since January 2020.12 This reading shows that the service sector is growing again after the end of the state of emergency in September, which bodes well for consumer spending in Q4. In addition, mobility near retail and recreation establishments has improved markedly since September, reaching levels not seen since December 2020.13 Consumer confidence also continued to grow in October, rising 17% year over year (YoY).14

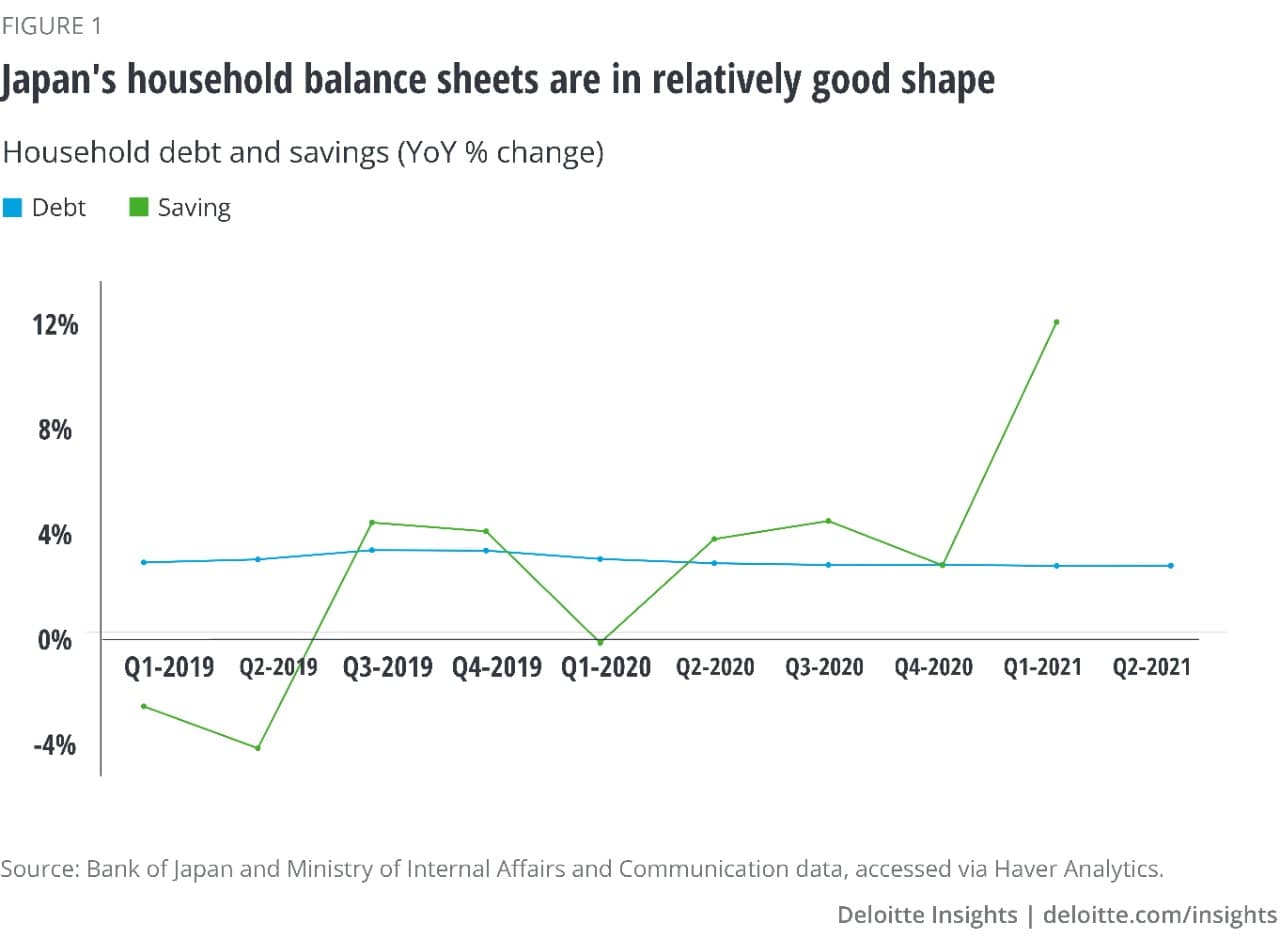

Household balance sheets, meanwhile, are in relatively good shape. Average savings per household increased 15.1% over the last two years.15 This sizable stockpile is more than enough to offset the 4.4% rise in household debt over the same period (figure 1).16 Business balance sheets could have a more detrimental effect on consumers. Nonfinancial corporate debt as a share of GDP has grown 16 percentage points over the last two years.17 Elevated debt levels on business balance sheets could restrain employers’ ability to hire more and offer stronger wage gains.

While other advanced economies are concerned about the rising inflation, consumer price growth remains weak in Japan, with headline inflation up just 0.2% from a year ago in September.18 Japan was initially slow to vaccinate its population and kept large parts of the country under a state of emergency into September. This has delayed the rebound of consumer demand, which, in turn, has contributed to inflationary pressures elsewhere. For example, in September, airline fares were up just 6.5% YoY in Japan,19 whereas they soared to 24.6% YoY in the United States last June.20 With the end of the state of emergency in Japan, the impending rebound in demand, and global supply disruptions, inflation should pick up next year. However, a wage-price upward spiral is unlikely as wages were up just 0.2% from a year earlier in September.21 Even if the new administration’s policies are effective at raising wage growth, those gains are likely to be gradual with most of them depending on the easing of the supply-side inflationary pressures next year.

Mobile phone charges, which were down 44.7% from a year earlier in September, are weighing down Japan’s inflation rate.22 Earlier this year, policymakers encouraged telecommunications companies to lower their rates.23 Those declines likely continued in October, but most of the base effects will disappear in April 2022, erasing a serious burden on headline inflation.

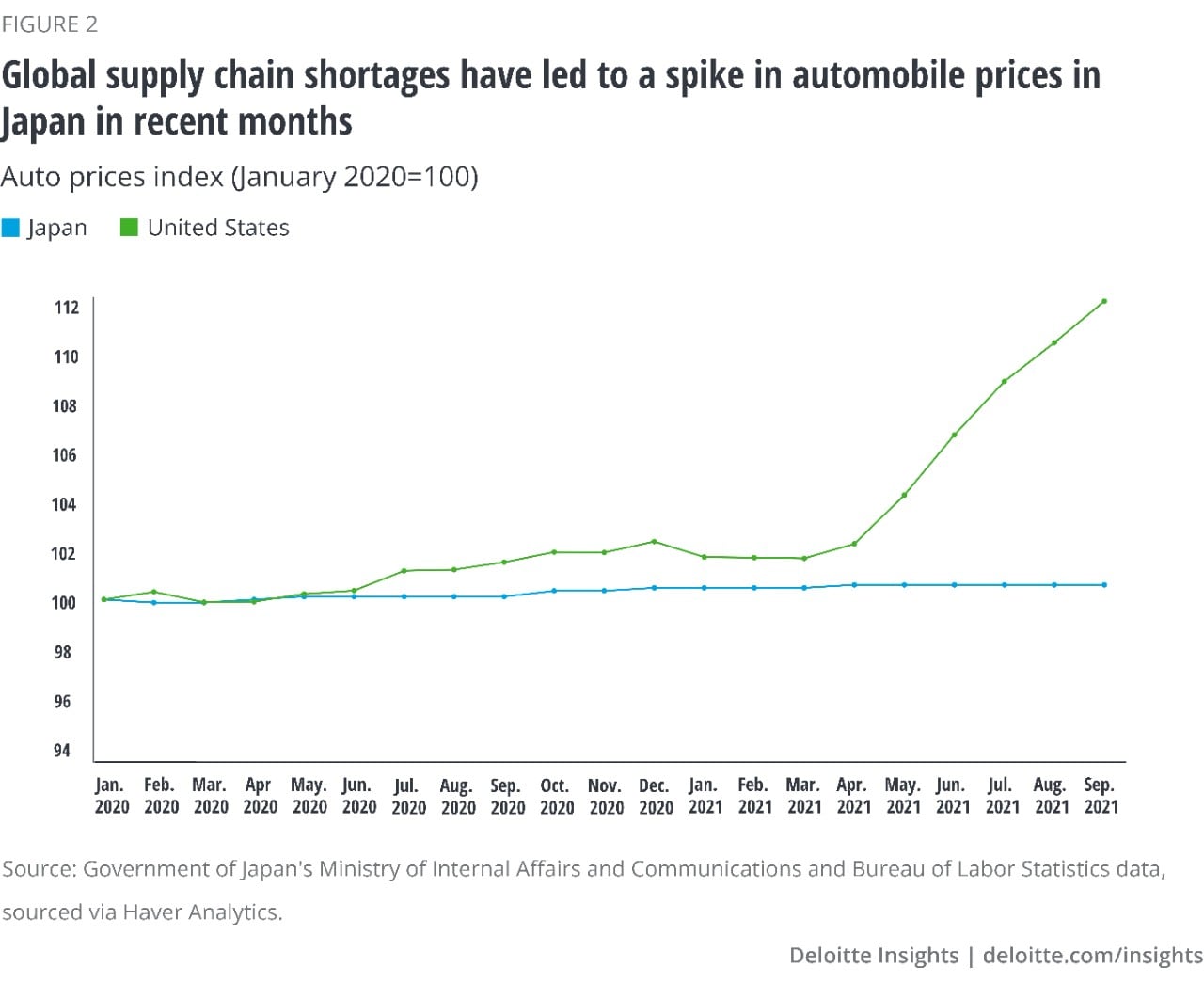

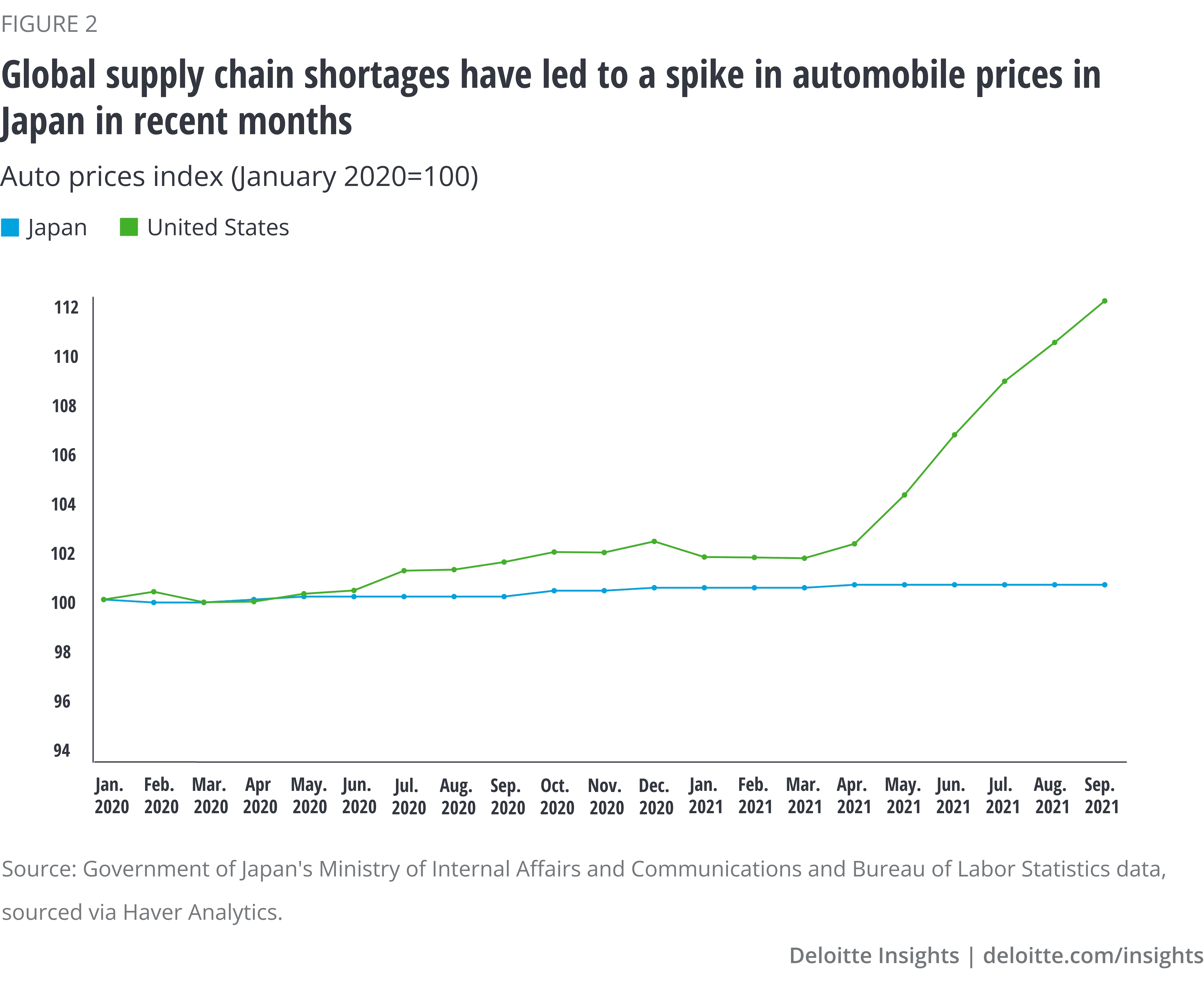

The inflationary pressures from supply-chain shortages seen around the globe will ultimately arrive in Japan as well. The automobile industry has seen substantial declines in production amid the global chip shortages. In many places, this has led to a spike in prices. For example, new vehicle prices in the United States were 8.7% higher YoY in September.24 However, in Japan, automobile prices were up just 0.4% during the same period,25 a rate that is unlikely to persist (figure 2). Domestic automakers had been hesitant to raise prices amid weak demand, but with the end of the state of emergency, demand is likely to rebound, pushing up prices with them. Some foreign automakers announced they are raising prices for cars exported to Japan,26 indicating that stronger inflation in automobiles is on the horizon.

Higher input and commodity prices outside of the automobile industry should add upward pressure to consumer inflation as well. Producer prices were up 6.9% from a year ago in September, the largest gain since 2008.27 Gas prices were up 16.5% and electricity prices jumped 4.1%.28 In addition, a weaker yen will push up the cost of imported goods, such as oil and gas. Import prices were already up 31.3% from a year earlier in September.29 In October, the yen dropped to its weakest level since November 2018.30 Faster-than-expected monetary tightening in the United States and Europe should keep the yen weak.

The main downside to inflation is expected to come from policy intervention, especially the reinstatement of the Go To Travel campaign, which subsidizes travel-related spending. This policy lowers the price of travel services, such as hotel accommodations. When the policy was implemented last year, hotel prices plummeted, creating a low base that contributed to a huge 43% YoY increase in these prices in September 2021.31 The inflation in travel-related services we see today will largely be erased assuming the Go To Travel campaign is renewed.

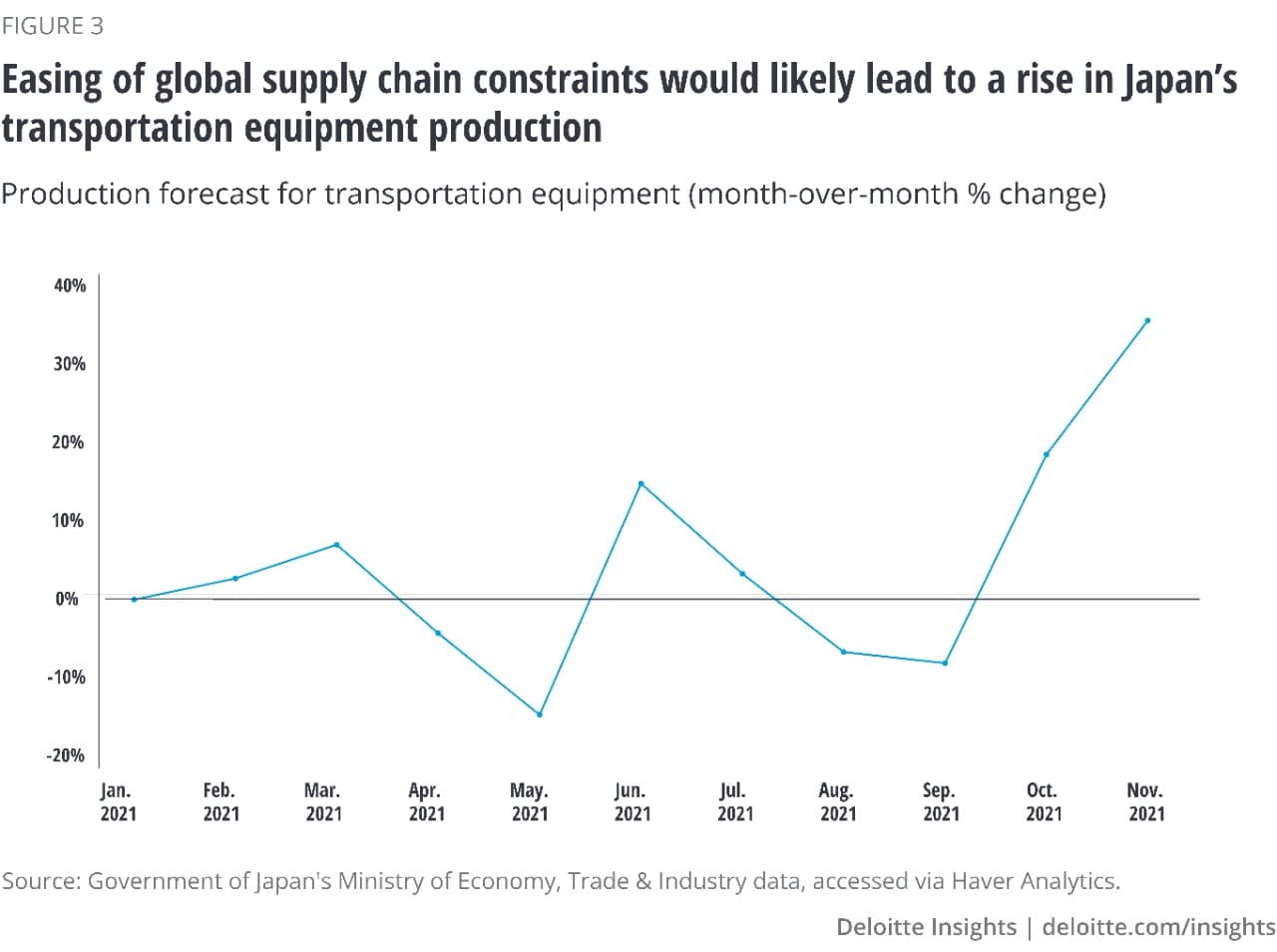

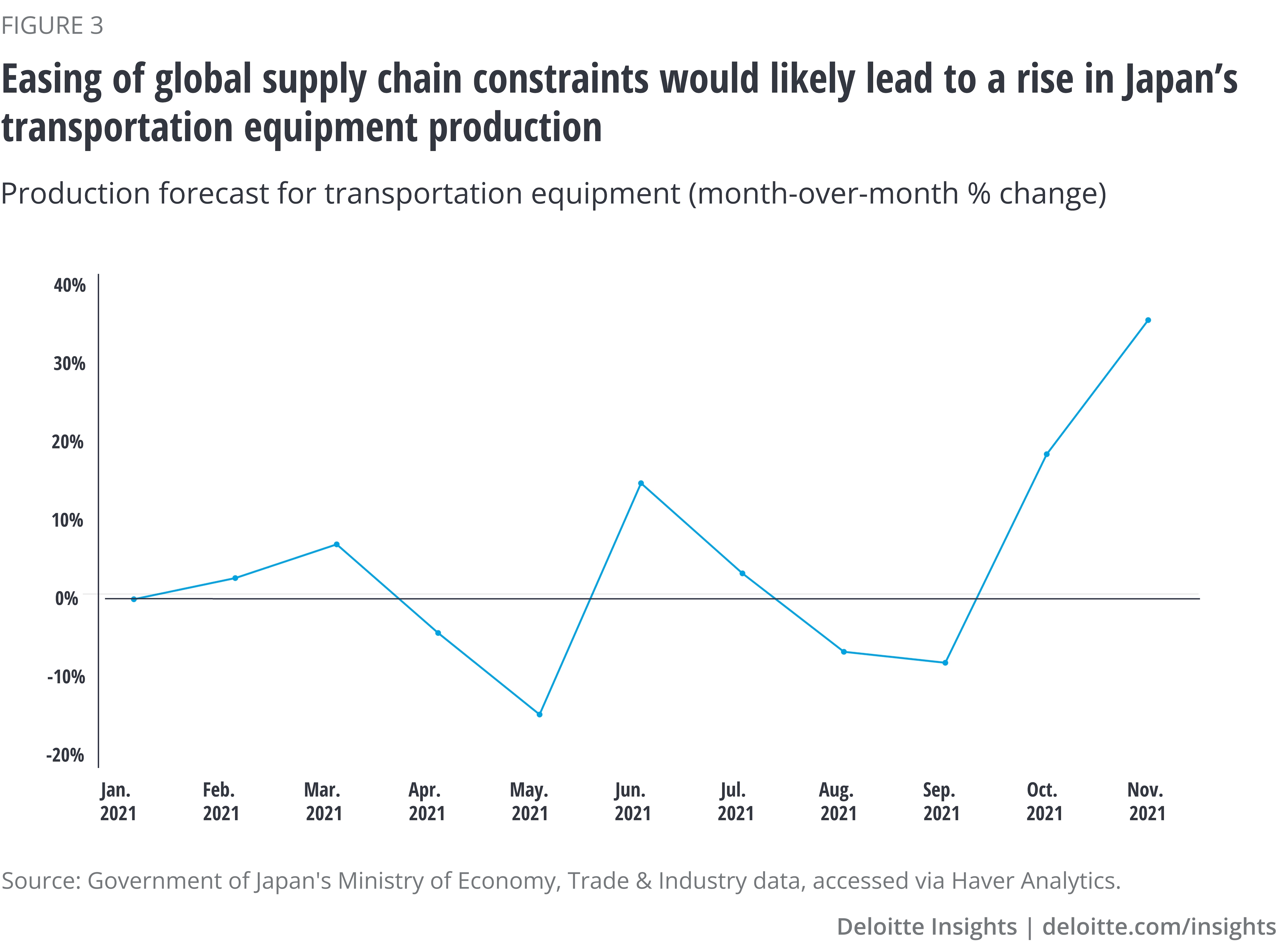

Despite relatively weak domestic demand, Japan ran a goods trade deficit of 624.8 billion yen in September, the largest deficit since February 2015.32 High commodity costs have contributed to the trend of imports rising faster than exports. At the same time, the chip shortage continues to plague the automotive industry, with motor vehicle exports down 40.3% YoY. Prior to the pandemic, motor vehicles accounted for a sizable 15–16% of all exports.33 These two trends should begin to reverse next year. As global supply constraints ease, the cost of commodities should come down. Forecasts for transportation equipment production, which mainly includes vehicles, show a sharp rise in production in October and November (figure 3).34

While automakers slowed production due to chip shortages, semiconductor production continues unabated. Semiconductor exports jumped 20.2% from a year earlier in September.35 Japan is also building its capacity to produce more semiconductors,36 which could help support export growth over the longer term. Policies to reshore goods production could also improve Japan’s export position, though it remains to be seen if such policies will have a material effect on the location preferences of manufacturers. A weak yen should make Japanese exports more competitive internationally while restraining import growth. However, China remains a serious risk to Japan’s export position. The prospect of considerably weaker growth in China could prevent Japanese exports from gaining much momentum.

Despite some risks, Japan’s economy is finally headed in the right direction. The new prime minister’s economic agenda will boost consumer spending and could prop up productivity growth. As demand rebounds amid ongoing supply constraints, inflationary pressures will build. However, some of those supply constraints will likely begin to abate next year, preventing inflation from getting out of control. At the same time, manufacturing production and goods exports are expected to rebound as supply-chain constraints ease.

Cover image by: Jaime Austin