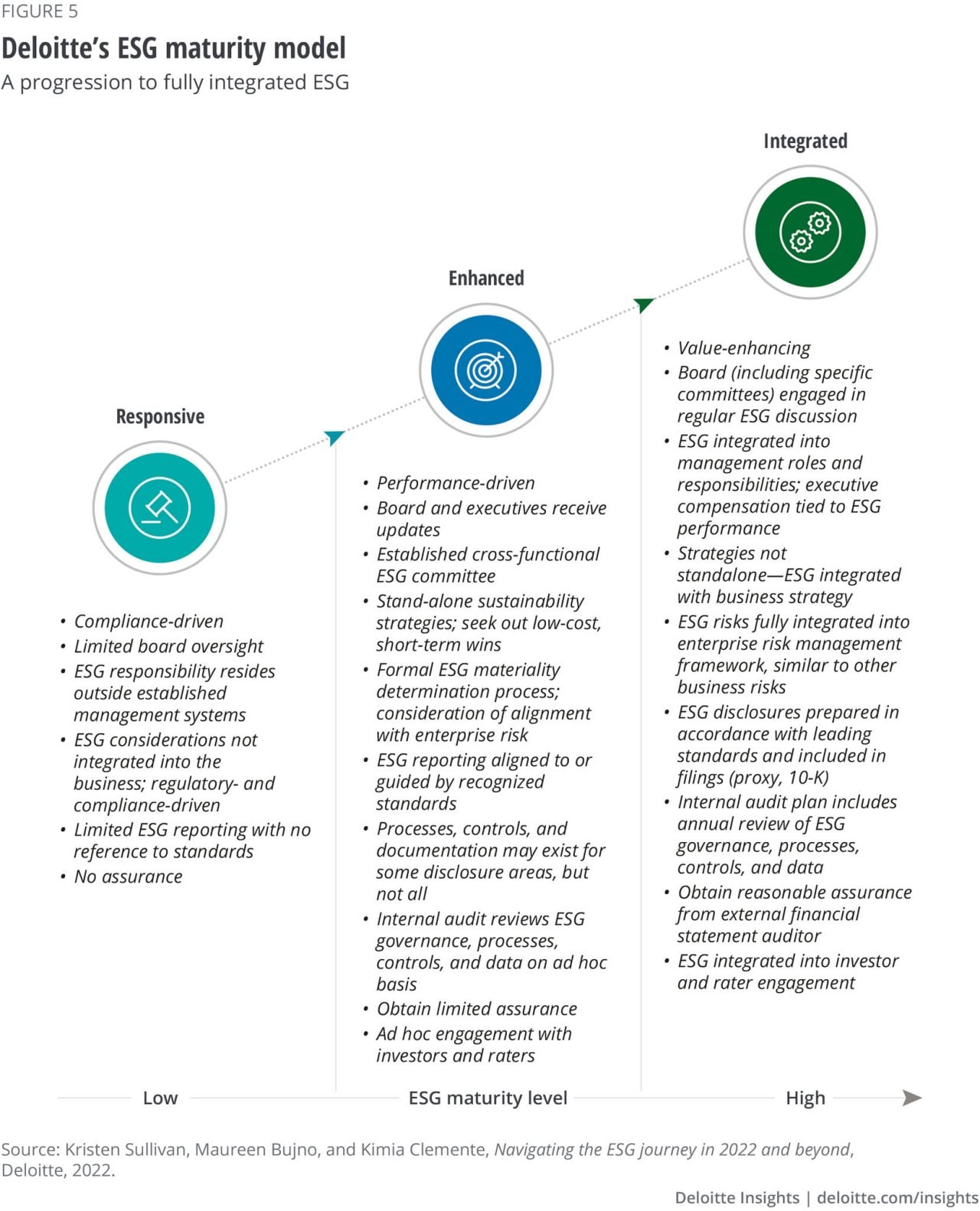

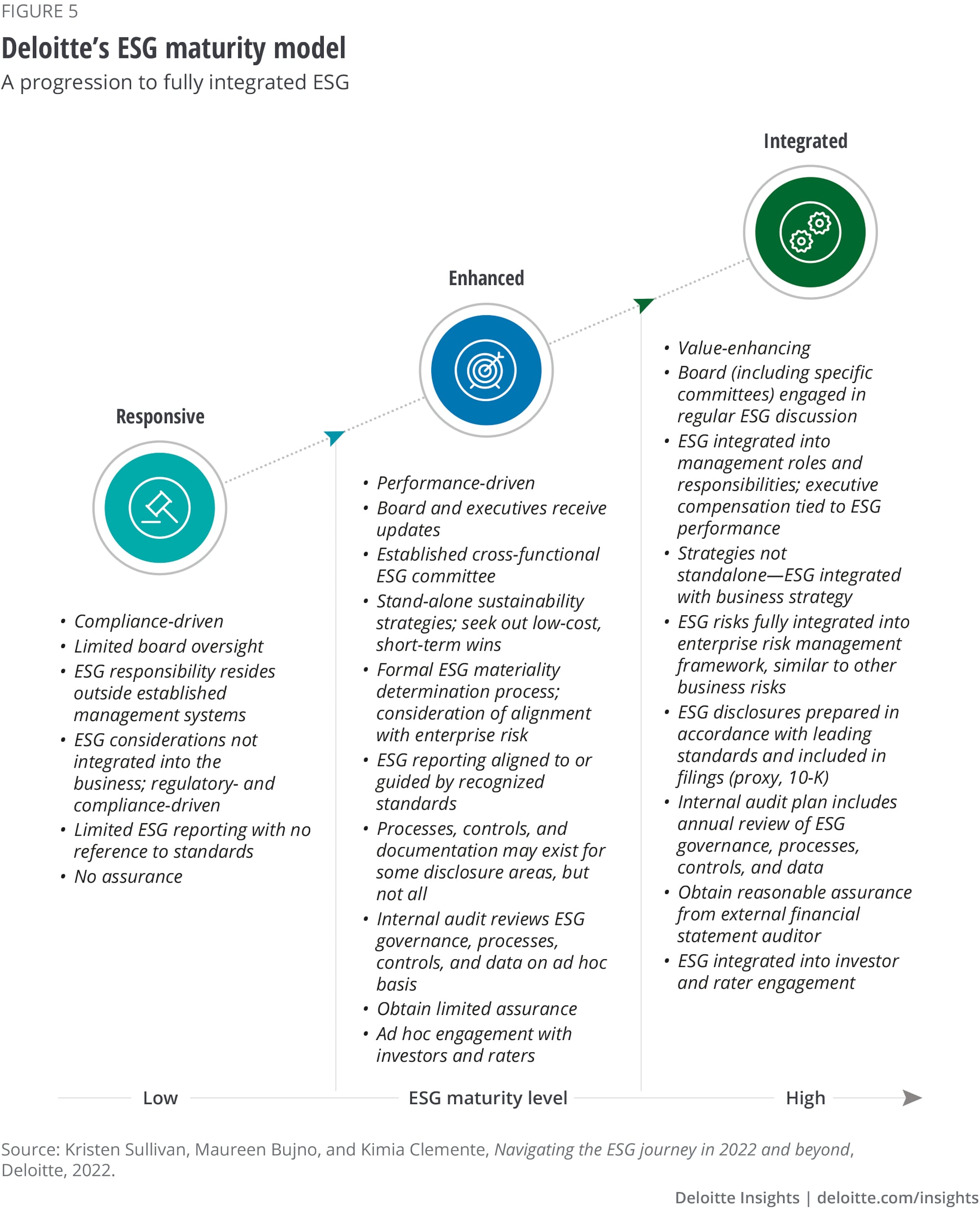

Develop accountable leadership

Governance starts with the board of directors. Accountable Sustainability means the board, including specific committees, regularly engages in sustainability discussions. Sustainability should also be integrated into management roles and responsibilities and linked to compensation. The change these leaders drive should be iterative, aiming for steady improvement over a timeline that can meet the company’s commitments. The processes and controls for improvement may not be obvious or simple, and so should be refined based on data indicating what is working—and what is not. This implies regular, cadenced reviews of effectiveness, cost-efficiency, and other implications.

Invest in governance infrastructure

Governance runs on data. This, in turn, requires an infrastructure for data governance. The infrastructure should span the necessary people, processes, and technology to run all the systems of governance, including aggregation and reporting platforms. Note that even Vanguard companies still direct most of their investment toward technology. Some companies are creating central “control towers” to help orchestrate, integrate, and aggregate relevant ESG data from both inside and outside of a company. Such systems can add automation and help enforce the rules to enhance the accuracy and trustworthiness of ESG data. They can also incorporate artificial intelligence to help make sense of the data and surface what truly matters.

Pursue strategic integration

Sustainability can’t stand alone. Integrating sustainability governance with existing core company governance processes boosts accountability by borrowing from well-established financial governance processes and systems. For instance, companies can integrate sustainability strategy with business strategy and sustainability risks into enterprise risk management frameworks along with other business risks.

Provide transparency and engagement

Increased accountability relies on reporting to and engaging with stakeholders. The reporting—as well as the data that fuels it—should be consistent and comparable, requiring disclosure standards. It also means presenting progress and supporting data to stakeholders in a concise, digestible way. Transparency requires letting stakeholders know what is really going on—not obscuring things by drowning them in facts. Transparency and embedded ESG metrics are needed internally too in order to manage progress.14

Establish independence

How can a company best assure its stakeholders that the data reported is credible and verifiable? Long a key tenet and tool of good governance, Accountable Sustainability improves through independent oversight—it’s a matter of trust. Limited or reasonable assurance for sustainability reporting and/or regular reviews of sustainability governance, processes, controls, and data should come from an independent auditor. It’s a leading practice recommended by prominent investor, accounting, and ESG groups and, as demonstrated earlier, it is a practice most frequently followed by the Vanguard companies in the survey.15

Conclusion

Just as a company would be hard-pressed to improve any aspect of its financial standing without a strong governance and reporting model, so too with sustainability goals. With Accountable Sustainability, companies can achieve sustainability metrics with an enhanced level of trust.

Many consumer companies are moving in the right direction. Several already recognize the potential benefits of greater accountability and have begun implementing multiple aspects of good governance. Eventually, they should reach a point where leadership, infrastructure, integration, transparency, and independence are embraced and function as a complete governance system—a system interwoven with a company’s purpose, business strategy, its management, and operations.

And to not forget the ultimate objective: Improve the sustainability of the environment for everyone. Becoming more accountable is about making a real difference, with consumer companies doing their part. Another benefit: Establishing strong governance to drive environmental progress can undoubtedly be applied to making real social progress as well, better addressing the broader scope of ESG goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}