Brazil economic outlook, April 2023 has been saved

Cover image by: Jaime Austin

With real GDP contracting at the end of 2022, Brazil’s economy appears poised for more slow growth. However, the outlook has proved more resilient than previously expected, and growth will likely pick up near the end of the year. In March, the composite purchasing managers’ index,1 which surveys manufacturing and service sector firms, indicated the economy was expanding, albeit modestly, for the first time since October. As we move through 2023, several headwinds the economy has been facing should begin to wane.

The new administration released its fiscal framework recently, outlining how it plans to stabilize government debt. Legislated restraints on spending should give businesses and investors more confidence in the financial health of the country. At the same time, inflation, although still hovering above the central bank’s target, is receding. There will likely be some hiccups in the data as removing tax exemptions makes inflation look worse temporarily. However, price growth should trend lower, allowing the central bank to ease rates later this year, providing support to the overall economy. Although Brazil’s external position will likely weaken a little this year as the global economy cools, exports and inward foreign direct investment should remain at relatively high levels.

Brazil has long struggled with public financing issues. Most recently, a flurry of government stimulus was used to support incomes during the pandemic and ease financial burdens ahead of last year’s election.2 In 2022, the government ran a budget deficit equivalent to 4.5% of GDP,3 while outstanding debt was equivalent to around 70% of GDP.4 For comparison, government debt in other major emerging market economies, including Chile and Indonesia,5 is typically far smaller. Many investors have grown concerned about the Brazilian government’s ability to keep its spending in check, leading to a sharp rise in government bond yields in the second half of last year.

Now that the government announced a new proposal to keep federal spending under control, yields have moved lower. Under the new framework, federal expenditures would be allowed to rise by up to 70% of revenue growth, allowing total revenue to catch up to total expenditures.6 The government expects the new policy will lead to a primary balance surplus, which excludes interest payments, by 2025. The government has not completely solved its fiscal challenges, as the policy needs to pass Congress before it can be implemented, and the primary balance target may be a bit optimistic. Even so, a credible framework is a welcome development. Financial markets seemed to agree, as the 5-year treasury yield slipped to its lowest since November 2022,7 when the new government took office.

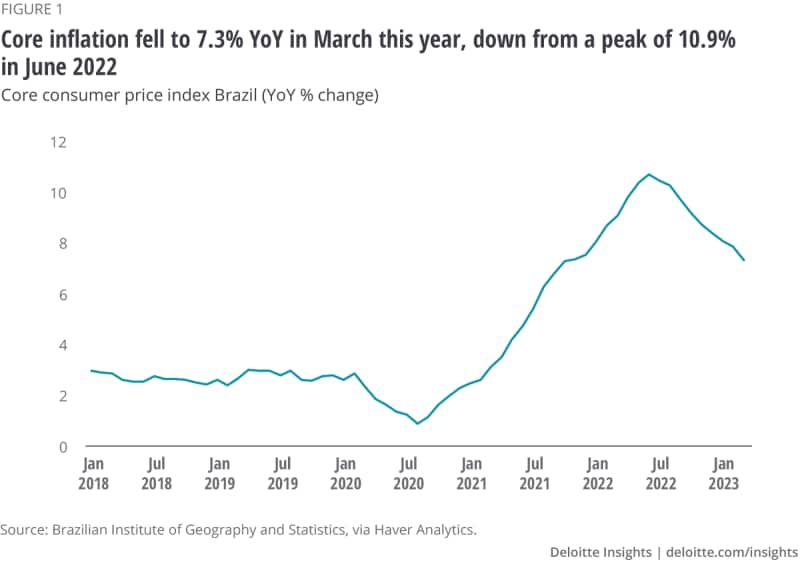

Getting the government’s fiscal house in order will also depend on how inflation, and therefore interest rates, evolve. The Banco Central do Brasil (BCB) had been relatively aggressive in its fight against inflation, raising rates in 2021, earlier than most major central banks. The BCB’s policy rate reached 13.75% in August 2022, where it has remained since. As a result, the core inflation rate, which excludes food and energy, has fallen to 7.3% year over year in March, down from a peak of 10.9% in June.8 Despite a strong month-to-month gain in core inflation in February, we expect the BCB to be able to cut rates later this year, which should help alleviate pressure on fiscal balances.

Government tax exemptions, especially those related to energy, have distorted the inflation statistics and made inflation look stronger than it really is. For example, residential electricity charges jumped 17.7% in February and 30.3% in March on an annualized basis.9 Fuel taxes expired in March, which pushed the price of fuels for personal transport up 125.5% on an annualized basis.10 Such large month-to-month movements are unlikely to be repeated in subsequent months as they relate to one-time changes in taxes. In addition, education prices skyrocketed in February,11 which coincides with the beginning of the school year. Education prices are typically adjusted just once per year, and the March data shows that the education price spike in February was a one-time adjustment yet again this year.12

Looking through the noise, it seems that the early tightening from the BCB is resulting in moderating inflation. A slowing economy will add to the disinflationary trend. The unemployment rate climbed to 8.6% in February from 7.9% in December.13 Meanwhile, the total number of employed fell for three consecutive months to February, resulting in about 1.5 million fewer workers since November.14 With the labor market loosening as inflation continues to run hot, real wage growth declined in February for the first time since April 2022. As a result, consumers are tightening their spending. For example, retail sales fell in November and December despite prices continuing to rise. After adjusting for inflation, retail sales were up just 0.2% from a year earlier.15

Although conditions for consumers have deteriorated recently, consumer confidence remains buoyant. For example, Fecomercio’s measure of consumer confidence hit its highest level since February 2019, just before everyone realized the world was living through a pandemic. Weaker inflation is likely helping to spur confidence even if wage growth is not keeping up.

Brazil’s trade surplus hit a record in March 2023.16 Exports jumped sharply in the month, with some of the largest gains seen in agricultural products. An exceptionally strong soybean crop should provide support for agricultural exports into April as well. Export gains were strong in other categories, including base metals and machinery. A weakening of the currency and the reopening of China have helped push exports in the right direction. However, export growth could slow from its breakneck speed as some of these tailwinds subside.

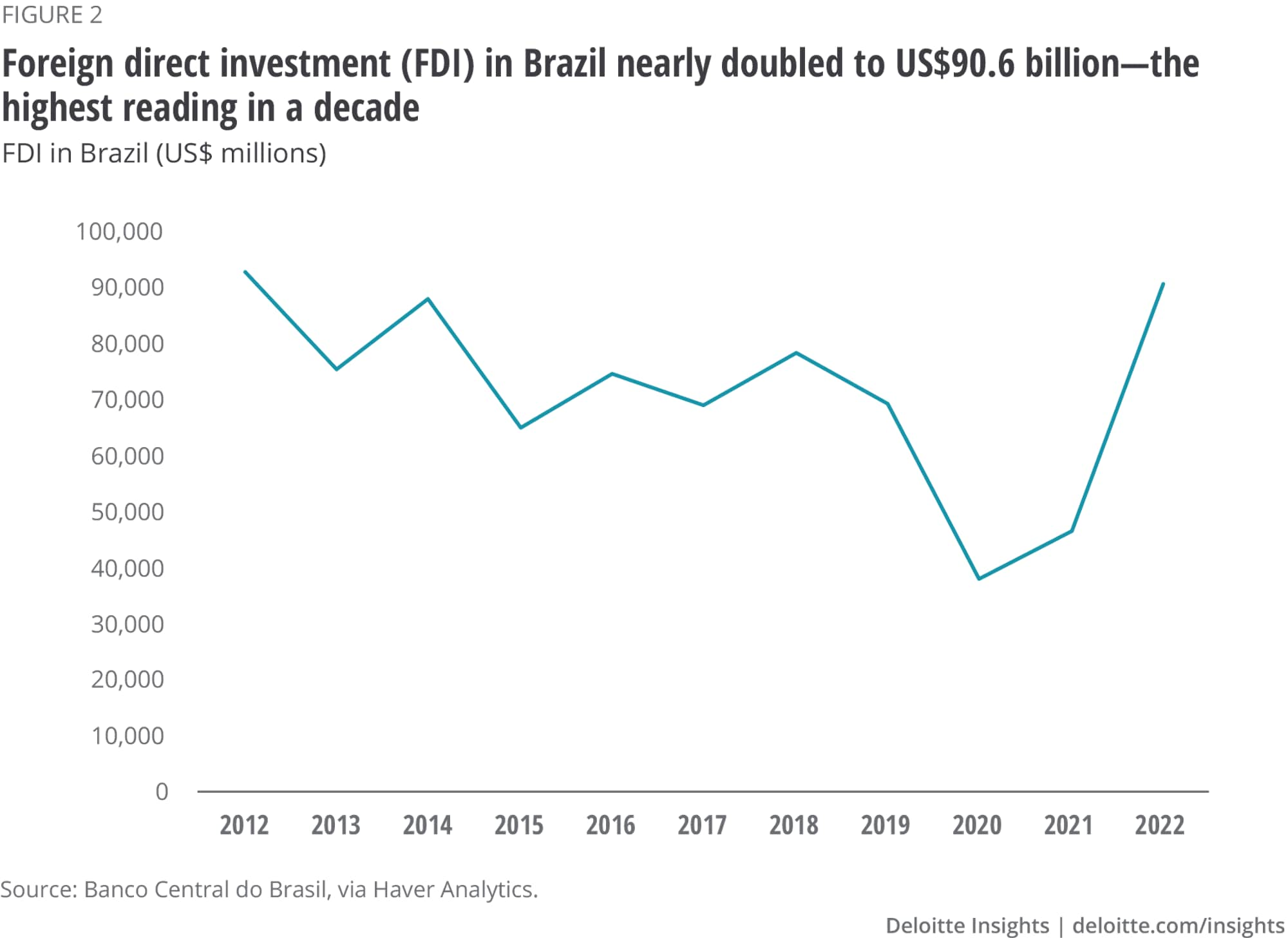

As export growth continues to impress, foreign direct investment (FDI) has also been notably strong. In 2022, FDI in Brazil nearly doubled to US$90.6 billion, the highest reading in a decade (figure 2).17 The BCB noted that energy and technology were among the largest recipients of FDI. During the pandemic, technology companies found Brazil to be an appealing place for expansion, given its relatively high adoption of technology and the internet.18 This allowed platform companies that link buyers and sellers to flourish. US FDI in Brazil in 2021, the latest available, was notably strong in the information sector, which is dominated by tech firms.

Geopolitics may also be affecting FDI flows into the country. With tensions between China and the United States ramping up, Brazil has likely been a beneficiary. Greater US scrutiny of Chinese company acquisitions has forced Chinese companies to look elsewhere for targets, including in Brazil. Sanctions of Russia have also likely fueled interest in Brazil’s energy industry, which has been by far the largest recipient of Chinese direct investment inflows. The BCB expects FDI flows to weaken this year as expectations of an economic slowdown will likely weigh on growth, but inbound investment is expected to remain strong.

Brazil’s economic cooling this year sets the stage for stronger growth later. Inflation remains high and will need to come back in line with the central bank’s targets. As inflation dissipates further, the BCB will be able to lower rates and likely usher in stronger growth. This should ease pressures on governments and households. Government authorities will face less interest expense, while households will likely see their incomes rise in inflation-adjusted terms. An improving outlook will likely reverse the rise in unemployment and support additional consumer spending.

{kind=link}

{kind=link}