Mexico has been saved

Cover image by: Jaime Austin

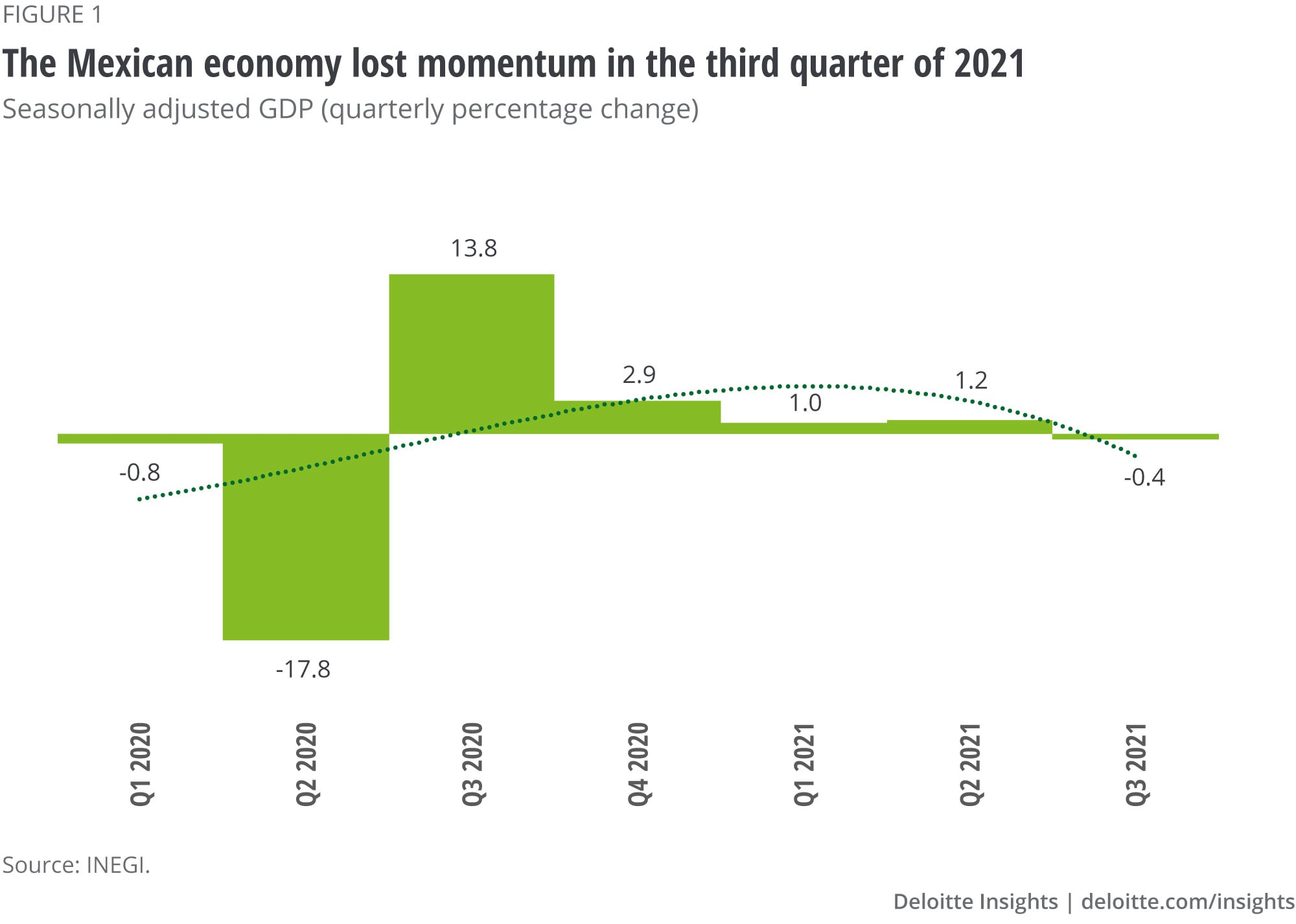

After witnessing a severe economic contraction in 2020 (–8.2%1), the largest since the Great Depression, the Mexican economy is on course to a reassuring recovery this year. The economy expanded 1%2 quarter to quarter in Q1 of this year and 1.2%3 in Q2. These rates of growth, although indicating a slight downward shift from Q4 2020 when the economy expanded 2.9% quarterly (figure 1), still exceed expectations and can be mainly attributed to the uptick in internal demand thanks to the decent progress made in vaccinations and the easing of mobility restrictions.4

However, in Q3, real GDP contracted by 0.4% with respect to Q2, partly because of the appearance of a third wave of COVID-19,5 which had a significant impact on the services sector (–0.9% quarterly). Other factors that may have weighed down on tertiary activities include high rates of inflation and the recent amendment to the labor law that substantially restricts outsourcing.6 It is mainly due to this amendment, which was approved in April and came into effect on September 1,7 that business support services8 witnessed a contraction of 11.6% in June, 14.3% in July, 26.9% in August, and 13.6% in September.9 However, these figures may not represent a net-loss in the overall GDP, considering other sectors may absorb these apparent leakages. Furthermore, as only legal modifications occurred during this period (June–September), to assess the real impact of the labor reform, it will be prudent to wait for the data for the coming quarters that will no longer have this one-time effect.

Mexican industries (including the automotive sector), meanwhile, have not escaped unscathed from the global supply chain crisis and the consequent shortage of goods.10 The impact, however, has been moderate—in fact, the Mexican industrial sector grew by 0.3% in Q3 2021 with respect to Q2, after expanding 0.4% and 0.8% in Q1 and Q2, respectively.

The short-term outlook for Mexico points to a fragile economic recovery in 2022, as issues in the global supply chains and uncertainty in the labor market are likely to persist for some time.11 We forecast a GDP growth of 3.0% in 2022 versus 5.8% this year (figure 2). However, we acknowledge that lingering industrial concerns mentioned above, a fragile recovery in investment, and new strains of the virus pose downside risks to growth. Furthermore, the sudden increase in consumer prices is leading to higher interest rates, which will make credit more expensive and, thus, act as a barrier to growth.

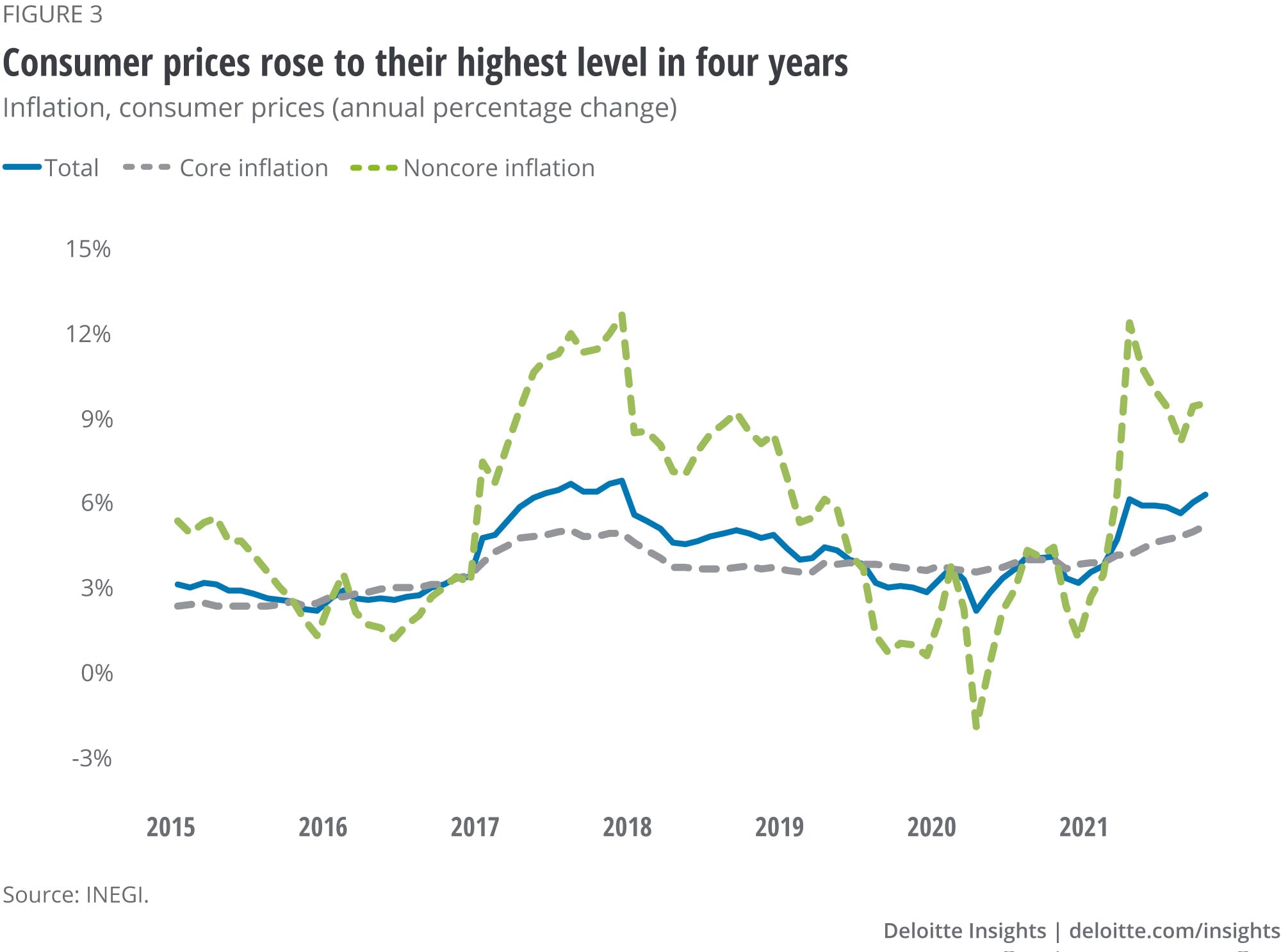

With global economic recovery underway, the prices of raw materials12 are on a steep rise as their demand has exceeded the existing supply. Additionally, fresh outbreaks of COVID-1913 have deterred an extended relaxing of mobility restrictions, posing challenges for companies to operate normally, thus limiting production and leading to goods shortages.14 These factors, in conjunction with exorbitant freight costs,15 have caused an alarming rebound in inflation.16 The interannual rate in Mexico reached 6.24% in October, the highest since December 2017, and has maintained an upward trend ever since (figure 3). In fact, for eight months now, inflation has stayed above the central bank’s upper bound of 4%. 17

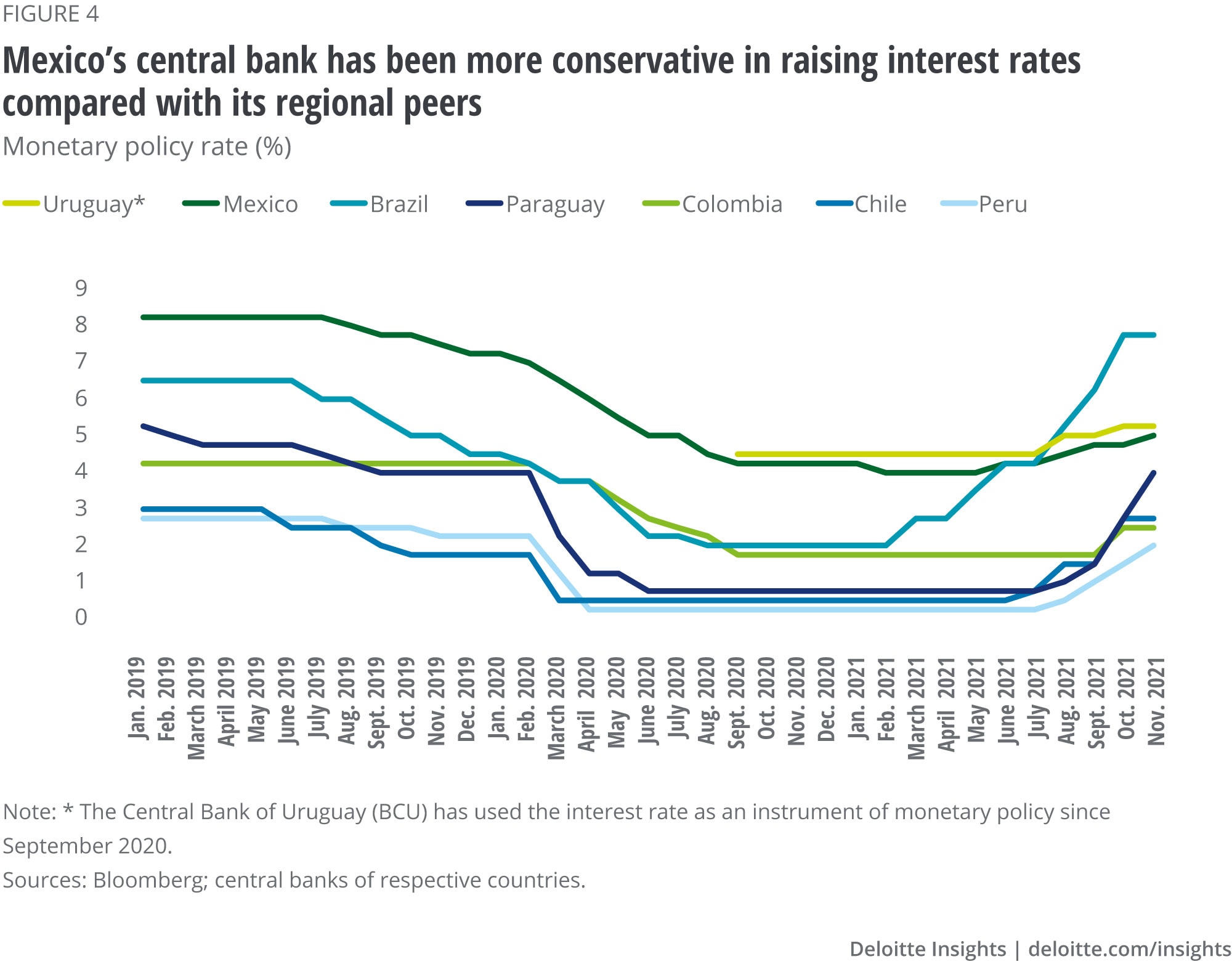

With external pressures expected to last a few additional months, inflation will likely remain on the higher end of the spectrum and will force the Central Bank of Mexico (Banxico) to continue its policy of monetary tightening: Banxico raised interest rates by 100 basis points (bps) earlier this year,18 and we anticipate a further raise of 25 bps in mid-December to 5.25%. Furthermore, the US Federal Reserve (Fed) may start to tighten its monetary policy next year,19 a scenario that will likely add supplementary pressure on Banxico.

Higher interest rates remain one of the main risks that the world economy will face in 2022,20 as it would imply less and more expensive credit, which will affect global economic recovery at a time when several countries are still struggling to free themselves from the grip of the COVID-19 pandemic. In addition, higher interest rates will likely increase debt service costs21 for governments that are already heavily indebted, especially in emerging markets.22

Within the region, Banxico has been more conservative in raising the interest rate compared to its regional peers who have acted more aggressively23 (figure 4). For example, compared to Banxico’s 100 bps increase, Brazil raised interest rates by 575 bps since the beginning of this year,24 Chile by 225 bps,25 and Paraguay by 325 bps.26 This places Mexico in a more favorable situation vis-à-vis a future scenario in which the Fed raises its reference rates and all other economies are required to match the increased rates to avoid a capital flight that could impact local currencies.

Meanwhile, by adopting a fiscal policy of avoiding higher foreign debt and keeping the fiscal deficit under control, public finances in Mexico remain in good condition. The 2022 budget proposal27 aims for a 0.3% primary deficit next year compared to an estimated 0.4% deficit this year. Besides, the general fiscal deficit was set at 4.2% of GDP for 2021 and 3.5% for 2022. The new budget should allow the reduction of public debt to 51% of GDP next year, versus 52.2% this year. The latter figure places Mexico at a more favorable position than its emerging peers28—Brazil, for example, is estimated to reach a 90.1% of gross debt as a percentage of GDP in 2022; for Argentina, this figure is 88.6%.29

Additionally, the rebound in commodity prices, particularly oil, could help achieve the government’s fiscal goals, since this good accounts for approximately 16% of total public revenues. For 2022, the Ministry of Finance estimates the average price for Mexican crude to be US$55.1 per barrel,30 something that seems feasible given the current context of elevated commodities prices.31 So far this year, the price has hovered around US$64.1 per barrel, which is slightly above this year’s goal of US$60.6.

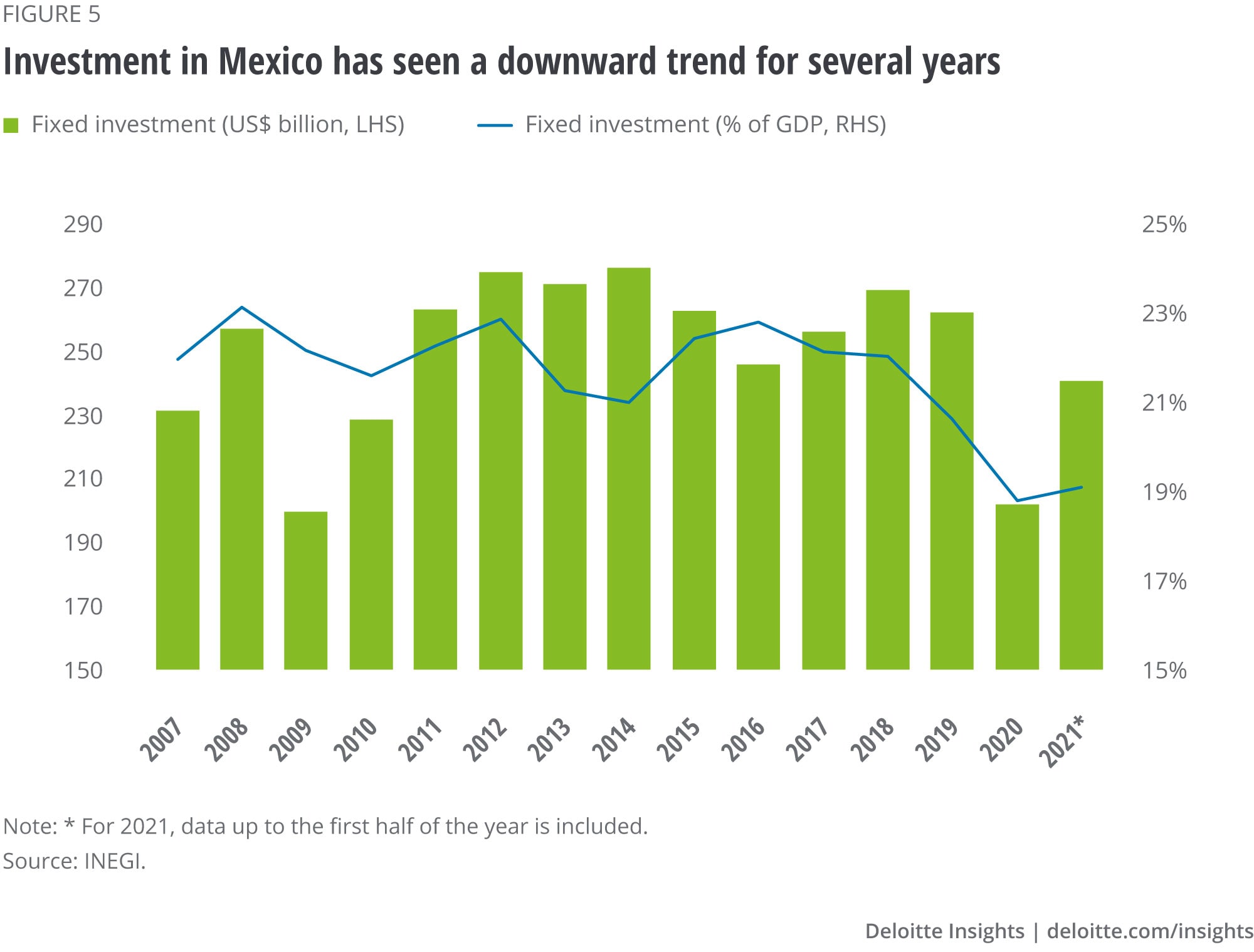

Fixed investment in Mexico has been on a downward trend for several years now (figure 5), due to the lack of public strategies to shore it up and an unfavorable business environment.32 Another indication of a lack of investments in Mexico is that imports of capital goods33 have been declining. From January to September 2021, capital goods worth US$29,856 million were imported, a volume that is barely comparable to what was imported in the same period of 2016 (US$29,799 million).

This complicated investment environment has been further affected by a series of domestic policies and regulatory decisions focused on restricting private participation and expanding the role of the state in the affairs of the economy.34 The most recent example, although still under discussion in Congress, is an initiative aiming for a constitutional amendment to the workings of the energy sector.35

The bill basically aims to modify the constitutional scheme for the generation and commercialization of electrical energy,36 establishing that the entire power supply chain—generation, transmission, distribution, and supply—will be reserved exclusively for plants owned by the national power company, the Federal Electricity Commission (CFE in Spanish).

This move does not take into account the fact that these state-owned plants rely on generating power from fossil fuels and are more expensive than other alternatives. The reform has two main implications for Mexico: (1) It places the country in a position contrary to the global movement that seeks to cut down the use of fossil fuels and opt instead for greener alternatives;37 and (2) it negatively affects business confidence in Mexico as the initiative aims to impose roadblocks for the issuance of new generation permits and even comes with the option to revoke existing self-supply permits that had been given under the previous law to small generators.38

However, before it can be passed as a law, the reform bill must be ratified by two-thirds of the upper and lower houses of the parliament, something that at present seems unlikely as the ruling party only has 278 seats in the lower house of the 331 required, and has only 76 out of 86 needed in the upper house.39 Nonetheless, the discussion around the bill and the ruling party’s endorsement have generated widespread skepticism about the future of Mexico’s power industry.

In light of recent global supply chain disruptions, policymakers and businesses around the world have started to take steps to mitigate the consequences these disruptions may have on them. In fact, these concerns about supply chains came to the fore well before the onset of the pandemic, as the US-China trade war escalated dramatically,40 intensifying fears of countries and businesses depending on certain regions other than China and the United States (mainly Asia) for the provision of critical and strategically sensitive goods. This discussion became more relevant when a revamped North American Free Trade Agreement (NAFTA) took effect in mid-2020, in the form of the US-Mexico-Canada Agreement (USMCA),41 as former US president Donald Trump was trying to reshore companies’ production units back to the United States.

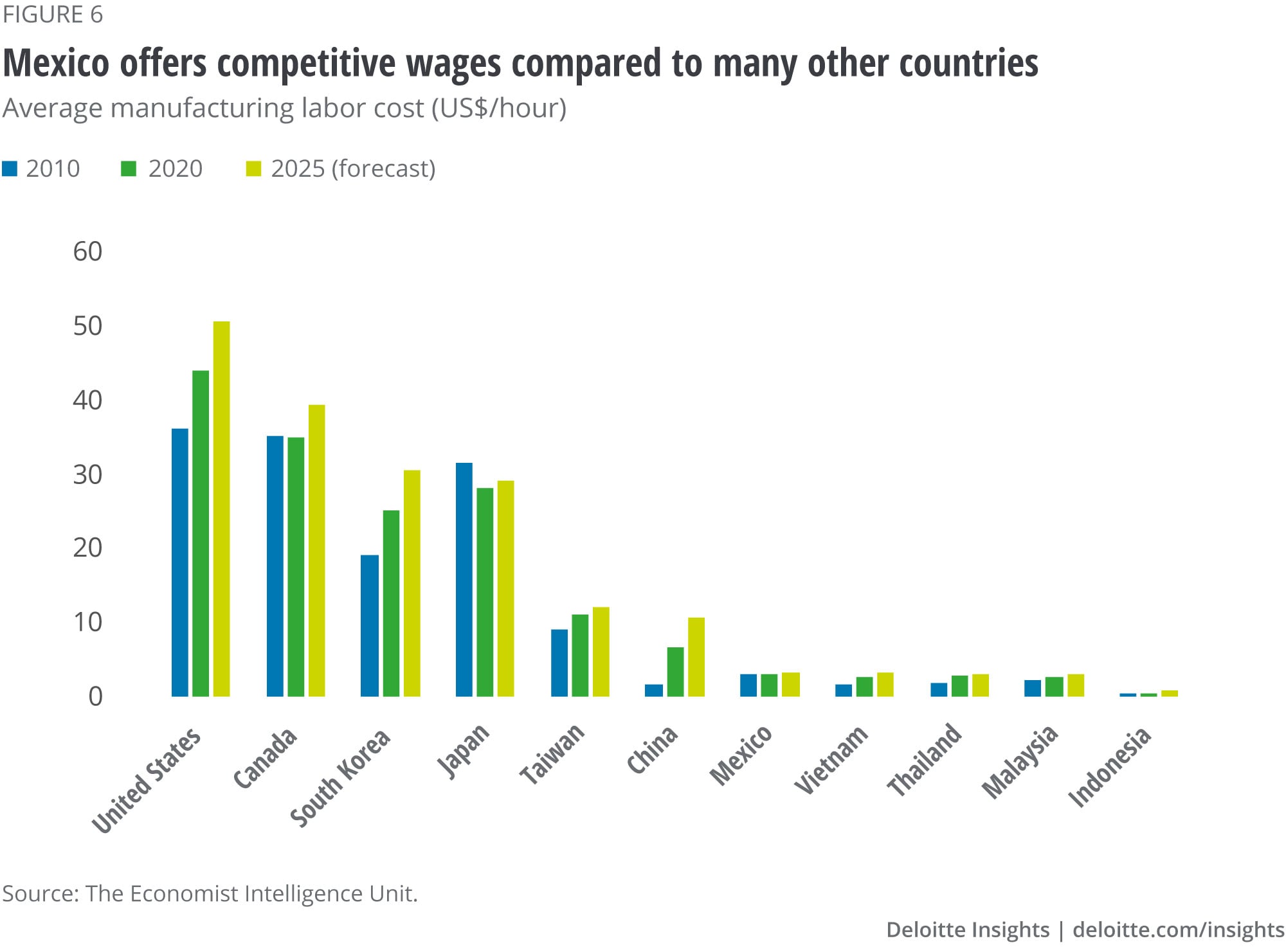

However, production costs are far higher in the United States than in Mexico, a factor that is fueling discussions around nearshoring42 among US companies.43 Mexico is strategically positioned if this scenario becomes a reality, as the country offers close proximity to the US market, a young workforce with competitive wages (figure 6), a range of flexible trade agreements with more than 40 countries, and duty-free access to the United States—advantages that cannot be ignored.44

Although we do not expect a large-scale relocation of supply chains out of Asia,45 at least in the medium term, given that Asian countries remain highly competitive in terms of costs and other comparative advantages, supply chain diversification is on the cards. The question is: Will Mexico be able to take advantage of this opportunity? Let’s illustrate this idea through an example.

According to the data released by Commerce Department’s Office of Textiles & Apparel (OTEXA), US jeans imports increased 32.9% in the first seven months of 2021.46 This spike was driven by a combination of a rebound in jeans production by Asian suppliers and significant contributions from key Western suppliers. US jeans imports from Mexico, as per OTEXA, jumped 55.4% in the first seven months of 2021 to a total value of nearly US$353 million, capturing in the process approximately 18% market share. Furthermore, imports from Nicaragua increased 39.5% and those from Colombia rose 4%. Shipments from Cambodia, in contrast, grew a moderate 5.8% in the same period, those from Vietnam decreased 4%, and from Indonesia declined 23.8%. Jeans manufacturers maintain that, under the current context, they are looking for suppliers that are close by in order to avoid bottlenecks in supply chains and higher transportation costs.47 If Mexico takes cognizance of these developments and acts in time, it can provide a much-needed boost to its economy.

Despite the great advantages that Mexico offers, several factors hamper its potential. On the one hand, low manufacturing costs in Mexico and a large production capacity for a variety of goods position it as one of the best nearshoring destinations for the United States. On the other hand, low levels of productivity48 and lack of specialization in some other goods, such as semiconductors,49 put it on a weaker footing. Another factor that can hinder Mexico benefitting from the nearshoring opportunity is its adverse investment environment. As discussed earlier in the article, some internal policy decisions have damped business confidence and if public policies do not create optimal conditions to attract investments, the nearshoring opportunity may not be fully utilized.

In summary, Mexico’s economic recovery is losing momentum in the absence of a stimulus plan large enough to jump-start economic growth. Moreover, in 2022, the risk of steeper interest rates and higher inflation are likely to remain in place. However, in light of the recent discussions around the possible reorientation of the global supply chains, a nearshoring opportunity has emerged for Mexico, which, if grabbed in time, has the potential to help the country reverse years of slow growth in investment and in fact propel it to higher growth in the coming years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}