{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

India has been saved

Cover image by: Jaime Austin

The economy was gradually turning towards recovery early this year until the much more severe second COVID-19 wave hit India in April. The comforting news is that improving business sentiments, coupled with a strong recovery among industrial nations, propelled growth in the January–March quarter of FY2020–21. While substantial spending by the government provided the biggest boost to growth, private investments and goods exports—in segments such as engineering goods, chemical products, and pharmaceuticals—did remarkably well in the last quarter of the fiscal year.

What, however, emerged as a worrying trend (from the GDP numbers) is that traction in consumption spending seemed restrained, highlighting spending hesitancy due to health and financial anxieties. With more COVID-19 variants emerging across the world and certain mutations suggesting variants of concern, the ebb and flow of the pandemic is likely to continue.1 This raises several questions: How damaging would the impact of successive waves be on the economy? Can consumers eventually shirk off their anxieties and resume spending with confidence? While we pin our hopes on pent-up demand to lift recovery, are there any risks that may materialize?

We responded to the first question in our earlier publication (see “The tunnel just got longer, but you can still see the light” for more details)—we are cautiously optimistic about the economy’s ability to bounce back once we tide over the second wave.2 Successive waves will likely have a diminishing economic impact as a larger proportion of the population gets vaccinated. Recovery, however, is likely to be delayed and will flow into the next fiscal year.

In this report, we try to answer the other two questions. High-frequency data suggests that consumers are yet to recover from the emotional and financial scars of the second wave. While the upper-middle or higher-income class with larger savings are longing to spend, the weakening labor market, rising inflation, and deteriorating household balance sheets are risks that may test the resilience of a majority of consumers for some time. To bring back consumer confidence, India must vaccinate its population rapidly. At the same time, it is important for policymakers to understand the above risks looming over pent-up demand that we are so relying on for a strong recovery. That way, they can take quick actions to prevent these factors from spinning out of control.

While infection spread affects health and confidence, it is the mobility restrictions that hurt the economy the most because they simultaneously impact both demand and supply. However, data suggests the impact on demand has lingered longer than on supply this year. After the first wave, manufacturing and industrial activity bounced back strongly. But consumer spending (in the GDP component) and the sectors requiring social interaction, such as hospitality and travel, grew modestly, suggesting that pandemic-related uncertainties weighed on consumers’ minds.

The second wave has probably accentuated the difference in demand and supply recovery further. This is because different states enforced slightly more relaxed rules for industrial activity and goods movement this time, compared to last year’s nationwide lockdown. Consequently, economic activity continued, albeit at a slower pace, despite supply chain disruptions, logistics challenges, and lower productivity. The manufacturing PMI dropped to a 10-month low of 50.8 in May 2021 and further to 48.1 in June.3 Industrial production growth also fell in May and manufacturing activity regressed to the lowest levels since August 2020. Due to the shutdowns of several car manufacturing plants, production of passenger cars and two- and three-wheelers in May 2021 were 58% and 56.8% lower than their corresponding levels of April 2021, respectively. As the infections gradually peaked and came down in June 2021, states opened up slowly and several supply-side challenges started coming down.

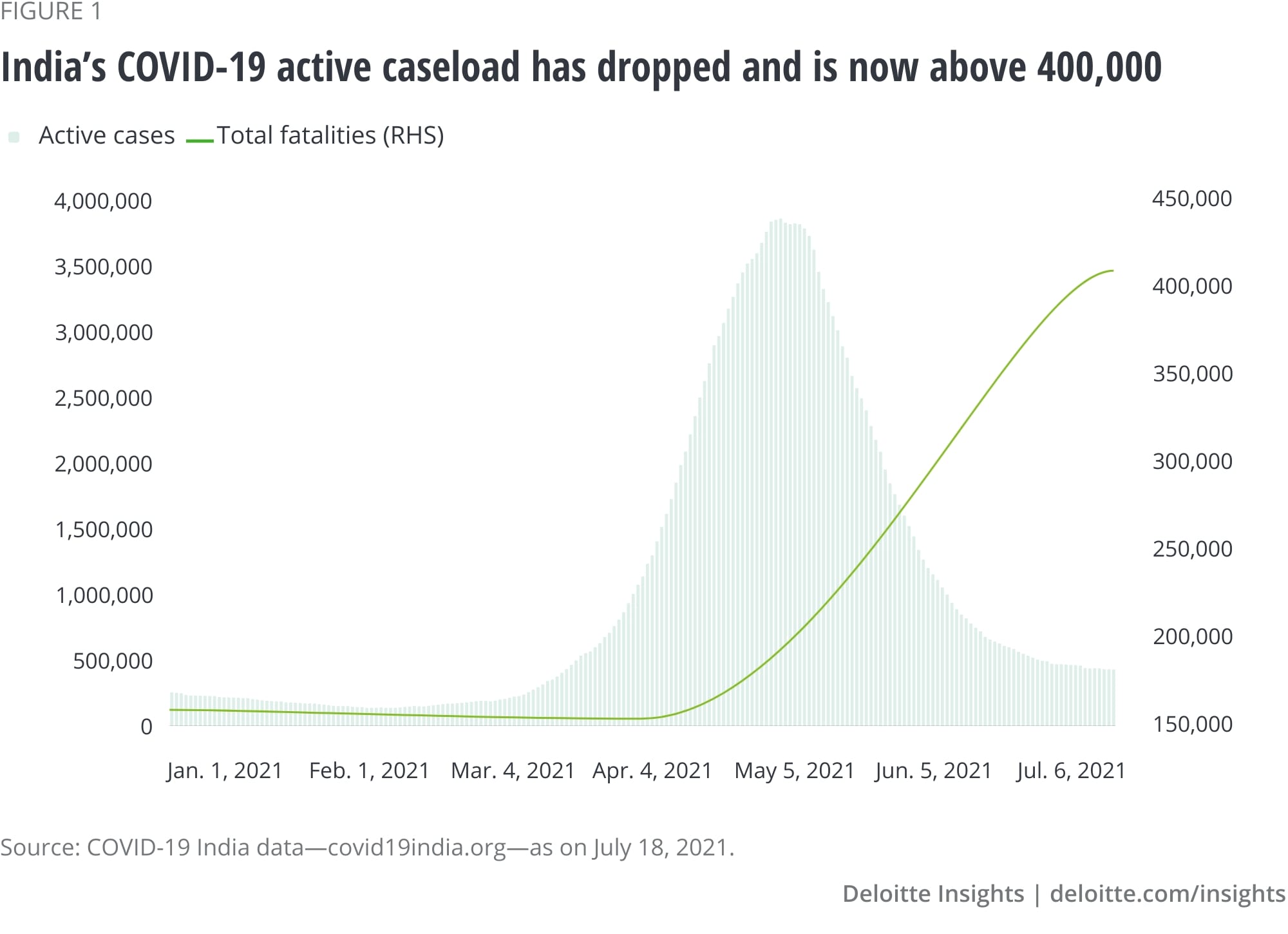

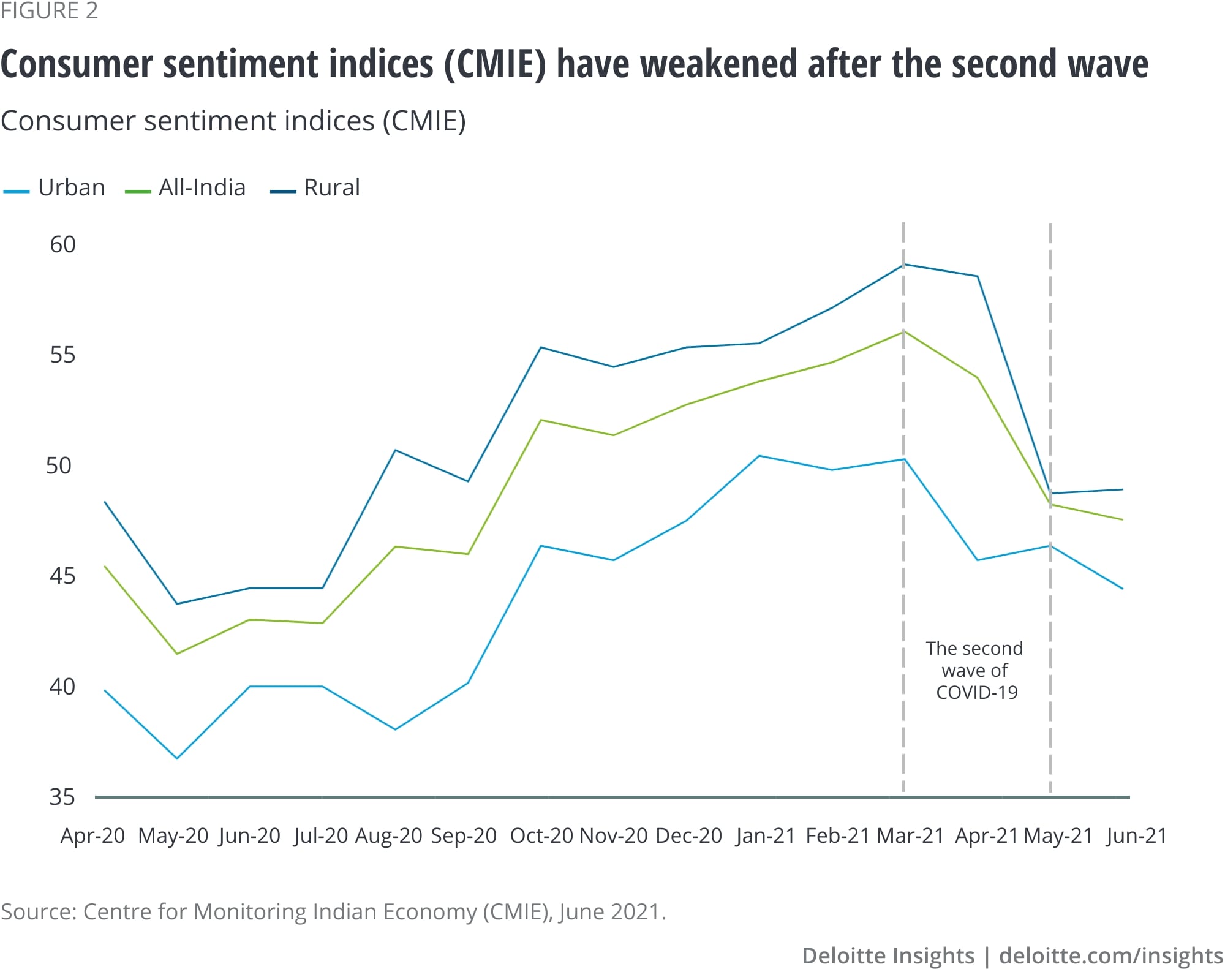

On the other hand, the impact of the second wave on human health and lives has been far more severe than the first wave. The fear and uncertainties associated with the virus, which has proven to be more indomitable than previously assumed (figure 1), have shaken consumer sentiment yet again, with the index reporting a consistent decline since March 2021, cumulatively dropping by a substantial 15.4% between March and June (figure 2). Unlike the first wave,the infection spread this time has been much more widespread and reached even the remotest locations, as suggested by India’s COVID-19 data.4 This has severely impacted rural sentiments and income and, therefore, one can expect rural demand to be relatively subdued compared to last year.

While there are not many high-frequency indicators to gauge the impact on demand, one can intuitively infer from the footfall in transit areas and recreation and entertainment centers (as indicated in the Google mobility index) that shoppers refrained from spending.5 In addition to the lockdowns, the hassle of traveling and the fear of falling sick were reflected in the reduced passenger traffic at railway stations and airports. Railway passenger traffic declined by 33% in April 2021. In the first 20 days of May 2021, passenger bookings shrank by 66% compared to the corresponding period of April 2021.6 Domestic air passenger traffic fell to 11.09 million in April 2021 from 15.3 million in March 2021 and further to 3.9 million in May 2021.

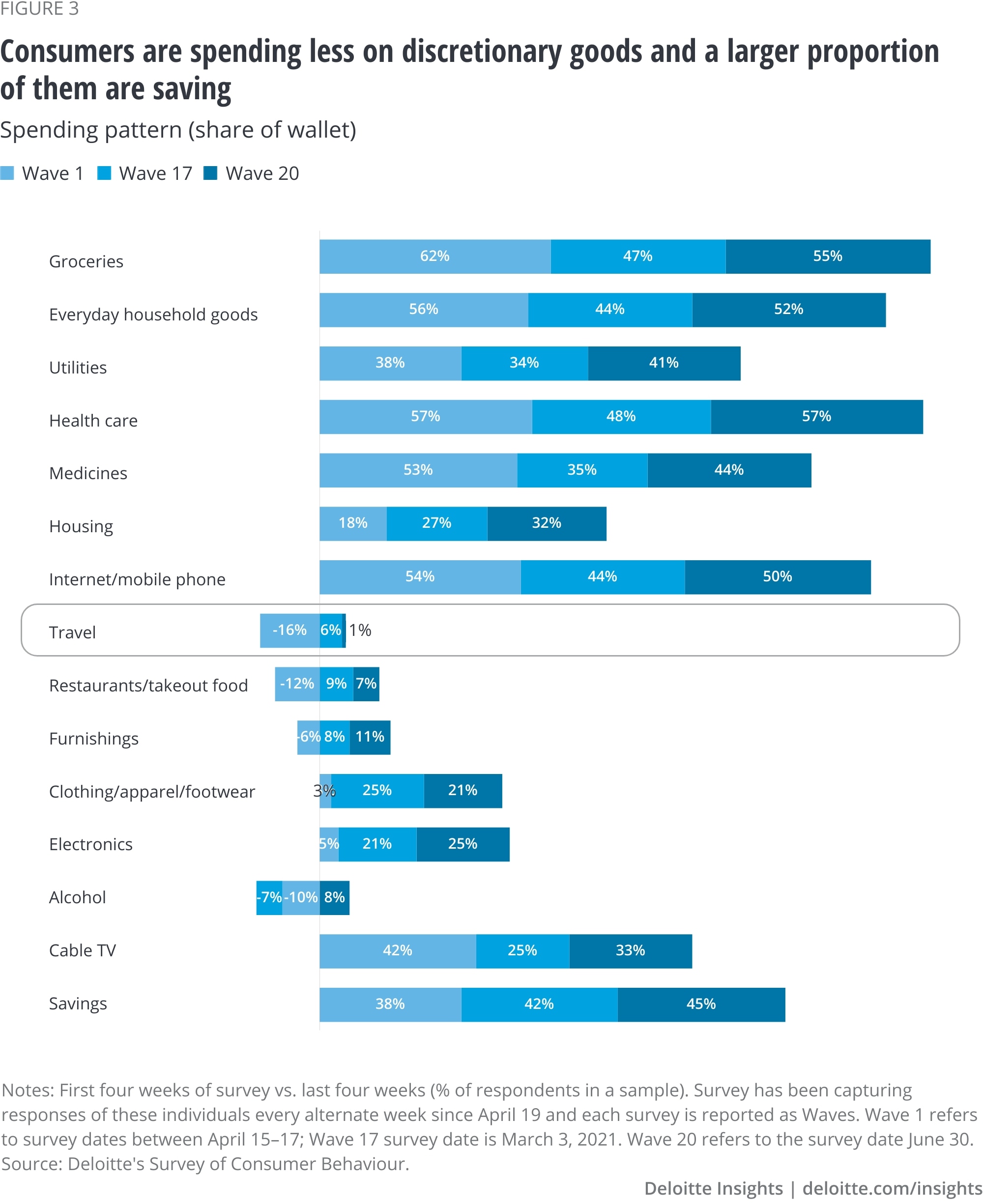

According to Deloitte’s Survey of Consumer Behavior, consumers’ spending intent, which was recovering after the first lockdown, reversed after the second wave (figure 3). The inclination to spend on essentials such as groceries, household goods, and medicine rose sharply in June 2021 compared to early March 2021. Travel sentiments improved after the first lockdown and peaked in March 2021. A few noticeable changes were observed: The proportion of people wanting to save more has consistently gone up and there is a perceivable shift away from using public transit and ride-hailing services.

In short, consumers are anxious and are saving for rainy days.

While infection anxieties persist, other risks—all results of the ebb-and-flow nature of the pandemic—may weigh on consumer sentiment and cap the pace of recovery.

Inflation: From the onset of COVID-19, inflation hovered around the upper range of the Reserve Bank of India’s target inflation range (2%–6%), and exceeded 6% during the second wave.7 It’s expected to remain high with several factors contributing to price pressures:

Higher prices are likely to increase production costs and erode the purchasing power of consumers. Risks of inflation can dent the demand recovery and weigh on pent-up demand.

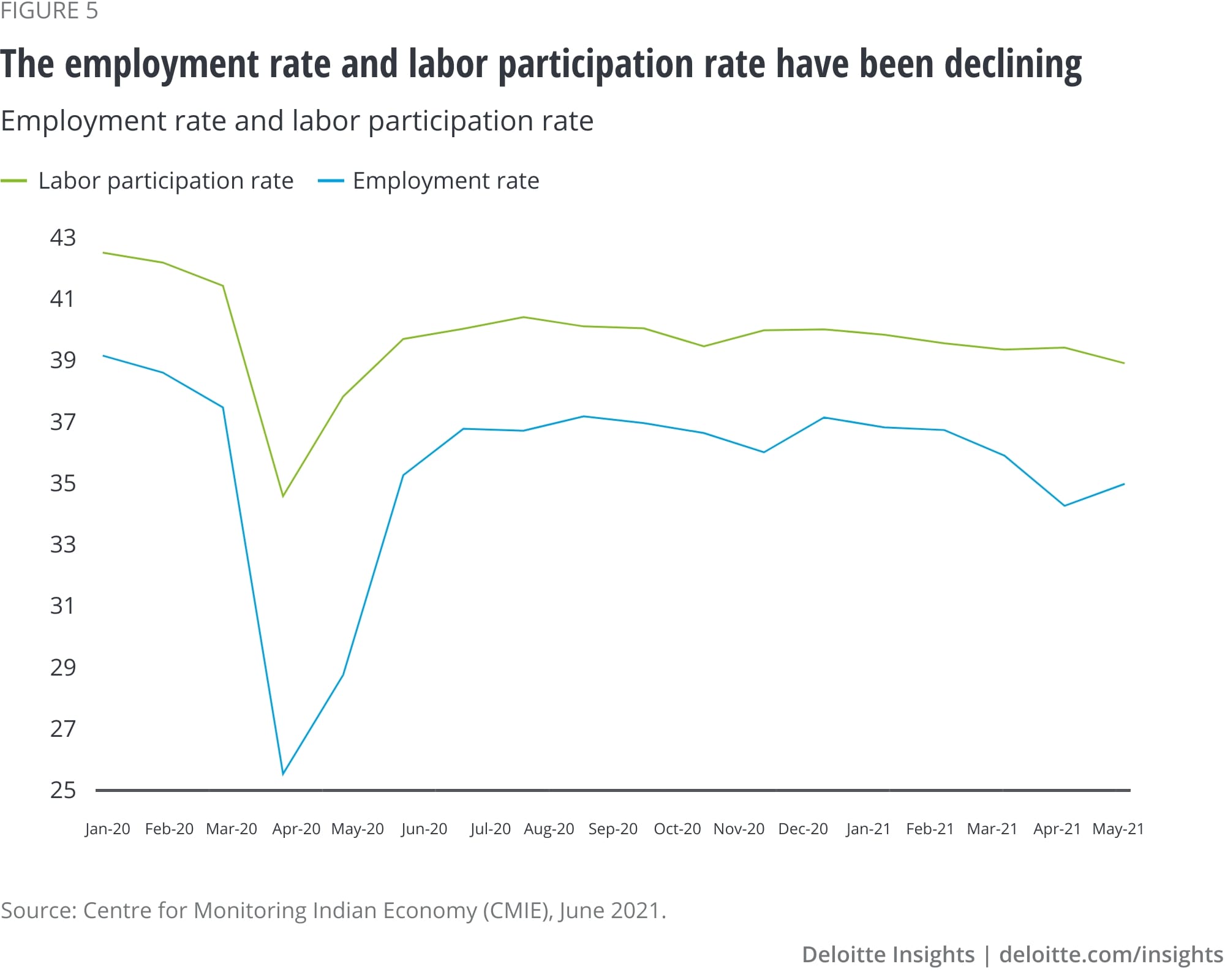

Labor market: Recurring lockdowns and mobility restrictions across the country have resulted in a weak labor market. India lost 22.7 million jobs during April‒May 2021, with the workers in the low- and semi-skilled and informal sectors bearing the brunt.8 Close to 17.2 million daily wage earners lost jobs as against 3.2 million salaried employees. Agriculture absorbed 3.4 million of the total losses. With easing lockdowns, the unemployment rate improved and 7.8 million jobs were back in June. However, the weakness in other labor parameters continue to be a matter of concern.

As the first lockdown of 2020 eased, the unemployment rate started to show hints of recovery; however, the labor participation rate (LPR) and employment rate (ER) continued to remain low. This is an indicator of a shrinking labor market, adding to a sense of dejection among the workers no longer pursuing employment. The second wave has had a devastating impact on LPR and ER, which, despite the improvement in unemployment rate, are unlikely to recover swiftly (figure 5).

Weaker household balance sheets: According to Pew Research Center, the pandemic has resulted in a sharp fall in the middle class and a rise in poverty in India.9 Growth in savings has fallen sharply from 21% of GDP in Q1 FY2020–21 to 8.2% in Q3 FY2020–21.10 At the same time, personal disposable income, as reported by Oxford database, declined for the first three consecutive quarters of FY2020–21. During this period, households borrowed heavily to meet expenses and, as a result, debt spiked to 37.3% of GDP in FY2020–21, up from 32.5% last year.11

The impact on savings and income growth after the second wave will likely be much more severe. According to a report by CMIE, the proportion of urban households that claimed their incomes were higher than a year ago dropped from 4.9% in May 2021 to 4% in June, and those that said incomes worsened increased from 51.4% to 52.3% during the period. In addition, the severity of the impact on health may have compelled households to spend more on health care and treatments.12 The decline in bank deposits in FY2020–21 suggest that households are continuing to borrow to meet increased health expenditure. This may result in a further increase in household debt to GDP in FY2021–22.

There is one segment of the population, primarily belonging to the upper-middle or higher-income class, which has been saving for the 1.5 years and is eager to spend but is limited by fears of the contagion.13 Once a significant portion of the population is vaccinated and this segment feels confident enough to step out of their homes more often, it will drive demand, spurring economic activity at a sustainable pace.

However, if the pent-up demand has to be broad-based and able to drive growth, there’s no alternative but to rapidly vaccinate the population so that successive waves have a marginal impact on the economy. Additionally, policymakers need to understand the three risks (highlighted above) that have implications on the confidence, willingness, and ability among consumers and can deter them from spending to their potential. The government has to make concerted efforts in creating jobs, especially for the youth and the semi- and low-skilled, educating and training workers to prepare for the future workforce, and implementing reforms and schemes quickly to improve the business ecosystem and kickstart private investment. The other measure could be to promote the exports sectors (through creating capacity and incentives) to take advantage of the improving global activity.

We remain cautious, but optimistic. With the right policy interventions, these risks can be minimized and consumers will gain confidence and be able to wade through the uncertainties to resume spending soon.