Eurozone has been saved

Cover image by: Tushar Barman

The second wave of the pandemic that started last autumn has hit the Eurozone harder and much longer than expected. High infection numbers and a slow vaccination rollout have resulted in ongoing restrictions on economic activity in the region in the first quarter and the beginning of the second quarter of 2021. Even then, business sentiment remains surprisingly optimistic, reaching new heights driven by the hope of an end of the pandemic and rising global demand. Thus, while the recovery remains interrupted since the last quarter of 2020, it is still likely to take off once the pandemic is under control.

Many analysts expected the Eurozone to ease the COVID-19–related restrictions on its economy by the end of the first quarter, based on the assumption that the pandemic would be largely under control by then. Unfortunately, this did not happen. In fact, Oxford University’s Stringency Index, which measures the strictness of COVID-19–related restrictions, shows that the major Eurozone economies have placed restrictions that are at a level similar to what it was in the first wave (figure 1).

These restrictions take a variety of forms but, generally, they involve the closure of nonessential stores and contact-intensive services. Schools are closed in Italy and France, while curfew is in place in Spain, France, and parts of Germany.1 In France, travel within the country is forbidden and personal mobility very restricted. Given the current infection rates, these measures will likely be in place in most countries at least until early May and will influence economic performance in the second quarter. A sustained easing of lockdown measures on a broad scale seems very unlikely to start before mid-May. No official data is available yet for the first quarter, but it can be assumed that the Eurozone economy contracted. Deloitte estimates a contraction of 0.5% took place during the quarter.

Meanwhile, the EUR750 billion COVID-19 recovery fund called Next Generation EU2—the key economic policy instrument at a European level to cushion the consequences of the pandemic—is not operational yet. Last summer, European Union (EU) leaders decided that the EU should take on debt for the first time in its history and distribute the money to the member states mainly in the form of grants and also loans. While digitalization and climate change are the most important focus areas, political reforms too are within the ambit of the fund. In order to receive money from the fund, member states should submit plans and recommend projects that meet certain criteria by the end of April. Then a formal approval process by the European Commission and the heads of member states in the European Council will start. Payouts from the fund are, therefore, unlikely to begin before autumn. In this sense, the fund will be less important as a short-term fiscal stimulus, but more important as an instrument to modernize economies and increase productivity.

Despite the serious health situation, the economic fundamentals remain promising. Labor markets are still robust and the unemployment rate in the Eurozone has not increased, thanks to ongoing policy interventions, such as furlough schemes. In Germany, for example, there are still 2.7 million employees covered by these schemes.3 The level of consumers’ disposable income is, therefore, largely intact, a precondition for a recovery once the restrictions are lifted. Not just that, the evidence from the last round of openings after the first wave as well as consumer reactions to recent temporary easing in some member states suggest that the crisis has not left major scars in the consumer sector. Consumer spending very quickly recovered in autumn when the economy opened up, while temporary easing in spring led to an immediate surge in consumer confidence (figure 2). There is one risk, however. If the pandemic is not brought under control and restrictions continue, the risk of companies going out of business increases. As such, when jobs disappear permanently, the economic policy instruments applied in the crisis, such as furlough schemes, would be of limited help.

The second bright spot from an economic perspective is the performance of the manufacturing sector. Together with the robust labor markets, it is the key reason why, compared to the first wave, the Eurozone economy has been much less affected by the second wave. In fact, the manufacturing industry is chasing records. The manufacturing PMI is at its highest level in 24 years with record increases in output, new orders, and exports activity.4 The manufacturing sector has benefited from the strong economic performance in the United States and China that are driving exports. At the same time, the short-term outlook for exports remains positive. The RWI/ISL Container Throughput Index, an early indicator for the development of world trade, remains stable at a very high level.5

Despite the ongoing health crisis and lockdowns, business optimism in Europe is high and widespread. The results of the latest Deloitte’s European CFO survey, a survey of CFOs of more than 1,500 large companies, show that business sentiment has turned substantially. Business sentiment in the Eurozone is close to its highs since 2017 and a majority of CFOs expect revenues to rise for the next 12 months.6

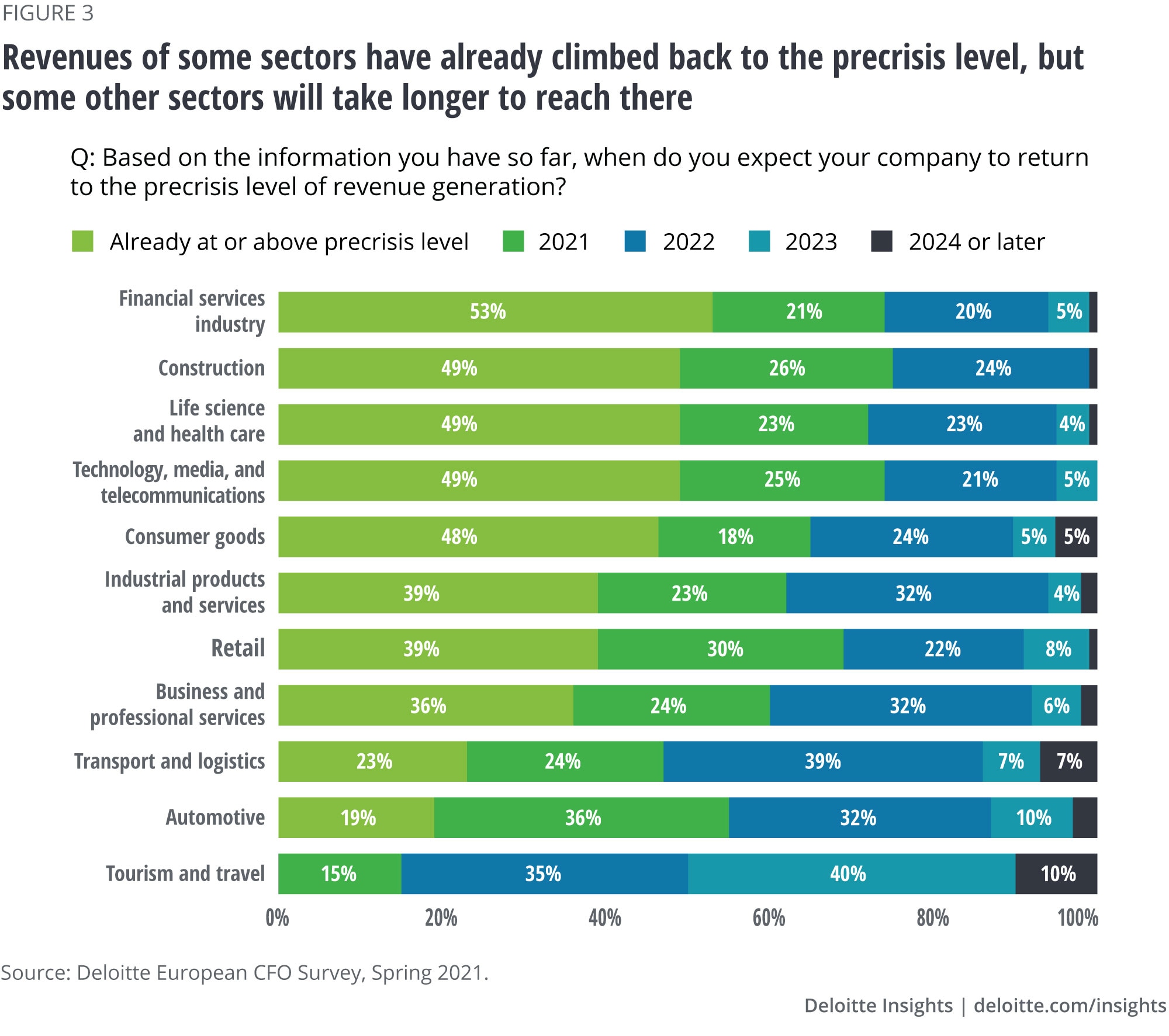

Maybe the most positive sign for a potential recovery is that the positive sentiment has led CFOs to increase capital expenditure—45% of businesses are planning to increase their capex in the next 12 months. The results show that revenues of 43% companies have already reached precrisis levels and additional 23% companies expect this to happen by the end of this year. In this sense, it seems as if the worst is over for European corporates, at least for the large companies that participated in the survey.

The improvement in business confidence is also evident from the industry cut of the CFO survey, although there are very strong sector differences. In some sectors, more than two-thirds of companies expect to return to their precrisis revenue level this year. Financial services; construction; life sciences and health care; technology, media and telecommunications; and consumer goods and retail are among them. At the other end of the spectrum, there are industries, such as tourism and travel, where the majority of CFOs think that they will reach the precrisis level only in 2022 or 2023 (figure 3).

The current situation in the Eurozone is influenced by the health crisis and improving business sentiment. There are good reasons to be optimistic that the Eurozone’s economic performance could improve and that growth could return in the second quarter and accelerate in the third. The thriving manufacturing sector, robust labor markets, and the rising investment plans of corporates suggest two things. First, that the economic fundamentals are intact, and second, that scarring in the economy, in terms of long-term consequences of the crisis, is limited. Given the progress of the vaccination rollout, we expect governments to start easing restrictions from mid-May.

As a consequence, a consumer-led recovery, on the back of accumulated savings during the crisis, is likely to develop. Deloitte Research estimates that these involuntary savings—calculated as the difference between the elevated savings rate last year and the average savings rate—amount to EUR470 billion in the Eurozone. Depending on how much of this money is spent and how quickly, a fast rebound might emerge in the second half of the year. However, this rebound will likely set in later than in other countries, such as the United States or the United Kingdom, as Eurozone restrictions have lasted longer. Therefore, we expect growth in the Eurozone to likely lag that in its international peers.

{kind=link}

{kind=link}

{kind=link}