European CFOs and the new geopolitical reality

Our latest survey of 1,300 European CFOs finds them feeling confident about their ability to make a positive impact – and yet also unsure how to face up to many risks in a world that has become more hostile

In recent years, the role of the chief financial officer (CFO) has transformed significantly. Traditionally focused on financial stewardship and reporting, today's CFOs are increasingly expected to also drive strategic initiatives, manage risks and navigate complex geopolitical landscapes. This shift reflects the growing complexity and interconnectedness of the global business environment. Despite these challenges, Deloitte’s latest survey of European CFOs finds them confident about their roles. Among 1,300 respondents, 90% believe in their ability to bring positive change to their organizations, with only 1% expressing doubt.

Respondents also confirm a trend seen in previous years of CFOs gaining more central and vital roles within their companies. Nearly three-quarters (73%) report that their influence with their company’s board has increased in the past five years, with 30% saying it has risen “significantly.” Their responsibilities have also expanded over the past five years, particularly in environmental, social, and governance initiatives (63%), risk management (58%) and digital transformation (57%).

Geopolitical risks increase but many CFOs do not have specific mitigation plans

Despite feeling empowered by their expanded roles and responsibilities, CFOs express concerns about a wide range of geopolitical threats. The world has become riskier and more unpredictable since the onset of the COVID-19 pandemic and Russia’s invasion of Ukraine. The rise of populist and nationalist sentiments in some regions, fears of a potential conflict between China and Taiwan, and the escalation of conflict in the Middle East, particularly since October 2023, add to the pressure CFOs face in safeguarding their organizations.

Our survey found that almost all European CFOs expect their businesses to be affected by geopolitics; only 2% do not. Five percent expect significant impacts, while 52% foresee some impact. Another 40% expect “limited” effects. CFOs in eight out of 13 European countries surveyed rank geopolitics in their top three risks.

European CFOs exhibit more intense geopolitical fears than their counterparts in other regions. Deloitte Asia Pacific’s 2023 survey of 276 CFOs in the region found 80% rated the risk of a global economic slowdown as their primary external risk.1 Meanwhile, Deloitte’s CFO Signals report surveyed 200 respondents in the second quarter of this year, revealing that 61% of CFOs in the United States see the economy as their leading external risk, with geopolitics and cybersecurity each cited by half of the respondents as their second most important risk.2

In response to these increased geopolitical risks, the vast majority of European CFOs (90%) are closely monitoring political and economic developments. Beyond monitoring the news, almost two-thirds (61%) are tracking structural and economic changes taking place within society and 34% are closely monitoring trends in trade and the capital markets. However, only 27%, have developed contingency plans to deal with specific geopolitical risks. Anticipating and evaluating has become a part of the CFO’s expanding role.

European CFOs focus on five domains of risk

European CFOs identify five broad domains of geopolitical risk:

- Outright hostility: The top risk includes hostility from cyberattackers, Russian aggression, attacks on shipping and a worsening of the conflict in the Middle East or the risk of conflict between China and Taiwan.

- Political populism: Political populism poses a significant threat to democracy, as evidenced by the contentious US presidential election and the rise of populist parties in the recent European Parliament election. The rise of populist parties can impact businesses in many ways, even when these parties do not win office. Markets may become more volatile due to the perception that political risks have risen. Governments may make economic policy shifts to try to diminish support for their populist opponents, such as introducing restrictions on trade and immigration, leading to operational disruptions and increased costs. Businesses may also face strategic challenges, such as reassessing investment locations and managing public relations in a politically charged environment. Companies should focus on diversifying operations and engage in robust scenario planning to mitigate these risks. The longer-term concern is about the potential direction of economic policy under populist politicians, should they come into power.

- Protectionism in global trade: Hostility between the United States and China has risen significantly in the past decade. It is now leading CFOs in Europe to fear restricted access to needed raw materials, such as rare earth minerals, and greater controls on trade in strategic technologies. They also worry about increasing friction in US-EU trade. More broadly, populist politicians make the surveyed CFOs concerned that protectionism would create further barriers to global trade.

- Climate change concerns: Climate change remains a familiar but extremely serious and difficult issue to combat, both on the macro scale for governments and societies and on the micro scale at the company level. More than a third of the surveyed CFOs see climate change as the most severe (7%) or a severe (28%) threat to their operations.

- Demographic trends: The fifth area of concern is demographic trends, especially aging societies across Europe, which also present significant challenges. Forty-seven percent of the CFOs are worried that these trends will reduce the talent pool available to them or restrict their customer base.

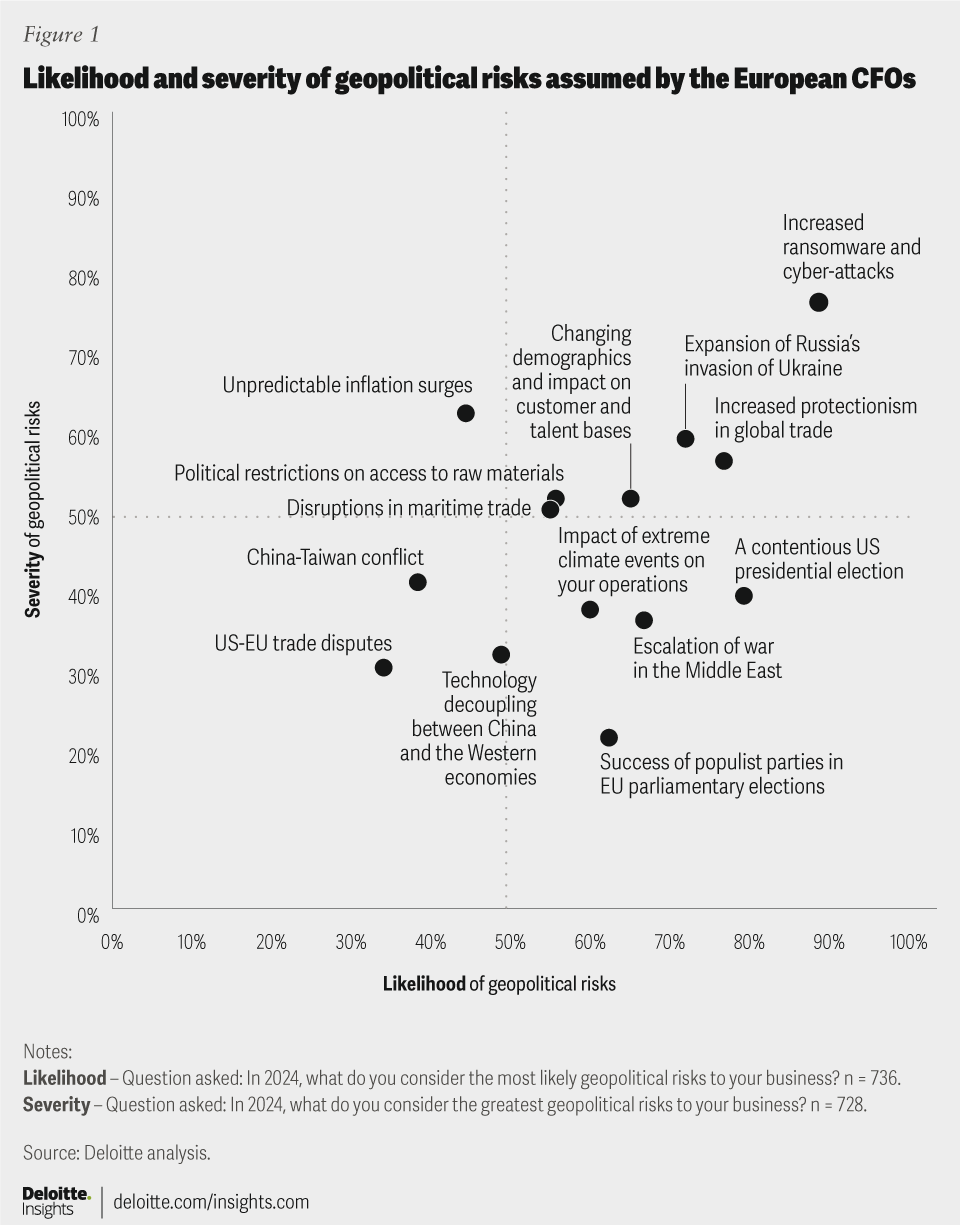

Figure 1 combines our CFOs’ assessments of the severity of different geopolitical risks and the likelihood of these risks materializing. European CFOs identify increased ransomware and cyber-attacks, the expansion of Russia's invasion of Ukraine, and heightened protectionism in global trade as geopolitical risks that hold high likelihood and high severity (top right corner of the chart). Conversely, they regard US-EU trade disputes, technology decoupling between economies, and the China-Taiwan conflict as geopolitical risks presenting a low likelihood and severity (bottom left corner of the chart).

In fear of cybercrime

Cybercrime is the top geopolitical risk for European CFOs. Nineteen percent judge cyberattacks as the “most severe” geopolitical risk, with 51% describing it as “severe.” A quarter of CFOs view such attacks as “highly likely,” and further 55% consider them “likely.”

CFOs in Germany dread political instability in the United States

Finance chiefs in Germany are particularly anxious about political instability in the United States, which has become their top geopolitical concern. This shift is notable, given that two years ago, their primary fears centered on the economic repercussions of Russia’s invasion of Ukraine. Expansion of Russia’s invasion of Ukraine no longer features in the top three risks cited by CFOs in Germany.

They have a particular reason, too, to fear the policies that the next US president may adopt. The US has become more protectionist during the past two presidencies, and the trend toward higher tariffs may persist. As Germany is the world’s third biggest exporter, behind only China and the United States, further protectionist policies would be a blow to global trade and Germany’s economy.

Although concern about the US is most intense among Germany’s CFOs, their counterparts in Sweden seem to think similarly. Their second significant worry is a contested US election, followed by fears of increased protectionism in global trade.

Inflation has fallen, but the fear of inflation remains

Inflation remains a significant concern for European CFOs despite recent declines in inflation rates. With the eurozone’s annual inflation rate at 2.5% in June 2024, significantly lower than the 5.5% annual inflation rate a year earlier, fears of renewed inflationary pressures persist. With protectionist winds blowing, a war raging in Ukraine, and a renewed conflict in the Middle East placing shipping in the Red Sea at risk, 11% of CFOs see renewed surges in inflation as the most severe risk and 46% a severe one.

The war in Ukraine

The expansion of Russia’s invasion of Ukraine remains a primary concern for CFOs in Portugal and ranks second among finance chiefs in Italy, Norway, Ireland and Iceland. None of these countries borders Russia, proving that CFOs fear the broadening of the political and economic repercussions of a worsening conflict rather than the immediate threat of invasion or escalation. Energy, grain and other supply shortages in 2022 following Russia’s invasion caused wholesale prices for many goods to spiral bringing about inflation and fears of economic slowdown.

Building resilience in uncertain times

The diverse range of dangers presents a significant challenge for Europe’s CFOs: How can they reduce their companies’ vulnerability?

While 27% of respondents have developed contingency plans for specific geopolitical events, the other main course of action has been to diversify operations across multiple regions. On average, 21% of surveyed CFOs have taken this approach, and the figure rises to 34% in Austria.

However, some European CFOs (just 4%) have decided to reduce their firms’ dependency on China. Austrian CFOs are the most proactive, with 12% reporting that their companies now avoid trading with China.

The international trade picture is, however, complex. As we report in “Global trade and the new geoeconomic reality,” global trade has proven resilient in recent years in the face of protectionist forces, the supply chain impacts of COVID-19 and rising geopolitical tensions.3 But, in a more fragmented and unpredictable world, companies need to focus more on resilience. Supply chains should be examined for potential vulnerabilities, especially those critical to company prospects. Preparing for potential risks must become a more central part of CFOs’ growing role.

On cyber, climate and demographics, too, prevention looks better than cure

Our survey found that European CFOs are increasingly driving strategic initiatives and taking on wider responsibilities. Despite the challenges of this evolving role, they feel confident in their ability to bring positive change within their organizations. Whether acting to prevent cyberattacks, ensuring their operations are more resilient in the face of extreme client events or managing the changes to customer and talent bases brought about by shifting demographics, CFOs have a leading role in profit protection. They can, and are, ensuring their businesses remain competitive as geopolitical and geoeconomic shifts lead to ever more complexity.

About the Deloitte European CFO Survey

Deloitte has conducted the European CFO Survey since 2015, giving voice twice a year to senior financial executives from across Europe. The data for the Spring 2024 edition was collected in March and April 2024 via an online survey and reflects responses from 1,333 CFOs in 13 countries (Austria, Denmark, Germany, Iceland, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom) and across a wide range of industries.

{kind=link}