Who’s afraid of postpandemic inflation? has been saved

Cover art: Tushar Barman

Why all the worries about inflation? Aggregate demand has been artificially lowered because of the pandemic. Consumers cut back on spending. Business investment plunged in early 2020, and is still recovering. The unemployment rate is high, and millions of potential workers have left the labor force entirely. Those aren’t normally the conditions that would allow inflation to accelerate. (See Deloitte’s US Economic Forecast1 to know more about how the economy has reacted to COVID-19).

But once enough Americans are vaccinated, consumer demand could easily snap back, and lower uncertainty might induce businesses to ramp up spending on capital projects. That potential spike in demand—perhaps enhanced by US government transfers to the unemployed, to low-income households, and to state and local governments—could overwhelm the capacity of the economy to produce goods and services. And that—demand greater than capacity—is the recipe for inflation.

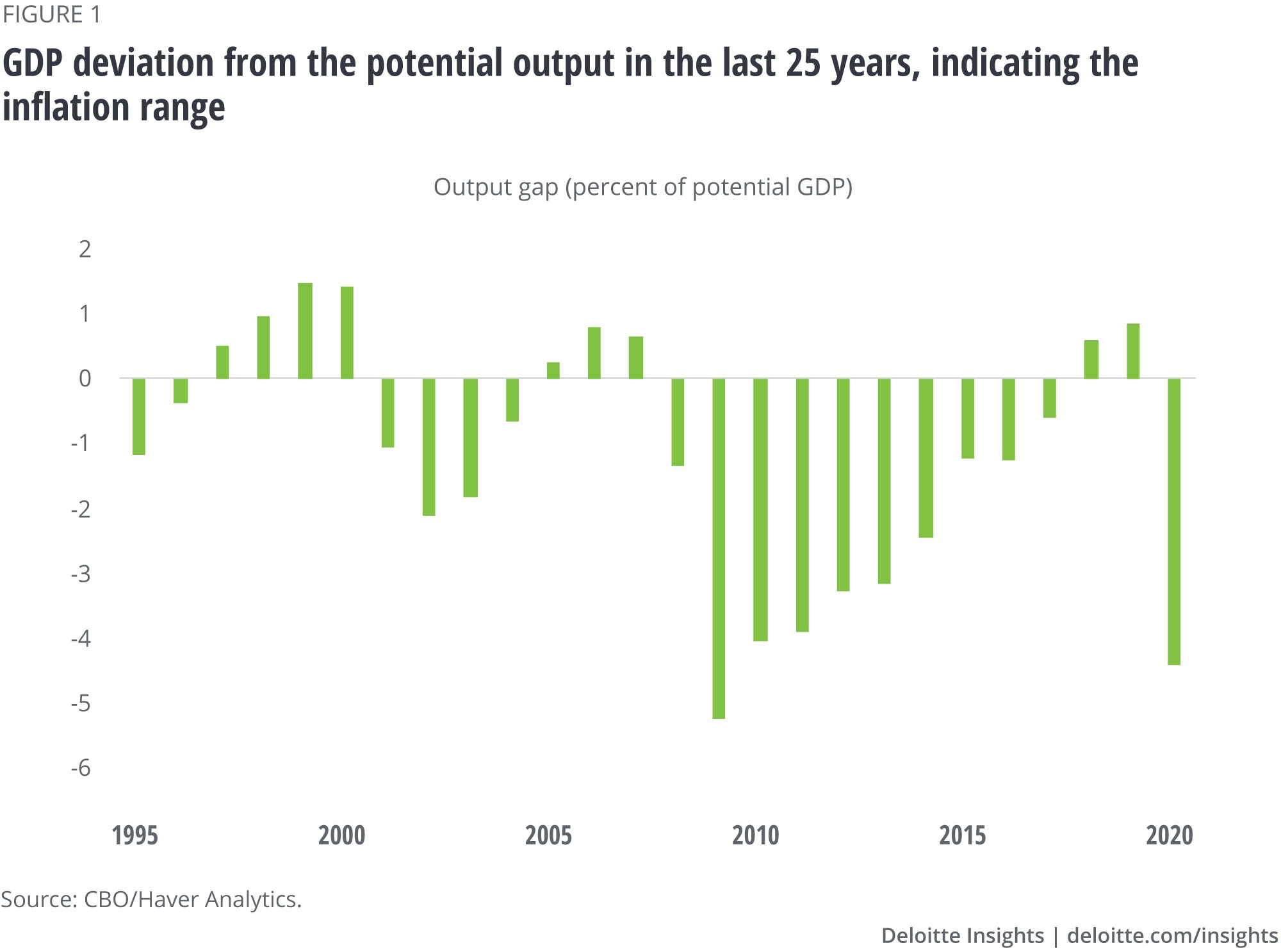

Figure 1 shows one estimate of the output gap, or difference between potential and actual GDP, since 1990. The concern, of course, is that demand (measured by GDP) could flip up above the economy’s potential later this year—likely creating shortages and allowing businesses to raise prices. In other words, inflation.

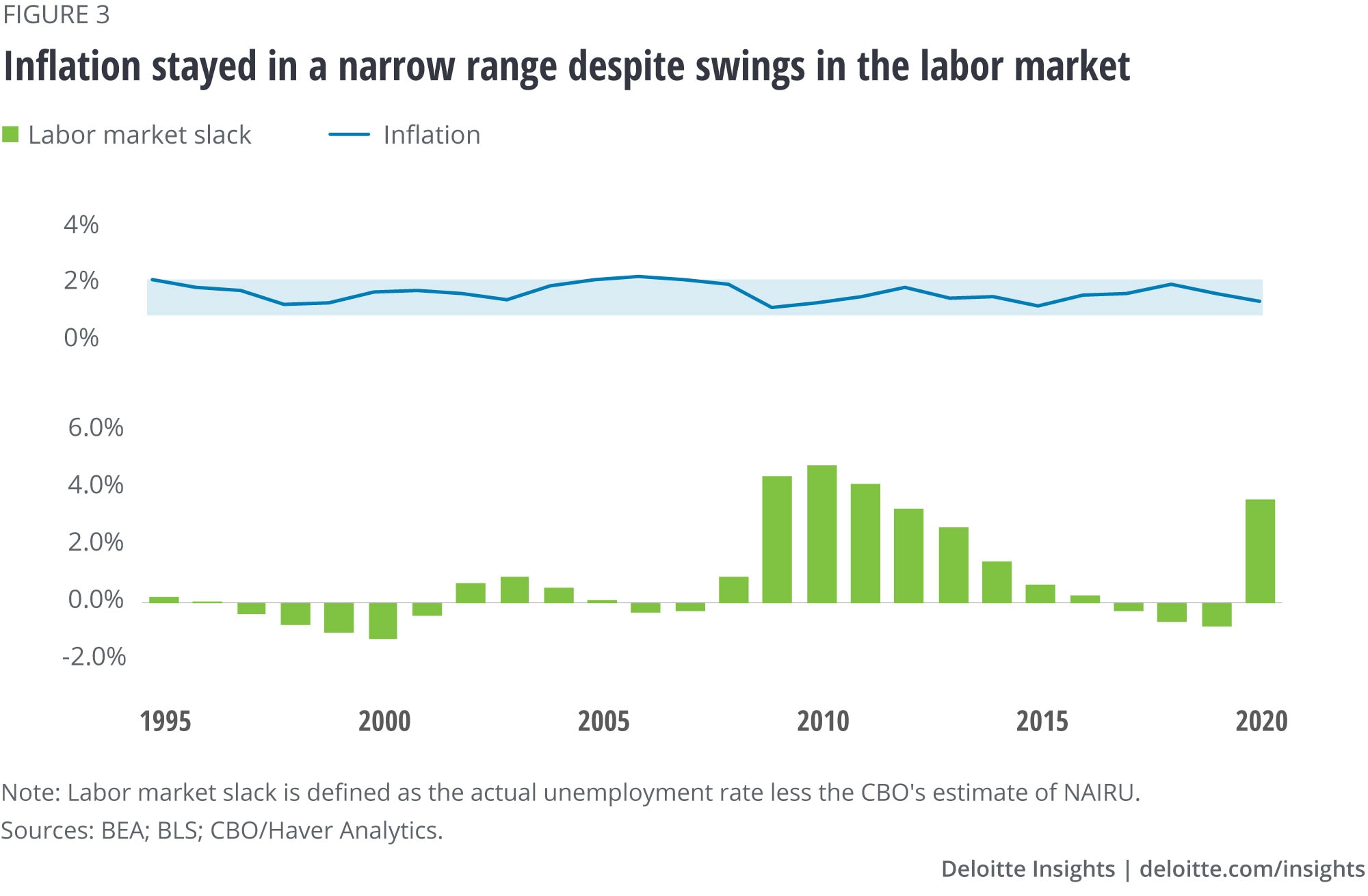

GDP was above capacity on three separate occasions in the past 25 years. During the economic recovery and boom of the 1990s, the recovery in the mid-2000s, and in the two years before the pandemic, demand outpaced the Congressional Budget Office estimate of the economy’s capacity. And yet, inflation didn’t show any signs of accelerating. Instead, over these 25 years—when the output gap ranged from 5% below capacity to 1.5% above capacity—inflation remained in a narrow range of 1.5% to 2.5%. Recent history doesn’t suggest there is much reason to worry about a moderate amount of excess demand generating much inflation.

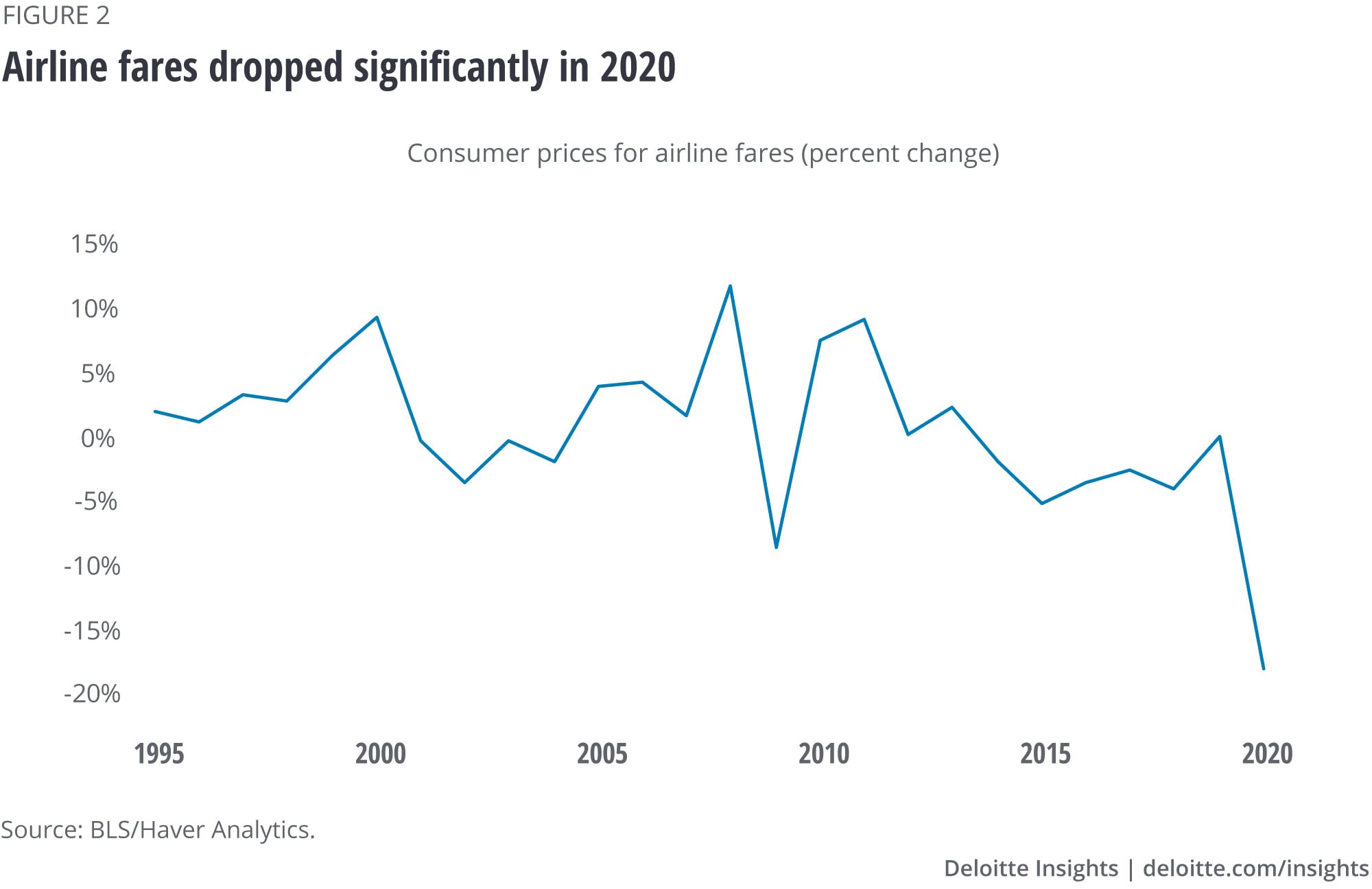

That’s not to say that inflation spikes might not happen. The pandemic created a sudden shutdown of some sectors of the economy, including travel, food and accommodation, and some leisure and recreation services. Vaccination is likely to create sudden demand in many of those same sectors. Figure 2 shows the CPI for airline fare, which plunged 17% in 2020 as airlines cut prices to cover their large fixed expenses. Since then, airlines have adjusted their capacity, by parking aircraft and freezing other resources. When demand picks up again, airlines won’t be able to recreate February 2020 operations in an instant. The full flights that might accompany the first few months of recovery may lead to shortages of seats and a runup in prices for those seats that are available. But over time airlines (and other producers in similar conditions, such as restaurants and theme parks) will be able to ramp up capacity, taking the pressure off their operations and allowing prices to settle back to longer term levels.

But a spike in prices does not necessarily translate into inflation. Prices change constantly in a market economy. They prompt economic actors to move resources into production (in the sector with higher prices) and out of other sectors (with lower prices). So, as the impact of COVID-19 fades, it is fair to expect a rise in some prices.

For inflation to kick in, those price spikes should lead to higher wages, resulting in cost pressures on businesses leading to further price hikes. At least, that’s the theory. But that theory hasn’t held much water over the past 20 years, when tight labor markets did not, in fact, lead to the acceleration of inflation. Fears of a postpandemic inflation are, therefore, overblown.

About 20 years ago, we economists thought we had inflation figured out. Turns out, we were wrong.

The conventional view of inflation was a reaction to the experience of the late 1960s and 1970s. Nobody liked the experience of high inflation, and, ultimately, monetary authorities (especially in the United States) engineered a brutal global recession in 1981–82 to bring it under control. Based on that experience, economists formed a consensus about inflation and how to fight it:

By the 1990s, this consensus had been successful in reducing inflation in the United States and other developed countries and keeping it low. Nobody should diminish that accomplishment. But more recent experience has had monetary economists rethinking their approach.

One measure of the economy’s capacity is the unemployment rate: Economists thought that if the unemployment fell below a level labeled the “natural” rate or Non Accelerating Inflation Rate of Unemployment (NAIRU), inflation would pick up. First in the late 1990s, and then again in the late 2010s, the unemployment rate went quite a bit below the NAIRU. And in the early 2010s, unemployment was substantially below NAIRU. But, as noted, the core inflation rate remained in a narrow band of 1.5% to 2.5 regardless of the condition of the labor market (figure 3).

Economists—including those on the staff at the Federal Reserve—scrambled to keep up. As a result of their research, many monetary economists now believe that the economy can run much “hotter” for longer periods of time than they previously thought. That’s why the Fed changed its operating procedure recently.2 Fed officials wanted to be clear that they are willing to tolerate lower rates of unemployment for longer than would have been the case in the past. They are also willing to tolerate more inflation, because they believe that, even at low unemployment rates, inflation is not likely to spark an accelerating wage/price spiral. That just follows from our recent historical experience.

Many monetary policy experts have essentially reversed their views on how to fight inflation. Today’s inflation fighters get their inspiration from William Prescott’s famous command before the Battle of Bunker Hill. They’ve gone from advising strong, proactive policy to quash inflation before it comes into view—keeping expectations “anchored”—to preferring to letting the economy roll, and the unemployment rate fall, until actual inflation becomes apparent.

Unfortunately, people’s perceptions of economic thought are sometimes also “anchored” in what was taught some decades ago when they took their economics classes. This holds true for economists as well. Economics is a dynamic field (as is the economy itself). Our views about the economy change as we learn more—and as the economy changes. Today’s inflation problems are nowhere near as scary as the inflation of the 1970s, and policymakers are—correctly—focused on today’s threats, not yesterday’s.

{kind=link}

{kind=link}

{kind=link}