Retail sales brace for headwinds has been saved

The author would like to thank Daniel Bachman, US Economics, for his reviews.

Cover image by: Jaime Austin

More than two years have passed since the deepest economic impact of COVID-19 in the United States. Retail sales1 too felt that pain before starting a swift and strong recovery.2 Sales have grown by more than half since the trough of April 2020 and are now 28.8% above prepandemic levels. This recovery, however, hasn’t been uniform. Online purchases thrived during the pandemic and continue to do so. In contrast, it took more than two years for sales at electronics and appliance stores to return to pre-COVID-19 levels. Sales at all store types, however, are higher than figures in February 2020. Even clothing and accessories stores and food services and drinking places, which suffered deeply in 2020, have bounced back.

Future retail sales growth faces offsetting problems. First, strong consumer demand for durable goods during 2020–2021 is giving way to more spending on services as the pandemic eases in intensity. While stores selling durable goods face slowing consumer demand, food services and drinking places will likely benefit. Second, high inflation is likely to weigh on consumers’ purchasing power and, hence, spending. This may dent retail sales volumes. In contrast, high inflation will offer tailwinds to the value of sales. Volumes, however, may be hit more if the economy slips into a recession in 2022–2023.3

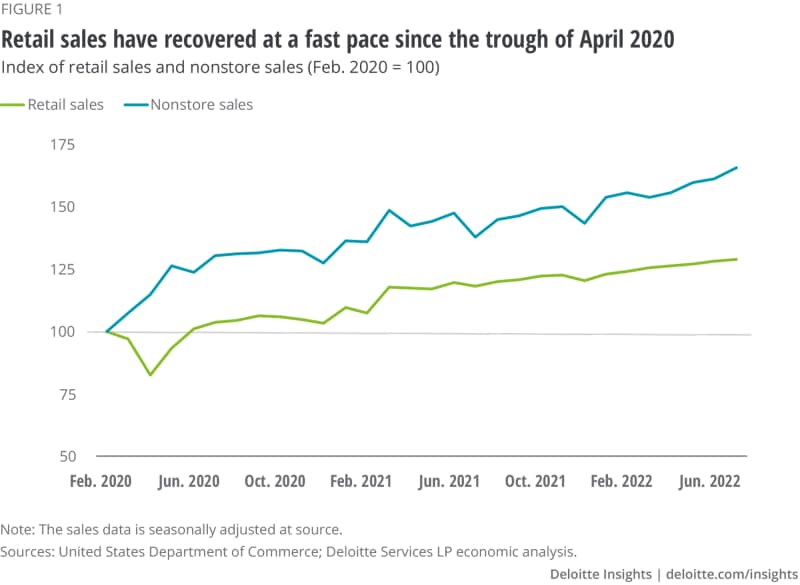

If the downturn of February–April 2020 induced the sharpest fall in retail sales (17.3%) during a recession in recent memory, the recovery in sales has been one of the fastest. The steep contraction and recovery in sales is mainly due to the nature of the downturn in 2020. While previous recessions have occurred due to economic or financial factors, the one in 2020 was pandemic induced. The sharp drop in retail sales during those initial months was due to people’s fears of contracting the virus, social distancing restrictions, and the rise in remote work. As the initial panic wore off and the economy reopened gradually, sales picked up (figure 1), with vaccinations in 2021 adding to the momentum. Figure 1 also highlights a key impact of the pandemic on retail sales—the rise in online shopping. As people tried to keep person-to-person contact to a minimum, nonstore sales surged. In fact, between February and April 2020, nonstore sales went up by 14.6%, even as total sales plunged.

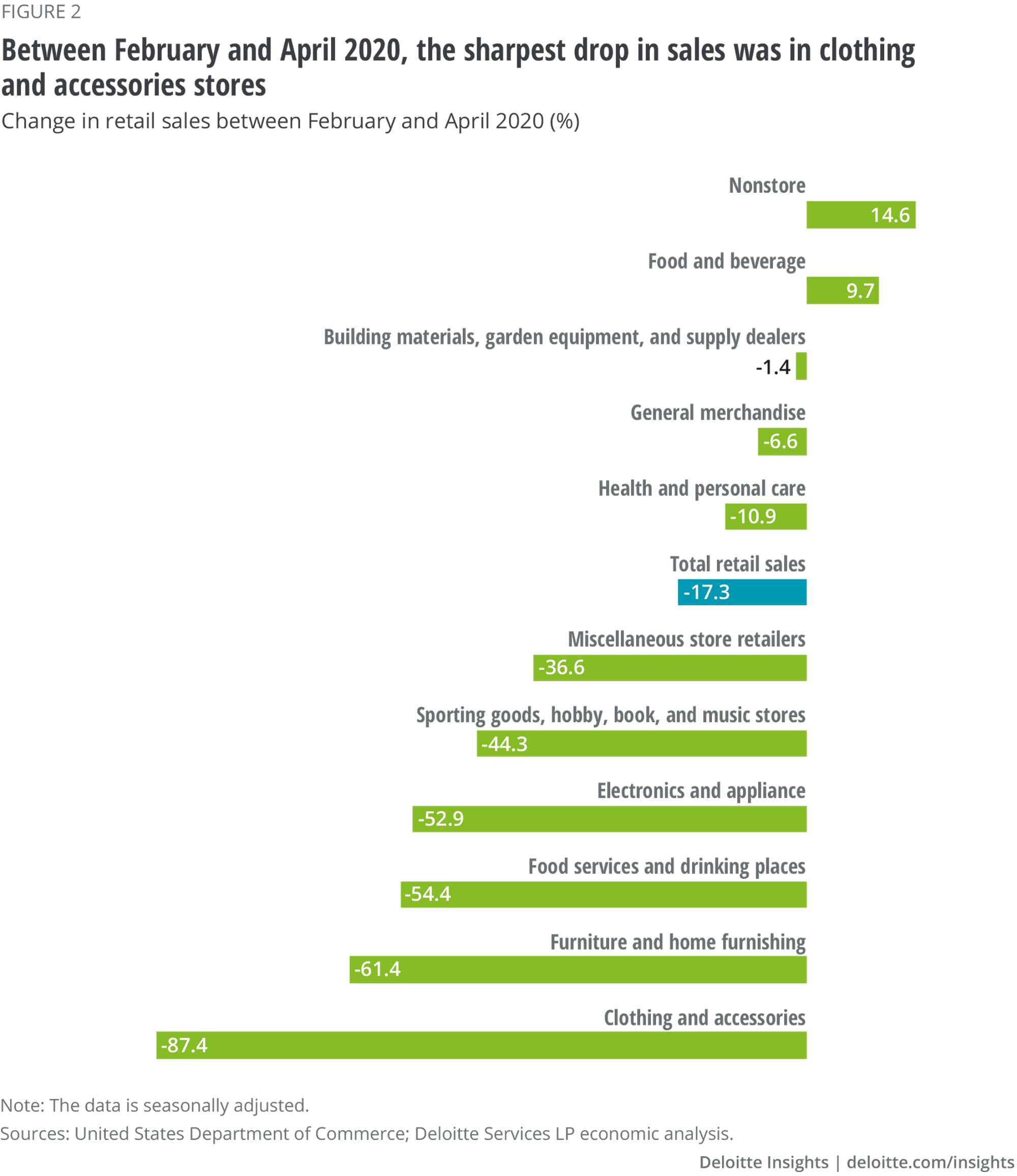

In the initial months of the pandemic—when people mostly stuck to their homes, social distancing measures were in force, and some businesses shifted to remote work—consumer and business spending fell more in certain key segments. Consumers prioritized stockpiling of essentials like food during these initial months, certainly not clothes. No wonder that the sharpest drop in sales among different store types between February and April of 2020 was in clothing and accessories (-87.4%). In contrast, sales at food and beverage stores went up 9.7%, the only store type to witness a rise in sales during this period (other than nonstore sales). People preferred food at home when going out to restaurants and pubs seemed a tad foolhardy; figure 2 shows the big drop in sales at food services and drinking places by April 2020.

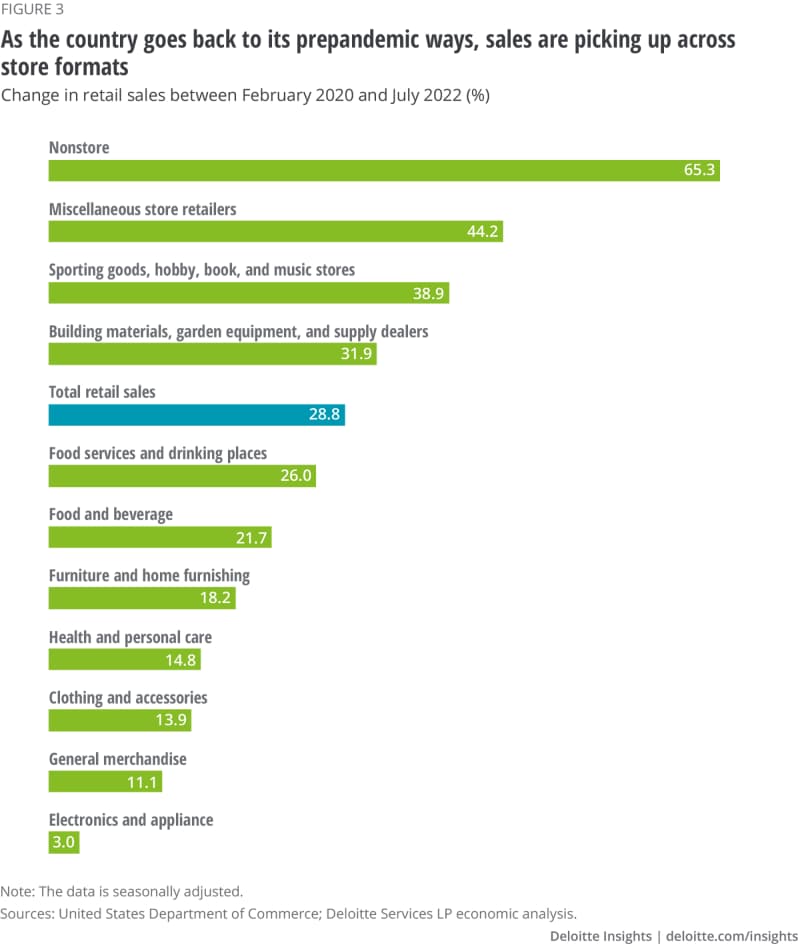

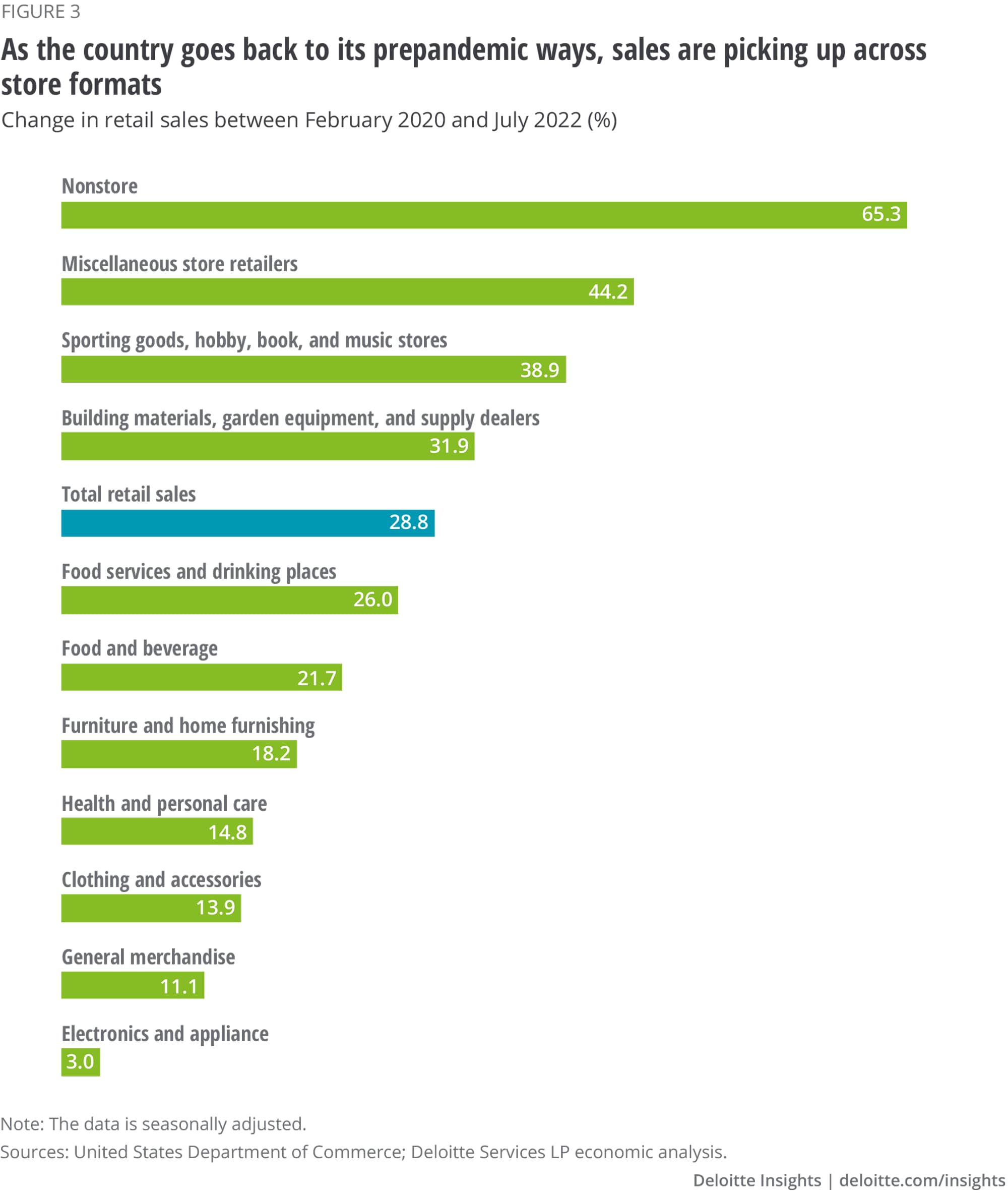

Figure 3 shows the recovery since April 2020. Sales at different store types picked up after the economy opened in mid-2020. Rising vaccinations last year have helped, even as consumers and businesses have also got better at “living with the virus.” With more people back in offices—some in a hybrid mode—and travel and leisure making a comeback in people’s lives, certain store types have experienced a strong boost in sales. At food services and drinking places, sales are now 26% above prepandemic levels. Even clothing and accessories stores are witnessing strong gains, as figure 3 shows, which is a sharp reversal of fortunes compared to April 2020. Nonstore sales also continue to remain healthy, up by 65.3% from prepandemic levels. It is evident that people are more comfortable with online shopping in the postpandemic era compared to pre-COVID-19 times.

For certain store types like sporting goods, hobby, book, and music, sales are losing a bit of steam (figure 4), even though the value of sales may still be high compared to prepandemic figures. This is likely due to a shift in consumer spending since mid-2021 to services from goods (especially durable goods). After all, there is a limit to the amount of gym equipment and sporting goods that one can buy. Figure 4 also shows that sales at building materials and supply dealers has been slowing since March this year, as demand in the residential housing market slows due to high home prices and rising cost of borrowing.

Three key trends will influence retail sales growth.

First, consumer spending4 on services has been picking up steadily as consumers flock back to pubs and restaurants, go on vacations, and enjoy sporting events as they did before the pandemic. Pent-up demand is also playing a part as consumers dip into their savings to make up for what they missed during 2020–2021. In contrast, durable goods, the mainstay of consumer spending in 2020, is slowing (figure 5). A shift in spending to services will therefore weigh on retail sales at consumer durable stores. However, the shift to services is expected to provide some tailwind to food services and drinking places.

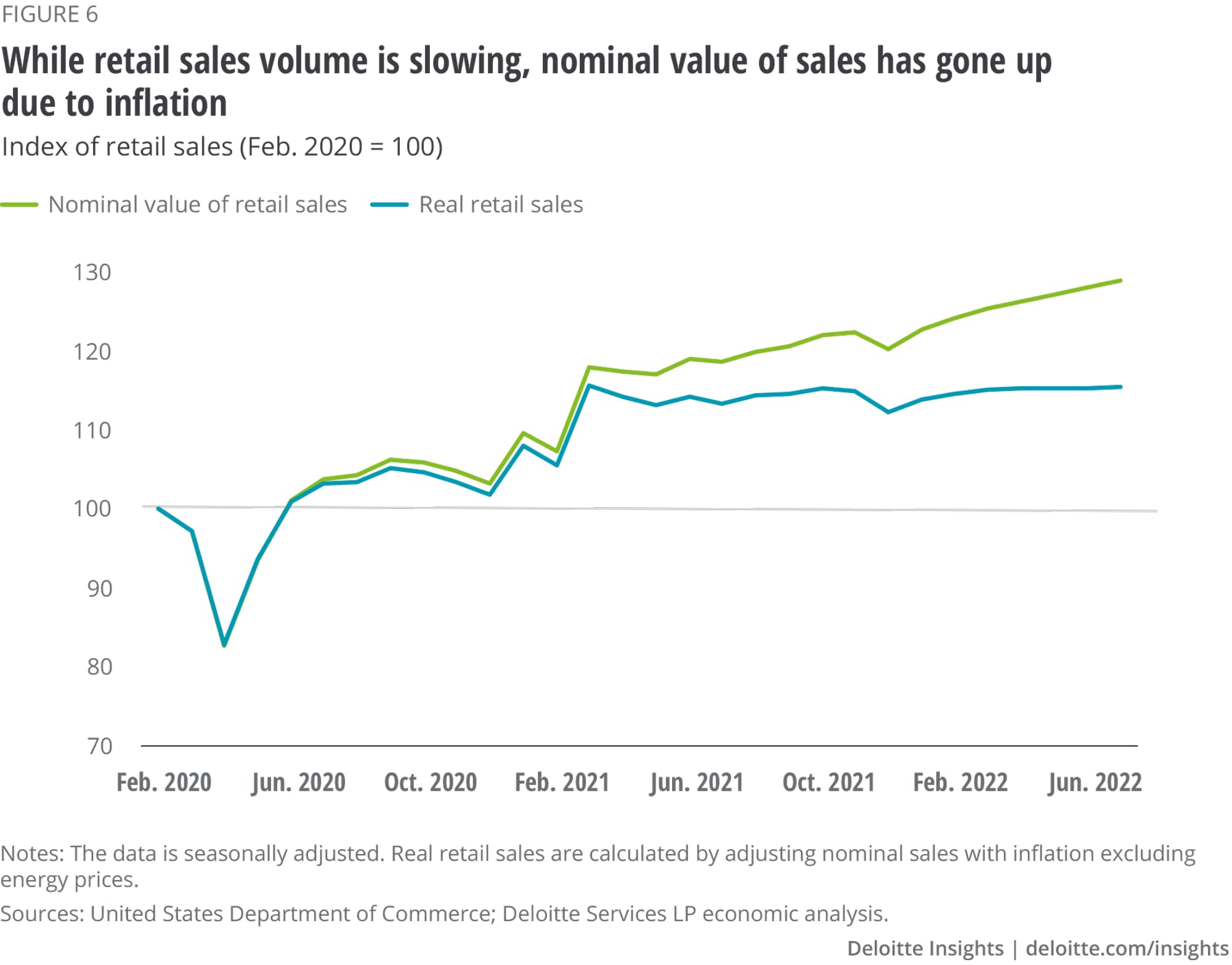

Second, inflation5 is denting consumers’ purchasing power, despite gains in nominal income due to a strong labor market. For example, even though nominal average weekly earnings have gone up by 7.5% since December 2020, real earnings have contracted by 4.7%.6 This is likely to weigh on consumer demand and, hence, volume of retail sales. Deloitte’s survey of consumers shows that the share of respondents who intend to delay large purchases has been going up since mid-2021.7 The same survey shows that worries about savings have gone up too,8 which is hardly surprising given that the personal saving rate (5.1% in June) is lower than pre-COVID-19 levels. Rising prices, however, will aid the nominal value of retail sales. Figure 6 shows nominal retail sales and real retail sales9 since February 2020 with the two series diverging since March 2021 due to the impact of inflation—while nominal sales have gone up 9.4% since March 2021, real sales are down by 0.1%.

Third, retail sales faces headwinds from a slowing economy. Deloitte economists, in their baseline scenario (55% probability), forecast GDP growth in the United States to slow to 1.6% this year from 5.7% in 2021.10 Worse, in the event of a recession (30% probability) in 2022–2023, growth next year may dip to as low as 0.2%. Such a scenario will likely weigh on overall consumer and business demand, thereby putting pressure on retail sales. Also, high home prices and rising interest rates will likely dent demand for housing, thereby impacting sales at certain store types such as building materials and supply dealers, and furniture and home furnishing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}