2021 insurance outlook Accelerating recovery from the pandemic while pivoting to thrive

19 minute read

03 December 2020

In our 2021 insurance outlook, 200 industry leaders weighed in on their companies’ COVID-19 recovery efforts. How can the emerging lessons serve as a catalyst for business transformation?

As new regulatory trends make an impact in the financial services marketplace, how can your organization remain resilient? Our 2021 regulatory outlooks explore key issues that could have a significant impact on the market and your business in 2021.

Subscribe now to receive your digital copy of the reports as soon as they are live.

Key messages

View sections

Where do insurers stand as they enter 2021?

What a difference a year makes. Or even a few months. The COVID-19 pandemic and resulting economic fallout radically shifted consumer and employee needs, habits, and expectations, while compelling virtualization of insurer operations practically overnight. But while most of those in the industry adapted quickly, insurers are still likely facing lingering obstacles to growth and profitability in the year ahead.

Learn more

2021 Financial services industry outlooks

Read the 2021 insurance regulatory outlook

Explore all of the 2021 regulatory outlooks

Visit the Within reach? Women in the financial services industry collection

Explore the Financial services collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

A global outlook survey by Deloitte’s Center for Financial Services found that many insurers know they still have their work cut out for them, even after spending most of 2020 adapting to the outbreak’s impact. Forty-eight percent of 200 responding insurance executives agreed the pandemic “showed how unprepared our business was to weather this economic storm,” while only 25% strongly agreed their carrier had “a clear vision and action plan to maintain operational and financial resilience” during the crisis. (See “Methodology” for details about who was surveyed.)

Pandemic losses hurt the property-casualty bottom line

The pandemic and other catastrophe losses hit many insurers hard in first-half 2020, especially those writing events cancellation and workers’ compensation. To illustrate, North American property-casualty insurers saw first-half annualized GAAP operating return-on-average equity fall to 2.8% from 8.3% the year before, in large part due to US$6.8 billion in incurred losses related to COVID-19 and concurrent drops in premium volume for key lines.1 Overall, the year-to-date total return of S&P’s Insurance Industry Index lagged the broader S&P 500 by 24.6% as of September 30, 2020.2

Given the pandemic’s impact on employment, business activity, and trade, global nonlife premiums are expected to be flat for full-year 2020, including a 1% decline in advanced markets.3 However, despite these challenges, the industry may yet rebound to 3% growth in 2021, led by a potential 7% boost in emerging regions (figure 1).4

The pandemic and its aftermath are expected to continue hitting some property-casualty lines harder than others. Workers’ compensation insurance sales, for example, were undermined by massive job losses,5 and Deloitte’s US premium projection suggests volume may not return to prepandemic levels until after the fourth quarter of 2022.6 In addition, small business premiums, battered by shutdowns and bankruptcies, may also be slow to recover if many more retailers, restaurants, and personal services outlets close down.

On the other hand, while many US auto insurers saw a significant loss in premiums after providing policyholders with rebates and rate cuts to reflect less driving during the pandemic, carriers may see improved profitability with an expected drop in accident frequency.7

Life and annuity sales undercut by pandemic, interest rate drop

Life insurance premiums may decline 6% globally through the end of 2020 and by 8% in advanced economies, while a recovery of 3% growth is projected overall for 2021. Emerging markets once again will likely lead the way while advanced markets continue to struggle (figure 2).8

Meanwhile, annuity sales also took a big hit. In the United States, for example, nearly all types of annuities plunged by double-digits in the second quarter (see figure 3), except for registered index-linked products—which are a cross between fixed and variable annuities with limited downside investment risk.9

Growth and profitability in both annuities and many nonterm life insurance products will likely be impacted through 2021 and beyond by persistently low interest rates. The German 10-year yield, for one, is expected to remain negative,10 while the US Federal Reserve has indicated it will likely leave rates near zero at least through 2023.11 This could pose challenges, particularly for insurers with increased exposure to lower-rated, less-liquid investment-grade securities.12 The same goes for annuities, as lower interest rates historically prompt a reduction in benefits offered, which could make them a harder sell this coming year.13

At the same time, life insurers may see 50% more losses on mortgage loans than what they experienced during the Great Recession.14

While it was hoped the pandemic might at least raise consumer awareness about the value of mortality products, a J.D. Power study found that not necessarily to be the case. Despite COVID-19 fatalities exceeding 200,000 in the United States at the time of the study, consumers surveyed did not seem any more motivated to buy life insurance, due to a “combination of infrequent client communications and a pervasive perception of high cost and transaction complexity.”15 This indicates the industry likely has more fundamental issues to address to expand consumer awareness and market penetration.

Looking ahead to 2021 and beyond

Businesses must concurrently manage three key phases of the COVID-19 crisis—respond, recover, and thrive.16 When the pandemic emerged, insurers responded by taking immediate steps to ensure business continuity, and help customers and their communities cope.17 As they head into 2021, insurers should consider a mix of offensive and defensive actions to accelerate longer-term recovery efforts and pivot to the thrive phase when growth is reemphasized, despite challenging economic conditions.

Deloitte’s third-quarter US forecast includes a 55% probability that under the most likely scenario, with the population being vaccinated throughout 2021, there may still be “significant drags on economic growth.”18 Worse, there is a 25% probability of facing a “no end in sight” scenario where a vaccine is delayed, resulting in protracted weakness in the economy.19 Considering these and other challenges facing insurers around the world, this year’s outlook uses Deloitte’s global survey to explore both the tactics industry leaders are following to ensure their foundation remains strong for however long the pandemic lasts, as well as the strategies they’re beginning to deploy to position themselves for success in the coming years. We examine how insurers are adapting and planning to invest from the perspective of operations, technology, talent, and finance.

Expense management still front and center to free up funds for accelerated digitization

In operations across insurance organizations, expense management efforts—which began well before the pandemic hit—remain crucial, not only to offset added costs incurred to respond to the outbreak, but also to fund faster innovation, spur quicker recovery, and fuel future growth.20 Sixty-one percent of survey respondents expect to cut costs between 11% and 20% over the next 12-to-18 months. Those from the Asia-Pacific region (APAC), especially Australia and Japan, anticipate more stringent reductions, with 35% expecting cuts over 20%, compared to 19% in Europe and 11% in North America (figure 4).

However, most insurers are not looking to cut across the board. They are more likely resetting priorities, reducing nonessential expenses, and postponing less critical investments to free up capital for areas needed to recover and thrive, with spending priorities differing by region (figure 5) and type of technology (next section).

Product development may shake up status quo

New types of coverage may be spurred in part by the pandemic, such as the launch of more parametric policies (which pay upon the occurrence of a triggering event rather than having to claim a specific insured property loss). This was cited as the top product development priority among North American and European respondents and number three in APAC. The concept, which has already been rising in prominence in property-catastrophe coverage, might have applications for future viral outbreaks. Lloyd’s of London recently introduced a parametric business interruption policy for small- and medium-sized firms suffering IT disruptions.21

Insurers also may have opportunities to innovate more in personal lines with the pandemic-induced change in driving habits and work environments. Many of those responding to a Deloitte global auto and homeowners’ insurance consumer survey taken during the early part of the pandemic indicated a preference for greater customization. Younger buyers in particular showed interest in wider-ranging policies, including one covering all types of transportation rather than being tied to one vehicle.22

Distribution balances hybrid systems

Forty percent of those surveyed expect to increase investment in direct online sales, which is not surprising since most customers likely didn’t want to meet face-to-face with insurance salespeople during the pandemic—a trend that may continue long term.

Still, most insurers indicated they are hedging their bets by supporting agents and brokers in a variety of ways—from prospecting to sales management. Many European respondents went so far as to cite direct financial aid for struggling distributors as their top priority, although that option finished eighth in North America. Such help will likely be welcome, as nearly half of those surveyed by the Independent Insurance Agents & Brokers of America reported a loss of commercial lines clients and decreased revenue for 2020, while 70% received a Payroll Protection Program loan or some other grant or financial assistance during the pandemic.23

Bolstering cybersecurity for a largely remote sales force during the pandemic was the number one distribution consideration of respondents in North America—coming in second for APAC and third for Europe.

Underwriting looks to augment roles

Many insurers are in the early stages of underwriting transformation projects going well beyond automating routine, labor-intensive data gathering and processing tasks. The ultimate goal is to better leverage artificial intelligence (AI), alternative data sources, and more advanced predictive models to augment an underwriter’s capabilities and eventually transition them to higher-level, multifaceted roles—such as portfolio management and greater interaction with brokers and large customers.24

For example, Ping An Life Insurance Company of China has an advanced risk model on its smart underwriting platform that served over 18 million policyholders in 2019 and approved 96% of policies through automated underwriting, cutting average turnaround time from 3.8 days of manual underwriting to 10 minutes.25

The question is whether most insurers will invest enough to make this vision a reality, at least in the short term. Increasing automation was the top underwriting priority among respondents in North America, but only ranked fourth among those surveyed in Europe and fifth in APAC. Expanding the use of AI in underwriting ranked eighth in North America versus second in APAC and Europe, while enhancing predictive modeling ranked fifth or lower across all regions surveyed.

Claims goes virtual, but can it be a differentiator?

Trends prompted by the pandemic have likely required insurers to contend with much more remote claims handling, formerly executed on the ground.26 Thus, it was surprising that “increasing virtual claims interactions” finished as a fourth claims priority across all regions surveyed. Similarly, “upgrading detection capabilities for claims fraud” finished sixth, even though fraud frequency often increases during economic distress.27 These results may reflect the need to make hard budgetary choices across multiple priorities.

For claims to become a more reliable retention driver and even a competitive differentiator, carriers will likely need to not only adopt new technologies and alternative data sources, but “establish a connected partner ecosystem and talent model that values technical claims handling and data science skills.”28 For example, Zurich UK has teamed up with Carpe Data to automate and accelerate its claims processes and detect fraud using alternative data.29

In the long term, such a course would likely help “reduce pressures of an aging workforce as no-touch insurance claims processing increases.”30

Compliance challenges emerging

Regulators have focused on multiple areas of concern during the pandemic, from policy disputes over infectious disease-related coverage,31 to consumer protection as more sales and claims handling go virtual.32 But there are many other compliance issues for insurers to address that have nothing to do with the pandemic. (See figure 6, and look for Deloitte’s 2021 Insurance Regulatory Outlook for a comprehensive analysis.)

Technology could play a crucial role, but most feel digital capabilities come up short

Technology was vital in helping insurers shift to remote work environments and in ensuring employees had the tools to conduct business while remaining connected with distributors and clients.

Even so, Deloitte’s survey found 79% of respondents believe the pandemic uncovered shortcomings in their company’s digital capabilities and transformation plans. That rose to 87% among respondents with operations responsibilities, who were probably the most directly impacted.

In response, 95% of those surveyed are already accelerating or looking to speed up digital transformation to maintain resilience. Europe (59%) and North America (55%) seem further along in implementing such plans, compared to 41% in APAC (figure 7).

Insurers plan to double down on cybersecurity

As insurers begin to focus more on the thrive phase, most CIOs surveyed will be reallocating technology spending as they reprioritize ongoing and planned projects (figure 8). Cybersecurity tops the list among those surveyed in terms of an expected increase in investment.

Close to two-thirds of respondents across all regions are looking to increase spending on cybersecurity. With most employees working remotely and more data and applications moving outside the traditional security perimeter, cyberattack risks keep rising. Insurers should consider implementing “zero trust” principles by imposing verification requirements on anyone seeking access to data or systems, regardless of being internal or external, while adopting “security by design” principles during technology development.

Cybersecurity teams should consider enhanced controls and endpoint protection technologies to exert greater control over end-user devices. Companies should also increase training and awareness activities, focusing on remote guidelines and etiquette for work-from-home environments.

Cloud migration gaining momentum

Although the shift to cloud computing was already well underway before the pandemic, it appears to be an even bigger priority now as insurers look to shed fixed expenses. Cloud’s consumption-based cost model can facilitate expense management while enabling leveraging of cloud services to drive innovation and agility. Cloud transformation projects are likely to accelerate in 2021, as building the cloud foundation would allow insurers to rapidly and cost-effectively implement advanced analytics and automation tools (figure 9).

To prioritize cloud investment, carriers should look to first migrate and modernize systems-of-engagement, enabling different ways to interact with customers and distributors. Next, insurers should consider moving systems-of-record, readying core systems for digital technologies powering new business models. In September 2020, for example, Prudential decided to utilize Vitech's cloud-based V3locity as its core administration platform across its group insurance business.33

Companies should keep in mind cloud adoption goes beyond IT upgrades. For benefits to materialize, it should be part of broader business transformation, including people and processes as integral components.

Privacy and data security (addressed below) should also be top-of-mind, as insurers are still accountable for protecting customer data through encryption and by applying appropriate security and access controls to cloud applications.

Data privacy a rising priority as sources, analytics keep expanding

With data-related regulations and cybersecurity concerns increasing, privacy is a growing board-level priority for insurers. Fifty-two percent of those surveyed (including nine of 10 CEO/president respondents) expect to boost spending on data privacy.

However, 27% expect no change, while 22% may cut spending on privacy, which could prove problematic given emerging vulnerabilities. Insurers may also have to increase spending if they expect to move beyond their traditional focus on regulatory compliance and engage more proactively and transparently with consumers by offering value for new types of data, thereby making privacy management a competitive differentiator.34

Cybersecurity and privacy are prominent concerns not only because of increasing regulatory pressure, but also due to how rapidly data volume is growing through sensors, third-party aggregators, and other alternative sources. Combined with advanced analytics, insurers can reconcile, combine, and analyze data from multiple sources to generate real-time insights that were previously not feasible technologically or viable economically. No surprise, then, that 49% of respondents (led by 56% in North America) are looking to boost investments in data analytics.

The goal is to speed up underwriting and improve customer experience. For example, Policygenius, a New York-based InsurTech, utilizes analytics on past medical and prescription data to offer accelerated term life products without a medical exam for eligible applicants.35

Building a data-driven organization requires a strong foundation that is secure and scalable, allows linkages to multiple internal and external data sets (possibly as microservices), and supports advanced analytics and automation capabilities. Insurers should keep modernizing outdated legacy systems that could prevent carriers from extracting value and making new data actionable.36

Insurers reevaluate talent strategies by balancing return-to-office plans with a hybrid workforce

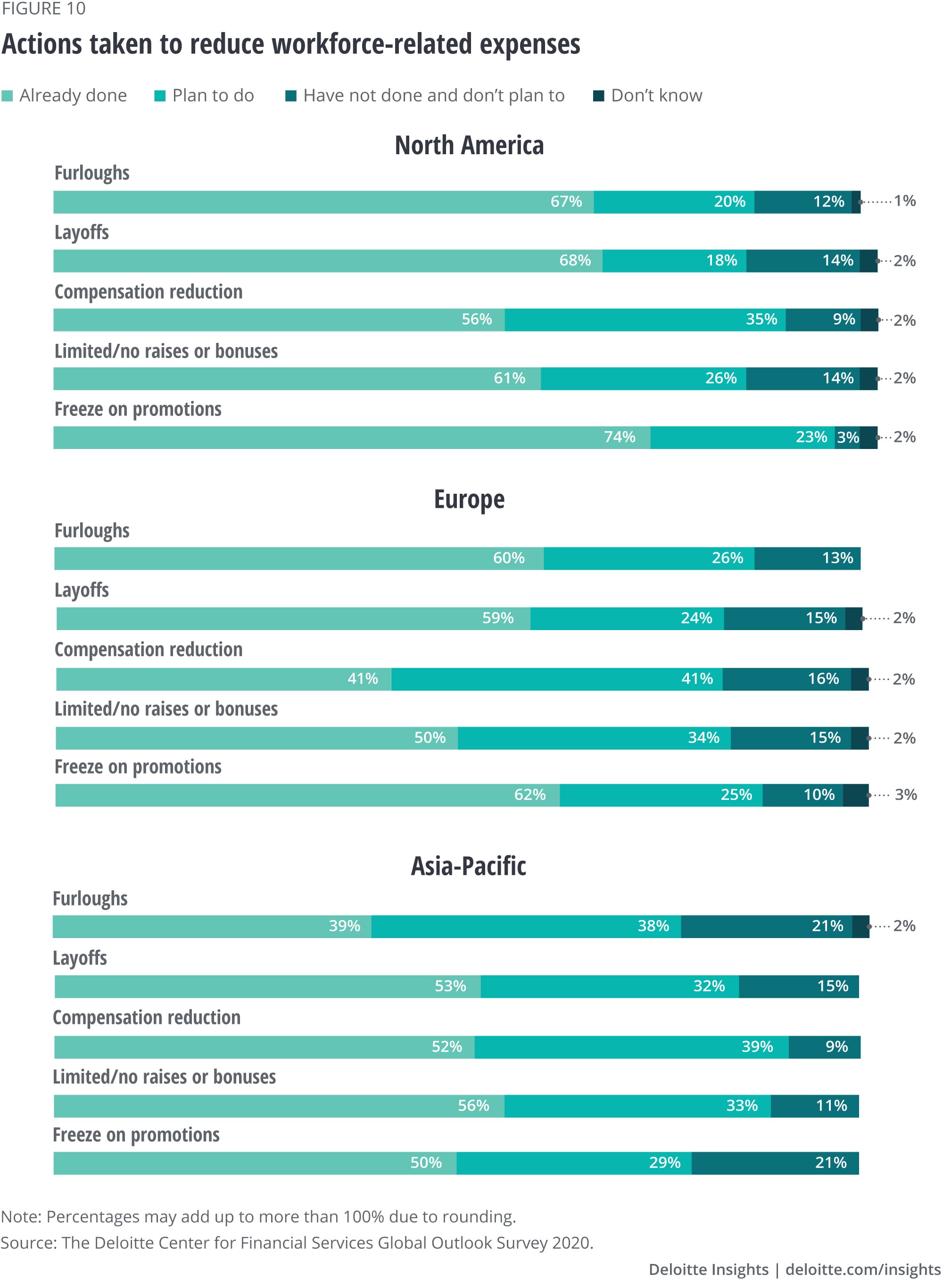

The insurance workforce was not immune to COVID-19’s effects. About 60% of those surveyed reported their companies had seen furloughs and layoffs. Over 50% experienced compensation reductions, limitations on raises and bonuses, and promotion freezes.

While the impact was felt across regions, respondents from North America reported being harder hit by various reductions (figure 10). Looking ahead, to support operational and financial stability, 39% of respondents believe they will need further rationalization of compensation and headcount.

Mandatory work-from-home models compelled unprecedented changes in day-to-day operations

Office closures and restricted movement prompted everyone and everything that could go virtual to do so immediately. However, the sudden pivot left insurers to grapple with challenges from multiple talent perspectives.

- Workplace: Many insurers with a traditional office mindset had to overcome a plethora of technology and collaborative obstacles to support a virtual operation of this magnitude while maintaining their productivity and culture.

- Workforce: Employees working remotely may lack an appropriate ergonomic space. Many must contend with additional personal responsibilities, such as child or elder care, requiring flexible or reduced schedules. These circumstances compelled many employees, especially women, to take voluntary career breaks.37 Indeed, the start of the new academic year for students learning at home prompted four times as many women as men in the United States to quit their job in September 2020.38

- Work expectations: There are often no clear policies laid out about what’s expected of virtual workers. Plus, the uptick in online insurance applications and claims management is fast-tracking digitization, impacting the nature of work and likely requiring retraining.

Most insurers are looking to eventually get the bulk of their people back to the office. However, with the risk of periodic surges in COVID-19 infections and uncertainty around large-scale vaccine availability,39 many workers may be concerned about potential health and safety risks. Indeed, 74% of respondents feel their organization’s success post-COVID-19 may be hampered by employee fear of returning to the office. Compounding this, those who have acclimated to remote work may question the need to return to an office, regardless of COVID-19’s status.

Respondents report taking several measures to ensure employee safety for those asked to return (figure 11). Insurers have opportunities to further reduce liability and enhance safety by utilizing adaptive technology. For example, insurers could require employees to download a mobile app regulating access to office facilities, while tracking intra-office activity and interaction if contact tracing is required.40

However, as most insurers are likely to at least offer remote work options until mid-2021 or beyond, they should therefore rethink “return to normal” talent strategies to enable productivity, collaboration, and innovation no matter where people work.

Conventional work strategies reimagined for near- and long-term

Insurers should consider moving beyond traditional structures and build a road map to thrive virtually. Some may decide to shut selected offices for good—an option chosen by Nationwide, which had already made long-term technology investments that facilitated a quick transition during the pandemic to a work-from-home model for 98% of employees.41 Others may consider a hybrid remote/office system, or at least a more flexible template.

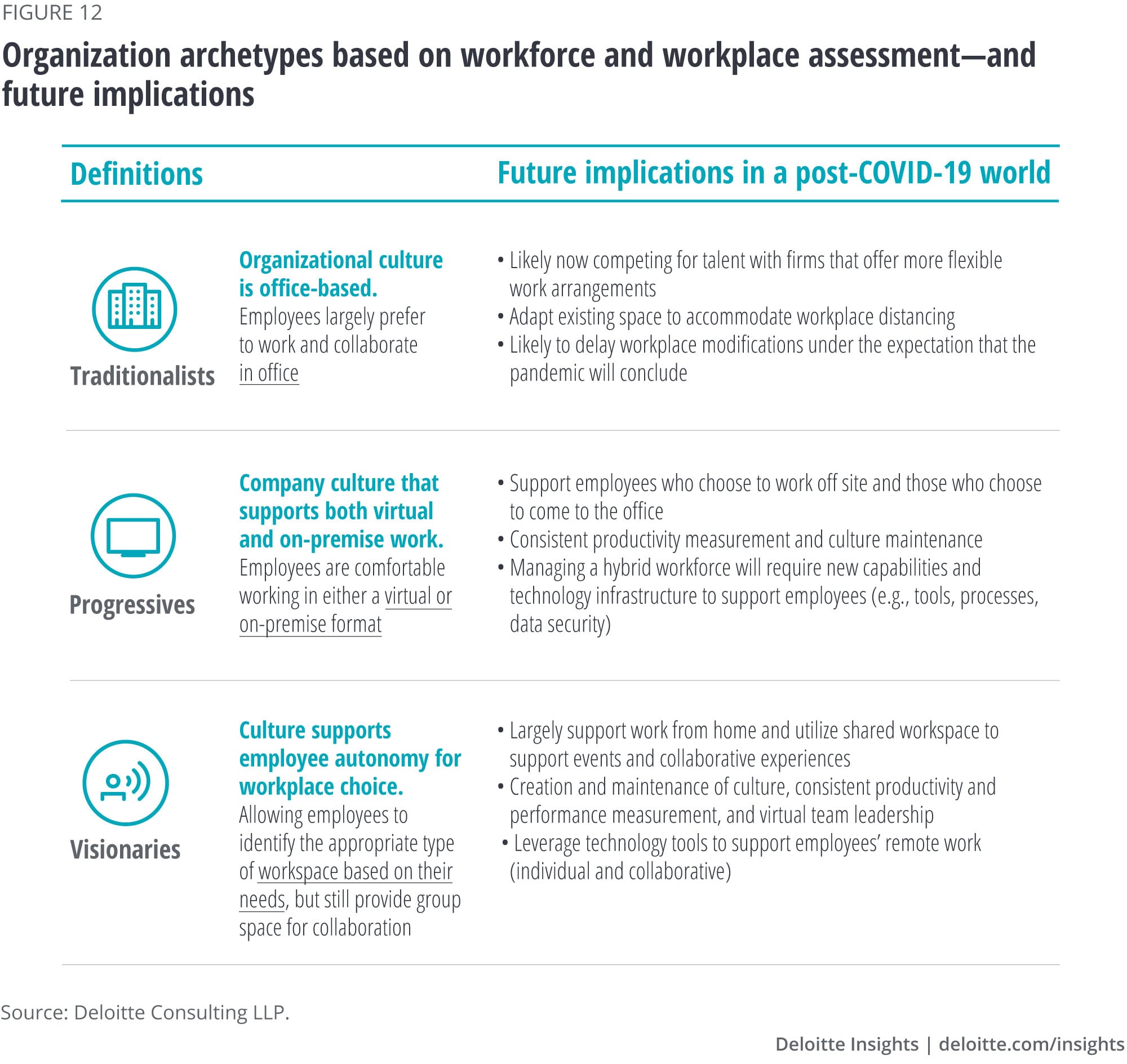

As insurers look to maintain their work culture for the postpandemic world, insurance leaders might consider three potential archetypes (figure 12): traditionalists (all employees eventually returning to the office); progressives (a hybrid on-premise/virtual model); and visionaries (most working virtually).

The vision for each postpandemic organization will be set at the top, so insurance executives will likely face hard decisions about which archetype best suits their company. Team managers will likely need to become microleaders, instituting organizational and cultural shifts at the small group level. Seeking a balanced approach, carriers that gravitate toward the progressive model need to decide what parts of the operation stay virtual versus on-premise.

Modifications to traditional talent models will potentially require revisions to hiring, onboarding, and performance management protocols. Formal expectations for remote workers should be established, taking into consideration employees’ personal situations while offering resources to enhance productivity, including well-being programs or flexible work options.

In-person training is hard to replicate for remote workers. Insurers with a fully remote or hybrid environment should therefore map out more robust, engaging virtual learning and development programs to complement or even replace in-person training. This could include training in pods and virtual cross-mentoring between seasoned and novice professionals (figure 13).

Diversity and inclusion efforts still need to be a priority

Beyond pandemic-related talent concerns, addressing employment inequality is emerging as a top priority for insurers. Nearly 67% of respondents report their company is focused on increasing the level of diversity in hiring, development, and leadership. Europe leads the charge for change (75%), followed by APAC (65%) and North America (61%).

Insurers should also not take their eyes off long-standing, longer-term talent objectives, such as attracting more millennials and Generation Z workers to backfill positions left open by what is likely to be a growing number of retirees in an aging workforce. They should also bolster the recruitment of those with advanced data analytics and automation skills to fuel faster, more effective digital transformation.

Finance priorities reconsidered for reporting, M&A, and taxation

Finance leaders continue to reevaluate processes and investments to optimize agility, assets, and growth heading into 2021. However, while only 25% of survey respondents strongly agreed their company had a clear vision and action plan to maintain financial resilience during the ongoing health and economic crisis, most indicated they were at least somewhat confident they are on the right track.

Meanwhile, Deloitte’s outlook survey also found 79% agreeing their insurer has been challenged to plan for and invest in targeted areas where they can have a competitive advantage post-COVID-19.

Interest in investment priorities to support financial stability is spread across a wide range of options and varies regionally. In North America, rationalizing compensation and headcount was cited as the top strategy followed by streamlining business functions, while in Europe and APAC, the largest focus of respondents will be on implementation of technology to enhance efficiency (figure 14). In Europe, these tech investments appear to be focused more on shorter-term strategies, as 42% of respondents will cancel or postpone long-term projects at least through 2021.

Insurers adapt quickly to meet reporting requirements

Meeting financial reporting deadlines in a virtual environment is one key concern. A Deloitte survey last spring on how insurer finance departments responded to the pandemic found most transitioning fairly well to a virtual actuarial and financial close process. While all insurers surveyed considered making improvements in close automation and 57% will upgrade core collaboration capabilities and communication for virtual exchanges, few reported significant delays in their typical closing time frame.42

Looking ahead, US financial reporting will likely become more complicated in the next couple of years. For one, the New York Department of Financial Services will be asking insurers to develop a financial disclosure approach specific to climate risk.43 In addition, life and annuity insurers will continue preparing to meet updated Financial Accounting Standards Board reporting rules for long-duration contracts, which will fundamentally change how insurers measure, recognize, and disclose insurance liabilities and deferred acquisition costs.44

M&A outlook may be more bullish than expected

The first-half global 2020 merger and acquisition (M&A) activity was consistent with the first-half 2019 activity.45 This was likely because most deals closing in this period were already in flight prior to the full-scale COVID-19 outbreak.46 In addition, while the level of uncertainty from medical, political, economic, and global trade challenges was expected to be the enemy of M&A, 25 insurance company deals were announced in the United States alone toward the latter part of Q3 2020, indicating the opposite trend may be occurring.47

Looking ahead, 31% of respondents said it was somewhat likely their insurer would increase M&A activity, although only 4% said that was very likely. Another 37% said increasing activity was somewhat unlikely, along with 4% seeing that as very unlikely.

New deals will reflect insurers’ altered priorities and strategies and vary across regions (figure 15). Exiting regions outside home countries ranked among the top three goals for those considering M&A deals. One example is AXA SA considering a sale of its Greek businesses to Generali SpA,48 as well its Singapore unit.49

A top focus appears to be adding new technology capabilities, at least in North America. Therefore, acquiring more mature InsurTechs could be increasingly attractive for legacy insurers, provided they can make a near-term impact on operations. For example, Prudential Financial announced the acquisition of Assurance IQ to reach a new demographic using the InsurTech’s business-to-customer platform.50 Some of this activity may include a broadening of the definition of buy side/sell side to embrace alliances and partnerships.

A mix of offensive and defensive M&A strategies will likely materialize as companies position to protect existing markets, accelerate the recover stage, and pivot to thrive (figure 16).

Meanwhile, tax planning in 2021 will likely require close monitoring of legislative and economic developments on multiple fronts, as well as investment in tax modeling and structuring to quantify and adapt to whatever changes materialize (figure 17).

Insurers should keep innovating to thrive after the pandemic

There are many additional challenges facing insurers in the year ahead. For one, while disputes over pandemic-related business interruption claims are resolved, policymakers and industry leaders will likely seek public-private solutions to provide affordable coverage for future outbreaks—no easy task.

Social issues are also expected to be front and center. Seventy-seven percent of respondents say their insurers are reprioritizing environmental, social, and governance issues, led by 88% in North America. And that’s beyond more immediate concerns about the impact of worsening climate change on insurer bottom lines, with 80% expecting to increase investment in initiatives promoting climate sustainability.

However, the biggest challenge overall may be coping with what we call “the unknown of unknowns.” While response and recover efforts have been generally robust in substituting digitization and virtual encounters for manual processing and face-to-face sales and service, what do these foundational changes mean for insurers, distributors, and policyholders in the short and long term?

It’s doubtful we’ll go back to what was considered “normal” whenever the outbreak is resolved, and world economies recover their footing. But more rapid digitization also likely means even greater dependence on connectivity. While such monumental operational changes may have been made out of necessity, it created a risk management challenge for the industry and its policyholders. It also poses a big opportunity for insurers to help mitigate and cover any resulting exposures with so many customers undergoing similar digital transformations. This may play out much like cyber risk did—a rapidly evolving exposure both threatening data-rich insurers and opening up a growing market for carriers to cover.

In the meantime, with a new type of economy to underwrite—more flexible, with increasing dependence on interconnections, real-time data, and advanced technology—insurers will likely be called upon to revise siloed thinking given blurring lines between personal and commercial auto, homeowners, and workers’ compensation. Similar challenges confront life insurers, with real-time data availability perhaps transitioning carriers into “insurers for life,” focused increasingly on maintaining wellness.

How insurers respond not just to the pandemic’s impact but to longer-term shifts in technology, the economy, and consumer preferences will be critical. Indeed, generating continuous innovation in insurance policies, sales strategies, operations, and customer experience could turn out to be the biggest differentiator in 2021 and beyond.

Survey Methodology

The Deloitte Center for Financial Services conducted a global survey among 200 senior insurance executives in finance, operations, talent, and technology. Survey respondents were asked to share opinions on how their organizations have adapted to the COVID-19 pandemic’s impact on their workforce, operations, technology, budget, and culture. We also asked about their plans for investment priorities and likely structural changes in the year ahead as they pivot from recovery back to growth.

Respondents were equally distributed among three regions—North America (the United States and Canada), Europe (the United Kingdom, France, Germany, and Switzerland), and Asia-Pacific (Australia, China, Hong Kong SAR, and Japan). The survey was conducted in July and August 2020.

The survey included insurers with at least US$1 billion in 2019 revenue. Sixteen percent had more than US$1 billion but less than US$5 billion in revenue, 24% had between US$5 billion and US$10 billion, 45% had between US$10 billion and US$25 billion, while 15% had more than US$25 billion.

Deloitte Insurance

Deloitte’s insurance group brings together specialists from actuarial, risk, operations, technology, tax and audit. These skill sets, combined with deep industry knowledge, allow us to provide a breadth of services to life, property and casualty, reinsurers and insurance broker clients.

Get in touch

- Gary Shaw

- Vice chairman and US Insurance leader

- Deloitte LLP

- gashaw@deloitte.com

- +1 973 602 6659

© 2021. See Terms of Use for more information.

More from the financial services collection

-

The path ahead Article4 years ago

The path ahead Article4 years ago -

US consumer payments in a post-COVID-19 world Article4 years ago

US consumer payments in a post-COVID-19 world Article4 years ago -

Preparing for the future of commercial real estate Article4 years ago

Preparing for the future of commercial real estate Article4 years ago -

COVID-19 return-to-the-workplace strategies Article4 years ago

COVID-19 return-to-the-workplace strategies Article4 years ago -

Confronting the crisis Article4 years ago

Confronting the crisis Article4 years ago