These forecasts are based on a regression model with a number of independent variables, including the federal funds rate, deposit mix, changes in the share of interest-bearing deposits, loans-to-asset ratio, and market valuation. Our forecast reiterates the importance of deposits for bank funding. Banks that have a higher share of deposits to liabilities, a lower share of time deposits, and generally more stable deposits, may face less pressure to keep deposit rates high, and thus, have lower deposit costs.

Going forward, the industry might be hard-pressed to bring down their deposit costs, and lower deposit betas, even as the Fed funds rate declines.

Customers are in the driver’s seat—and they will likely continue to expect higher rates

After nearly a decade of earning low to zero interest rates on their deposits, customers appear to be back in the driver’s seat. Many have become more sensitized and savvier, and armed with information, and as a result, they are demanding higher rates on their deposits. Many have already switched their cash into higher-yielding time deposits.13 The average share of interest-bearing deposits in the US banking industry increased to 72% in Q1 2023, from 69% a year ago.14

Additionally, many depositors moved their funds to higher-yielding money market funds offered by both banks and nonbanks, and T-bills. For instance, the flows into money market funds climbed to a record high in March 2023, increasing by US$416 billion from March 8 to May 3, 2023, to a total of US$5.3 trillion.15 This coincided with about US$512 billion in deposit withdrawals during the same period.16 The convenience of digital banking has made these money movements all the more easy.17

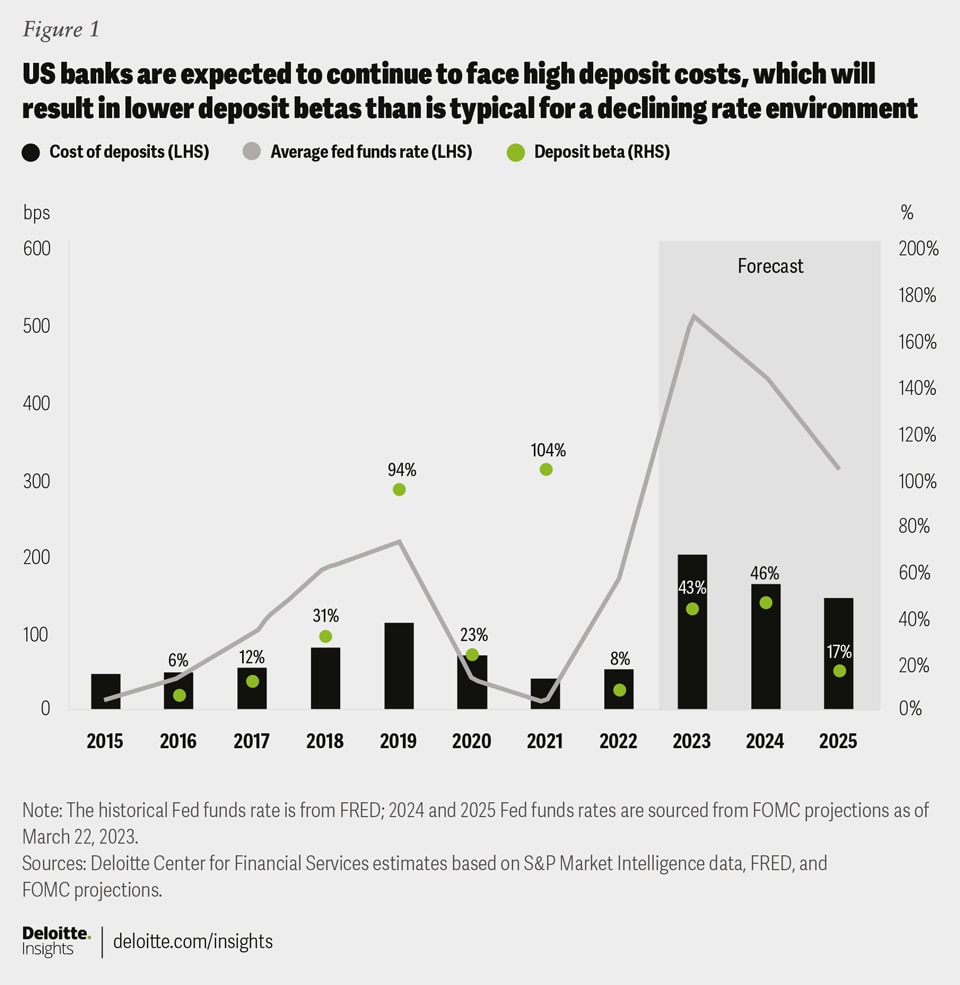

Competitive pressure should remain elevated

The competitive dynamics in the deposit market have taken a new dimension since March 2023 when a few regional banks came under stress. The limited pool of available cash could see increased competition from banks of all sizes, money market funds and T-bills, and also fintechs and nonbanks. Digital-only banks, for instance, will likely continue to offer higher Certificate of Deposits (CD) rates; they are also offering variations on typical features such as a CD with no early withdrawal penalty.18

Several banks have also hiked rates and extended new marketing campaigns.19 Financial institutions, such as Capital One, Citigroup, and Synchrony, for example, are marketing one-year CDs with rates in excess of 4%.20 Yet, responses vary across the industry. The average deposit beta for top US banks in the current hike cycle as of Q1 2023 stands at 41%, 600 bps lower than the last cycle’s peak deposit beta in 2015–19, despite current rate hikes already far beyond the last period’s peak. The cumulative deposit beta differed from 69% to 19%—a substantial range.21

The type and stickiness of deposits in banks’ portfolios can also play an important role. Many banks with a portfolio skewed toward retail deposits have enjoyed a softer cushion when compared to commercial deposits. In fact, among the top 30 banks, those with strong retail deposit portfolios had an average deposit beta of 34% compared to 45% for banks with strong commercial deposits.22

Banks should expect changes and new applications of supervisory tools and regulatory frameworks. These may include: Modification of the tailoring rules implemented in 2019 that reduced compliance requirements for smaller and less complex banks; recalibration of thresholds for capital and liquidity; and potential new CCAR scenarios, including more severe stress testing assumptions for liquidity. There could possibly be higher deposit insurance fund (DIF) fees, and reevaluation of assumptions about deposit stickiness by supervisors and banks alike, and how these factor into modeling. There could also be sharper scrutiny by examiners on safety and soundness.

Another new and notable item is how recent bank deposit runs were “fueled” by social media.23 Regulators have warned banks about the perils of social media–driven information flows. This has added a new dimension to how banks manage their exposure across multiple risk stripes, including liquidity, operational, and reputation.

These additional changes to current regulations and supervisory practices should increase the funding pressure on banks that are not already facing the severest regulatory constraints. (See Deloitte’s report, Prepare for more stringent regulation and agile supervision after bank failures.)24

Actions banks could take to help offset the impact of higher deposit costs

Higher deposit costs (and lower deposit betas) will have a detrimental effect on banks’ ability to generate strong net interest income, unless they are also able to raise lending rates, resulting in downward pressure on net interest margins in the medium term. This should be particularly challenging for banks that have less diversified business models and that are exposed to concentration risk. These new factors will likely force banks to reassess the true cost of deposits and how they may be deployed. Lower profits may also affect market valuations.

As a result, many banks may be forced to charge higher lending rates to borrowers. This may create a delicate balance between asset quality and loan volume in the future. Diversifying revenue streams and focusing more on fee income should be pursued with greater vigor.

Recent events have also reiterated the importance of scale and stability. Some banks may not have the incentives to remain small or below certain asset thresholds. As a result, more M&A activity within the banking industry is likely.

![[bold-start]Figure 1: US banks are expected to continue to face high deposit costs, which will result in lower deposit betas than is typical for a declining rate environment [bold-end]](/us/en/insights/industry/financial-services/financial-services-industry-predictions/2023/bank-deposit-costs/_jcr_content/root/responsivegrid_380572564/advanced_image.coreimg.png/1720605798476/us176545-figure1.png)

{kind=link}