Climbing the electric vehicle transformation mountain

A convergence of concerns appears to hang over the automotive industry, which is already struggling to reinvent itself on a compressed timeline.

If not for the economic fallout of the pandemic causing massive global inflation and reactionary spikes in interest rates over the past 12 months, the automotive industry may have had a much easier time convincing consumers to join them on a journey to electrification. As it stands, achieving the US federal government’s target of having electric vehicles (EVs) represent 50% of light vehicle sales by 20301 could be seen as ambitious when they represented just 7.2% of new vehicle demand in the second quarter of this year (up from 5.7% last year).2 The pace of change should accelerate dramatically over the next six years, but several challenges persist, including affordability, infrastructure, supply chain evolution, and the likelihood of production disruptions resulting from upcoming labor negotiations.

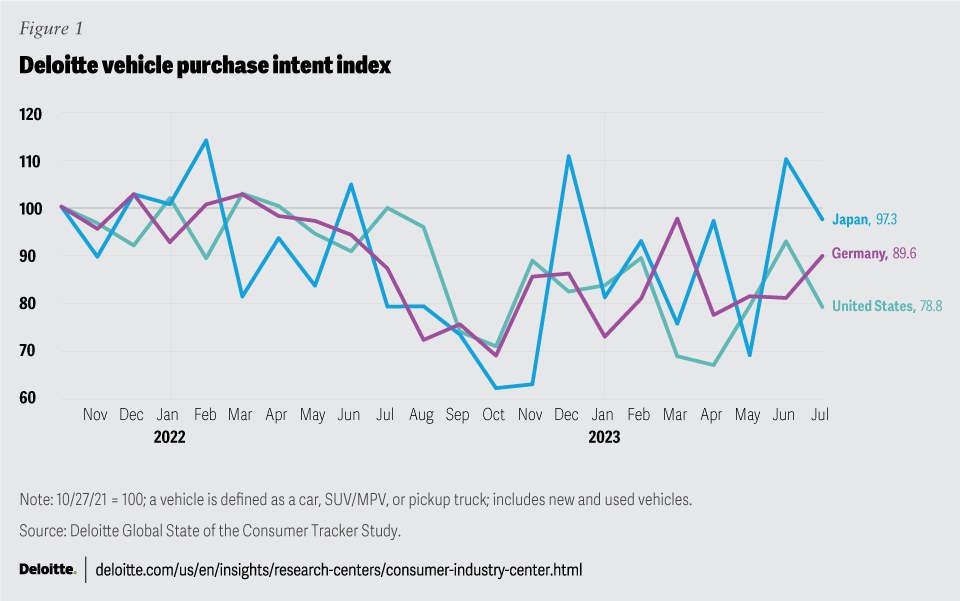

Light vehicle affordability is not a new concern. Transaction prices in the United States have been ratcheting up for over a decade. However, a market-wide shift to inherently more expensive light trucks, coupled with the rapid rise in borrowing costs and the introduction of electrification technology, has collided with a consumer concern for financial capacity in a protracted period of high inflation. The latest results from Deloitte Global State of the Consumer Tracker study suggest half of US consumers are concerned about the amount of money they have saved and nearly one-third are worried about their credit card debt. While less than a quarter of consumers are concerned about making upcoming payments, less than half of survey respondents (46%) report having money left over at the end of the month, and only four in 10 can afford a large, unexpected expense. As a result, the Deloitte vehicle purchase intent index has remained well below the baseline (set in October 2021) for the past year, suggesting underlying softness in core consumer sentiment, which is currently being masked by efforts to replenish dealer inventories (figure 1). It may also reflect the rising level of incentives required to keep people engaged in the vehicle market.3

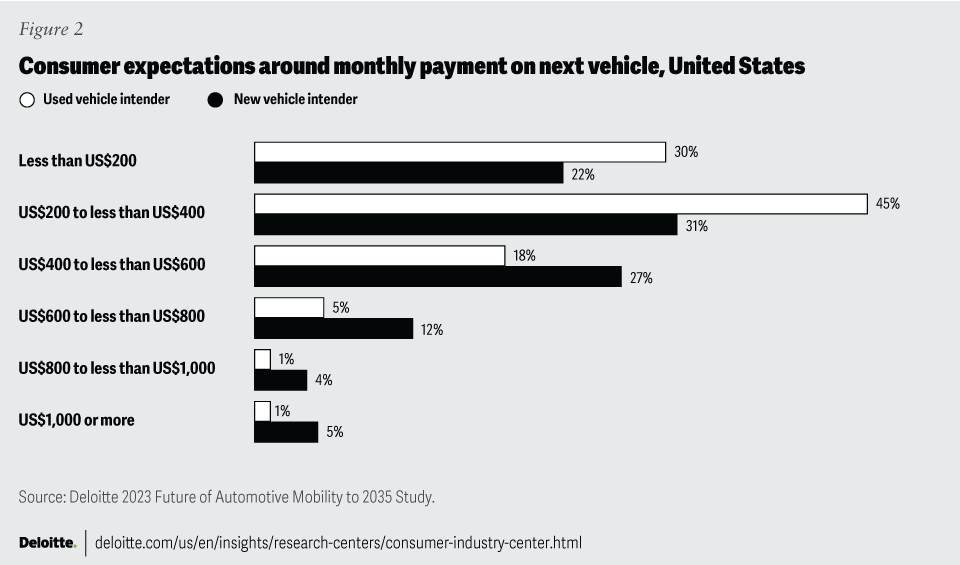

Although new vehicle transaction prices have moderated slightly since the start of the year, averaging US$48,334 in July,4 there is still a large gap between this market reality and what consumers expect to pay for their next vehicle. Results from the 2023 Deloitte Global Automotive Consumer Study suggest that more than two-thirds (68%) of consumers expect to pay less than US$50,000 the next time they are in the market for a new vehicle. Even more striking is the apparent disconnect between the average monthly payment for a new vehicle, which reached a record of US$733 in the second quarter of this year (up from US$678 in the same quarter a year prior),5 and that 80% of new vehicle intenders expect to pay less than US$600 per month (figure 2).6

It should be noted that healthy purchase incentives contained in the Inflation Reduction Act and a raft of price cuts implemented earlier this year have been supportive of EV sales growth. Some automakers are also promising more moderately priced electric models that will likely be introduced to the market over the next few years.7 However, many original equipment manufacturers (OEMs) are finding it difficult to offer EVs at an affordable yet profitable price. The key to improving the cost equation includes the rapid developments being made in battery chemistry using lower-cost materials, and the application of giga-presses designed to dramatically reduce complexity in the vehicle manufacturing process.8

Another hurdle to overcome is building an effective, affordable, and reliable national EV charging network. As recent Deloitte consumer survey data shows, 46% of consumers cite the lack of public charging infrastructure as their greatest concern regarding battery electric vehicles.9 Further, 40% of consumers cite the lack of a home charger as their biggest concern, and although the majority of people intending to acquire an EV expect to charge their vehicle at home, nearly a quarter will be relying on access to a public charger, as the cost of installing a private charger is prohibitive.10

At the moment, the United States has around 32,000 public DC fast chargers. However, to support the expected number of EVs in operation by 2030, the US Department of Energy’s National Renewable Energy Laboratory estimates that the number will have to grow to 182,000.11 Again, the federal government is making funds available for the build-out of this infrastructure, but more coordinated oversight may be required to help ensure optimal placement of chargers. It also appears that OEMs are finally acknowledging that a more standardized approach to charging technology is necessary to drive mass EV adoption.12

It is also important that these chargers are functional and reliable. Having said that, a recent study data suggests consumer satisfaction with publicly available chargers declined in Q2 of this year compared to the same period a year ago.13 The main drivers of dissatisfaction include charging speed, inoperable chargers, and long queues at charging locations. Access to federal infrastructure funds is also predicated on that fact that chargers need to be functional 97% of the time,14 but some questions remain regarding how this will likely be achieved and/or monitored, as reports suggest current performance remains well below that mark.15

From a supply chain perspective, the transition to EVs can be likened to the analogy of changing the engines on an airplane while in flight. For suppliers that have traditionally been dependent on vehicle assembly volume in a piece price environment, the production slowdowns experienced over the last two years, sparked by the semiconductor crisis, have been difficult to endure. Many suppliers were unable to renegotiate contracts with their OEM customers and were left to take on a significant amount of debt.16

At the same time, the need to innovate and keep pace with the OEMs’ transition to EVs has applied even more pressure on suppliers at a time when the cost of borrowing to fund capital investments has risen substantially. Vehicle production and sales are expected to rebound over the next two years, which should help suppliers as pandemic-induced pent-up demand is released into the market. However, the second half of the decade is predicted to look very different as demand stagnation sets in, limiting light vehicle sales to 16–16.5 million units per year (figure 3).17

Overall, as demand for light vehicles begins to recede, industry stakeholders may need to rethink their business models and service offerings to compensate for lower revenue and profitability contribution emanating from the sale of vehicles to end consumers. Several OEMs are attempting to lay the foundation for digital service offerings in conjunction with the introduction of new EVs in the marketplace. A big question is whether consumers will pay for added connectivity and digital services.18 Recent study results show that consumers are interested in services that optimize their journey, suggesting alternate routes to minimize travel time while improving road safety.19 However, wrestling consumers away from high-tech players that have embedded many of these features into value-added smartphone apps for over a decade may be a significant challenge for OEMs looking to monetize these services. Vehicle retailers also have a role to play in the mainstream adoption of EVs and should help ensure their personnel are proficient when it comes to the unique aspects of selling and maintaining EVs.

EV vehicle production may also face a near-term derailment because of the already contentious upcoming labor negotiations.20 On the one hand, the economics of producing vehicles may be impacted by substantial wage increases and other demands put forward by union leadership. On the other hand, OEMs may use the negotiations to affect major changes in their manufacturing footprint that align to longer-term EV transformation strategies. Either way, the outcome of this year’s collective bargaining efforts may have a significant impact on the transition to EVs in North America.

There is no doubt that the US automotive industry is on the path to an electric mobility future, but getting there will likely not be a leisurely walk in the park. Many obstacles threaten the path to electrification where each step is important, given the role the automotive sector is being asked to play in the global decarbonization effort. The need for a variety of stakeholders across the automotive ecosystem to converge with a common goal to help solve these issues will likely be essential to maintain momentum.

{kind=link}

{kind=link}

{kind=link}