{kind=link}

{kind=link}

{kind=link}

Food fight: Consumers confront inflation with frugality has been saved

The authors would like to thank Marcello Gasdia and David Levin for their contributions to the article.

Cover image by: Sofia Sergi

Netherlands

United States

United Kingdom

United States

United States

Global consumers are getting punched in the pocketbook by high inflation. Perhaps nowhere has inflation hit them harder than at the grocery store.

It’s largely unavoidable. Everyone needs to eat. Unlike a car, vacation, or even a new pair of socks, consumers can’t put off buying groceries until the financial squeeze loosens its grip. In many countries, high food inflation has dwarfed other spending categories.1 In the United States, for instance, year-over-year inflation rates for food eaten at home increased more than 10-fold over the last 18 months ending December 2022.2 Spiking prices have been especially tough on lower-income households, as they generally spend a greater portion of their funds on food and so are even more exposed.3,4

When inflation first hit, consumers seemingly tried their best to take higher prices in their stride. Many dipped into built-up pandemic savings to maintain their prepandemic spending levels.5 But now that some of that savings buffer is gone, weathering a prolonged storm could mean making different decisions at the grocery store.

The extent to which consumers are being frugal (and exactly how they’re going about it) has important strategic implications for retailers and consumer packaged goods (CPG) companies, including their pricing strategies, marketing, promotions, product mixes, and volume expectations.

But there may be broader implications too. Consecutive months of sticker shock and stress around everyday purchases like milk and eggs could spark a frugality ripple effect across other purchase categories. Globally, consumer discretionary spending intentions have been slipping over the past year.6 And in some countries like the United States, weakening retail sales have started to echo the sentiment.7

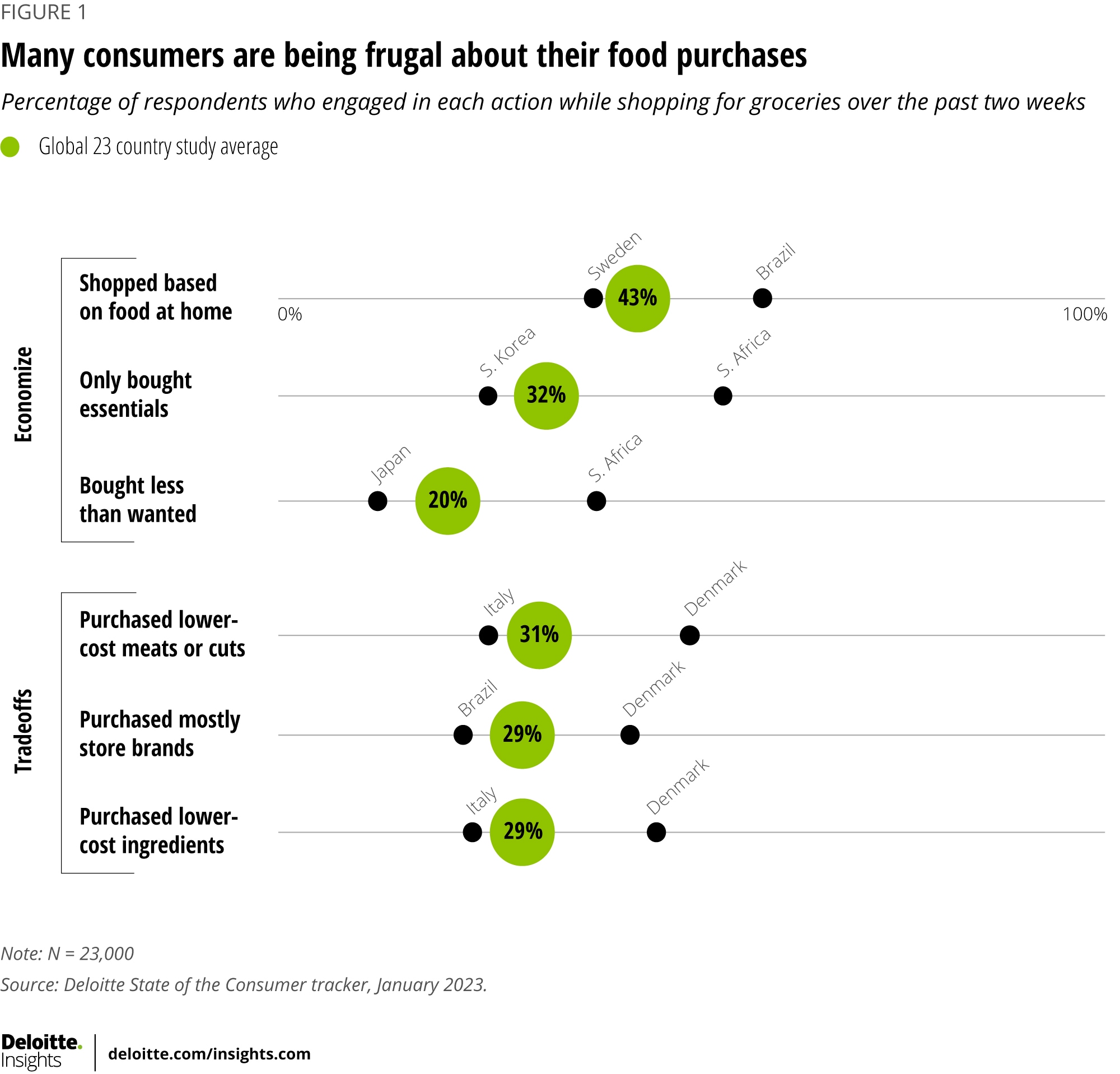

Across nearly a dozen grocery behaviors studied over a five-month period, six were found to have a strong connection to consumer frugality. Three represent how grocery shoppers make efforts to economize. Another three represent important trade-offs consumers make when under pressure.

The most frequently used strategy fell into the economize bucket. In January, four in 10 consumers surveyed as part of Deloitte’s ConsumerSignals cited making efforts to reduce their food waste by shopping based on food and ingredients already at home (figure 1). Rising prices are likely making consumers more diligent about what ends up in the trash. And that’s an important sentiment for consumer product companies and retailers to consider—largely because it can create a foundation for many other behaviors. For example, consumers being extra cautious about food waste may be more likely to buy frozen and shelf-stable foods; further, when they shop for fresh food, they are likely to do so within the strict confines of planned meals.

Reflecting on other behaviors in the economize bucket, one-third of global consumers surveyed cite only buying the essentials. Like those focused on food waste, one might assume these consumers would be less likely to take risks with new products or be influenced by promotions for items not on their shopping list. One in five cited leaving the grocery store over the past two weeks buying less than they wanted to. This behavior goes beyond mere food frugality and could hint at the presence of food insecurity. The figure sits relatively high across a number of developed economies, including France (24%), Italy (21%), Germany (20%), the United States (18%), and the United Kingdom (19%).

For some consumers, food frugality isn’t just about how much they buy, but what. The trade-offs bucket represents strategies consumers use to keep the cart full and grocery bills down.

Perhaps not surprisingly, trade-offs often center around expensive items like meat and seafood. Nearly a third of survey respondents (31%) cited switching to cheaper cuts of meat or different sources of protein. Closely related, a similar number (29%) say they are generally choosing cheaper ingredients, relying more on things like dried beans, rice, and lentils over more expensive alternatives. The resulting change in the sales mix for grocers affects profitability and could cause challenges for the supply chain’s ability to keep the right items in stock.

However, some trade-offs could open up new opportunities for retailers. Roughly three in 10 surveyed say they are dropping popular name brands for less expensive store brands (figure 1). Research suggests once consumers make the switch to private or store-labelled goods, they tend to stick with it and buy more, especially if they find quality and good taste, in addition to price advantages.8 Naturally, this could also present risks for national CPG brands.

Economic headlines have been offering a bit of sorely needed optimism in recent months. While still elevated, inflation rates have started easing in some major economies such as the United States and Germany.9 Other measures like job growth and unemployment remain fairly positive. Overall, however, many forecasts still call for slowed global growth.

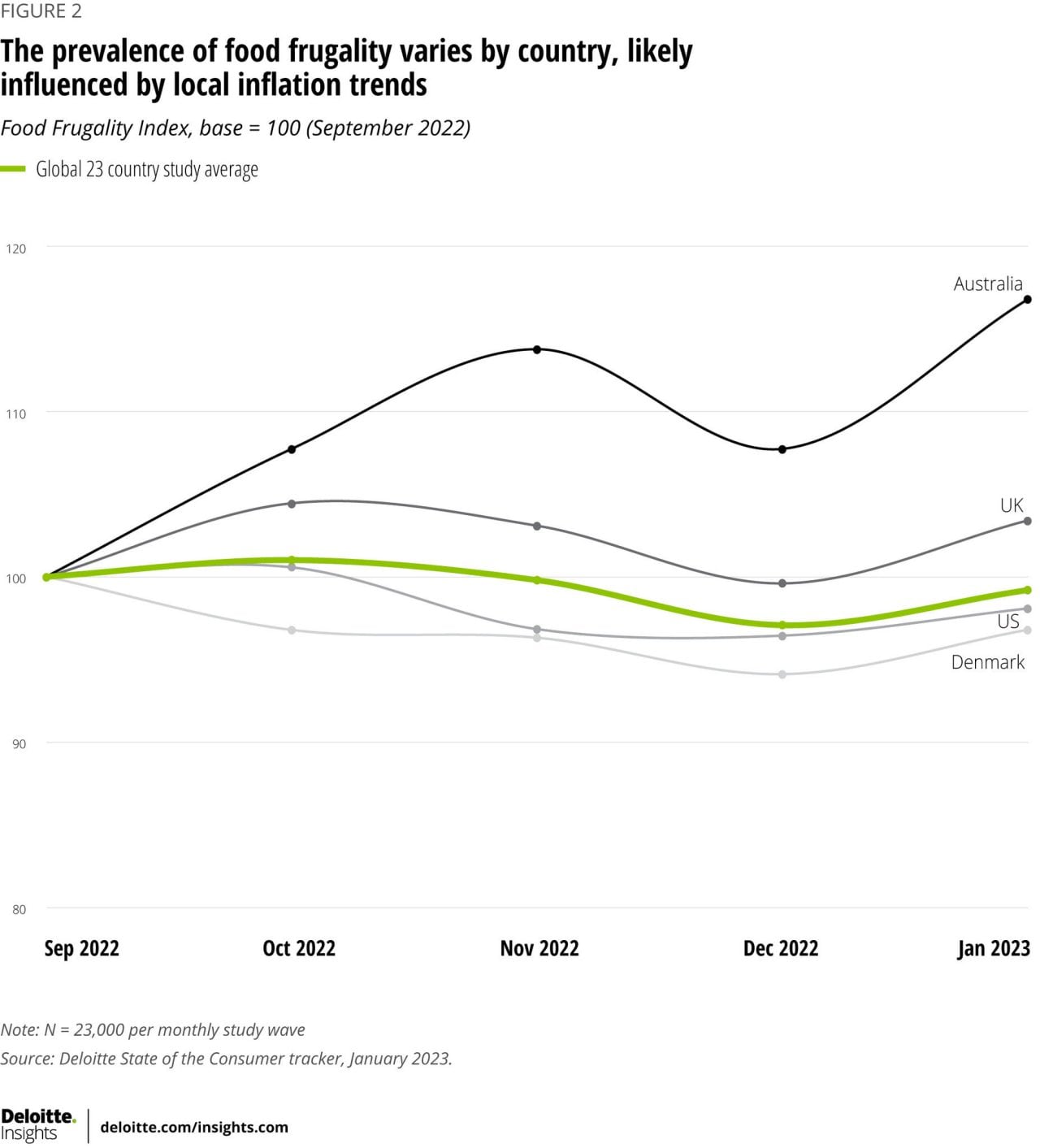

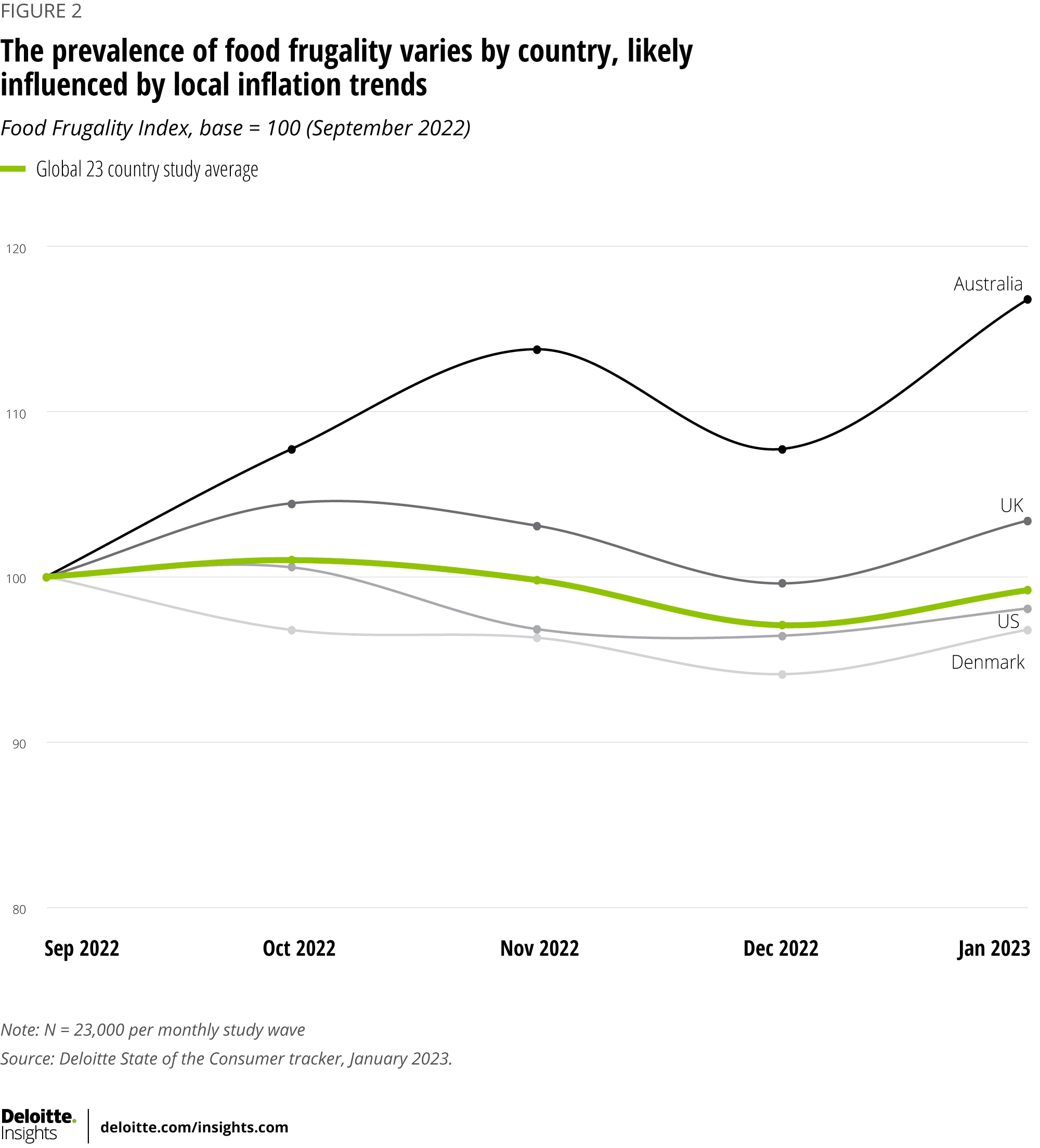

Frugality, however, has yet to show signs of any big swings since September 2022. Deloitte’s Food Frugality Index (FFI),10 a metric designed to capture longitudinal change across the six cost-saving behaviors featured in figure 1, has remained flat in recent months (figure 2). FFI index values fall when fewer consumers engage in frugal behaviors at the grocery store.

At a global level, consumers surveyed in January 2023 say they’re being about as frugal as they were five months ago. Although index values dipped as consumers loosened their purse strings during the end-of-year holiday season, they already seem to be back on the upswing.

FFI volatility, however, varies significantly by country. And it’s likely being driven by local economic conditions such as inflation trends. Australia provides a good example. There, inflation rates are still spiking. Similar to where countries such as the United States were during the summer of 2022, monthly inflation numbers in Australia are painting record-highs.11 Perhaps not by coincidence, FFI values for Australia suggest consumers are increasingly on the defensive.

In the United Kingdom, frugality has been relatively high, even as inflation rates eased in recent months. Food inflation (rather than overall inflation) might provide a clue as to why. While overall inflation has decreased since October in the United Kingdom, food inflation hasn’t followed suit—it rose by 16.8% in December 2022, marking the biggest annual jump in food prices in the country since 1977.12

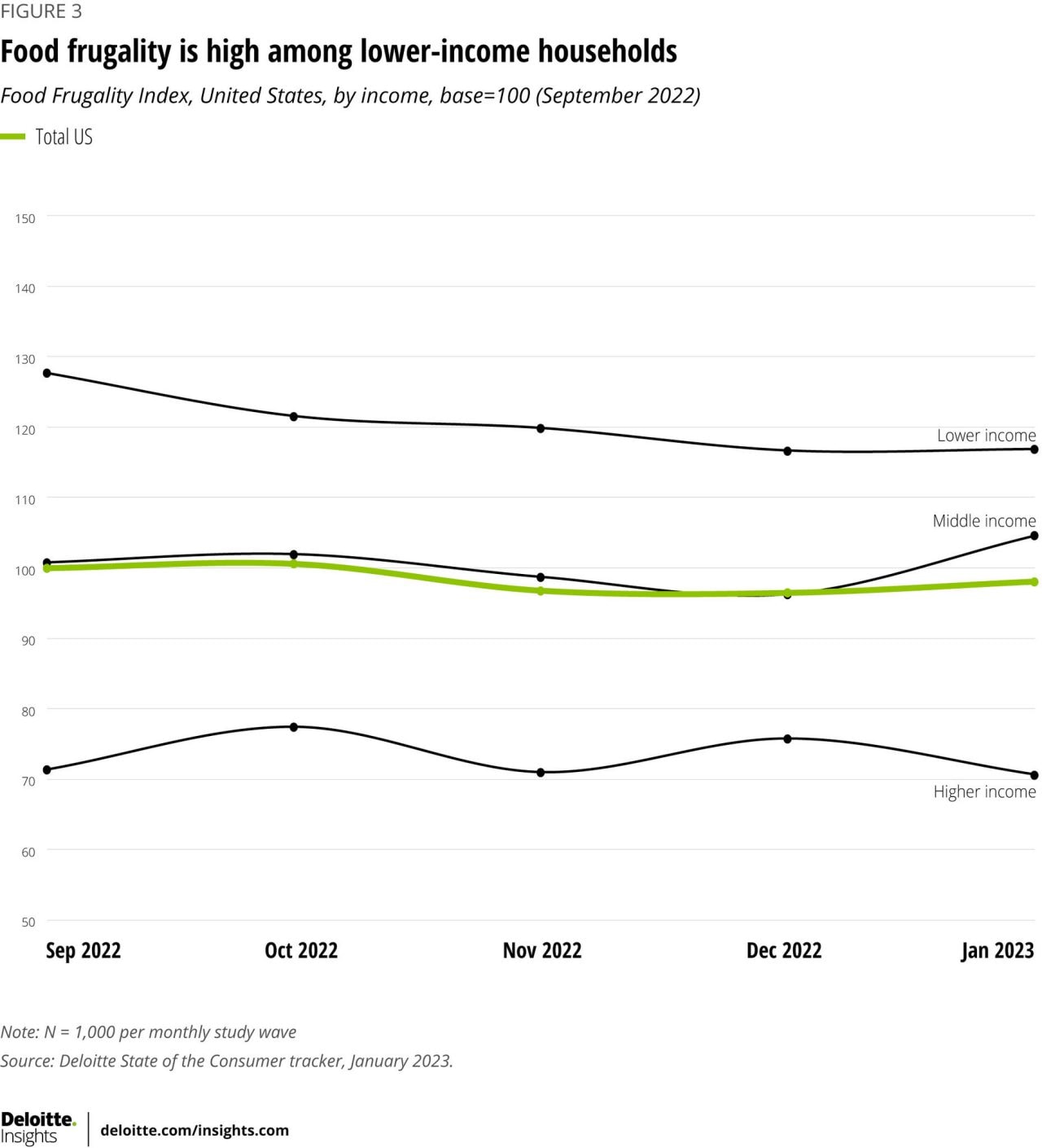

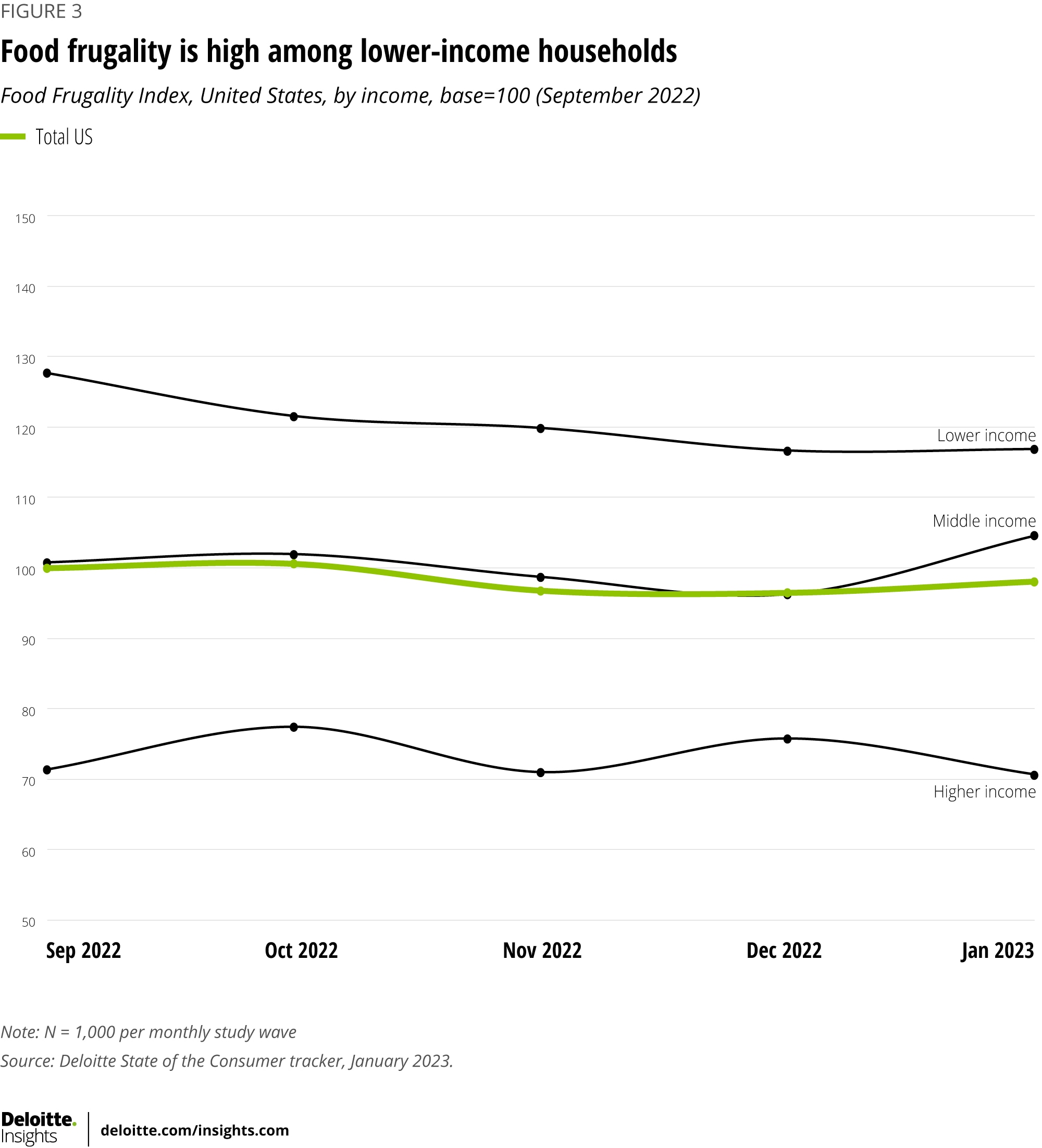

Frugality also varies by income. Perhaps not surprisingly, food frugality is exceptionally high among lower-income households (figure 3). As haves and have-nots continue to bifurcate the market, those with less money to spend are, not surprisingly, more frugal. In countries where frugal behavior has eased or spiked, lower-income consumers are typically behind the trend. That story is illustrated well in the United States. From September 2022 leading into the holiday season, easing frugality among lower-earning Americans helped drive down the overall US score.

But lower earners are by no means the only group showing signs of frugality. Middle-income consumers, for example, drove much of the January increase in the overall US index score (figure 3). And higher earners, while less likely to engage in all six cost-saving behaviors, do show unique patterns. For example, a relatively large portion of higher-income Americans surveyed cited choosing store brands over name brands.

Federal Reserve (Fed) Chairman Jay Powell put it bluntly this past August when he said that the actions of the Fed will “bring some pain to households” and that it was all part of the “unfortunate costs of reducing inflation.”13 Deloitte’s FFI was designed to help measure that pain for consumers worldwide around perhaps the most basic, frequent, and necessary purchases each household makes.

Food inflation largely started on the supply side. Some of those pressures are now easing and higher central bank interest rates are squeezing the money supply and doing their part. Prices, however, tend to go up faster than they come down. That is where collective frugality begins to play its part. When consumers signal they can no longer tolerate higher prices, retailers and consumer products companies could begin to lose their pricing power. It may be painful, but frugality is expected to precede, and with time, contribute to decreased retail food inflation.

Inflation and frugality will likely find an equilibrium. But it may take time. In many parts of the world, food inflation remains hot. And for the most part, consumers cite being just as frugal as they were five months ago.

Retailers and suppliers will have an interest in continuing to manage costs tightly. Operational considerations may include ongoing efforts to decrease waste and stock loss, reducing stock keeping units, scrutiny in the margin management process, and aggressively collecting trade funds (or better targeting them to just the most effective marketing channels).

Grocers should understand how these frugality behaviors are playing out in their own stores and pass on that data to their CPG suppliers. Understanding the extent of price push-back and where it’s happening could help in decision-making and pricing contract negotiations. When possible, brands should share their price advocacy efforts with customers. Let them know you are fighting along with them.

Perhaps most importantly, events like pandemics and historic inflation spikes only reinforce the importance of greater organizational agility. The modern retailer and manufacturer should be able to “pivot” to remix formulations and business models. Inflation should eventually pass. But it won’t be the last industry disruption.

Deloitte, ConsumerSignals, 2022.

View in ArticleDeloitte, ConsumerSignals.

View in ArticleJerome H. Powell, “Monetary policy and price stability,” speech at “Reassessing Constraints on the Economy and Policy,” an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, August 26, 2022.

View in ArticleThe authors would like to thank Marcello Gasdia and David Levin for their contributions to the article.

Cover image by: Sofia Sergi