As we look ahead to 2025 and beyond, it's clear that TMT is on the verge of a significant leap forward, largely powered by rapid generative AI adoption. But to get there, the industry will need to close gaps, including: balancing gen AI infrastructure investments with monetization, addressing gender disparities in gen AI usage, managing the energy consumption of gen AI data centers, tackling trust concerns surrounding deepfake content, discovering how best to use gen AI in media and gaming, and harnessing the power of gen AI agents to manage and act in real time. Further gaps exist in streaming video and cloud spending. Plus, there are non-gap predictions, around new smartphones and PCs with gen AI chips on them, new stadiums and other sports infrastructure leveling up the fan experience, and telco consolidation, specifically of wireless players. Overcoming these hurdles will be important to help businesses and industries thrive.

This blank space is caused due to formatting limitations. Text continues on next page.

Closing the gap for a brighter future

We are at a pivotal moment in the history of human invention. Future generations will certainly look back on the choices we make today. Deloitte’s prediction that 2025 will be a “gap year” for generative AI underscores this significant inflection point. These gaps—spanning infrastructure investment, gender disparities, energy consumption, trust deficits, and the capabilities of gen AI agents—are not just challenges for the industry but societal imperatives. How we collectively address these gaps will define the legacy we create.

Beyond gen AI, advancements in cloud computing and telecommunications are expected to bring unprecedented efficiencies, new business models, and augmented consumer experiences. Investments in sports infrastructure and the increasing prominence of women’s sports can act as catalysts for economic and social development. These trends reinforce the industry’s role in fostering innovation that enhances businesses, consumers, and broader communities.

The 2025 TMT Predictions represent opportunities to create lasting impact. By navigating the path forward with trust, inclusivity, and sustainability at the forefront, industry advancements can benefit not only the current generation, but all those who follow. Together, we can rise to the occasion and bridge the gap to a brighter tomorrow.

-Lara Abrash, chair, Deloitte US

Eight gaps that mark 2025 as a “gap year” for TMT

- The gen AI infrastructure and monetization gap. As we predicted last year, companies are spending tens of billions of dollars on chips and further hundreds of billions to build gen AI data centers for training and inference of gen AI models. While some companies offering gen AI enterprise software are seeing incremental revenues, the investment is 10 times (or more) higher than the return, at least for now. Those spending the most might suggest that the risk of underinvesting in gen AI is higher than the risk of overinvesting. But the gap persists and seems to be widening.

- The gen AI data center electricity and sustainability gap. Proposed gen AI data centers require unprecedented amounts of power, preferably low carbon, which is creating a gap between their needs and the capacities of electrical grids, and companies’ sustainability targets. Much is being done to close it by hyperscalers, chip companies, and utilities around the world, but the gap is expected to remain in 2025.

- The gen AI gender gap. Women are less likely than men to use gen AI tools for both work and play. Some of this is due to lack of trust, but women’s usage of gen AI is expected to catch up to men’s usage … within the year in some markets.

- The gen AI deepfake trust gap. The proliferation of deepfake gen AI content (images, video, and audio) is making it harder for consumers, as a society, to trust their own eyes and ears. That gap needs to be bridged by the gen AI ecosystem comprehensively and immutably labeling gen AI content, as well as reliably and accurately detecting fake images in real time. The marginal cost of creating convincing deep fakes is falling, and the cost of detection needs to fall at an equivalent pace to help close the gap.

- The studio gen AI usage gap: Many expect large studios to be using gen AI for content production, and some are, but there is a gap between those expectations and reality. Many are cautious about challenges with intellectual property inherent to generative content, but they are keen to gain enterprise capabilities that can reduce time, lower costs, and expand their reach.

- The autonomous gen AI agent gap. The prospect of autonomous bots that can consistently and reliably complete discrete tasks and orchestrate entire workflows is tantalizing. Agentic AI pilots are launching in 2024—will they reach widespread adoption in 2025?

- The streaming video gap. Many media and entertainment companies assumed consumers would “buy and hold” multiple subscriptions. Instead, customers are looking to cut costs by bundling their favorite subscriptions and dropping others. We now see the number of services per household not merely stagnating but shrinking, and streamers increasingly relying on bundling to help fill the growth gap and using other parties to aggregate and distribute their content.

- The cloud spending gap. One of the original selling points of using the cloud was the claim that it was cheaper, but in reality, spending is often decentralized and poorly controlled. Some buyers are leaning into FinOps to bridge the gap between promised cost savings and current spending to manage their cloud spending and potentially save billions.

New this year

This year, we’re introducing two new sections containing 11 additional mini predictions between them. Our Updates segment revisits seven topics from previous TMT Predictions reports to ask: “How’d we do?” while also exploring the latest predictions on those subjects. (Spoiler: We did really well!) Next, in our Rising trends section, we unveil four cutting-edge topics in TMT. While these emergent themes may not have made it into mainstream forecasts just yet, we believe they could be the hidden gems of tomorrow's industry conversations.

2025 topics

Here's a quick look at our main topics, plus those from our two new sections:

Women and generative AI: The adoption gap is closing fast, but a trust gap persists

For women to reap the full rewards of gen AI, tech companies should work to increase trust, reduce bias, and strive for more representative workforces

Deloitte predicts that women’s use of generative AI will equal or exceed that of men in the United States by the end of 2025. Although their use of gen AI was half that of men’s in 2023, their pace of adoption suggests they’ll reach parity in the United States within the next year and in many European countries within one to two years. Despite accelerating adoption, women express less trust that gen AI providers will keep their data secure—which may inhibit their full engagement and their gen AI spending. To help overcome this, tech companies should enhance data security and data management practices, mitigate AI bias, and improve women’s representation in their AI ranks.

As generative AI asks for more power, data centers seek more reliable, cleaner energy solutions

The tech industry should optimize infrastructure, rethink chip design, and collaborate with electricity providers to help secure a more sustainable future for data centers

AI-driven data center power consumption will continue to surge, with Deloitte predicting data centers will only make up about 2% of global electricity consumption by 2025. This growth is expected to emerge from high-density data center infrastructure to support massive computing power and cooling needs. But regulatory, infrastructure, and cost issues are posing challenges for electricity generation and the grid to keep pace with data centers’ unprecedented demand for 24/7 reliable energy. Technology and electric power industries can jointly address these issues by increasing the use of carbon-free sources, improving energy efficiency in gen AI chips and algorithms, and re-balancing compute-intensive AI workloads.

Ambitious stadium projects aim to bridge public-private investment goals

Sports owners transform stadiums into destinations, driving socioeconomic growth, community engagement, and revenue diversification

The sports industry has repeatedly demonstrated its ability to act as a catalyst for economic and social development, with stadiums largely at the epicentres of their communities. Investment in sports infrastructure is seeing an upward trend, as these developments often instigate wider returns to both the public and private sectors. With growth as a common goal between the public and private sectors, governments and communities can work with sports investors to provide supplementary investments in infrastructure and supercharge the socioeconomic impact of sports, enhance fan engagement, and diversify revenue streams for the organization. In 2025, we expect to see new stadium developments continue at pace, with almost half of these new projects expected to take place across North America and Europe.

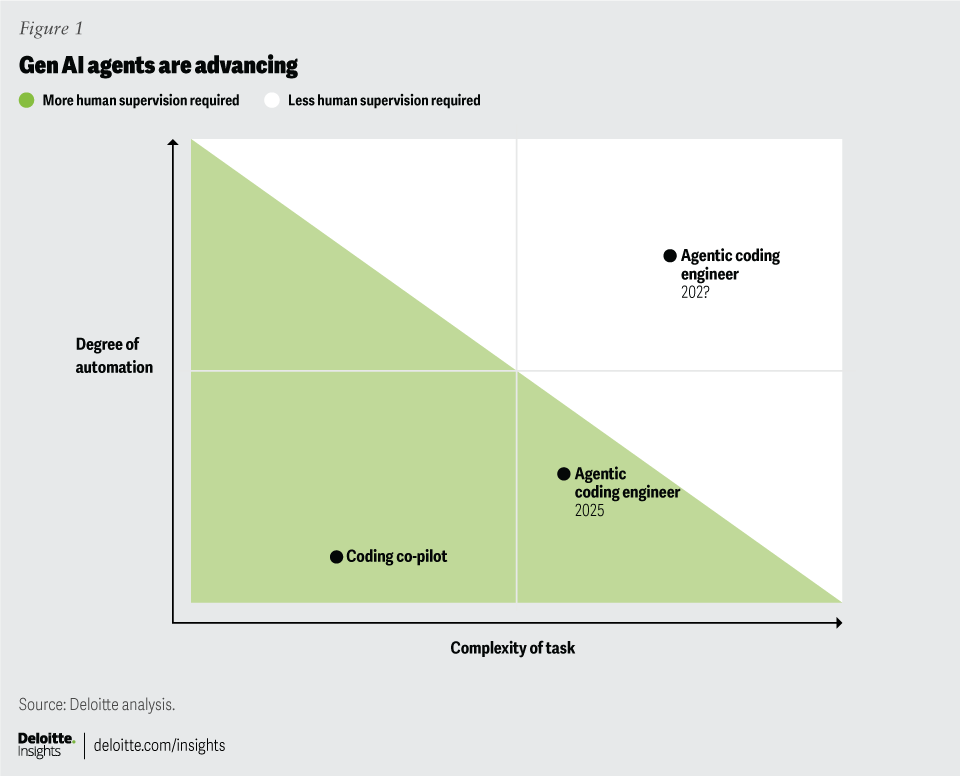

Autonomous generative AI agents: Under development

Autonomous gen AI agents—agentic AI—could increase the productivity of knowledge workers and make workflows of all kinds more efficient. But the “autonomous” part may take time for wide adoption.

Deloitte predicts that in 2025, 25% of companies that use gen AI will launch agentic AI pilots or proofs of concept, and this figure will grow to 50% in 2027. Agentic AI has the potential to complete complex tasks autonomously, improving the productivity and efficiency of knowledge workers. Some of today’s most promising applications include software development, customer support, cybersecurity, and regulatory compliance. The pace of improvement for agents is accelerating, but like most new technologies, widespread use will take time. That said, some agentic AI applications, in some industries, and for some use cases, may see actual adoption into existing workflows in 2025.

Deepfake disruption: A cybersecurity-scale challenge and its far-reaching consequences

As the effort to detect and combat fake content escalates, the costs of maintaining a credible internet may fall on consumers, creators, and advertisers alike

As AI generates increasing amounts of online images and video, questions around content authenticity and the potential harms of fake content grow more urgent. Online platforms, tech companies, and media players are taking two complementary approaches: using technology (often AI) to detect and flag fakes and using cryptographic metadata to assure provenance of authentic media assets. Deloitte predicts that this market will follow a similar pattern as that of cybersecurity, with bad actors finding ways to thwart detection tools and industries collaborating to confirm the credibility of at least some online content.

Cloud gets lean: ‘FinOps’ makes every dollar work harder

Enterprise cloud spend is growing, and using FinOps strategies can make each dollar work harder. Companies can save money, boost value, and build cross-functional cohesion.

Global cloud spend is set to top US$825 billion in 2025,1 but ask an organization’s leaders what they spend, and it might be difficult for them to answer. However, in 2025 Deloitte predicts more companies than ever will turn to “FinOps”, a set of tools and strategies to measure and optimize cloud spend, to save an estimated US$21 billion. Companies can start simple, acting to reduce cloud waste, take advantage of discounts, and proactively right-sizing compute, network, and storage. But advanced companies could also drive cultural change, such as making business units financially accountable for their portion of the cloud bill. The goal is a “cloud unit economics” model—linking each dollar of spend to the business value it generates, so that companies can make more effective decisions about IT.

On-device generative AI could make smartphones more exciting—if they can deliver on the promise

With specialized chips and extensive mobile OS integration, smartphones could become smart—even intelligent. Will users embrace the new approach?

Deloitte predicts that in 2025, global smartphone shipments will see a modest lift to around 7%, up from about 5% annual growth in 2024. Some of this lift will be due to the device upgrade cycle, which has been down the past two years, and some will be from early adopters seeking new generative AI capabilities. Smartphones with on-device generative AI capabilities will test the value of features like intelligent assistants and conversational interfaces; the capabilities of small models running on-device; and the business models seeking economic value from the capital intensity of the generative AI buildout. There is excitement about generative AI, but can the technology deliver on its promises, and will users embrace a new way of interacting with the most widely used consumer device?

Large studios will likely take their time adopting generative AI for content creation. Social media isn’t hesitating.

Hollywood (and others) may be cautious about using gen AI for content creation, but they will likely be quicker to adopt it for operations and distribution

In 2025, Deloitte predicts that the biggest TV and film studios—especially those in the United States and European Union—will be cautious in adopting generative AI into their creative workflows, with less than 3% of their production budgets going to these tools. But we also predict that operational spending will expand by 10% to integrate generative AI enabled tools for more bread-and-butter functions like contract and talent management, permitting and planning, marketing and advertising, and localization and dubbing of content that can expand their reach into diverse global markets. This approach can help studios slow the potential disruptions that gen AI can pose to talent and content, while more quickly adopting gen AI tools that can help reduce costs and accelerate performance across their businesses.

Reevaluating direct-to-consumer: The shift toward video aggregators

Video content creators may need more distributors to reach their total addressable market

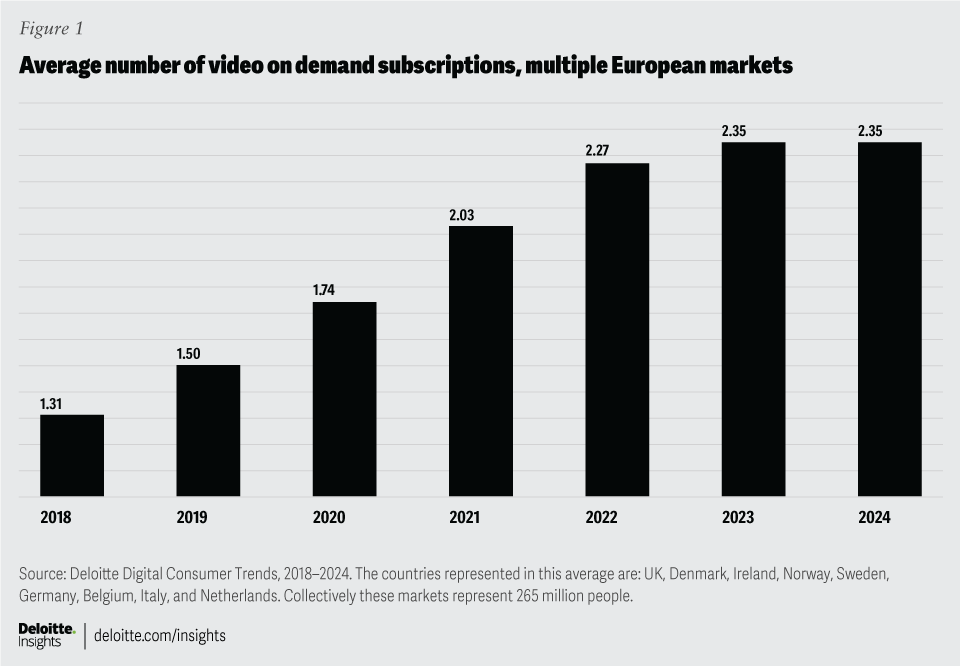

Consumers are expected to continue to stack streaming video services and have more than one standalone subscription at a time in 2025, but Deloitte predicts that the stack is about to get shorter. According to Deloitte surveys, after reaching more than four services per consumer in the United States and over two in most European markets in 2023 and 2024, we appear to have passed the peak, and the number of standalone services will slowly decline in most markets. Instead of consumers directly subscribing to each content provider’s service, there will likely be increased aggregation, where intermediaries—ranging from telcos to grocery stores to tech platforms to streamers themselves—combine multiple content sources in a single package. This trend is likely a win for many of the players, keeping costs under control and creating a stable and sustainable streaming ecosystem for 2025 and beyond.

Wireless telecom consolidation speeds up … where regulators allow

In many markets, smaller wireless telecoms see slow growth, low profits, and have debt to repay. M&A, specifically combining assets or even entire consumer-facing companies, may help where it gets approved by regulators.

In some markets, especially Europe and Asia, there is an increasing perception that wireless markets are too fragmented, subscale and unsustainable, with the smaller third and fourth place operators not able to invest in networks over the long term. Although these markets have historically kept the number of operators high, recent conversations have seen opportunity to allow or even encourage consolidation. Deloitte predicts that although it is expected to be a slow process, and regulators will have their conditions, there will be an increased pace of consolidation, beginning in 2025 and continuing, creating a more viable and sustainable wireless ecosystem, especially in smaller markets.

Updates

This year we’re looking at seven previous predictions to see how we did, and what the latest developments are:

Generative AI comes to the enterprise edge: ‘On-prem AI’ is alive and well

Owning their own servers gives companies a more private, secure, flexible, and possibly cheaper IT environment for AI

Deloitte predicts that although gen AI via cloud will continue to be the dominant option in 2025, about half of the enterprises worldwide will add AI data center infrastructure on premises, primarily to protect their IP and sensitive data, comply with data sovereignty or other regulations, and save costs. Deloitte’s 2024 State of Generative AI in the Enterprise Q2 survey noted 80% of companies with “very high” AI expertise reported spending more on AI in the cloud … but 61% are investing more in their own hardware. Enterprise gen AI will likely be a hybrid approach, with enterprises doing some in the cloud, and some on premise.

(Re)defining the investment case for women’s sports

Rising women’s sports revenue fuels investor interest and valuation records

The increasing professionalization and commercialization of women’s sports around the world is garnering the attention of fans, sponsors and—critically—investors. In 2024, we predicted the women’s elite sports market would generate over $1 billion in revenue. In North America, clubs are recognizing record valuations, from Angel City FC in the National Women’s Soccer League at a valuation of $250 million2 to Las Vegas Aces in the Women’s National Basketball Association at $140 million.3 Elsewhere, organizations are creating innovative structures to channel investment into their women’s teams and emphasizing strategic growth, independent leadership, and commercial opportunities. In 2025, we expect to see an expanding group of investors—including institutional investors, private equity and high net worth individuals—take more note.

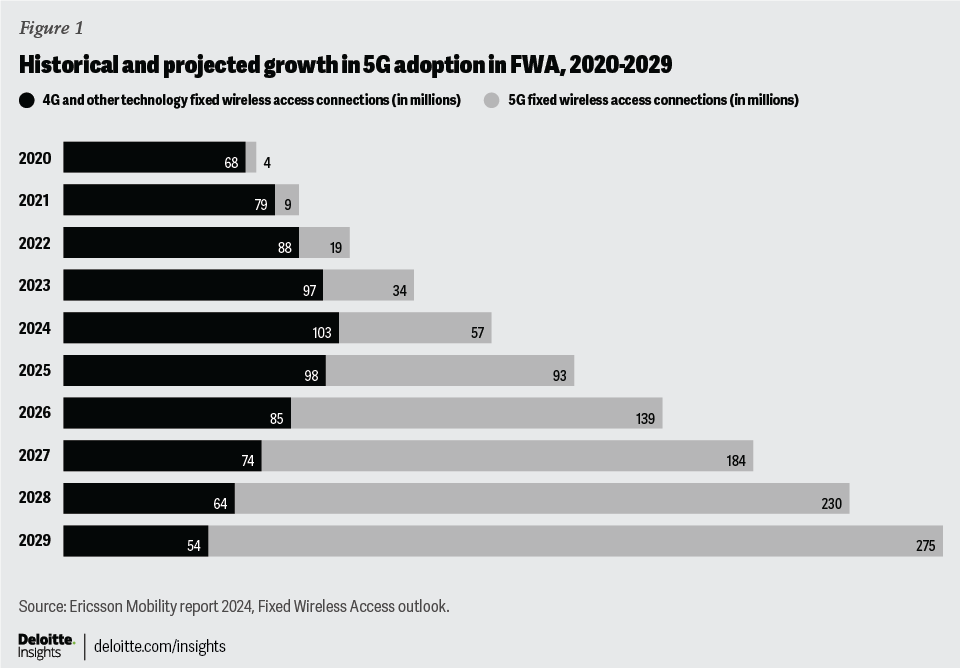

Fixed wireless access: Contrary to popular opinion, adoption may continue to grow

With US FWA net adds likely being slightly lower than last year, and some markets not expected to take off until 2026 … there may be pockets of unrealized or potential growth out there, both in the US and globally

Fixed wireless access (FWA)—when consumers and enterprises get their home broadband over a fixed cellular device (mainly 5G) rather than via wires—has been the 5G growth story over the last few years in the United States, with well more than 10 million homes expected to be connected by the end of 2024. However, growth is slowing, with the first quarter of 2024 net additions lower than Q1 2023, and a potential slowdown anticipated in 2025. Despite this, Deloitte predicts global FWA net additions will rise by 20% annually in 2025 and 2026 (in line with our 2022 Prediction on FWA), driven by growth in new enterprise FWA and markets that are not as large as the United States or India individually but still add up to millions in new subscriptions annually.

5G standalone appears to be at a standstill: Will 6G run late?

Telecoms reassess investments in 5G standalone and delay 6G progress amid ROI concerns

The deployment of 5G standalone networks is progressing more slowly than expected. Telecom companies may be hesitant to invest heavily in this next generation of 5G in part due to underwhelming returns on their existing 5G investments, making the rollout of 6G seem further away than ever. In 2022, Deloitte Global predicted that the number of telcos investing in 5G SA networks would double from more than 100 operators in 2022 to at least 200 by the end of 2023, but that has not happened: as of March 2024, only 49 operators (out of 585 who have launched 5G globally) have deployed, launched, or soft-launched 5G SA networks.4 In 2025, Deloitte predicts that fewer than 20 additional networks will be upgraded to standalone, keeping 5G SA at around 12% of all 5G deployments.

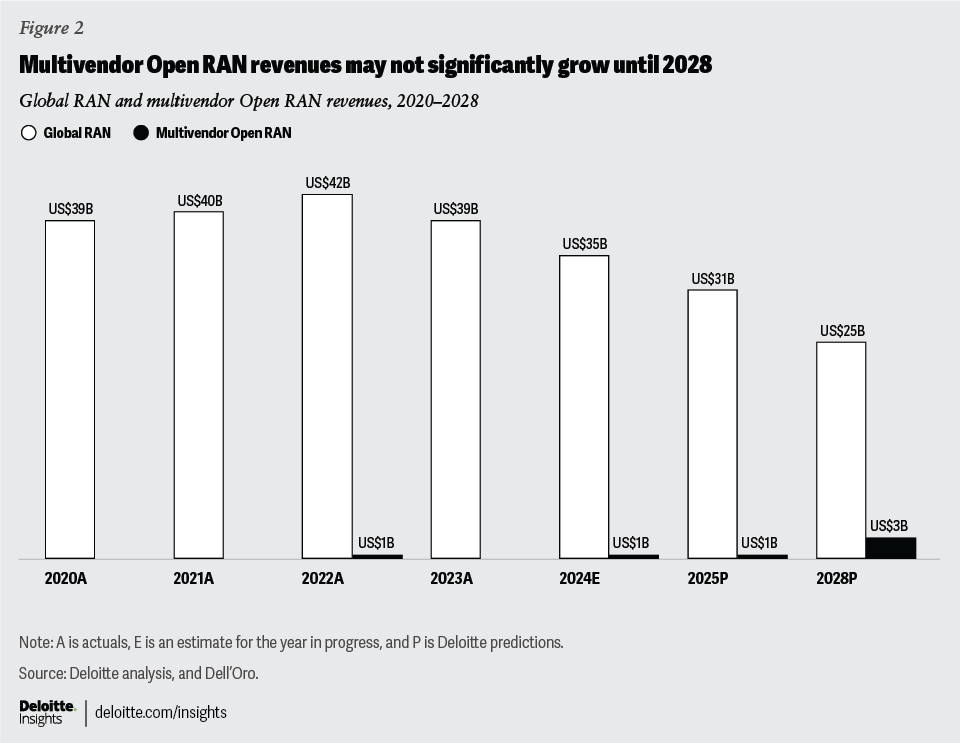

Open RAN mobile networks and vendor choice: Single vendor now, multivendor when?

Open RAN's journey toward a diverse, multivendor ecosystem is marked by slow growth and complex challenges

Open Radio Access Network (Open RAN) aims to democratize networks by providing mobile network operators (MNOs) who build RANs with greater choice and more flexibility. In 2021, Deloitte predicted that global active Open RAN deployment would double from 35 to 70. We were too optimistic: as of March 2024, the ongoing Open RAN deployments and trials stand at 45, with only two networks globally being multivendor Open RAN.5 The transition towards a diverse, multivendor ecosystem is proving slower and more complex than initially anticipated, and realizing true multivendor Open RAN may take a while. Deloitte predicts that no additional multivendor Open RAN networks will be deployed or announced in 2025.

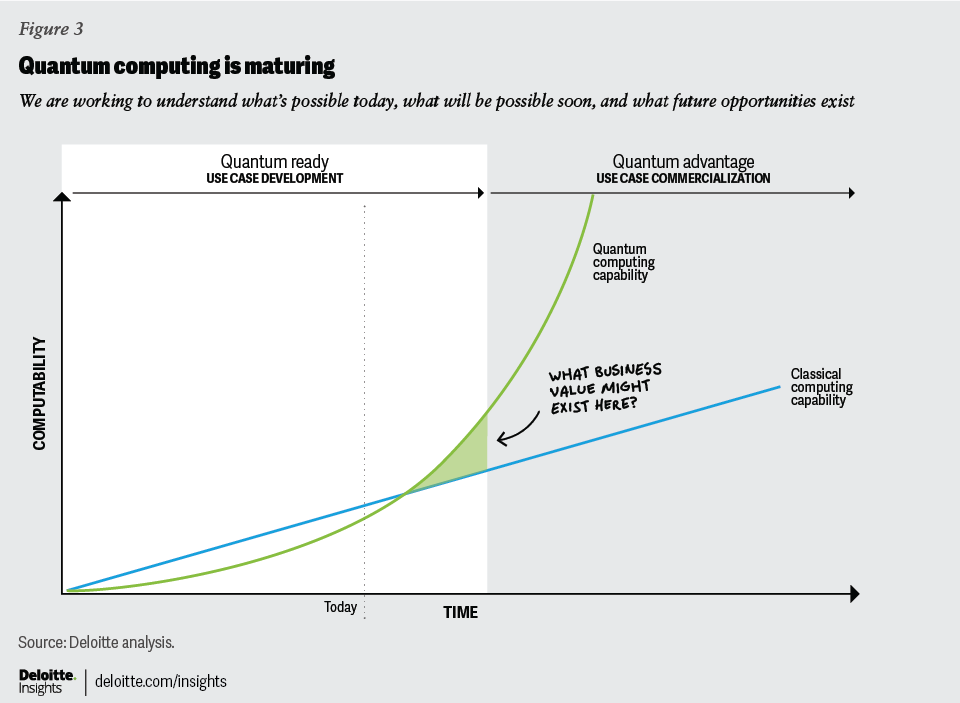

Despite quantum’s slow start, don’t be slow to start your defense against it

Quantum drug discovery and financial modeling are likely several years away, but the time needed to upgrade cyber defenses for the quantum age likely necessitates prompt action

As Deloitte predicted in past reports, quantum computers remain works in progress, with few real-world use cases where they offer a computing advantage, at least for now. But the threat of “harvest now, decrypt later” attacks, where threat actors gather encrypted data, store it for years, and then unlock it with cryptographically relevant future quantum computers at some point has reached a tipping point. Deloitte predicts that the number of companies, and the dollars spent, working on implementing post quantum cryptography standards will quadruple in 2025 compared with 2023. Post-quantum cryptographic solutions are expected to span the gamut in 2025, from enterprise and hyperscalers to consumer smartphones and messaging services.

RISC-V: Closing the geopolitical gen AI loophole

An open-source alternative to proprietary chip design is gaining popularity among CPU designers. Its potential role in gen AI for markets under export restriction is a new twist for a new technology.

As predicted in Deloitte’s 2022 Global TMT Predictions report, open-source RISC-V (pronounced risk five) CPU chips revenues are expected to be close to US$1 billion by 2024. And RISC-V based SoC shipments could be close to two billion units. But in a new development, there are discussions in the United States about restricting RISC-V chips exports, as it involves potential national security risks, given how China is “making significant investments in RISC-V chip design architecture” to undermine US export controls and “leapfrog” US technological leadership in chip design. Gen AI servers need both GPUs (already under various export restrictions) and CPUs to control data flows. Closed-source CPU architectures are already under US export restrictions, and therefore, restricting RISC-V based designs may close an apparent alternative.

Rising trends

Keep your eye on these newly emerging trends. We predict they could soon become the center of attention, transforming the conversation and shaping the future of the industry:

Generative AI and cyber: Big risks, but big opportunities too

Recognizing generative AI's potential for enabling both threats and cyber solutions, cybersecurity professionals are exploring ways to harness its power to counter emerging risks and help fortify the technology environment

From the 2024 Deloitte-NASCIO Cybersecurity Study, nearly three quarters of security experts surveyed said the cyber threat from AI was high. Gen AI-based cyberattacks look like they will have doubled or tripled in 2024, and Deloitte predicts they will grow again in 2025, used by threat actors writing malicious phishing emails, deepfakes, or software code for malware attacks. Tech companies who make gen AI tools will likely develop guardrails to prevent malicious use in 2025. While gen AI tools can be used by threat actors for malicious purposes, the same tools can also be used by defenders to help improve security processes, monitoring, and risk management.

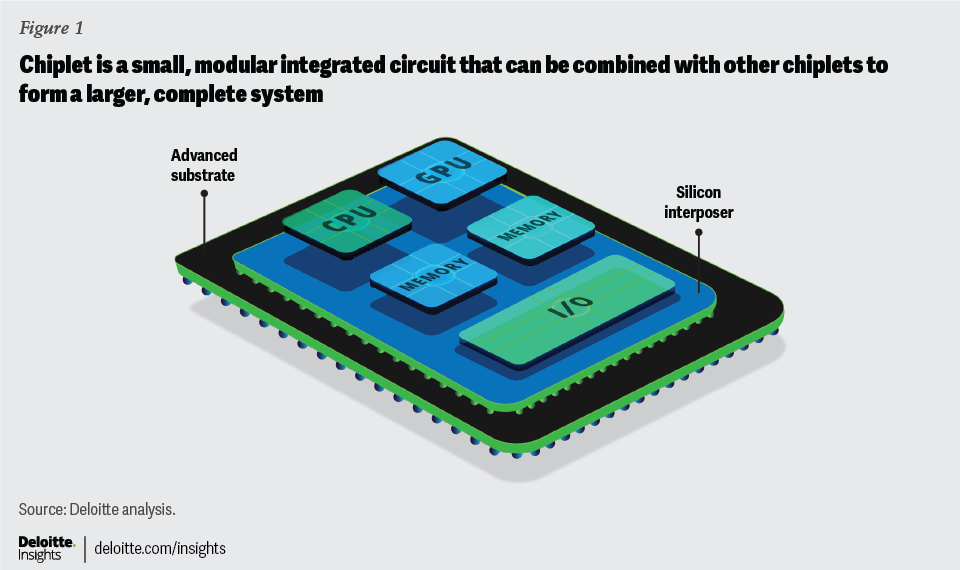

Silicon building blocks: Chiplets could move Moore’s Law forward

Chiplets promise to deliver more flexible, scalable, and efficient systems for AI and high-performance computing environments, at higher yields

Chiplets—a heterogeneous technological architecture to develop and package semiconductors—enable high-speed data transfers, reduce latency, and help optimize PPA (power, performance, and area). Deloitte predicts worldwide advanced packaging revenue based on chiplets will more than double from an estimated US$7 billion in 2021 to reach US$16 billion in 2025. Chiplets are already used and explored in some of the fast-growing markets such as AI accelerators (especially generative AI), high performance computing, and telecommunications applications. They’re enabling the semiconductor industry to continue increasing performance and yield.

B/OSS: Telcos modernize their business and operational support systems software

Telcos’ back-end business and operations software market is growing slowly but modernizing it—by adopting SaaS and microservices architecture, moving to the cloud and more—is a hot spot of growth for software vendors and an opportunity for telcos to do more with 5G, fiber, and AI

Historically, telcos maintained separate IT systems: business support systems (BSS) for customer orders, customer relationship management (CRM), and billing, and operational support systems (OSS) for order management, network inventory, and operations, often custom-built and hardware defined. These systems were typically on-premises and composed of vertical, siloed solutions. However, by 2025, many telcos are expected to modernize and integrate these systems, driven by evolving customer expectations and new digital revenue streams. Deloitte predicts that the global B/OSS market will reach $70 billion by 2025, growing at 5% annually. Cloud-based solutions and software-as-a-service offerings are expected to grow significantly faster, at 22% and 18% annually. Most of the growth in the next few years is expected to come from the Americas, Middle East, North Africa, and emerging Asia-Pacific regions.

Silicon photonics: Gen AI communicates at lightspeed

Propelled by the demanding requirements of gen AI, optical devices on silicon are stepping out of research labs and into the limelight of data centers

Deloitte predicts that sales of silicon photonics chips used as optical transceivers will grow at a compounded annual growth rate of 25% from 2023 to 2025 to reach US$1.25 billion in 2025. These chips allow gen AI data centers to communicate at lightspeed, use components that are smaller and cheaper, consume less energy, and produce less heat than the traditional alternatives. In 2025, the main driver of silicon photonics adoption is expected to be in data center applications, specifically for those running gen AI training and inference—especially where data needs to travel anywhere from 10 cm to 10 meters between chips, trays, and racks.

Endnotes

Gartner, “Gartner forecasts worldwide public cloud end-user spending to surpass $675 billion in 2024,” press release, May 20, 2024.

Angle City FC, “Willow Bay and Bob Iger to become Angel City's new controlling owners,” July 17, 2024.

Josh Sim, “Las Vegas Aces valued at US$140m as average WNBA team hits US$96m,” SportsPro, June 18, 2024.

GSA, “5G - GSA Market Snapshot March-2024,” March 4, 2024.

TeckNexus, “Current State of Open RAN – Countries & Operators deploying & trialing Open RAN,” March 10, 2024.

Acknowledgements

We wish to thank Duncan Stewart, Jeff Loucks, and Paul Lee, plus the entire team, for their work on the Predictions report.

Cover image by: Jaime Austin; Getty Images, Adobe Stock

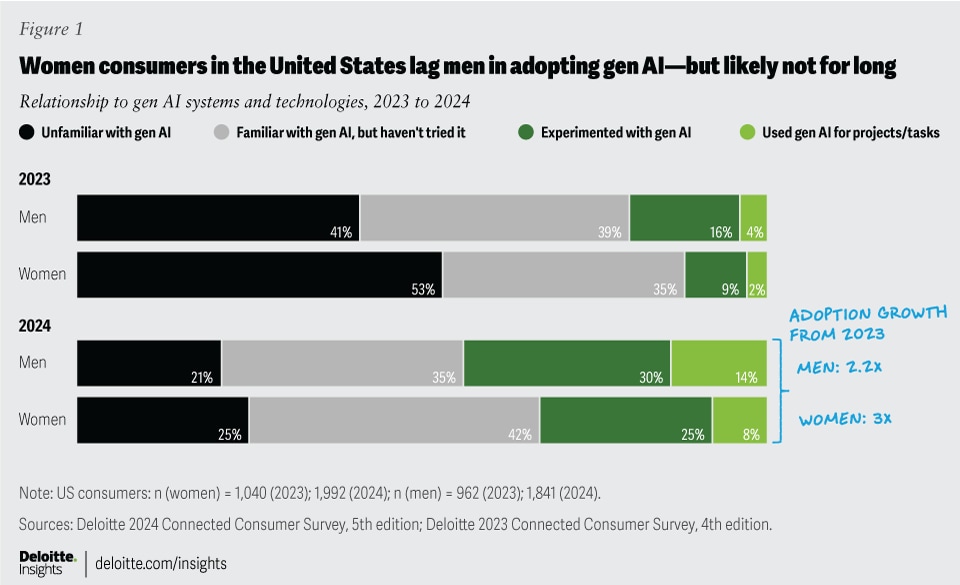

Deloitte predicts that the experimentation with and use of generative AI by women will equal or exceed that of men in the United States by the end of 2025.1 Although women’s use of gen AI was half that of men’s in 2023, their pace of adoption suggests they’re likely to reach parity within the next year.2 While this parity prediction is for the United States, the gen AI gender gap is a global phenomenon: In European countries, where the use of gen AI has been surveyed, our analysis not only identified significant gender adoption differences but also revealed that women are making up ground rapidly.3 These countries will likely close the adoption gender gap within the next two years—and the global challenges and opportunities for adoption will likely mirror the US findings.

Despite accelerating their gen AI adoption, women express less trust than men that gen AI providers will keep their data secure.4 This “technology trust gap” could inhibit women’s regular use of the technology and full participation in new gen AI applications, as well as slow down their future purchasing of gen AI products and services. To help overcome this trust gap, tech companies should enhance their data security, implement clearer data management practices, and provide greater data control.

AI model bias can also have a negative impact on trust.5 Women constitute less than one-third of the AI workforce,6 and most AI workers feel that AI will produce biased results as long as their field continues to be male dominated.7 Increasing women’s presence in the field can help reduce gender bias in AI, as well as give women a greater role in steering the future of the technology.

The gen AI adoption gap is closing rapidly

Recent Deloitte research has highlighted a gender gap in generative AI adoption across various geographies. For the past two years, the Deloitte Connected Consumer Survey has investigated the adoption of gen AI by US consumers as part of its research into digital life.8 Our analysis revealed that women in the United States have been lagging in taking up this emerging technology (figure 1): In 2023, women’s adoption of gen AI was roughly half that of men (11% of women reported experimenting with gen AI or using it for projects and tasks beyond experimentation, vs. 20% of men). In 2024, the same survey revealed that gen AI adoption overall had more than doubled, but the gender gap remained: Thirty-three percent of women surveyed reported using or experimenting with gen AI, vs. 44% of men.

The gen AI gender gap has been noted in other geographies too: Deloitte UK’s 2024 Digital Consumer Trends survey of UK consumers reported that 28% of women were using gen AI, vs. 43% of men.9 Analysis of this study, as well as Deloitte UK’s European study on gen AI and trust, revealed double-digit differences between women’s and men’s adoption of gen AI in 12 additional European countries.10

In the United States, women are rapidly closing the adoption gap. In the past year, the proportion of US women surveyed who have adopted gen AI tripled—outpacing the 2.2x rate of growth for men.11 Analysis of current adoption levels and these rates of growth allows Deloitte to predict that the proportion of women experimenting with and using gen AI for projects and tasks will match or surpass that of men in the United States by the end of 2025.12

Full engagement may be harder to achieve

While the trend is encouraging, reaching adoption parity won’t automatically ensure that women will incorporate gen AI into their everyday workflows. Indeed, among gen AI users surveyed in Deloitte’s 2024 Connected Consumer Survey, 34% of women say they use the technology at least once a day, vs. 43% of men.13 And among gen AI users who reported using it for professional tasks, 41% of women currently feel that gen AI substantially boosts their productivity, vs. 61% of men.14 Tech companies and other organizations looking to benefit from using gen AI should heed these differences and take active steps to improve women’s engagement.

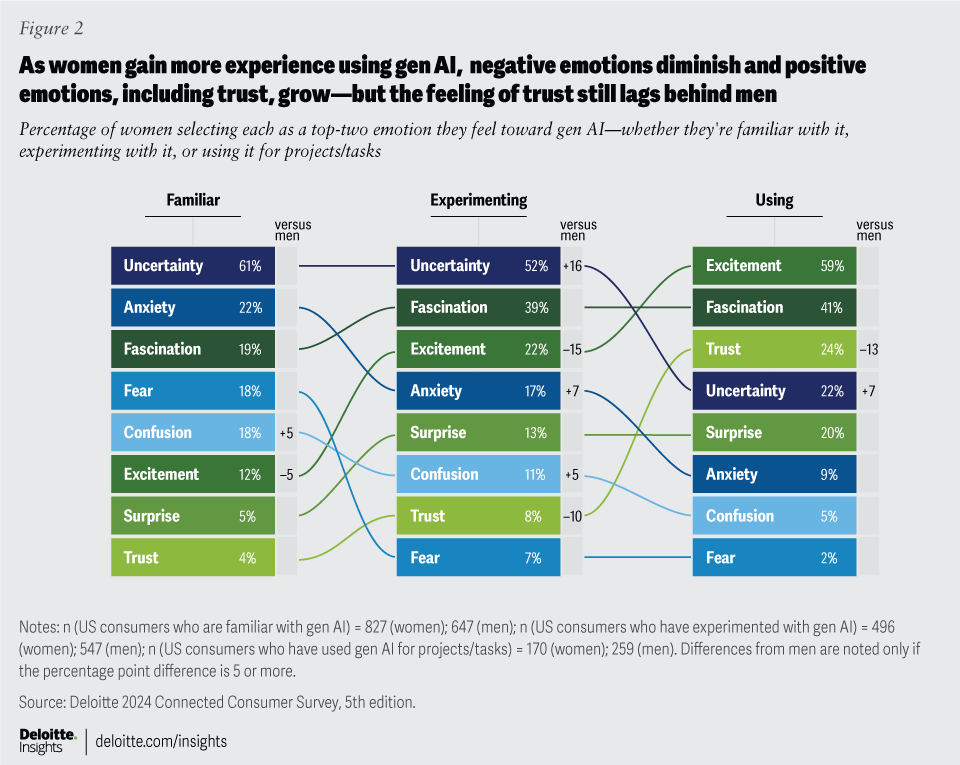

The contrasts between genders may stem partly from a striking difference in perspective on trust.15 As women progress from familiarity with gen AI into experimentation and use, negative emotions of uncertainty, anxiety, fear, and confusion diminish, while positive feelings of fascination, excitement, surprise, and trust grow (figure 2).16 However, at both the experimentation and project and task use levels, women’s feelings of trust toward the technology are significantly lower than men’s, and their feelings of uncertainty remain higher. Indeed, only 18% of women surveyed who are experimenting with or using generative AI indicated having “high” or “very high” trust that the providers of the gen AI capabilities they use will keep their data secure—whereas, for male adopters, that number has reached 31%.17

The trust gap is not unique to gen AI, but extends to broader tech services and interactions: While 54% of women surveyed in Deloitte’s 2024 Connected Consumer Survey agree that the benefits they get from online services outweigh their data privacy concerns (an improvement from 46% in 2023), more men agree (62%).18 Last year, we reported that women are more wary than men about how their personal data is used and protected and that it was affecting their willingness to share data, particularly when it comes to sensitive health and fitness metrics.19 Women may perceive the potential consequences of a security breach or data misuse as more significant.20

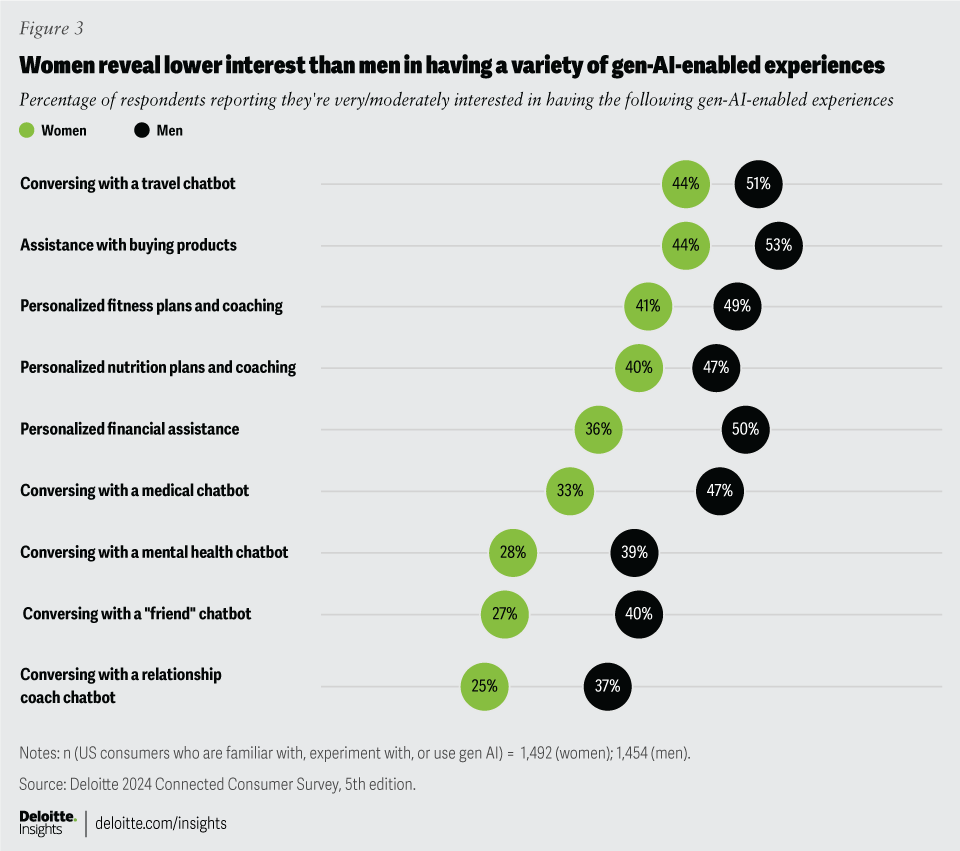

The growing popularity of generative AI may exacerbate these longstanding issues around data privacy and tech.21 As users interact with gen AI, the systems may feed users’ data back into their AI models—and experts say it’s not necessarily clear or easy to opt out of having one’s data used for AI training.22 As consumers start to converse with gen AI for advice on sensitive, personal topics, the data privacy and security stakes grow. Indeed, the trust gap around data privacy and security may underpin the differences we’re seeing between women’s and men’s levels of interest in having a variety of gen AI experiences in the future (figure 3).23 Surveyed women are somewhat less interested than men in interacting with gen AI on less-sensitive topics (such as travel, shopping, fitness, and nutrition), but they are substantially less interested than men in engaging with gen AI around more sensitive topics (such as personal finances and relationships, and medical or mental health issues).

The trust gap may also contribute to less excitement among women to purchase new gen AI technologies. Tech companies are beginning to sell laptops, tablets, and smartphones with embedded AI chips designed to improve functionality (for example, summarizing information in real time, generating photos and videos, and instantly translating foreign languages).24 When Deloitte’s 2024 Connected Consumer Survey asked whether new AI functionality will have any effect on their plans to upgrade devices, fewer women said they’re likely to upgrade their devices sooner compared to men.25 For example, while 43% of men with smartphones said embedded AI would make them very or somewhat likely to upgrade their phone sooner than planned, only 32% of women said the same (conversely, 58% of women said it would have no effect on their upgrade plans, vs. 50% of men). And when it comes to laptops, 41% of men said on-device AI would make them very or somewhat likely to upgrade those devices sooner, vs. 28% of women. With women controlling or influencing an estimated 85% of consumer spending, their lower enthusiasm for upgrading to devices with AI could pose an issue for tech providers.26

The trust gap is not the only factor holding women back from maximizing their use of gen AI. Women gen AI users surveyed are less likely to feel that their company actively encourages their use of the technology at work (61% of women users feel this way, vs. 83% of men).27 And while 49% of women gen AI users say that their company invests in training employees on how to use generative AI, that falls short of the 79% of men reporting the same. Whether these numbers reflect differences in perception or actual experiences with access to training programs and encouragement in the workplace, companies should pay heed and work to close the gaps.

Women in tech are forging ahead with gen AI—but better representation is needed

In the tech industry, there is a different story about gen AI adoption entirely—and women working in tech may hold clues for fostering greater gen AI engagement by women overall in the future. Not surprisingly, the industry creating AI products and services has higher levels of gen AI adoption among its employees: In Deloitte’s 2024 Connected Consumer Survey, 70% of women and 78% of men working in the tech industry reported experimenting with gen AI or using it for projects or tasks—far outpacing nontech women (32%) and men (40%).28 What may be more surprising is that women working in the tech industry appear to be moving beyond gen AI experimentation and into using it for projects and tasks faster than their male counterparts (44% vs. 33%). And both groups are anticipating greater benefits: About 7 in 10 women and men working in tech expect their use of gen AI to “substantially boost” their productivity at work a year from now.29

What’s more, there’s no notable trust gap between tech women and men. Both groups have greater trust in generative AI than adopters overall: More than 40% of tech women and men using or experimenting with gen AI reported having “high” or “very high” trust that gen AI providers will keep their data secure.30 In both groups, 75% of those surveyed agree that the benefits they get from online services outweigh their privacy concerns—vs. just 54% of women and 60% of men working outside tech.31 It’s likely that women in the tech industry have a better understanding of how gen AI works than nontech workers, and that their heavier professional use of gen AI has increased their comfort level and shown them how they can benefit from the technology. Moreover, most tech women who use gen AI reported that their companies encourage its use (84%) and provide training (72%)—in contrast, among women using gen AI in other industries, far fewer reported that their companies encourage its use (55%) or provide training (45%).32

Despite the greater adoption of AI by women in the tech industry, there’s a relative lack of women working in AI roles. Women only make up about 30% of the AI-related workforce, which is comparable to their representation in STEM fields overall.33 This underrepresentation of women in AI could have serious implications for the development and deployment of AI systems across various domains and sectors.

One of the major challenges posed by the relative lack of women in the AI workforce is the risk of perpetuating gender bias against women in AI applications.34 As many as 44% of AI systems across industries exhibit gender bias, which can negatively affect outputs from AI systems in ways that continue to marginalize and underrepresent women.35 For instance, gender bias in AI can lead to bias in hiring practices,36 lower quality health care,37 and reduced access to financial services for women.38 And Deloitte research has shown that bias in AI models can erode employee and customer trust.39 Bringing more women into AI jobs can be crucial for achieving gender equality and ensuring that AI benefits society.40

Bottom line

There are several reasons why tech companies should work toward increasing women’s engagement with gen AI. First, with women controlling or influencing most consumer purchasing, failing to get women on board with frequent gen AI use could increase the risk that AI products and services won’t achieve their expected potential. Second, if women don’t engage with gen AI tools as fully as male employees, companies could risk not achieving the productivity gains they might expect to see after investing in gen AI. And, because gen AI depends upon collecting and building upon interaction data, the underrepresentation of women’s interactions could exacerbate biases in AI models.41 Finally, if women don’t participate in emerging gen AI use cases as fully as they could, that may keep them from maximizing future tech benefits (for example, advantages of chatbot interventions in medical or mental health) and deepen existing inequities.42

To help bolster women’s trust in gen AI, tech companies should work to address the potential risks associated with the technology. Deloitte’s 2024 Connected Consumer Survey found that earning trust may depend at least partially on improving the transparency of tech companies’ data privacy and security policies, as well as making it easier for consumers to control their personal data.43 Tech companies should consider prioritizing robust data security measures and communicating their data-handling practices more effectively. Making it simpler for consumers to understand what data gets collected and how it’s used, along with providing easier ways to control that use (such as prompting users at appropriate points to make informed choices about the use of their data) may not only build trust but could also confer a competitive advantage. But it’s not just tech companies that should pay heed to potential gen AI risks: Eighty-four percent of survey respondents believe that governments should do more to regulate the way companies collect and use consumer data.44

Across industries, companies that want to achieve full use of gen AI by men and women workers should take care to encourage the use of gen AI capabilities. Beyond various popular professional use cases—document editing, web searches, summarizing materials, and research assistance—companies can embrace industry-specific ways to use generative AI.45 Maximizing the use of gen AI by employees may require establishing training programs.

Striving for full consumer engagement in generative AI is a commendable objective, but it may be more difficult to achieve without equitable representation among the people who develop generative AI technologies. To increase the diversity and inclusion of women in AI roles, companies should consider focusing on creating workplaces that meet the needs of those they employ. For example, a study of women in AI noted that work/life balance is the most important factor for their job satisfaction, which includes elements such as having a flexible working schedule or being able to work remotely.46 Women also reported looking for jobs with women in leadership, transparency around pay and promotions, and zero-tolerance policies for harassment and abuse.47 Attracting more women to the field may also involve providing more education and training opportunities for women to learn AI skills and competencies. It could also be beneficial to create more mentorship and networking programs that allow women in AI to share their experiences and support one another, and to provide funding for more women to participate in AI research and innovation projects. As women’s role in developing gen AI grows, it’s likely that there will be applications and systems that engage all women more.

Endnotes

To understand consumer attitudes toward digital life, the Deloitte Center for Technology, Media & Telecommunications surveyed 3,857 US consumers in the second quarter of 2024 and 2,018 US consumers in the second quarter of 2023. These 2024 and 2023 Connected Consumer Surveys collected data on consumers’ reported adoption of generative AI, including experimentation and use for projects and tasks (beyond experimentation). By analyzing longitudinal adoption data and calculating the rate of change in adoption from 2023 to 2024 for men and women, we are able to project that women will close the adoption gap by the end of 2025; see: Jana Arbanas et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey, 5th edition, Deloitte, December 3, 2024; Jana Arbanas, Paul H. Silverglate, Susanne Hupfer, Jeff Loucks, Prashant Raman, and Michael Steinhart, “Balancing act: Seeking just the right amount of digital for a happy, healthy connected life,” Deloitte Insights, Sept. 5, 2023.

Ibid.

Our analysis was conducted from August to October 2024, based on data from Deloitte UK’s 2023 and 2024 Digital Consumer Trends surveys, as well as a 2024 Deloitte UK survey of European consumers on the topic of generative AI; see: Paul Lee and Ben Stanton, “Generative AI: 7 million workers and counting,” Deloitte, June 25, 2024; Jonas Malmlund, Frederik Behnk, and Joachim Gullaksen, “Generative AI is all the rage,” Deloitte, 2023; Roxana Corduneanu, Stacey Winters, Jan Michalski, Richard Horton, and Ram Krishna Sahu, “Europeans are optimistic about generative AI but there is more to do to close the trust gap,” Deloitte Insights, Oct. 10, 2024.

Analysis based on Deloitte’s 2024 Connected Consumer Survey; see: Arbanas et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Don Fancher, Beena Ammanath, Jonathan Holdowsky, and Natasha Buckley, “AI model bias can damage trust more than you may know. But it doesn’t have to.” Deloitte Insights, Dec. 8, 2021.

World Economic Forum, “Global gender gap report 2023,” June 2023.

Deloitte AI Institute, “Women in AI,” accessed November 2024.

Jana Arbanas et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey, 5th edition, Deloitte, publishing December 3, 2024; Arbanas, Silverglate, Hupfer, Loucks, Raman, and Steinhart, “Balancing act.”

Deloitte, “Generative AI: 7 million workers and counting,” accessed November 2024.

The Digital Consumer Trends study conducted in various countries in 2024 revealed gen AI adoption gaps of 17 points in Denmark; 12 points in Sweden, Italy, and the Netherlands; 11 points in Belgium; and 10 points in Norway. Additional analysis of a Deloitte European gen AI study revealed gen AI adoption gaps ranging from 10 to 15 points in 11 European countries studied (Belgium, France, Germany, Ireland, Italy, the Netherlands, Poland, Spain, Sweden, Switzerland, and the United Kingdom); see: Deloitte, “Generative AI”; Deloitte, “Generative AI is all the rage,” accessed November 2024; Corduneanu, Winters, Michalski, Horton, and Sahu, “Europeans are optimistic about generative AI but there is more to do to close the trust gap.”

Analysis based on 2024 and 2023 Deloitte Connected Consumer Surveys; see: Arbanas et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey; Arbanas, Silverglate, Hupfer, Loucks, Raman, and Steinhart, “Balancing act.” Deloitte, “Generative AI.”

Ibid.

Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Ibid.

Ibid.

Ibid.

Ibid.

Ibid.

For example, only 43% of women we surveyed in the Deloitte 2023 Connected Consumer Survey who owned smart watches or fitness trackers said that they share the data collected by those devices with their health care provider, vs. 57% of men; see: Susanne Hupfer, Jennifer Radin, Paul H. Silverglate, and Michael Steinhart, “Tech companies have a trust gap to overcome—especially with women,” Deloitte Insights, Nov. 8, 2023.

These fears may be warranted. Consider that most health apps—along with the data they gather and transmit—are not covered by the Health Insurance Portability and Accountability Act, which means the data may be shared or sold to third parties; see: Steve Alder, “Majority of Americans mistakenly believe health app data is covered by HIPAA,” The HIPAA Journal, July 26, 2023.

Ina Fried, “Generative AI’s privacy problem,” Axios, March 14, 2024; Federal Trade Commission, “AI companies: Uphold your privacy and confidentiality commitments, Jan. 9, 2024.

Ibid; Matt Burgess and Reece Rogers, “How to stop your data from being used to train AI,” Wired, April 10, 2024.

Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Baris Sarer, Ricky Franks, Cheryl Ho, and Jake McCarty, “AI and the evolving consumer device ecosystem,” The Wall Street Journal, April 24, 2014; Sam Reynolds, “AI-enabled PCs will drive PC sales growth in 2024, say research firms,” Computer World, Jan. 11, 2024; Clare Conley, “Generative AI in 2024: The 6 most important consumer tech trends,” Qualcomm, Dec. 14, 2023.

Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Monique Woodard, “Unlocking the trillion-dollar female economy,” TechCrunch, May 21, 2023.

Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Ibid.

Across industries, 51% of women workers using gen AI anticipate it would substantially boost their productivity at work a year from now, vs. 64% of men; see: Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Tech women and men are statistically tied: Forty-two percent of tech women who use or experiment with gen AI have “high” or “very high” trust that gen AI providers will keep their data secure, and another 40% report moderate trust, while 47% of tech men report “high” or “very high” trust and another 30% report moderate trust; see: Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Ibid.

Greater proportions of men in the tech industry who use gen AI report that their employers encourage its use (93%) and provide training (91%). While there’s still a gender gap in these views among workers in the tech industry, the gap is significantly smaller than among men and women working in other industries; see: Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

World Economic Forum, “Global gender gap report 2023.”

Deloitte, “Generative AI.”

Genevieve Smith and Ishita Rustagi, “When good algorithms go sexist: Why and how to advance AI gender equity,” Stanford Social Innovation Review, March 31, 2021.

Charlotte Lytton, “AI hiring tools may be filtering out the best job applicants,” BBC, Feb. 16, 2024.

Carmen Niethammer, “AI bias could put women’s lives at risk - A challenge for regulators,” Forbes, March 2, 2020.

Ryan Browne and MacKenzie Sigalos, “A.I. has a discrimination problem. In banking, the consequences can be severe,” CNBC, June 23, 2023.

Fancher, Ammanath, Holdowsky, and Buckley, “AI model bias can damage trust more than you may know. But it doesn’t have to.”

World Economic Forum, “Global gender gap report 2023.”

Smith and Rustagi, “When good algorithms go sexist.”

Hyun-Kyoung Kim, “The effects of artificial intelligence chatbots on women’s health: A systematic review and meta-analysis,” Healthcare, Feb. 23, 2024; Sheryl Jacobson and Jen Radin, “Can FemTech help bridge a gender-equity gap in health care?” Deloitte, Oct. 5, 2023; Karen Taylor, “Why investing in FemTech will guarantee a healthier future for all women,” Deloitte UK, June 23, 2023.

Arbanas, et al., Earning trust as gen AI takes hold: 2024 Connected Consumer Survey.

Ibid.

Deloitte AI Institute, “The generative AI dossier: A selection of high-impact use cases across six major industries,” April 3, 2023.

Women in AI, “WAI at work: Shaping the future of work for women in AI,” 2022.

Ibid.

Acknowledgements

Authors would like to thank Duncan Stewart, Paul Lee, Ben Stanton, Vipul Mehta, Roxana Corduneanu, Michael Steinhart, Michelle Dollinger, Jeff Stoudt, Catherine King, Elizabeth Fisher, Andy Bayiates, Prodyut Borah, Molly Piersol, Deloitte Insights team.

Cover image by: Jaime Austin; Getty Images, Adobe Stock

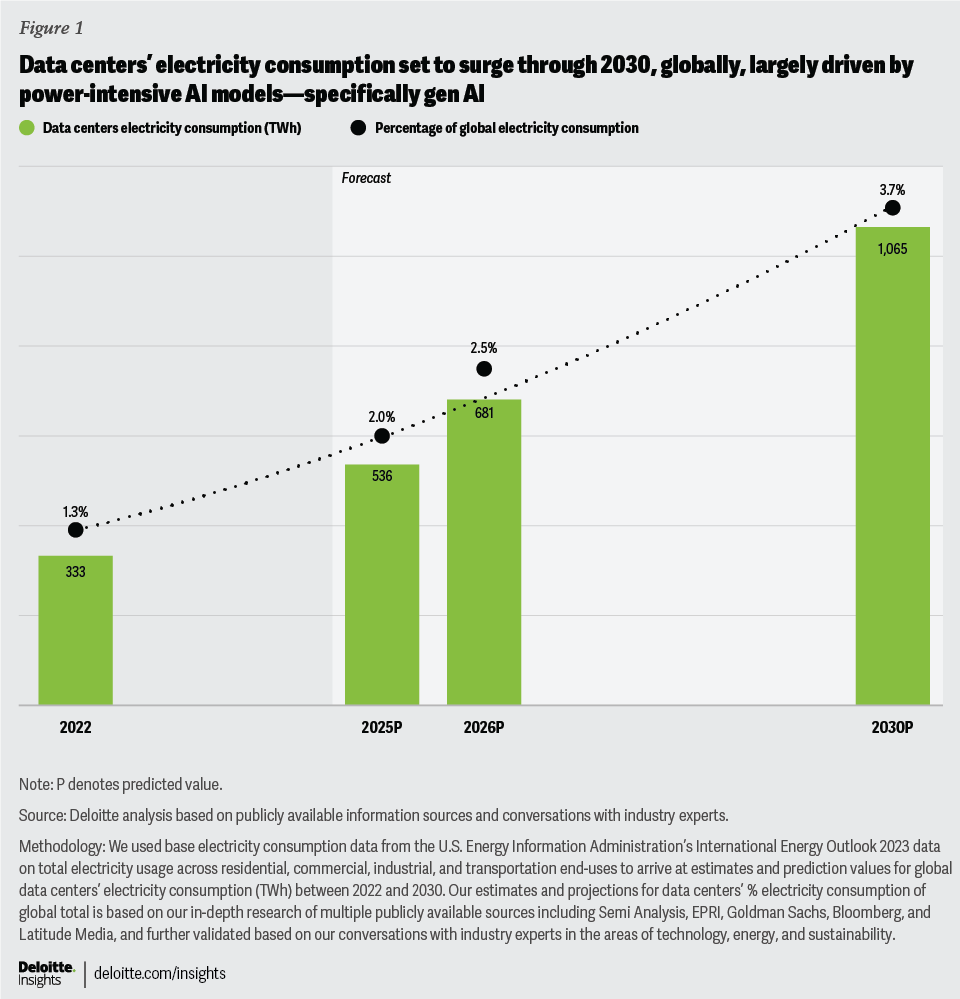

AI-driven data center power consumption will continue to surge, but data centers are not—in fact—that big a part of global energy demand. Deloitte predicts data centers will only make up about 2% of global electricity consumption, or 536 terawatt-hours (TWh), in 2025. But as power-intensive generative AI (gen AI) training and inference continues to grow faster than other uses and applications, global data center electricity consumption could roughly double to 1,065 TWh by 2030 (figure 1).1 To power those data centers and reduce the environmental impact, many companies are looking to use a combination of innovative and energy-efficient data center technologies and more carbon-free energy sources.

Nonetheless, it’s an uphill task for power generation and grid infrastructure to keep pace with a surge in electricity demand from AI data centers. Electricity demand was already growing fast due to electrification—the switch from fossil-fueled to electric-powered equipment and systems in the transport, building, and industrial segments—and other factors. But gen AI is an additional, and perhaps, an unanticipated source of demand. Moreover, data centers often have special requirements as they need 24/7 power supply with high levels of redundancy and reliability, and they’re working to have it be carbon-free.

Estimating global data centers’ electricity consumption in 2030 and beyond is challenging, as there are many variables to consider. Our assessment suggests that continuous improvements in AI and data center processing efficiency could yield an energy consumption level of approximately 1,000 TWh by 2030. However, if those anticipated improvements do not materialize in the coming years, the energy consumption associated with data centers could likely rise above 1,300 TWh, directly impacting electricity providers and challenging climate-neutrality ambitions.2 Consequently, driving forward innovations in AI and optimizing data center efficiency over the next decade will be pivotal in shaping a sustainable energy landscape.

Some parts of the world are already facing issues in generating power and managing grid capacity in the face of growing electricity demand from AI data centers.3 Critical power to support data centers’ most important components—including graphics processing unit (GPU) and central processing unit (CPU) servers, storage systems, cooling, and networking switches—is expected to nearly double between 2023 and 2026 to reach 96 gigawatts (GW) globally by 2026; and AI operations alone could potentially consume over 40% of that power.4 Worldwide, AI data centers’ annual power consumption is expected to reach 90 terawatt-hours by 2026 (or roughly one-seventh of the predicted 681 TWh of all data centers globally), roughly a tenfold increase from 2022 levels.5 As such, gen AI investments are fueling demand for so much electricity that in the first quarter of 2024, global net additional power demand from AI data centers was roughly 2 GW, an increase of 25% from the fourth quarter of 2023 and more than three times the level from the first quarter of 2023.6 Meeting data center power demand can be challenging because data center facilities are often geographically concentrated (especially in the United States) and their need for 24/7 power can burden existing power infrastructure.7

Deloitte predicts that both the technology and electric power industries can and will jointly address these challenges and contain the energy impact of AI—more specifically, gen AI. Already, many big tech and cloud providers are investing in carbon-free energy sources and pushing for net-zero targets,8 demonstrating their commitment to sustainability.

Hyperscalers plan massive expansion of gen AI data centers to help support growing customer demand

The surge in electricity demand is largely due to hyperscalers’ plans to build out data center capacity, globally.9 As AI demand—specifically gen AI—is expected to grow, companies and countries are racing to build more data centers to meet that demand. Governments are also establishing sovereign AI capabilities to maintain tech leadership.10 The data center real estate build-out has reached record levels based on select major hyperscalers’ capital expenditure, which is trending at roughly US$200 billion as of 2024, and estimated to exceed US$220B by 2025.11

Moreover, Deloitte’s State of Generative AI in the Enterprise survey noted that enterprises have been mostly piloting and experimenting until now.12 But as they experiment with getting value from gen AI, respondents are seeing tangible results and so intend to quickly scale up beyond pilots and proofs of concept. If usage grows as the technology matures, hyperscalers’ and cloud providers’ capital expenditure will most likely remain high through 2025 and 2026.

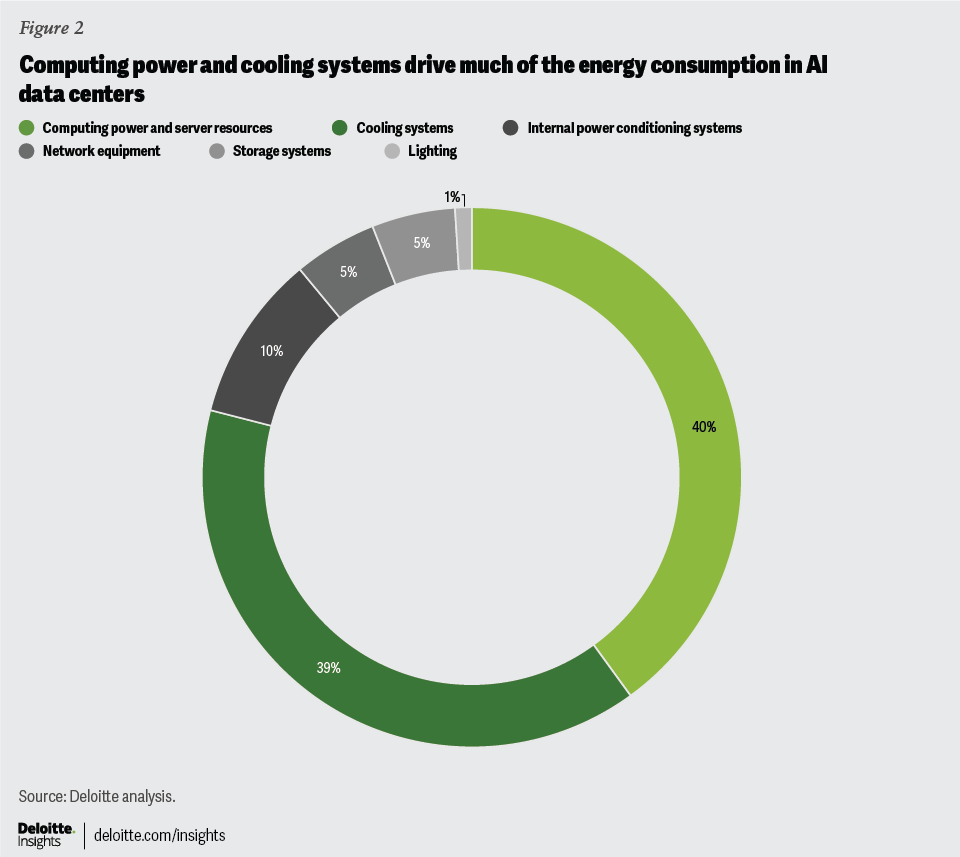

Two broad areas drive most of the electricity consumption in a data center: computing power and server resources like server systems (roughly 40% data center power consumption) and cooling systems (consume 38% to 40% power). These two are the most energy-intensive components even in AI data centers, and they will continue to fuel data centers’ power consumption. Internal power conditioning systems consume another 8% to 10%, while network and communications equipment and storage systems use about 5% each, and lighting facilities usually use 1% to 2% of power (figure 2).13 With gen AI requiring massive amounts of power, data center providers—including the hyperscalers and data center operators—need to look at alternate energy sources, new forms of cooling, and more energy-efficient solutions when designing data centers. Several efforts are already underway.

Gen AI is contributing to increased electricity demand

Data centers’ energy consumption has been surging since 2023, thanks to exploding demand for AI.14 Deploying advanced AI systems requires vast numbers of chips and processing capacity, and training complex gen AI models can require thousands of GPUs.

Hyperscalers and large-scale data center operators that are supporting gen AI and high-performance computing environments require high-density infrastructure to support computing power. Historically, data centers relied mainly on CPUs, which ran at roughly 150 watts to 200 watts per chip.15 GPUs for AI ran at 400 watts until 2022, while 2023 state-of-the-art GPUs for gen AI run at 700 watts, and 2024 next-generation chips are expected to run at 1,200 watts.16 These chips (about eight of them) sit on blades placed inside of racks (10 blades per rack) in data centers, and are using more power and producing more heat per square meter of footprint than traditional data center designs from only a few years ago.17 As of early 2024, data centers typically supported rack power requirements of 20 kW or higher. But the average power density is anticipated to increase from 36 kW per server rack in 2023 to 50 kW per rack by 2027.18

Total AI computing capacity, measured in floating-point operations per second (FLOPS), has also been increasing exponentially since the advent of gen AI. It’s grown 50% to 60% quarter over quarter globally since the first quarter of 2023 and will likely grow at that pace through the first quarter of 2025.19 But data centers don’t only measure capacity in FLOPS, they also measure megawatt hours (MWh) and TWh.

Gen AI’s multibillion parameter LLMs and the multibillion watts they consume

Gen AI large language models (LLMs) are becoming more sophisticated, incorporating more parameters (variables that enable AI learning and prediction) over time. From the 100 to 200 billion parameter models that were released initially during 2021 to 2022, current advanced LLMs (as of mid-2024) have scaled up to nearly two trillion parameters, which can interpret and decode complex images.20 And there’s competition to release LLMs with 10 trillion parameters. More parameters add to data processing and computing power needs, as the AI model must be trained and deployed. This can further accelerate demand for gen AI processors and accelerators, and in turn, electricity consumption.

Moreover, training LLMs is energy intensive. Independent research of select LLMs that were trained on more than 175 billion parameters of data sets demonstrated that they consumed anywhere between 324 MWh and 1,287 MWh of electricity for each training run … and models are often retrained.21

On average, a gen AI–based prompt request consumes 10 to 100 times more electricity than a typical internet search query.22 Deloitte predicts that if only 5% of daily internet searches, globally, use gen AI– based prompt requests, it would require approximately 20,000 servers (with eight specialized GPU cores in each of the servers) that consume 6.5 kW on an average per server to fulfill the prompt requests, amounting to an average daily electricity consumption of 3.12 GWh and annual consumption of 1.14 TWh23—which is equivalent to annual electricity consumed by approximately 108,450 US households.24

Data center demand could present challenges and opportunities for power sector transition

The electric power sector was already planning for rising demand: Many in the industry predicted as much as a tripling of electricity consumption by 2050 in some countries.25 But that trajectory has recently accelerated in some areas due to burgeoning data center demand. Previous forecasts in many countries have projected rising power demand due to electrification as well as increasing data center consumption and overall economic growth. But recent sharp spikes in data center demand, which could be just the tip of the iceberg, reveal the growing magnitude of the challenge.26

Round-the-clock, carbon-free electricity that many tech companies seek can be hard to come by, especially in the short term.

This comes against the backdrop of a multi-decade power industry transformation, as electric companies build, upgrade, and decarbonize electric grid infrastructure, and digitalize systems and assets. In many areas, electric companies are also hardening assets against increasingly severe weather and climate events and protecting networks from rising cybersecurity threats.27 Electric power grids in some countries are struggling to keep up with demand, especially for low- or zero-carbon electricity. In the United States, data centers are anticipated to represent 6% (or 260 TWh) of total electricity consumption in 2026.28 The United Kingdom may witness a sixfold growth in electricity demand within a period of just 10 years, largely due to AI.29 In China, data centers—including the ones that power AI—will likely make up 6% of the country’s total electricity demand by 2026.30 Data centers could also add to China’s pollution problem, since the country’s power generation is dominated by coal, which accounted for 61% of its energy use and 79% of its carbon dioxide emissions in 2021.31

Some countries that are facing the rising demand for electricity from data centers are responding with regulations. For instance, in Ireland, existing data centers consume a fifth of the country’s total electricity consumption and this is only expected to grow further as AI-driven data centers spring up more; households are even lowering their power consumption.32 Temporarily, Ireland halted the construction of new data centers connected to the grid, but has since reversed that position.33 Like Ireland, even the city of Amsterdam halted new data center construction to support sustainable urban development.34 Singapore announced new sustainability standards for data centers that require operators to gradually increase the overall operating temperatures of their facilities to 26°C or higher. Higher operating temperatures reduce the demand for cooling and lower power consumption, but at the cost of shortening the lifespan of the chips.35

The urgency and geographic concentration of data center demand—and the requirement for 24/7 carbon-free energy—can further complicate the challenge for tech companies and electricity providers, in addition to new demand from electrification, manufacturing, and other sources. The largest data center market globally is in northern Virginia,36 and the local utility, Dominion Energy, expects power demand to grow by about 85% over the next 15 years, with data center demand quadrupling.37 The round-the-clock, carbon-free electricity that many tech companies seek can be hard to come by, especially in the short term. Electricity providers are exploring multiple avenues to help meet demand while maintaining reliability and affordability. In addition to new renewable energy and battery storage, many electricity providers have also announced plans to build natural gas–fired power plants, which are not carbon-free.38 This could potentially make it more challenging to meet utility, state, and even national decarbonization targets.39

Despite being poised to consume massive amounts of clean energy, AI could also potentially help hasten the clean energy transition: Some utilities are already using AI to enable electric grids to operate more cheaply, efficiently, and reliably through improved weather and load forecasting, enhanced grid management and renewable asset performance, faster storm recovery, better wildfire risk assessment, and more.40

Data center cooling is water-intensive

Next-generation CPUs and GPUs have higher thermal density properties than their predecessors. At the same time, some server vendors are packing more and more power-hungry chips into each rack in an endeavor to cater to the growing demand for high-performance computing and AI applications. But denser racks will demand more water, especially to cool the gen AI chips. AI data centers’ freshwater demand could be as much as 1.7 trillion gallons (at the higher end) by 2027.41 A hyperscale data center that intends to manage excess heat with air-based cooling and evaporated drinking water would require over 50 million gallons of water every year (or roughly what it takes to make 14,700 smartphones).42 This water cannot be returned to the aquifer, reservoir, or water supply where it came from.43

Air-based cooling alone uses up to 40% of a typical data center’s electricity consumption. Therefore, data centers are looking at alternatives to traditional air-based cooling methods, mainly into liquid cooling, as its higher thermal transfer properties could help cool high-density server racks and enable them to reduce power usage by as much as 90% when compared with air-based methods.44 As liquid cooling directly delivers cooling to server racks, it can support dense power racks on the order of 50 kW to 100 KW or more.45 Moreover, it may help eliminate the need for chillers, which were traditionally used for producing the cooling water.

However, despite liquid cooling technology’s promise to help save energy across the data center stack,46 it’s still in its early days and is yet to be widely adopted or integrated into AI data centers, globally.47 Moreover, water is a finite resource, and therefore its cost and availability will likely affect future decisions about its usage.

The tech industry is moving toward more sustainable solutions and carbon-free sources

To help expedite the move toward using carbon-free sources to power AI data centers, tech industry majors continue to be aggressive in their pursuit of renewable energy by way of power purchase agreements, or long-term contracts with renewable energy providers.48 These deals have helped bankroll renewable energy projects by enabling them to secure financing. In some cases, technology companies are working with electricity providers and innovators to help test and scale promising energy technologies, including advanced geothermal, advanced wind and solar technologies, hydropower, and even underwater data centers.

In some areas, local grid constraints and long interconnection times for new renewable and battery storage facilities are causing delays in connecting these resources to the electric grid.49 These delays, which can be as long as five years in the United States, are often due to high demand and insufficient transmission infrastructure. As a result, tech companies are increasingly pursuing onsite, sometimes off-grid, energy solutions.50 Additionally, they are investing in new technologies such as long-duration energy storage and small modular nuclear reactors to help address these challenges. In some cases, tech companies and utilities are planning to coordinate to bring innovative clean energy technologies to scale, which could eventually benefit other organizations and help decarbonize the electric grid faster.51 Many of these research and development programs, pilots and other clean energy investments may take years before reaping benefits, demonstrating return on investment, and becoming commercially viable.52 For example, small, modular nuclear reactors are still in early development stages, and may not be a near-term zero-carbon solution.53

The technology sector consistently dominates US corporate renewable procurement and accounted for more than 68% of the nearly 200 deals of associated contracted capacity tracked over the 12 months prior to Feb. 28, 2024.54 Similarly, hyperscalers and data center operators in India are increasingly using solar to power their data centers in the region.55 Without these purchase commitments, many renewable energy projects would not be built.56

As such, the tech industry’s role in bankrolling clean energy technologies to help bring them to scale will continue to be valuable. In some cases, they’re working directly with innovators and renewable energy producers, and in other cases, they’re partnering with utilities.57 Importantly, the way tech companies inject capital to help advance the clean energy transition is critical, as neither the innovators nor the power industry would typically have the level of financial resources that the tech industry possesses.

Bottom line

What should the broader tech industry, hyperscalers, data center operators, utilities, and regulators do to help meet gen AI demand sustainably? Several considerations for hyperscalers and the broader tech industry are more or less in line with what we presented in Deloitte Global’s 2021 prediction on cloud migration.58 Though demand drivers may have changed and the pace of change has accelerated, the industry is working to achieve balance between sustainability and expedited time to market, while keeping data centers rising energy demands under control and finding more sustainable ways to power AI—specifically gen AI.

Do we need to keep racing to build bigger and bigger foundational models (for example, more than a trillion parameter models), or are smaller models sufficient, while being more sustainable?

1. Make gen AI chips more energy-efficient: Already, a new generation of AI chips can perform AI training in 90 days, consuming 8.6 GWh. This would be less than one-tenth the energy that the previous generation of chips takes to do the same function on the same data.59 Chip companies should continue to work with the broader semiconductor ecosystem to help intensify focus on improving FLOPS/watt performance, such that, future chips can train AIs several times larger than the largest AI systems currently available while using less electricity.

2. Optimize gen AI uses and shift processing to edge devices: This includes assessing whether it’s energy-efficient to do training and inference in the data center, or on the edge device, and accordingly rebalance data center equipment needs. Edge not only can support applications where response times are critical, but also for those use cases where sensitive data is involved, or privacy needs are high. It also helps save network and server bandwidth, rerouting gen AI workloads to local and near-location or co-location devices, while only transmitting select AI workloads to data centers.60

3. Implement changes in gen AI algorithms and rightsize AI workloads: Do we need to keep racing to build bigger and bigger foundational models (for example, more than a trillion parameter models), or are smaller models sufficient, while being more sustainable? Already, startups are developing on-device multimodal AI models, which do not require energy-intensive computations in the cloud.61 Customers should fine-tune and adjust the size of their AI workloads and go for targeted gen AI models (including preexisting models and training only when needed) based on real business needs, which can minimize energy use. Additionally, depending on specific needs with AI inferencing (for example, doing inference in real time and when latency is critical), CPUs can be more advantageous and efficient.62

4. Form strategic partnerships to serve local and cluster-level AI data center needs: For several small to midsize organizations (including universities) that may find it hard to tap into gen AI data center capacity, those organizations should work with specialized data center operators and cloud service providers that focus on delivering high-performance computing solutions for smaller high-performance computing GPU-cluster co-locations.63 A corollary: Data centers can then actively track usage and availability for potential opportunities and demand pockets to help deliver near-term co-location services.

5. Collaborate with other stakeholders and sectors to make an overall positive environmental impact: The various ecosystem players—including hyperscalers, their customers, third-party data center operators and co-location service providers, electricity providers, the local regulators and municipalities, and the real estate firms—should have ongoing conversations around what’s feasible and viable for the business, environment, and society.64 That collaboration should encompass multiple aspects including determining potential strategic co-location needs (where a data center company rents computing and server resources to one or more companies), assessing cooling needs such as adequate temperatures in liquid cooling systems, identifying solutions to manage heat and wastewater, and figuring out recycling needs. For example, in Europe, data center operators are directing waste heat to warm swimming pools in the vicinity.65 Electricity providers should consider working more closely with the tech industry to understand how to meet data center energy demand, while identifying ways the tech companies could potentially help fund and scale new energy technologies, which is a vital step to bring more clean energy to the grid.

The holistic efforts of hyperscalers and electricity providers to help increase the use of carbon-free sources to power data centers—including the ones being built exclusively for gen AI—may bear fruit in the longer term.

Endnotes

Deloitte analysis based on publicly available information sources and conversations with industry specialists. We used base electricity consumption data from the US Energy Information Administration’s (EIA) International Energy Outlook 2023 data on total electricity usage across residential, commercial, industrial, and transportation end uses (a reference to US Energy Information Administration, “Table: Delivered energy consumption by end-use sector and fuel,” accessed Nov. 4, 2024) to arrive at estimates and prediction values for global data centers’ electricity consumption (TWh) between 2022 and 2030. Our estimates and projections for data centers’ percent electricity consumption of global total are based on our research of multiple publicly available sources including SemiAnalysis, EPRI, Goldman Sachs, Bloomberg, and Latitude Media, and further validated based on our conversations with subject matter specialists in the areas of technology, energy, and sustainability. Total energy consumption by end-use sector and fuel (as noted from the aforementioned table from EIA’s International Energy Outlook 2023 data), globally, is estimated and forecast at 26,787 TWh in 2025, 27,256 TWh in 2026, and 29,160 TWh in 2030— increasing from 25,585 TWh back in 2022.

As noted in endnote 1 above, we arrived at 2022 to 2030 data, estimates, and predictions based on a combination of in-depth secondary research of multiple publicly available sources, and validated further from our discussions with subject matter specialists. Also, see Prof. Dr. Bernhard Lorentz, Dr. Johannes Trüby, and Geoff Tuff, "Powering artificial intelligence," Deloitte Global, November 2024."

One-fifth of Ireland’s electricity is consumed by data centers, and this is expected to grow, even as households are lowering their electricity use. To read further, see: Chris Baraniuk, “Electricity grids creak as AI demands soar,” BBC, May 21, 2024.

Dylan Patel, Daniel Nishball, and Jeremie Eliahou Ontiveros, “AI data center energy dilemma: Race for AI data center space,” SemiAnalysis, March 13, 2024.

Ibid.

Data center BMO report, Communications Infrastructure, “1Q24 data center leasing: Records are made to be broken,” April 28, 2024; Moreover, due to strong demand from cloud providers and AI workloads, the data center primary market supply in the United States alone was up 26% year over year to 5.2 GW in 2023, and more are under construction. See further: CBRE, “North America data center trends H2 2023,” March 6, 2024.

Lisa Martine Jenkins and Phoebe Skok, “Mapping the data center power demand problem, in three charts,” Latitude Media, May 31, 2024.

Based on our analysis of multiple publicly available information and reports from what companies self-report, and further validated from third-party sources.

For context, hyperscalers are large cloud service providers and data centers that offer huge amounts of computing and storage resources typically at enterprise scale. See: Synergy Research Group, “Hyperscale operators and colocation continue to drive huge changes in data center capacity trends,” Aug. 7, 2024.

Yifan Yu, “AI’s looming climate cost: Energy demand surges amid data center race,” Nikkei Asia, June 12, 2024.

Data center BMO report, Communications Infrastructure, “1Q24 data center leasing: Records are made to be broken,” April 28, 2024. Further, Deloitte analysis based on information from select tech companies’ publicly available sources such as earnings releases and Dell’Oro Group’s market research data on data center IT capital expenditure shows that if we consider the capital expenditure spending of other data center providers, including third-party operators and outsourced cloud service providers, data centers’ aggregate capital expenditure spending could be at least US$250 billion in 2025. See: Baron Fung, “Market research on data center IT capex,” Dell’oro Group, accessed Nov. 4, 2024.

Nitin Mittal, Costi Perricos, Brenna Sniderman, Kate Schmidt, and David Jarvis, “Now decides next: Getting real about generative AI,” Deloitte’s State of Generative AI in the Enterprise quarter two report, Deloitte, April 2024.