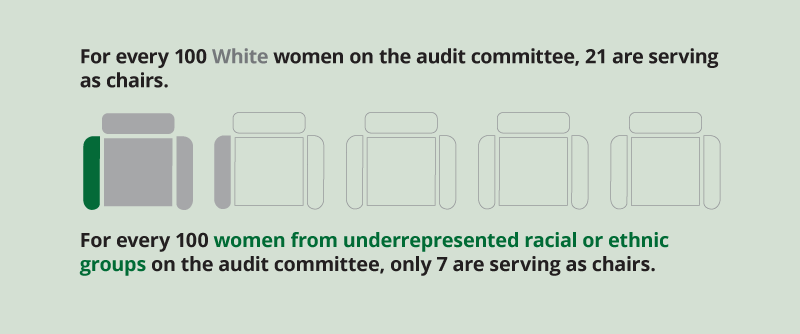

Missing Pieces Report

A board diversity census of women and underrepresented racial and ethnic groups on Fortune 500 boards, 7th edition

The importance of diversity on the board of directors

The Missing Pieces report is a multiyear study organized by the Alliance for Board Diversity (ABD) in collaboration with Deloitte for the 2016, 2018, 2020, and 2022 censuses. The report highlights the progress to date that has, or has not, been made in the equitable representation of women and individuals from underrepresented racial and ethnic groups (UR&EG) on Fortune 500 boards.

${subheader}

${video-2-title}

${video-3-title}

In the Fortune 500, boards seats held by individuals from UR&EG have increased since 2020.

Fortune 500 board seats held by individuals from underrepresented racial and ethnic groups increased to 22.2% in 2022, an improvement from 17.5% in 2020. But as we note in other sections of this edition of Missing Pieces, the level of representation in the Fortune 500 lags the Fortune 100.

Take a look back

${column4-title}

${column4-text}

Key contacts