Rising to the challenge: Semiconductor sustainability trends has been saved

Perspectives

Rising to the challenge: Semiconductor sustainability trends

Drivers for growth and change in the semiconductor industry

New sustainability drivers in the semiconductor sector

Clients and other industry actors are interested in learning about the broad trends and patterns that we see in our work in the semiconductor sector, and interest is especially high in the critical task of driving sustainability through their operations and ecosystems. In this article, we summarize the primary sustainability drivers and strategies that we are seeing across the industry. Subsequent articles will discuss each trend in depth.

Commitment to transforming the social and environmental sustainability of our economy is present across many industries. Progress toward these objectives has been met with many challenges and successes, as companies navigate their responsibilities in addressing business impacts on communities and climate, while dealing with the economics, market structures, and incentives of their specific industry. While the task is far from simple, the resolve of the majority of companies in the semiconductor sector to solve these challenges remains strong: addressing the industry’s energy use during manufacturing, water consumption, labor conditions, limited supplier diversity, mineral and other raw material sourcing, as well as both its direct and indirect climate emissions,i is mission-critical to the sector’s continued growth and resilience—and arguably also to maintaining social acceptance of the ever more pervasive role that semiconductors play in our lives.

What are the overarching sustainability trends that Deloitte sees in the sector?

Learn more about the sustainability trends and strategies driving change in the semiconductor industry.

Sustainability drivers and strategies in today’s semiconductor sector

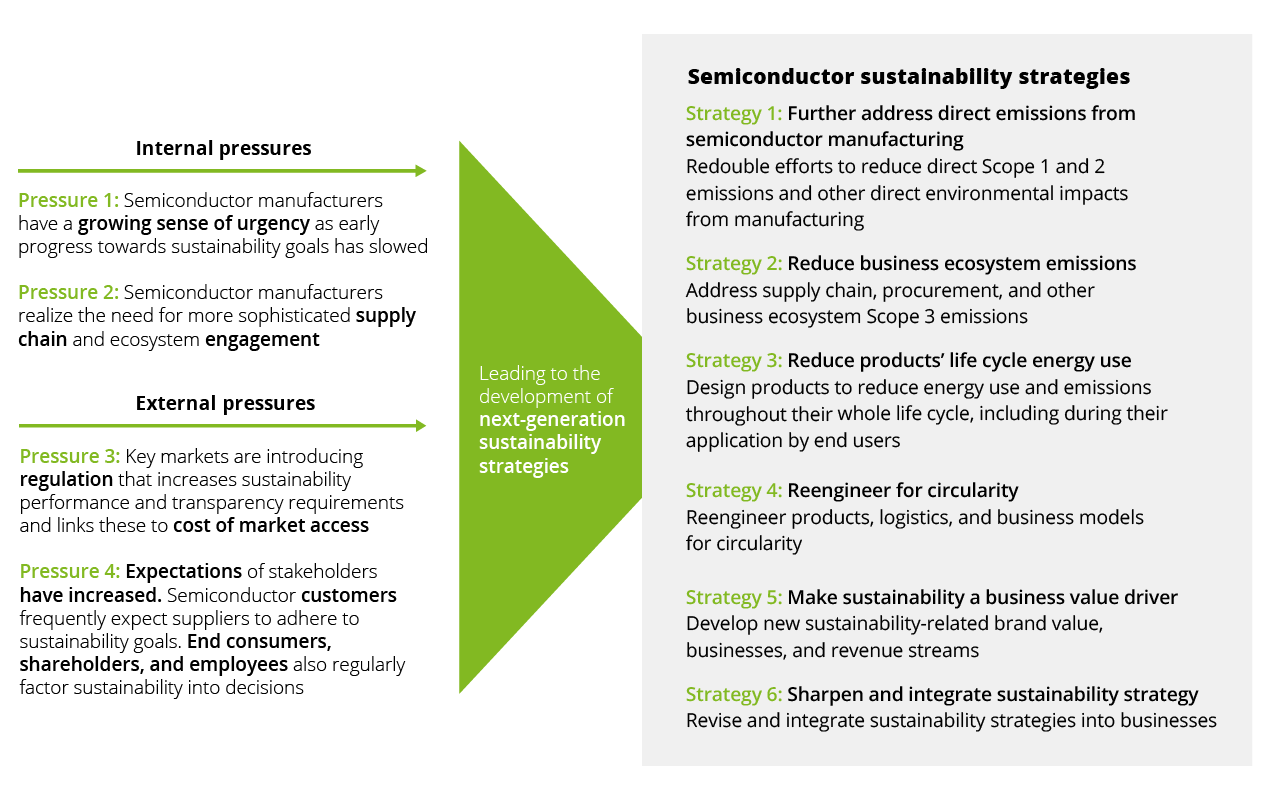

While the pressures toward increased sustainability in the semiconductor industry are many and various, we see them coalescing around four dominant drivers:

- Driver 1: Learned experience

From an internal perspective, many leading semiconductor companies announced sustainability goals several years ago, and enough time has passed that they are now able to take stock of early lessons in pursuing those objectives. - Driver 2: Ecosystem management

Recent shocks to supply chain security and shifting geopolitics have forced many semiconductor businesses to become more sophisticated in managing and engaging their broader industry ecosystem. This has been motivated by factors including the need to better understand and manage sustainability, as well as the need for greater supply chain resilience in support of business continuity. - Driver 3: Regulation

External to individual semiconductor companies, with clear leadership from European regulators, regulation of both capital and product markets now provides a clear sense of direction and standard-setting, thus providing increased clarity to the industry in the standards that need to be attained and reinforcing the need for a clear pathway to net-zero emissions. - Driver 4: Expectations

Additional stakeholders, including direct customers and end-consumers, staff, and capital providers have become much more sophisticated in their understanding of the direct and embedded sustainability challenges of semiconductor products and are increasingly likely to factor this understanding into their decisions related to the sector. Sustainability is becoming a significant differentiating factor in semiconductor companies’ brands.

How are semiconductor companies responding to these drivers?

We see six dominant strategies in how companies are currently responding to these drivers

Next-generation sustainability strategies:

Across the breadth of our engagement in the sector, we see six dominant strategies in how semiconductor companies are currently responding to these pressures to address their sustainability footprint:

Strategy #1: Further addressing the direct emissions from semiconductor manufacturing

With many semiconductor companies having declared emissions reduction goals several years ago, some progress and sense of direction has generally been achieved in reducing “Scope 1 and 2” emissions. (Scope 1 emissions are from sources directly owned by an organization, while Scope 2 emissions result from its purchase of energy). Opportunities invariably remain to further reduce environmental and social impacts, and climate emissions, from fabrication, assembly, and distribution operations as well as from energy sourcing. Having by-and-large addressed the easier initiatives such as facilities energy efficiency and purchasing of renewable energy supplies, semiconductor companies are redoubling efforts to reduce “Scope 1” emissions and other direct environmental impacts that result from their core fabrication and packaging operations.

Strategy #2: Reducing “Scope 3” business ecosystem and procurement emissions

In addition to furthering progress in reducing the direct Scope 1 emissions from their own manufacturing processes, leaders are now turning serious attention toward addressing the more difficult to control “Scope 3” emissions category. This requires deeper engagement of the supplier ecosystem, coordinating commitments, incentives, and actions to reduce emissions throughout the web of corporations and facilities which participate in the design-source-fabricate-test-assemble-distribute chain – as well as during product use and at end-of-life. An example of this is the proposed collaboration by a global semiconductor equipment company, between engineers and procurement teams, to define emissions-focused metrics and criteria for supplier selection.2 These efforts often go hand-in-hand with the objective of strengthening supply chain resilience and the resulting business continuity. Fortunately, advancement of mechanisms such as carbon insetting (reducing carbon within your own supply chain) markets and supply chain management capabilities have made Scope 3 emissions reduction more achievable now than ever before.

Strategy #3: Designing products to reduce energy use and emissions throughout their life cycle

The demand for semiconductor technology continues to grow over the longer term, driven by electrification in less developed countries and the proliferation of applications such as cloud computing, 5G communications and artificial intelligence in advanced economies. Without significant gains in the energy efficiency of computing power, direct and indirect emissions from the sector will likely grow as well. To reduce emissions and meet sustainability priorities of their customers, semiconductor manufacturers face intense pressure to develop highly efficient chips that reduce the energy consumption of the products into which they are incorporated. For instance, a large memory company recently announced the development of ultra-low power memory chips that aim to significantly reduce the annual power consumption of memory products used in data centers and mobile devices.

Strategy #4: Reengineering products, logistics and business models for circularity

The environmental and social footprint of raw materials essential to semiconductor products, as well as growing uncertainty in their long-term availability, is now well understood. These raw materials include minerals, gases, chemicals, as well as spare parts for semiconductor equipment and consumables. The challenge of acceptably disposing of semiconductor products at end-of-life is also a growing concern of both business and consumer end-users.

Achieving better environmental performance and supply chain resilience demands new approaches to semiconductor products’ end of life. Successful efforts to improve reusability and recyclability of semiconductor components are beginning to be incentivized by pricing differentials in consumer and secondhand markets, as evidenced by the creation of Trade-In programs by large consumer tech companies, to provide financial incentives to customers while reusing and/or recycling valuable materials Manufacturers have also recognized material reuse as an essential capability for business longevity amidst growing uncertainty around finite (or politically acceptable/reliable) mineral supplies. This has implications for semiconductor design, manufacture, marketing, and logistics/reverse logistics that companies are increasingly addressing. For instance, semiconductor companies have been partnering with industry actors to launch product takeback pilots, as well as pilots to reuse materials traditionally treated like waste, such as scrap magnets in Hard Disk Drives (HDDs)

Strategy #5: Developing new, sustainability-related businesses and revenue streams

Semiconductor companies are exploring ways to harness consumer and corporate demand for sustainable products as a value driver in both product and service markets. Estimates suggest that around 40% of carbon reductions needed to achieve Paris commitment goals will rely on new technologies, indicating significant market potential. In addition to entering carbon markets, leaders in semiconductor sustainability are creating new revenue streams such as emissions reduction advisory services, premium pricing for versions of their products with sustainable features such as use of recycled materials, and movement to “as a service” delivery of their products’ capabilities which can reduce energy and transportation impacts while generating service-related revenue.

Strategy #6: Sharpening sustainability strategies and integrating them into the business

In addition to pursuing individual sustainability strategies such as those summarized above, we are increasingly finding that as semiconductor corporations learn from both the successes and challenges in their sustainability journey, they are now sharpening their strategies against more rigorous goal setting and reporting expectations, clearer and more stringent regulatory compliance requirements (e.g. CSRD in Europe, California bills SG-253 and SB-261, and the proposed SEC climate rule), and the opportunity for greater integration of social and environmental sustainability objectives into the goals and plans of leadership and business units. Semiconductor leaders who have successfully undertaken initial sustainability efforts are revisiting the aspirations and governance of their sustainability programs, perhaps in preparation for meeting the higher expectations, and greater opportunities afforded in their product, employee and capital markets.

Take a deeper look at current trends and emerging strategies in our Semiconductor Sustainability series

In conclusion

With semiconductors playing an increasingly pervasive role in our lives and in the economy, progress toward sustainability throughout the semiconductor lifecycle – from design through manufacture, use and end-of-life treatment – is essential. The drivers and strategies outlined in this article summarize how sustainability pressures are manifesting in the industry, and how its leading actors are responding. In forthcoming articles of this series, we will delve deeper into the specific strategies we see being taken by semiconductor businesses in each of these areas.

Get in touch

Endnotes

1 S&P Global ESG industry report card: Technology, accessed October 2023.

2 International Energy Association, CO2 emissions reduction by type of abatement measure, 2050 (GTCO2-e, %).

Recommendations

Semiconductor | Deloitte US

Deloitte's semiconductor consulting practice can solve critical issues. Explore semiconductor industry trends, from M&A to cloud to IoT, to help drive growth.